CVD Coating Machine Market

CVD Coating Machine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708975 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

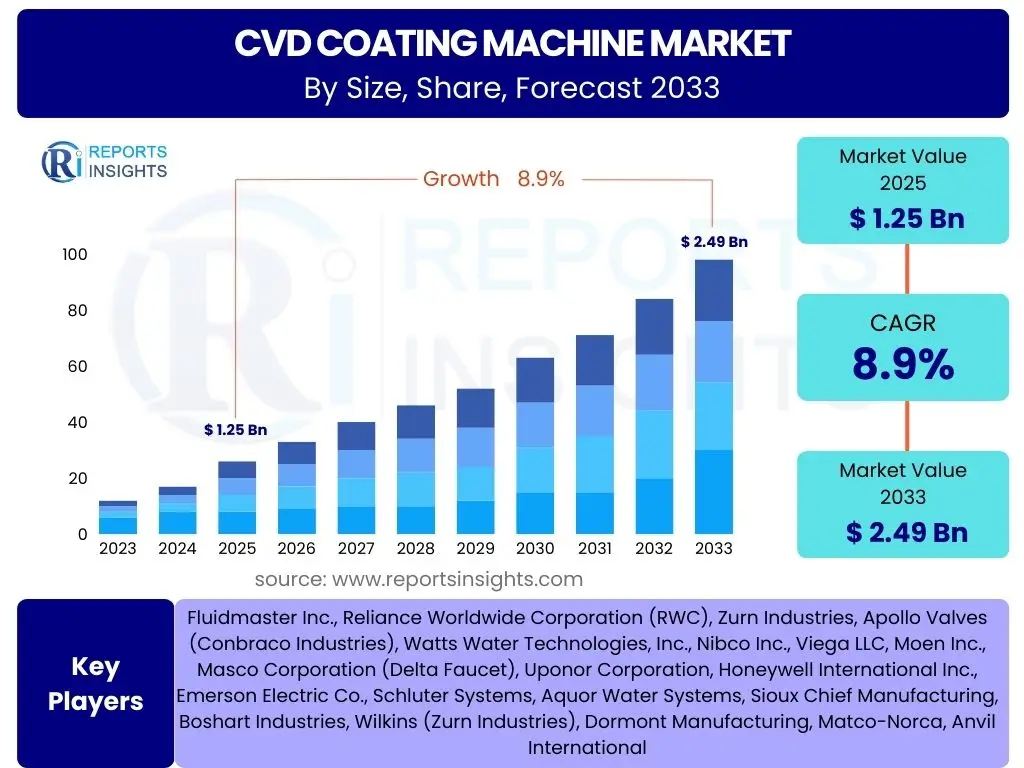

CVD Coating Machine Market Size

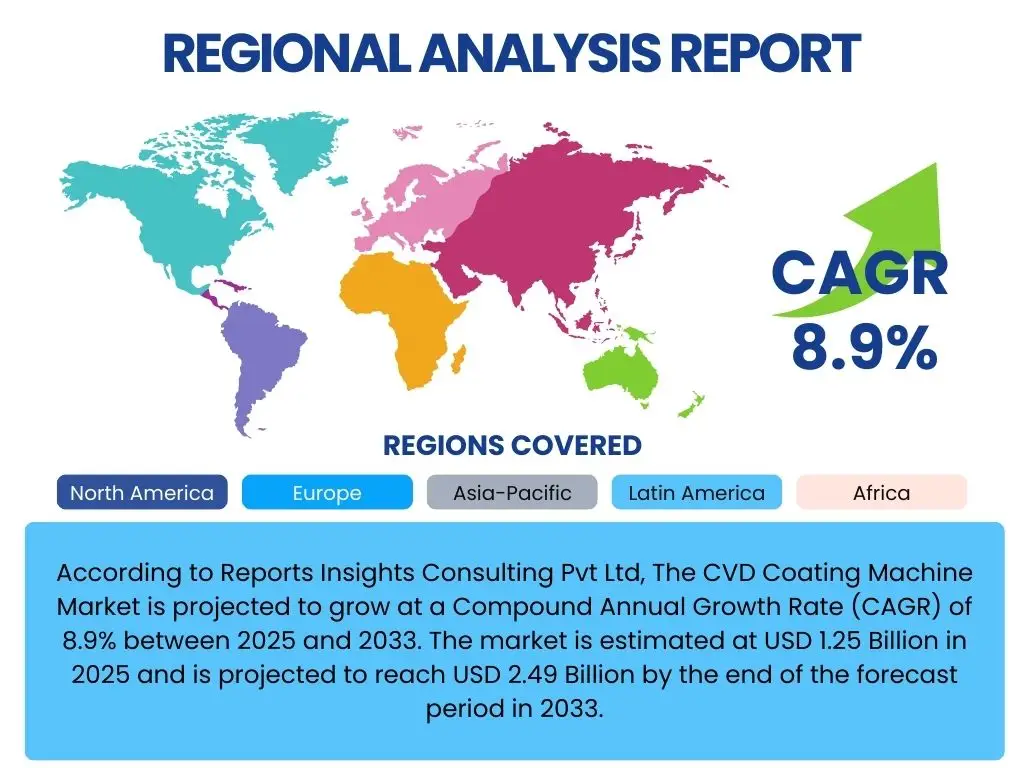

According to Reports Insights Consulting Pvt Ltd, The CVD Coating Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.49 Billion by the end of the forecast period in 2033.

Key CVD Coating Machine Market Trends & Insights

User inquiries frequently revolve around the technological advancements and application expansion driving the CVD Coating Machine market. Key themes include the push for enhanced material properties, the demand for more efficient and precise deposition processes, and the integration of smart manufacturing principles. Users are keen to understand how these factors are shaping the evolution of CVD technology, particularly in high-growth sectors like semiconductors and advanced materials, and how these trends contribute to the overall market trajectory and competitive landscape.

The market is witnessing a significant shift towards more sophisticated coating solutions that offer superior performance and durability. This includes the development of multi-layer and nano-coatings, enabling enhanced functionality for components across various industries. Furthermore, there is a growing emphasis on environmentally friendly and cost-effective CVD processes, addressing both regulatory pressures and operational efficiencies, which are crucial for market adoption and sustained growth.

- Miniaturization and complex geometries demand: Driving innovation in precise and conformal coating capabilities for micro-electronic components and intricate mechanical parts.

- Development of advanced materials: Increasing adoption of new substrates and a broader range of coating materials (e.g., graphene, ceramics, composites) requiring specialized CVD processes.

- Automation and process integration: Enhanced automation features and integration with Industry 4.0 technologies for improved throughput, consistency, and reduced human intervention.

- Sustainable and eco-friendly processes: Growing focus on reducing waste, energy consumption, and the use of hazardous precursors in CVD operations.

- Demand for multi-functional coatings: Development of coatings with combined properties such as wear resistance, corrosion protection, thermal insulation, and biocompatibility.

- Expansion in renewable energy applications: Increased use of CVD for coatings in solar cells, fuel cells, and energy storage devices.

AI Impact Analysis on CVD Coating Machine

Common user questions regarding AI's influence on CVD Coating Machines center on how artificial intelligence can enhance process control, optimize material properties, and reduce operational costs. Users are particularly interested in AI's role in predictive maintenance, real-time quality assurance, and the development of new coating recipes. The overarching expectation is that AI integration will lead to more efficient, reliable, and adaptable CVD systems, pushing the boundaries of what is currently achievable in thin-film deposition.

The application of AI in CVD processes marks a significant technological leap, enabling the systems to learn from vast datasets of process parameters, material characteristics, and output quality. This capability allows for dynamic adjustments to process variables, leading to superior coating uniformity, adhesion, and overall performance. AI-driven models can identify optimal operating conditions much faster and more accurately than traditional empirical methods, accelerating research and development cycles and improving manufacturing yields.

- Predictive maintenance: AI algorithms analyze operational data to forecast equipment failures, minimizing downtime and optimizing maintenance schedules.

- Process optimization and control: Machine learning models optimize parameters like temperature, pressure, and gas flow in real-time, leading to improved coating quality, uniformity, and efficiency.

- Real-time quality assurance: AI-powered vision systems and sensors detect defects or inconsistencies during deposition, enabling immediate corrective actions and reducing scrap rates.

- Accelerated material discovery: AI assists in simulating and predicting the properties of new coating materials and their deposition characteristics, speeding up R&D.

- Autonomous recipe generation: AI can learn from past successful coating recipes and automatically generate new ones for specific application requirements, reducing manual experimentation.

- Energy efficiency optimization: AI monitors energy consumption patterns and suggests adjustments to reduce power usage during CVD processes.

Key Takeaways CVD Coating Machine Market Size & Forecast

User queries frequently highlight the most critical insights derived from the CVD Coating Machine market's size and forecast, focusing on the future growth trajectory, market drivers, and the most promising opportunities. They seek a concise summary of the market's health, areas of significant investment, and the primary factors that will dictate its expansion. The key takeaway is the market's robust growth, propelled by the escalating demand for advanced materials and sophisticated coating solutions across diverse high-tech industries.

The sustained expansion of the semiconductor industry, coupled with the increasing adoption of CVD technology in sectors like aerospace, medical devices, and renewable energy, underpins this positive outlook. Technological advancements, particularly in areas like AI-driven process optimization and the development of novel coating materials, are crucial in overcoming existing challenges and unlocking new application areas. This robust growth trajectory signifies significant opportunities for both established players and new entrants specializing in innovative CVD solutions.

- Robust Market Growth: The CVD Coating Machine Market is set for substantial growth, driven by technological advancements and expanding application bases.

- Semiconductor Industry Dominance: The semiconductor sector remains the primary growth engine, with increasing demand for smaller, more powerful, and durable components.

- Diversification of Applications: Significant growth is anticipated in non-semiconductor fields, including advanced materials, medical technology, aerospace, and solar energy.

- Technological Innovation as a Catalyst: Continuous R&D in areas like AI integration, new material deposition, and process efficiency is vital for market expansion.

- Asia Pacific Leads Expansion: The APAC region is expected to maintain its leading position due to extensive manufacturing capabilities and increasing industrialization.

- Strategic Investments: Companies are focusing on investments in automation, sustainability, and high-performance coating solutions to gain a competitive edge.

CVD Coating Machine Market Drivers Analysis

The CVD Coating Machine market is significantly propelled by the increasing demand for high-performance materials and advanced functional coatings across various industries. As manufacturing processes become more sophisticated and product specifications more stringent, the need for precise, durable, and customized thin films has escalated. This demand is particularly evident in sectors requiring components with enhanced wear resistance, corrosion protection, electrical insulation, or specific optical properties, which CVD technology is uniquely capable of delivering.

Furthermore, the miniaturization trend in electronics and the continuous innovation in semiconductor manufacturing are powerful drivers. The intricate architectures and complex multi-layer structures of modern electronic devices necessitate advanced deposition techniques that can achieve ultra-thin, conformal, and highly uniform coatings. CVD machines are indispensable in producing these critical layers, ensuring the reliability and performance of next-generation microprocessors, memory chips, and other semiconductor components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Advanced Materials & Coatings | +2.1% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 |

| Growth in the Semiconductor and Electronics Industry | +2.5% | Asia Pacific (China, Taiwan, South Korea, Japan), North America (USA) | 2025-2033 |

| Miniaturization of Electronic Devices | +1.8% | Global, with strong impact in developed and emerging tech hubs | 2025-2033 |

| Rising Adoption in Aerospace & Defense | +1.2% | North America, Europe | Mid to Long-term |

| Expansion of Solar Energy and Renewable Sector | +1.3% | Asia Pacific (China, India), Europe, North America | 2025-2033 |

CVD Coating Machine Market Restraints Analysis

Despite the robust growth prospects, the CVD Coating Machine market faces several significant restraints, notably the high initial capital investment required for acquiring and installing these sophisticated systems. The cost of CVD equipment, coupled with the expenses associated with facility setup, specialized infrastructure, and precursor materials, can be prohibitive for smaller companies or new market entrants. This high barrier to entry limits market participation and can slow down the adoption of CVD technology in industries with tighter budget constraints.

Another key restraint is the operational complexity and the need for highly skilled personnel to operate and maintain CVD machines. The precise control over numerous parameters such as temperature, pressure, gas flow rates, and precursor chemistry demands specialized expertise. A shortage of trained engineers and technicians capable of managing these intricate processes can impede efficient operation and lead to higher operational costs, posing a challenge to wider market expansion, especially in regions with developing technical skill bases.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.5% | Global, particularly SMEs in developing regions | 2025-2030 |

| Operational Complexity & Need for Skilled Personnel | -1.2% | Global, especially emerging economies | 2025-2033 |

| Availability and Cost Volatility of Precursor Materials | -0.8% | Global, impacting supply chains | Short to Mid-term |

| Environmental Concerns & Regulatory Compliance | -0.7% | Europe, North America, increasingly Asia Pacific | Long-term |

| High Energy Consumption of Certain CVD Processes | -0.6% | Global, particularly in regions with high energy costs | 2025-2033 |

CVD Coating Machine Market Opportunities Analysis

Significant opportunities in the CVD Coating Machine market emerge from the burgeoning demand for specialized coatings in rapidly evolving industries such as electric vehicles, advanced medical devices, and renewable energy. The electric vehicle sector, for instance, requires high-performance coatings for batteries, power electronics, and structural components to enhance efficiency, durability, and safety. Similarly, medical devices benefit from biocompatible, wear-resistant, and anti-corrosive coatings applied via CVD, opening new avenues for market expansion.

Furthermore, continuous research and development in novel materials and deposition techniques present substantial growth opportunities. The exploration of new precursors, hybrid CVD processes, and additive manufacturing integration can unlock unprecedented capabilities in creating multi-functional and tailor-made coatings. These innovations not only expand the addressable market for CVD technology but also position it as a critical enabler for future technological advancements across a multitude of applications, from flexible electronics to advanced optics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Applications in EV, Medical, & Optics | +1.9% | Global, particularly developed economies | 2025-2033 |

| Advancements in Precursor Chemistry & Hybrid CVD Processes | +1.5% | Global, R&D focused regions (North America, Europe, Japan) | 2027-2033 |

| Growing Investment in R&D for Nanotechnology & Advanced Materials | +1.3% | Global, academic and industrial research hubs | Long-term |

| Increased Adoption in Developing Economies' Industrial Sectors | +1.0% | Asia Pacific (India, Southeast Asia), Latin America | Mid to Long-term |

| Integration with Additive Manufacturing (3D Printing) | +0.9% | Global, across high-value manufacturing sectors | 2028-2033 |

CVD Coating Machine Market Challenges Impact Analysis

The CVD Coating Machine market encounters several notable challenges, including the complexities associated with process scalability and maintaining uniformity for large-area or high-volume production. Achieving consistent coating quality and thickness across large substrates or a multitude of small components simultaneously remains a significant technical hurdle. Variations in temperature, gas flow, and pressure within the reaction chamber can lead to inconsistencies, which are unacceptable in critical applications like semiconductors or optical coatings, thus impacting yield and production costs.

Another persistent challenge is the management of hazardous precursor materials and the byproducts generated during the CVD process. Many commonly used precursor gases are toxic, corrosive, or pyrophoric, necessitating stringent safety protocols, specialized handling equipment, and complex waste treatment systems. Adherence to increasingly strict environmental regulations regarding emissions and waste disposal adds to operational costs and complexity, posing a significant hurdle for manufacturers and users of CVD technology to ensure both worker safety and ecological compliance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Process Scalability & Uniformity for Large Areas | -1.0% | Global, affecting high-volume manufacturing | 2025-2033 |

| Management of Hazardous Precursors & Byproducts | -0.9% | Global, under increasing regulatory scrutiny | 2025-2033 |

| Intellectual Property & Patent Landscape Complexity | -0.7% | North America, Europe, Asia Pacific (competitive regions) | Long-term |

| High Research & Development Costs for New Materials | -0.6% | Global, impacting market entry and innovation | 2025-2033 |

| Economic Volatility and Supply Chain Disruptions | -0.5% | Global, short to mid-term impact | Short to Mid-term |

CVD Coating Machine Market - Updated Report Scope

This report provides an in-depth analysis of the global CVD Coating Machine market, meticulously examining market dynamics, segmentation, and regional trends to offer a comprehensive outlook from 2025 to 2033. It encompasses a detailed assessment of market size, growth drivers, restraints, opportunities, and challenges, along with the impact of emerging technologies like Artificial Intelligence. The scope extends to profiling key market players, presenting their strategies, product portfolios, and recent developments, thereby providing stakeholders with actionable insights for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.49 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials Inc., AIXTRON SE, ASM International N.V., Tokyo Electron Limited, Veeco Instruments Inc., CVD Equipment Corporation, SPTS Technologies Ltd. (KLA Corporation), Oxford Instruments plc, Samco Inc., centrotherm international AG, Ulvac, Inc., IHI Corporation, Kokusai Electric Corporation, Bühler AG, Plasma-Therm LLC, Lam Research Corporation, SENTECH Instruments GmbH, Picosun Oy, Beneq Oy, Jusung Engineering Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The CVD Coating Machine market is comprehensively segmented to provide a granular understanding of its diverse landscape and growth dynamics. This segmentation is crucial for identifying key trends, competitive advantages, and market opportunities across various technological types, specific applications, and end-user industries. Analyzing these segments helps stakeholders understand which technologies are gaining traction, where demand is highest, and how different industry verticals are adopting CVD solutions to meet their evolving material and performance requirements.

- By Type:

- Chemical Vapor Deposition (CVD)

- Plasma Enhanced Chemical Vapor Deposition (PECVD)

- Low-Pressure Chemical Vapor Deposition (LPCVD)

- Atmospheric Pressure Chemical Vapor Deposition (APCVD)

- Metal-Organic Chemical Vapor Deposition (MOCVD)

- Photo-Assisted Chemical Vapor Deposition (PACVD)

- High-Density Plasma Chemical Vapor Deposition (HDPCVD)

- Atomic Layer Deposition (ALD)

- By Application:

- Semiconductor Manufacturing

- Solar Cell Manufacturing

- Medical Devices

- Optical Coatings

- Tool & Die Coatings

- Aerospace Components

- Automotive Components

- Consumer Electronics

- Energy Storage

- By End-User:

- Electronics & Semiconductor

- Healthcare

- Automotive

- Aerospace & Defense

- Energy

- Industrial Tools

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to the robust presence of semiconductor manufacturing hubs, extensive electronics production, and significant government investments in advanced materials research in countries like China, South Korea, Taiwan, and Japan. This region is a major consumer and producer of CVD equipment.

- North America: A leading region for innovation and R&D in CVD technology, particularly in aerospace, defense, and high-end electronics. The presence of major technology companies and research institutions drives the adoption of advanced CVD solutions.

- Europe: Characterized by strong growth in the automotive, industrial tools, and medical device sectors. Countries like Germany, France, and the UK are investing in advanced manufacturing technologies, fostering demand for precision coating solutions.

- Latin America: Expected to show steady growth, driven by increasing industrialization and foreign direct investments in manufacturing, particularly in automotive and electronics assembly, though from a smaller base.

- Middle East and Africa (MEA): Emerging market with growing investments in industrial diversification, energy infrastructure, and, to a lesser extent, electronics manufacturing, leading to a gradual adoption of CVD coating technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the CVD Coating Machine Market.- Applied Materials Inc.

- AIXTRON SE

- ASM International N.V.

- Tokyo Electron Limited

- Veeco Instruments Inc.

- CVD Equipment Corporation

- SPTS Technologies Ltd. (KLA Corporation)

- Oxford Instruments plc

- Samco Inc.

- centrotherm international AG

- Ulvac, Inc.

- IHI Corporation

- Kokusai Electric Corporation

- Bühler AG

- Plasma-Therm LLC

- Lam Research Corporation

- SENTECH Instruments GmbH

- Picosun Oy

- Beneq Oy

- Jusung Engineering Co., Ltd.

Frequently Asked Questions

What is a CVD Coating Machine?

A CVD Coating Machine is specialized equipment used to deposit thin films of various materials onto substrates through a chemical process. It involves exposing the substrate to volatile precursors, which react and/or decompose on the substrate surface to form the desired solid coating.

What are the primary applications of CVD technology?

CVD technology is primarily applied in semiconductor manufacturing for creating insulation and conductive layers, in solar cell production, for enhancing the durability of medical devices and industrial tools, and in aerospace components for corrosion and wear resistance.

How does AI impact the efficiency of CVD Coating Machines?

AI significantly enhances CVD efficiency by enabling predictive maintenance, optimizing process parameters in real-time for improved coating quality and uniformity, accelerating material discovery, and automating recipe generation, leading to reduced downtime and increased yields.

What are the key drivers for the CVD Coating Machine market growth?

Key drivers include the escalating demand for advanced materials and high-performance coatings, the rapid expansion and miniaturization trends in the semiconductor and electronics industries, and the increasing adoption of CVD in emerging applications like electric vehicles and medical devices.

What types of CVD processes are commonly used?

Common CVD processes include Plasma Enhanced CVD (PECVD), Low-Pressure CVD (LPCVD), Atmospheric Pressure CVD (APCVD), Metal-Organic CVD (MOCVD), and Atomic Layer Deposition (ALD), each suited for specific material types and application requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted