Credit Risk Rating Software Market

Credit Risk Rating Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702374 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Credit Risk Rating Software Market Size

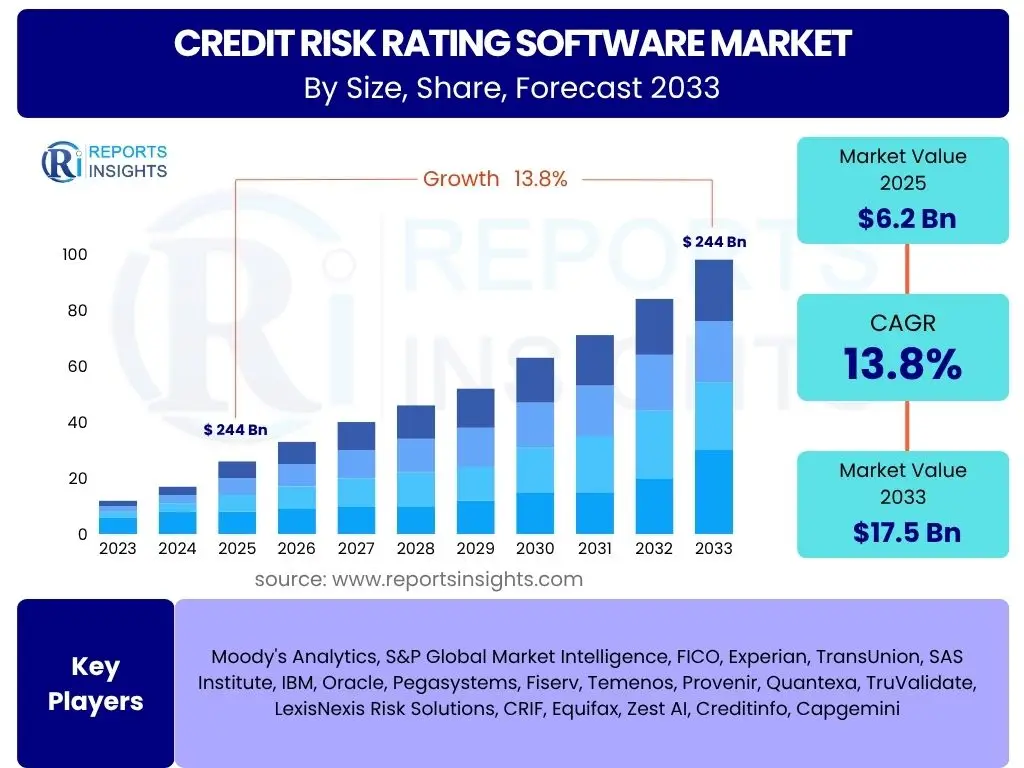

According to Reports Insights Consulting Pvt Ltd, The Credit Risk Rating Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 17.5 Billion by the end of the forecast period in 2033. This growth is primarily driven by the increasing need for robust risk management solutions in a volatile global economic landscape and the accelerating digital transformation within the financial sector. Organizations are actively seeking advanced software to enhance their assessment capabilities, ensure regulatory compliance, and mitigate potential financial losses.

The expansion of the market is also significantly influenced by the proliferation of big data and the advent of sophisticated analytical tools. Financial institutions, ranging from large banks to agile fintech startups, are investing heavily in technologies that can provide accurate, real-time insights into creditworthiness. This enables them to make more informed lending decisions, optimize portfolios, and better understand their exposure to various risks. The demand for scalable and adaptable credit risk rating software continues to rise as businesses navigate complex regulatory frameworks and strive for greater operational efficiency.

Key Credit Risk Rating Software Market Trends & Insights

The Credit Risk Rating Software market is undergoing significant transformation driven by technological advancements and evolving regulatory landscapes. Common user inquiries often revolve around the integration of artificial intelligence and machine learning, the shift towards cloud-based solutions, and the increasing demand for real-time data analytics. Users are also keen on understanding how these solutions address compliance mandates and enhance overall risk mitigation strategies.

Another area of focus for users is the emphasis on explainable AI (XAI) within credit risk models, as financial institutions strive for transparency and auditability. The market is witnessing a surge in customized solutions tailored to specific industry verticals, moving beyond one-size-fits-all approaches. Furthermore, the rising awareness of environmental, social, and governance (ESG) factors is influencing credit risk assessments, prompting software providers to incorporate these metrics into their platforms.

- Increased adoption of Artificial Intelligence (AI) and Machine Learning (ML) for enhanced accuracy and predictive capabilities.

- Growing preference for cloud-based Credit Risk Rating Software due to scalability, cost-efficiency, and accessibility.

- Demand for real-time credit risk analytics to facilitate faster and more agile decision-making.

- Integration of alternative data sources (e.g., social media, behavioral data) for more comprehensive credit assessments.

- Emphasis on Explainable AI (XAI) to ensure transparency and compliance with regulatory requirements.

- Rising importance of Environmental, Social, and Governance (ESG) factors in credit risk evaluations.

- Shift towards highly customizable and modular software solutions to meet diverse institutional needs.

AI Impact Analysis on Credit Risk Rating Software

Common user questions regarding AI's impact on Credit Risk Rating Software frequently center on its ability to revolutionize traditional credit assessment methodologies. Users are interested in how AI can process vast quantities of data more efficiently than conventional methods, leading to more precise risk predictions. There is a strong expectation that AI will significantly reduce manual effort, automate routine tasks, and enable financial institutions to identify subtle patterns that human analysts might miss, thereby enhancing the overall accuracy and speed of credit evaluations.

While the benefits are clear, users also express concerns about the ethical implications of AI, potential algorithmic bias, and the challenge of model explainability, particularly in a highly regulated environment. The desire for transparent and auditable AI models, often referred to as Explainable AI (XAI), is a recurring theme, as institutions need to justify their lending decisions. Furthermore, questions arise regarding data privacy, the integration complexity of AI systems with existing infrastructure, and the need for skilled personnel to manage and interpret AI-driven insights, underscoring a dual focus on innovation and responsible deployment.

- Enhanced Accuracy and Predictive Power: AI/ML algorithms analyze complex datasets, identifying intricate patterns for more accurate risk scoring.

- Automation of Credit Assessment: AI automates data collection, processing, and preliminary analysis, significantly reducing manual effort and processing time.

- Integration of Alternative Data: AI enables the seamless incorporation and analysis of non-traditional data sources, providing a holistic view of creditworthiness.

- Real-time Risk Monitoring: AI-powered systems offer continuous, real-time monitoring of credit portfolios, allowing for dynamic risk adjustments.

- Improved Fraud Detection: AI algorithms are highly effective at identifying unusual patterns indicative of fraudulent activities in credit applications.

- Personalized Credit Products: AI facilitates the development of highly customized credit offerings by precisely segmenting customer risk profiles.

- Challenges in Explainability and Bias: While powerful, AI models often pose challenges in explaining their decisions, raising concerns about bias and regulatory compliance.

Key Takeaways Credit Risk Rating Software Market Size & Forecast

Users frequently inquire about the primary factors driving growth in the Credit Risk Rating Software market, seeking insights into where the most significant opportunities lie. A key takeaway is the pervasive influence of digital transformation across the financial sector, necessitating sophisticated tools to manage escalating data volumes and complex risk profiles. The increasing stringency of regulatory compliance further underscores the market's upward trajectory, compelling institutions to invest in robust, automated solutions.

Another crucial insight is the transformative role of advanced technologies such as AI and cloud computing, which are not just improving efficiency but also enabling entirely new approaches to credit assessment. The market is not merely growing in size but also evolving in complexity, with a clear trend towards more integrated, predictive, and data-driven risk management. Investment in real-time analytics and predictive modeling capabilities will remain paramount for stakeholders aiming to maintain a competitive edge and navigate an increasingly uncertain global economic landscape.

- The market is poised for significant expansion, driven by digital transformation and the increasing complexity of financial transactions.

- Regulatory mandates and compliance requirements are acting as strong catalysts for adoption across financial institutions.

- AI and Machine Learning integration will be central to improving the precision and efficiency of credit risk assessments.

- Cloud-based deployments are gaining considerable traction due to their scalability, flexibility, and reduced infrastructure costs.

- Emerging markets present substantial growth opportunities as their financial sectors mature and adopt advanced risk management practices.

- Data quality and integration challenges remain critical hurdles that require innovative solutions for seamless operation.

- The emphasis on real-time analytics and predictive capabilities will define the next generation of credit risk rating software.

Credit Risk Rating Software Market Drivers Analysis

The Credit Risk Rating Software market is significantly propelled by several concurrent global trends and industry demands. Foremost among these is the escalating complexity of financial products and markets, which necessitates sophisticated tools beyond traditional manual assessments. As financial institutions deal with larger volumes of diverse data, the ability of software to process and interpret this information efficiently becomes critical for informed decision-making. This drives the demand for advanced analytical capabilities embedded within credit risk rating solutions.

Furthermore, the intensifying regulatory landscape, including frameworks like Basel III, IFRS 9, and CECL, imposes stringent requirements on financial institutions for risk assessment and reporting. Compliance with these evolving regulations is not optional, forcing organizations to adopt advanced software that can automate compliance processes, ensure data integrity, and provide audit trails. The digital transformation initiatives across the banking and financial services sector also play a crucial role, accelerating the adoption of automated and integrated credit risk management systems to enhance operational efficiency and reduce human error.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Regulatory Compliance Requirements | +1.5% | Global, particularly North America, Europe, APAC | Short- to Mid-term (2025-2029) |

| Growing Digital Transformation in Financial Services | +1.2% | Global | Mid- to Long-term (2026-2033) |

| Proliferation of Big Data and Advanced Analytics Needs | +1.0% | Global | Short- to Mid-term (2025-2030) |

| Demand for Real-time Risk Assessment | +0.8% | Developed Economies | Mid-term (2027-2032) |

| Rising Global Economic Volatility | +0.7% | Global | Short-term (2025-2027) |

Credit Risk Rating Software Market Restraints Analysis

Despite significant growth drivers, the Credit Risk Rating Software market faces several notable restraints that can impede its full potential. A primary concern is the substantial initial investment required for implementing sophisticated credit risk rating software. This includes not only software licenses but also costs associated with integration, customization, data migration, and comprehensive training for personnel. For smaller financial institutions or those with limited IT budgets, these high upfront costs can act as a significant barrier to adoption, potentially slowing down market penetration.

Another crucial restraint involves data privacy and security concerns. Credit risk assessment relies on sensitive financial and personal data, making data breaches and unauthorized access a critical vulnerability. Organizations are hesitant to fully transition to cloud-based solutions or third-party software without robust security protocols and compliance with stringent data protection regulations such as GDPR and CCPA. Furthermore, the complexity of integrating new credit risk software with legacy systems presents a formidable technical challenge, often leading to protracted implementation times and operational disruptions, thereby adding to the overall cost and risk of adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Implementation Costs | +0.9% | Global, particularly SMEs | Short- to Mid-term (2025-2029) |

| Data Privacy and Security Concerns | +0.8% | Global | Short- to Long-term (2025-2033) |

| Complex Integration with Legacy Systems | +0.7% | Mature Markets with established infrastructure | Mid-term (2026-2031) |

| Lack of Skilled Professionals for Advanced Analytics | +0.6% | Emerging Economies, some Developed Markets | Mid-term (2027-2032) |

| Resistance to Change and Adoption Barriers | +0.5% | Traditional Financial Institutions | Short-term (2025-2028) |

Credit Risk Rating Software Market Opportunities Analysis

The Credit Risk Rating Software market is rich with opportunities, particularly stemming from the accelerating adoption of cloud technologies and the continuous advancement of artificial intelligence and machine learning. The shift towards cloud-based solutions offers scalability, cost-effectiveness, and enhanced accessibility, appealing to a broader range of financial institutions, including smaller banks and fintech startups. This presents a significant avenue for vendors to offer Software-as-a-Service (SaaS) models, reducing the upfront burden for clients and expanding market reach. The ability to leverage cloud infrastructure for robust data processing and analytics also opens doors for more dynamic and real-time risk assessments.

Furthermore, the integration of AI and ML within credit risk rating software is evolving beyond basic automation to more sophisticated predictive analytics and anomaly detection. This allows for the incorporation of alternative data sources, such as social media sentiment, transactional behaviors, and utility payments, providing a more holistic and nuanced view of an applicant's creditworthiness. This capability is especially critical for assessing individuals and small businesses with thin credit files. Additionally, the expansion into emerging economies, where financial inclusion initiatives are gaining traction, offers substantial growth potential for vendors providing localized and flexible credit assessment solutions tailored to unique market dynamics and data availability challenges.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud-based and SaaS Solutions | +1.8% | Global | Mid- to Long-term (2026-2033) |

| Increasing Integration of AI and ML | +1.5% | Global | Short- to Long-term (2025-2033) |

| Growing Demand in Emerging Economies | +1.3% | APAC, Latin America, MEA | Mid- to Long-term (2027-2033) |

| Development of Customized and Niche Solutions | +1.0% | Global | Mid-term (2026-2031) |

| Adoption of Alternative Data for Assessment | +0.9% | Developed Economies | Short- to Mid-term (2025-2030) |

Credit Risk Rating Software Market Challenges Impact Analysis

The Credit Risk Rating Software market, while growing, is not without significant challenges that can impede its advancement and adoption. One prominent challenge is ensuring high-quality and consistent data. Credit risk models are highly dependent on accurate, complete, and timely data, yet financial institutions often grapple with fragmented data sources, inconsistencies, and issues related to data cleanliness. Poor data quality can lead to inaccurate risk assessments, undermining the very purpose of the software and potentially resulting in significant financial losses or misjudged credit decisions.

Another critical challenge involves the rapid evolution of regulatory frameworks and compliance standards. Software providers must continuously update their solutions to align with new mandates, which requires significant investment in research and development. This dynamic regulatory environment poses a perpetual challenge for both vendors and users to remain compliant without incurring excessive costs or operational disruptions. Furthermore, the ethical implications of AI, particularly concerning algorithmic bias and the need for explainable models, present a complex hurdle. Ensuring that AI-driven credit decisions are fair, transparent, and non-discriminatory is paramount, requiring sophisticated governance frameworks and ongoing model validation to mitigate reputational and legal risks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Quality and Integration Issues | +1.1% | Global | Short- to Long-term (2025-2033) |

| Evolving Regulatory Landscape and Compliance | +0.9% | Global | Short- to Mid-term (2025-2029) |

| Cybersecurity Threats and Data Breaches | +0.8% | Global | Short- to Long-term (2025-2033) |

| Explainability and Bias in AI Models | +0.7% | Developed Economies, Highly Regulated Markets | Mid-term (2026-2031) |

| Intense Competition Among Market Players | +0.6% | Global | Short- to Mid-term (2025-2030) |

Credit Risk Rating Software Market - Updated Report Scope

This market research report provides an in-depth analysis of the Credit Risk Rating Software market, covering its current size, historical performance, and future growth projections from 2025 to 2033. It examines key market dynamics, including drivers, restraints, opportunities, and challenges that shape the industry landscape. The report segments the market comprehensively by component, deployment, enterprise size, and end-user, offering granular insights into each category's contribution to market expansion.

Furthermore, the study delves into regional analyses across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, highlighting key growth pockets and strategic initiatives. It profiles top key players, providing an overview of their business strategies, product offerings, and competitive positioning. The report also integrates an AI impact analysis, illustrating how artificial intelligence is transforming credit risk assessment, and includes a section on frequently asked questions to address common user queries and provide actionable market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 17.5 Billion |

| Growth Rate | 13.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Moody's Analytics, S&P Global Market Intelligence, FICO, Experian, TransUnion, SAS Institute, IBM, Oracle, Pegasystems, Fiserv, Temenos, Provenir, Quantexa, TruValidate, LexisNexis Risk Solutions, CRIF, Equifax, Zest AI, Creditinfo, Capgemini |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Credit Risk Rating Software market is meticulously segmented to provide a granular understanding of its diverse components and applications. These segmentations allow for a detailed analysis of market dynamics, identifying growth opportunities and competitive landscapes within specific categories. Understanding how different components, deployment models, enterprise sizes, and end-users contribute to the market's overall trajectory is crucial for strategic planning and investment decisions, reflecting the varied needs and operational scales of financial entities globally.

The segmentation by component distinguishes between the core software solutions and the essential services that support their implementation and ongoing functionality, such as consulting, integration, and maintenance. Deployment models highlight the shift from traditional on-premise installations to flexible, scalable cloud-based solutions, reflecting technological advancements and changing preferences for infrastructure management. Enterprise size delineates demand patterns and feature requirements for large corporations versus small and medium-sized enterprises (SMEs), acknowledging their distinct operational capacities and budgetary constraints. Finally, end-user segmentation provides insight into the diverse applications of credit risk rating software across various financial sectors, from conventional banking to rapidly evolving fintech industries, each with unique risk assessment needs and regulatory adherence.

- By Component:

- Software

- Services

- By Deployment:

- On-premise

- Cloud

- By Enterprise Size:

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By End-User:

- Banks

- Credit Unions

- Financial Institutions (Non-Banking)

- Fintech Companies

- Mortgage Lenders

- Others (e.g., Investment Firms, Insurance Companies)

Regional Highlights

- North America: This region is a dominant market for Credit Risk Rating Software, driven by stringent regulatory frameworks, high adoption rates of advanced technologies, and the presence of numerous large financial institutions and fintech innovators. The U.S. and Canada lead in investments in AI and cloud-based risk solutions.

- Europe: Europe represents a mature market, characterized by robust regulatory compliance (e.g., GDPR, Basel III) and a strong emphasis on data privacy and security. Countries like the UK, Germany, and France are significant contributors, with increasing adoption of integrated risk management platforms.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid economic growth, increasing financial inclusion initiatives, and digital transformation across emerging economies like China, India, and Southeast Asian countries. The expanding banking sector and rising internet penetration contribute significantly to market expansion.

- Latin America: This region is experiencing steady growth, driven by an expanding middle class, increasing access to financial services, and efforts to modernize financial infrastructure. Brazil and Mexico are key markets, witnessing rising demand for automated credit assessment tools.

- Middle East and Africa (MEA): The MEA region shows promising growth, particularly in the GCC countries, due to economic diversification efforts, increased investments in smart infrastructure, and the development of fintech ecosystems. South Africa and UAE are leading the adoption of credit risk technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Credit Risk Rating Software Market.- Moody's Analytics

- S&P Global Market Intelligence

- FICO

- Experian

- TransUnion

- SAS Institute

- IBM

- Oracle

- Pegasystems

- Fiserv

- Temenos

- Provenir

- Quantexa

- TruValidate

- LexisNexis Risk Solutions

- CRIF

- Equifax

- Zest AI

- Creditinfo

- Capgemini

Frequently Asked Questions

What is Credit Risk Rating Software?

Credit Risk Rating Software is a specialized application designed to assess, quantify, and manage the creditworthiness of individuals, businesses, or financial institutions. It analyzes various data points and financial indicators to assign a risk score, helping lenders make informed decisions, mitigate potential defaults, and comply with regulatory requirements.

Why is Credit Risk Rating Software essential for financial institutions?

Credit Risk Rating Software is essential because it automates and enhances the accuracy of risk assessments, enabling financial institutions to efficiently manage large volumes of applications, reduce human error, and identify high-risk exposures. It supports regulatory compliance, optimizes capital allocation, and ultimately protects against financial losses by improving the quality of lending decisions.

How does AI impact Credit Risk Rating Software?

AI significantly impacts Credit Risk Rating Software by improving predictive accuracy through advanced algorithms, enabling the analysis of vast and diverse datasets including alternative data, and automating complex processes. This leads to faster, more consistent, and often more precise risk assessments, although it also introduces considerations around model explainability and bias.

What are the main benefits of cloud-based Credit Risk Rating Software?

The main benefits of cloud-based Credit Risk Rating Software include enhanced scalability, allowing institutions to easily adapt to changing data volumes and user needs; cost-efficiency by reducing the need for significant upfront infrastructure investments; improved accessibility from any location; and automatic updates ensuring the software remains current with the latest features and security protocols.

What are the key challenges in implementing Credit Risk Rating Software?

Key challenges in implementing Credit Risk Rating Software include the high initial costs associated with purchase and integration, ensuring the quality and consistency of data from disparate sources, navigating the complexities of integrating with existing legacy systems, addressing data privacy and cybersecurity concerns, and adapting to rapidly evolving regulatory landscapes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted