Cryocooler Market

Cryocooler Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709834 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

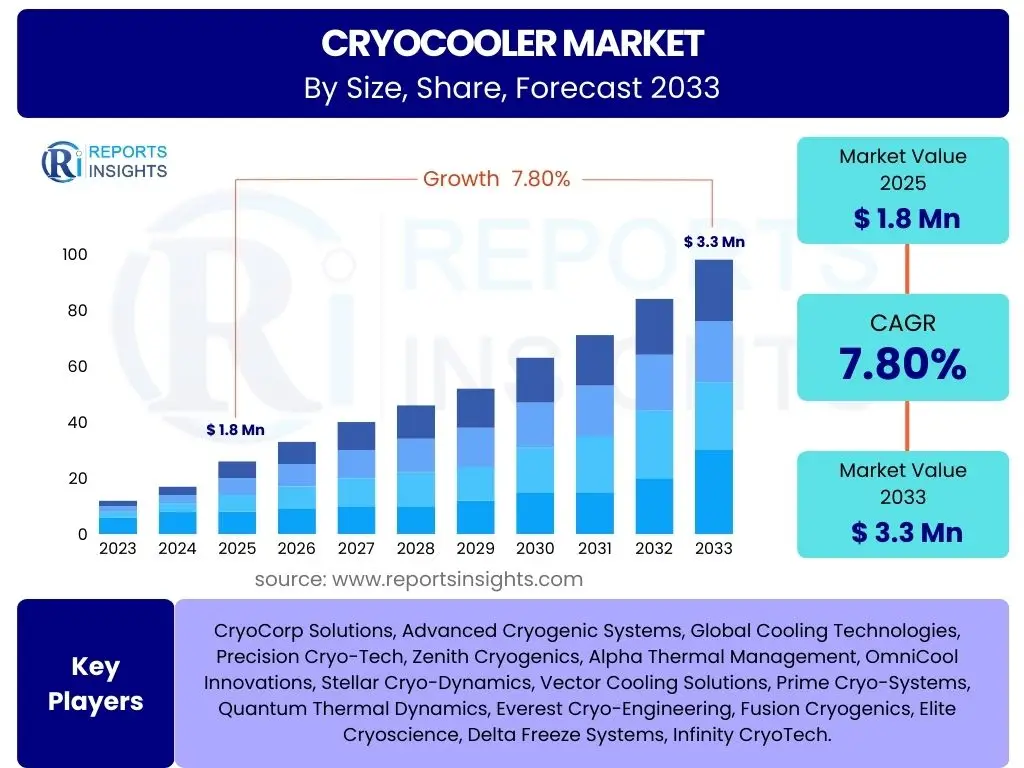

Cryocooler Market Size

According to Reports Insights Consulting Pvt Ltd, The Cryocooler Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 3.3 Billion by the end of the forecast period in 2033.

Key Cryocooler Market Trends & Insights

The cryocooler market is witnessing significant transformation driven by advancements in material science, energy efficiency requirements, and expanding applications across various high-tech sectors. Users frequently inquire about the emerging technologies enabling lower operating temperatures, reduced vibration, and enhanced reliability. There is a strong focus on miniaturization for integration into portable devices and increasingly complex scientific instruments, alongside the growing demand from quantum computing and space exploration which necessitate ultra-low temperature capabilities. These trends reflect a strategic shift towards more versatile, robust, and energy-efficient cooling solutions.

Furthermore, the integration of advanced control systems, including automation and remote monitoring, is becoming a pivotal aspect of modern cryocooler design. This evolution addresses the need for reduced manual intervention, improved system stability, and optimized performance in critical applications. The market is also seeing a rise in specialized cryocoolers tailored for specific niche applications, moving beyond general-purpose cooling, thereby fostering innovation in areas like high-temperature superconductivity and medical imaging. This specialization underscores the market's maturity and its responsiveness to diverse industrial and scientific requirements.

- Miniaturization and compact designs for portable and integrated systems.

- Increased demand from emerging applications such as quantum computing and advanced semiconductor manufacturing.

- Enhanced energy efficiency and reduced power consumption across various cryocooler types.

- Development of pulse tube cryocoolers for lower vibration and longer operational lifetimes.

- Growing adoption in space exploration, satellite technology, and infrared detection systems.

- Integration of smart monitoring and diagnostic features for predictive maintenance.

- Technological advancements in materials for improved cooling performance and reliability.

AI Impact Analysis on Cryocooler

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to revolutionize the cryocooler market by enhancing operational efficiency, predictive maintenance, and design optimization. User inquiries often highlight how AI can improve the control algorithms of cryocoolers, leading to more stable temperature regulation and reduced energy consumption. AI-driven analytics can process vast amounts of operational data, identifying subtle patterns indicative of impending failures, thereby enabling proactive maintenance and extending the lifespan of critical components. This shift towards intelligent cryocooling systems offers substantial benefits in terms of reliability and cost reduction, particularly in mission-critical applications where downtime is highly undesirable.

Beyond operational improvements, AI is also influencing the research and development phase of cryocooler technology. Machine learning algorithms can accelerate the discovery of novel materials with superior cryogenic properties, optimizing component design for better thermal performance and reduced size. Furthermore, AI can simulate complex thermodynamic processes, allowing engineers to virtually test and refine designs more rapidly and cost-effectively than traditional physical prototyping. This analytical capability is instrumental in pushing the boundaries of what cryocoolers can achieve, facilitating the development of systems capable of reaching even lower temperatures with greater efficiency and stability.

- AI-powered predictive maintenance for early fault detection and reduced downtime.

- Optimization of cryocooler control algorithms for enhanced temperature stability and efficiency.

- Machine learning for advanced material discovery and design optimization of components.

- AI-driven data analytics for performance monitoring and operational insights.

- Automated system calibration and self-correction for improved reliability.

- Simulation and modeling of cryogenic systems using AI to accelerate R&D.

- Integration with smart manufacturing processes for improved production quality.

Key Takeaways Cryocooler Market Size & Forecast

The cryocooler market is set for robust growth, driven by expanding applications in high-technology sectors and continuous innovation in cooling capabilities. User queries frequently seek to understand the primary drivers behind this growth, the most lucrative application areas, and the long-term outlook for investment and market expansion. The forecast indicates significant opportunities stemming from the increasing sophistication of scientific research, the burgeoning space economy, and the critical need for advanced thermal management in electronics and medical diagnostics. The consistent growth trajectory underscores the indispensable role cryocoolers play in enabling cutting-edge technological advancements and scientific discoveries.

Furthermore, a key takeaway is the increasing convergence of demand from both commercial and defense sectors, creating a diversified growth landscape. While traditional applications in military and defense continue to provide a stable demand base, the explosive growth in quantum computing, advanced scientific instrumentation, and next-generation medical devices is opening new, high-growth avenues. Manufacturers focusing on modularity, customizability, and integration capabilities are particularly well-positioned to capitalize on these trends, indicating a market that values adaptability and specialized solutions alongside core performance metrics.

- Strong growth projected, driven by increasing demand from quantum computing, space, and medical sectors.

- Technological advancements in efficiency, miniaturization, and reliability are crucial for market expansion.

- Asia Pacific is expected to emerge as a significant growth region due to industrialization and R&D investments.

- Pulse tube and Stirling cryocoolers are gaining traction due to lower vibration and improved longevity.

- Strategic partnerships and collaborations among market players will be key for innovation and market penetration.

- High-temperature superconductivity applications represent a substantial future opportunity.

Cryocooler Market Drivers Analysis

The cryocooler market is significantly propelled by the escalating demand for ultra-low temperature environments across a myriad of advanced technological applications. The proliferation of infrared (IR) detectors in defense, surveillance, and astronomy, for instance, critically relies on efficient cryocooling to achieve optimal sensitivity and performance. Similarly, the rapid advancements in medical diagnostics, including MRI systems, and the growing sophistication of scientific research in fields like material science and particle physics, necessitate precise and stable cryogenic temperatures. These sectors consistently drive innovation and adoption, demanding cryocoolers that are more compact, reliable, and energy-efficient.

Moreover, the burgeoning space economy and the intense global competition in quantum computing and high-performance computing are creating unprecedented demand for advanced cryocooling solutions. Space-borne instruments require robust cryocoolers capable of operating reliably in extreme conditions, while quantum computers need to maintain qubits at millikelvin temperatures for stable operation. These high-stakes applications not only drive volume but also push the boundaries of cryocooler technology in terms of cooling power, vibration reduction, and extended operational lifespans. The continuous investment in these cutting-edge fields acts as a powerful catalyst for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for IR detection and sensing in military and defense applications. | +1.5% | North America, Europe, Asia Pacific (China, India) | Short to Mid-Term |

| Rising adoption in medical devices such as MRI, SQUID, and cryosurgery. | +1.2% | North America, Europe, Asia Pacific (Japan, South Korea) | Mid to Long-Term |

| Expansion of space exploration and satellite technology requiring cryogenic systems. | +1.0% | USA, Europe (ESA), China, India | Mid to Long-Term |

| Advancements in quantum computing and high-performance computing. | +1.8% | Global, particularly USA, Europe, Japan | Long-Term |

| Increased R&D in material science and scientific research requiring ultra-low temperatures. | +0.8% | Global | Short to Mid-Term |

Cryocooler Market Restraints Analysis

Despite the robust growth drivers, the cryocooler market faces significant restraints that can impede its full potential. The high initial cost associated with the procurement and installation of advanced cryocooler systems is a primary barrier, particularly for small and medium-sized enterprises or research institutions with limited budgets. These systems often involve complex engineering, specialized materials, and precise manufacturing processes, all contributing to their elevated price point. This financial constraint can lead to longer adoption cycles and a preference for less sophisticated, albeit less efficient, cooling methods in certain applications.

Furthermore, the technical complexity and specialized maintenance requirements of cryocoolers pose another substantial restraint. Operating and maintaining these systems demand highly skilled personnel, which can be scarce and expensive to retain. The need for periodic maintenance, which often involves specialized tools and procedures to ensure optimal performance and longevity, adds to the operational expenditure. Additionally, vibration, noise generation, and the overall physical footprint of some larger cryocooler systems can limit their applicability in space-constrained or vibration-sensitive environments, creating design challenges for integration into compact or sensitive instrumentation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial cost of cryocooler systems. | -0.9% | Global, impacting developing economies more | Short to Mid-Term |

| Technical complexity and specialized maintenance requirements. | -0.7% | Global | Short to Mid-Term |

| Vibration and noise generation in certain cryocooler types. | -0.5% | Applications requiring high precision (e.g., quantum computing, space telescopes) | Short to Long-Term |

| Limitations in cooling capacity for certain ultra-large-scale applications. | -0.3% | Global | Mid to Long-Term |

Cryocooler Market Opportunities Analysis

The cryocooler market is ripe with opportunities driven by technological advancements, emerging applications, and geographical expansion. The continuous push towards miniaturization and enhanced energy efficiency presents significant avenues for innovation, allowing cryocoolers to be integrated into a wider range of compact and portable devices, such as handheld IR imagers and small-scale medical diagnostic tools. Developing more compact, lighter, and lower-power cryocoolers will unlock new market segments and increase adoption in areas where size and energy consumption are critical limiting factors, such as in drone-based remote sensing or advanced personal electronics.

Moreover, the explosive growth in quantum computing, which requires temperatures close to absolute zero, represents a monumental opportunity for specialized cryocooler solutions. As quantum technologies mature from research to commercial applications, the demand for highly reliable, ultra-low temperature systems will surge. Similarly, advancements in high-temperature superconductivity (HTS) and magnetic refrigeration offer novel avenues for cryocooler applications, potentially enabling more energy-efficient power transmission, advanced medical devices, and innovative transportation solutions. The expansion into emerging economies, particularly in Asia Pacific, where industrialization and scientific investments are rapidly increasing, also offers substantial market growth potential for cryocooler manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of compact and miniaturized cryocoolers for portable applications. | +1.3% | Global, with high demand in defense and medical fields | Short to Mid-Term |

| Emerging demand from quantum computing and related cryogenic electronics. | +1.6% | USA, Europe, Japan, China | Mid to Long-Term |

| Growth in the high-temperature superconductivity (HTS) market. | +0.8% | Global | Mid to Long-Term |

| Increased investment in R&D for advanced medical imaging and cryosurgery. | +0.9% | North America, Europe, Asia Pacific | Short to Mid-Term |

| Expansion into new geographical markets, especially developing economies. | +0.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-Term |

Cryocooler Market Challenges Impact Analysis

The cryocooler market faces several significant challenges that necessitate ongoing innovation and strategic adaptation from manufacturers. One critical challenge is the inherent complexity in achieving ultra-low temperatures with high efficiency and minimal power consumption, especially as demand grows for applications requiring temperatures approaching absolute zero. Balancing performance metrics such as cooling power, operating temperature, efficiency, reliability, and vibration suppression against the constraints of size, weight, and cost remains a complex engineering feat. Overcoming these technical hurdles requires continuous investment in research and development and the adoption of cutting-edge materials and design methodologies.

Furthermore, the highly specialized nature of the cryocooler industry often leads to a limited supply chain for specific components and a shortage of highly skilled technical personnel. The production of cryocoolers involves intricate manufacturing processes and relies on specialized expertise in thermodynamics, vacuum technology, and precision engineering. This can result in production bottlenecks, increased manufacturing costs, and difficulties in scaling up operations to meet surging demand. Navigating these supply chain vulnerabilities and addressing the talent gap are crucial for sustained growth and market stability, requiring strategic partnerships, vertical integration, and targeted educational initiatives to foster a skilled workforce.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving ultra-low temperatures with high efficiency and minimal power consumption. | -0.8% | Global, particularly in quantum and space applications | Short to Long-Term |

| Supply chain vulnerabilities for specialized components and materials. | -0.6% | Global | Short to Mid-Term |

| Shortage of skilled workforce for design, manufacturing, and maintenance. | -0.5% | Global | Short to Mid-Term |

| Intense competition and pricing pressures in established market segments. | -0.4% | Global | Short to Mid-Term |

| Disposal and environmental impact concerns of certain refrigerants or materials. | -0.2% | Europe, North America (due to stringent regulations) | Mid to Long-Term |

Cryocooler Market - Updated Report Scope

This report provides an in-depth analysis of the global Cryocooler market, offering comprehensive insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers a detailed forecast from 2025 to 2033, building upon historical data from 2019 to 2023, to present a holistic view of market evolution. The scope includes critical market attributes, growth drivers, restraints, opportunities, and challenges that shape the industry, aiming to provide stakeholders with actionable intelligence for strategic decision-making and investment planning. The analysis also incorporates the impact of emerging technologies and macroeconomic factors on market trajectories.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 3.3 Billion |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CryoCorp Solutions, Advanced Cryogenic Systems, Global Cooling Technologies, Precision Cryo-Tech, Zenith Cryogenics, Alpha Thermal Management, OmniCool Innovations, Stellar Cryo-Dynamics, Vector Cooling Solutions, Prime Cryo-Systems, Quantum Thermal Dynamics, Everest Cryo-Engineering, Fusion Cryogenics, Elite Cryoscience, Delta Freeze Systems, Infinity CryoTech. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cryocooler market is comprehensively segmented to provide a granular understanding of its diverse components and application areas, allowing for a detailed analysis of market dynamics within specific niches. This segmentation helps in identifying key growth drivers and restraints pertinent to each category, as well as emerging opportunities that may not be apparent from a broader market perspective. By breaking down the market based on type, cooling capacity, application, component, and end-user, stakeholders can gain a more precise view of where innovation is occurring and where investment opportunities lie, enabling more targeted strategic planning and product development.

Understanding these segments is crucial for manufacturers to tailor their product offerings, for investors to identify high-potential areas, and for researchers to focus on unmet needs. For instance, the distinction between Gifford-McMahon and Pulse Tube cryocoolers highlights differences in vibration characteristics and maintenance requirements, which are critical for applications like quantum computing versus industrial gas liquefaction. Similarly, analyzing the market by cooling capacity allows for insights into the demand for miniaturized systems for portable devices versus high-power systems for large-scale scientific facilities. This detailed approach ensures that the report captures the full complexity and diversity of the cryocooler landscape.

- By Type:

- Gifford-McMahon (GM)

- Pulse Tube (PT)

- Stirling

- Joule-Thomson (JT)

- Brayton

- Others (e.g., Sorption, Thermoacoustic)

- By Cooling Capacity:

- Less than 1W

- 1W-10W

- Greater than 10W

- By Application:

- Military & Defense (e.g., IR sensors, missile guidance, night vision)

- Space (e.g., satellite instrumentation, cryosatellites, astronomy)

- Medical & Healthcare (e.g., MRI, cryosurgery, SQUID devices)

- Research & Development (R&D) (e.g., particle physics, material science, superconductivity)

- Commercial (e.g., gas liquefaction, scientific instruments)

- Industrial (e.g., vacuum coating, semiconductor manufacturing)

- Semiconductor (e.g., wafer cooling, device testing)

- Energy (e.g., power transmission, energy storage)

- Others (e.g., environmental monitoring, food preservation)

- By Component:

- Compressor

- Cold Head

- Regenerator

- Heat Exchanger

- Motor

- Others (e.g., valves, seals)

- By End-User:

- Aerospace & Defense Sector

- Healthcare & Life Sciences

- Electronics & Semiconductor Industry

- Energy & Power Sector

- Research Institutions & Universities

- Chemical & Petrochemical Industry

- Automotive Industry

- Others

Regional Highlights

- North America: This region maintains a significant share in the cryocooler market, driven by robust defense spending, advanced medical infrastructure, and substantial investment in scientific research, particularly in the United States. The presence of leading technology companies and a strong ecosystem for quantum computing research further propels demand. Canada also contributes through its burgeoning aerospace and defense sector, alongside a focus on environmental and climate research requiring advanced sensing technologies. The region is characterized by early adoption of new cryogenic technologies and high R&D expenditure.

- Europe: Europe represents a mature and technologically advanced market for cryocoolers, with countries like Germany, the UK, and France at the forefront. The region benefits from strong government funding for scientific research, particularly in particle physics (e.g., CERN), space exploration (e.g., ESA), and medical technology innovation. Strict regulatory standards for energy efficiency and environmental impact also drive the development of more sustainable and high-performance cryocooler solutions. Eastern European countries are gradually increasing their adoption rates, particularly in industrial and research applications.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the cryocooler market, primarily due to rapid industrialization, increasing defense budgets, and significant investments in semiconductor manufacturing and scientific research in countries such as China, Japan, South Korea, and India. China's massive governmental initiatives in space programs, quantum technology, and advanced manufacturing are creating unprecedented demand. Japan and South Korea lead in advanced electronics and high-precision scientific instruments, while India's expanding healthcare sector and space missions are also contributing significantly to market expansion.

- Latin America: This region exhibits a nascent but growing cryocooler market, primarily driven by increasing investments in scientific research and a developing healthcare infrastructure in countries like Brazil and Mexico. The demand is often concentrated in public research institutions and large-scale industrial projects. While smaller in market share compared to other regions, opportunities are emerging as economic development and technological adoption accelerate across various sectors, including mining and energy, which are beginning to explore cryogenic applications.

- Middle East and Africa (MEA): The MEA region is characterized by steady growth in the cryocooler market, largely influenced by defense modernizations, investments in oil & gas exploration, and nascent advancements in healthcare and scientific research, particularly in countries like Saudi Arabia, UAE, and South Africa. The demand from military applications, especially for surveillance and infrared systems, is a significant driver. Furthermore, investments in renewable energy and scientific infrastructure development are expected to gradually open up new opportunities for cryogenic technologies in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cryocooler Market.- CryoCorp Solutions

- Advanced Cryogenic Systems

- Global Cooling Technologies

- Precision Cryo-Tech

- Zenith Cryogenics

- Alpha Thermal Management

- OmniCool Innovations

- Stellar Cryo-Dynamics

- Vector Cooling Solutions

- Prime Cryo-Systems

- Quantum Thermal Dynamics

- Everest Cryo-Engineering

- Fusion Cryogenics

- Elite Cryoscience

- Delta Freeze Systems

- Infinity CryoTech

- Universal Cryogenics

- Pioneer Cryo-Engineers

Frequently Asked Questions

What is a cryocooler and what are its primary applications?

A cryocooler is a refrigeration device that cools an object to cryogenic temperatures, typically below 120 Kelvin (-153 degrees Celsius or -243 degrees Fahrenheit). Its primary applications include cooling infrared sensors for military and space, maintaining superconducting magnets in MRI machines, enabling quantum computing, and facilitating various scientific research experiments in material science and particle physics. They are crucial for technologies requiring extremely low temperatures to operate effectively or precisely.

How do cryocoolers differ from traditional refrigeration systems?

Cryocoolers differ from traditional refrigeration systems primarily in their operating temperature range and design principles. Traditional refrigerators typically achieve temperatures down to a few degrees below freezing (around -20°C), while cryocoolers are designed to reach ultra-low temperatures, often below -150°C, and sometimes even millikelvin ranges. They utilize specialized thermodynamic cycles (like Gifford-McMahon, Stirling, or Pulse Tube) and working fluids (like helium) to achieve these extreme cold temperatures, often with precision temperature control not seen in conventional cooling.

What are the key types of cryocoolers available in the market?

The key types of cryocoolers available in the market include Gifford-McMahon (GM), Pulse Tube (PT), Stirling, Joule-Thomson (JT), and Brayton cryocoolers. GM cryocoolers are known for their high cooling capacity and reliability. Pulse tube cryocoolers offer very low vibration and long operational lifetimes. Stirling cryocoolers are compact and efficient, suitable for various applications. Joule-Thomson cryocoolers are often used for extremely low temperatures, while Brayton cryocoolers are typically for larger-scale industrial applications due to their high cooling power.

Which factors are driving the growth of the cryocooler market?

The cryocooler market growth is primarily driven by the escalating demand for advanced cooling solutions in key sectors. These include the expanding military and defense sector for infrared detection, significant investments in space exploration and satellite technology, the increasing adoption of cryocoolers in medical devices like MRI systems, and the rapid advancements in quantum computing and scientific research requiring ultra-low temperatures. Miniaturization and energy efficiency advancements also contribute significantly to this growth by broadening the applicability of cryocoolers.

What role does Asia Pacific play in the global cryocooler market?

Asia Pacific plays a crucial role in the global cryocooler market and is anticipated to be the fastest-growing region. This growth is fueled by rapid industrialization, substantial government investments in scientific research and development, and increasing defense expenditures in countries such as China, India, Japan, and South Korea. The region's expanding semiconductor manufacturing industry, coupled with significant advancements in space programs and quantum technology research, creates robust demand for diverse cryocooler solutions, positioning APAC as a key hub for future market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted