Procurement Software Market

Procurement Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703282 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Procurement Software Market Size

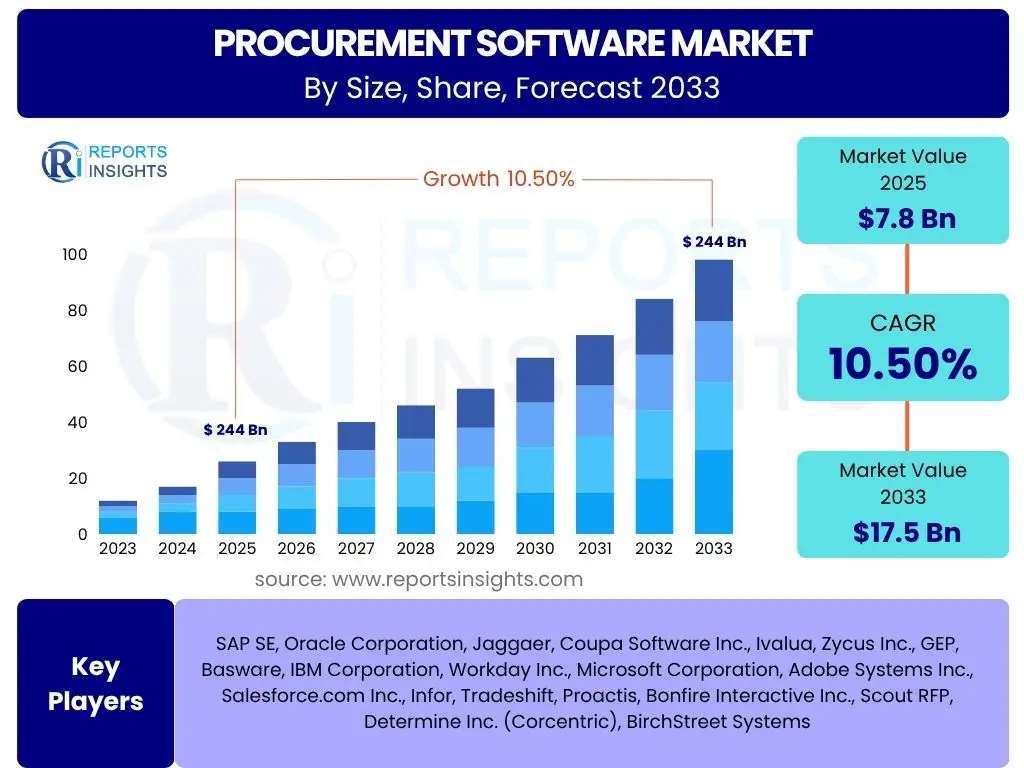

According to Reports Insights Consulting Pvt Ltd, The Procurement Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 7.8 billion in 2025 and is projected to reach USD 17.5 billion by the end of the forecast period in 2033.

Key Procurement Software Market Trends & Insights

The procurement software market is undergoing significant transformation driven by evolving technological landscapes and increasing demands for operational efficiency. Common user inquiries frequently revolve around the shift towards cloud-based solutions, the integration of advanced analytics for data-driven decision-making, and the growing emphasis on automation to streamline procurement processes. Furthermore, there is considerable interest in how these solutions enhance supply chain visibility and resilience amidst global disruptions, as well as their role in achieving sustainability goals.

These trends indicate a market moving beyond basic transaction processing to encompass more strategic functions. Organizations are seeking comprehensive platforms that can manage the entire procure-to-pay lifecycle, from sourcing and contract management to supplier relationship management and risk assessment. The focus is increasingly on end-to-end solutions that offer greater control, cost savings, and a competitive advantage in a complex global supply chain environment.

- Shift to cloud-based and SaaS deployment models for scalability and accessibility.

- Increased adoption of artificial intelligence and machine learning for predictive analytics and automation.

- Emphasis on enhanced supply chain visibility and risk management capabilities.

- Growing demand for integrated procure-to-pay suites rather than standalone modules.

- Focus on sustainability and ethical sourcing features within procurement platforms.

- Leveraging advanced analytics and business intelligence for strategic sourcing decisions.

- Expansion of supplier relationship management (SRM) functionalities to foster collaboration.

AI Impact Analysis on Procurement Software

User questions regarding the impact of AI on procurement software primarily focus on its ability to automate mundane tasks, enhance data analysis for better decision-making, and revolutionize supplier interactions. Users are keen to understand how AI can improve spend visibility, optimize contract negotiations, and predict potential supply chain disruptions, thereby moving procurement from a reactive to a proactive function. Concerns often include the accuracy of AI algorithms, data privacy, and the need for human oversight to ensure ethical procurement practices.

The integration of AI is fundamentally transforming traditional procurement processes, offering unprecedented levels of efficiency and insight. By automating repetitive tasks such as invoice processing, purchase order generation, and even initial supplier vetting, AI frees up procurement professionals to focus on strategic initiatives. Furthermore, AI-driven analytics can identify patterns in spending, forecast demand, and recommend optimal sourcing strategies, leading to substantial cost savings and improved supplier performance. This shift represents a move towards intelligent procurement, where data-driven insights underpin every decision.

- Automated invoice processing and reconciliation, significantly reducing manual effort and errors.

- Predictive analytics for spend forecasting and demand planning, enabling proactive procurement.

- Enhanced supplier selection and risk assessment through AI-driven evaluation of supplier data.

- Intelligent contract analysis and negotiation support, identifying optimal terms and potential risks.

- Chatbots and virtual assistants for internal requisitioning and supplier query management.

- Fraud detection and compliance monitoring by identifying anomalous transaction patterns.

- Optimization of sourcing strategies by analyzing market trends and supplier performance data.

Key Takeaways Procurement Software Market Size & Forecast

Common user questions about the procurement software market size and forecast reveal a strong interest in the primary growth accelerators, the role of specific technological advancements, and the most promising geographical regions for expansion. Users frequently inquire about how digital transformation initiatives within organizations are influencing software adoption and the long-term sustainability of the market's growth trajectory. There is also a notable emphasis on understanding the segments expected to witness the most significant growth and the overarching implications for operational efficiency and cost management.

The market's robust growth forecast is primarily driven by the increasing digitalization of business processes, the urgent need for cost optimization, and the critical imperative of strengthening supply chain resilience. Organizations are increasingly recognizing procurement software as an essential tool not just for transactional efficiency, but as a strategic asset for competitive advantage. The continued integration of emerging technologies like AI and blockchain, coupled with the expansion into small and medium-sized enterprises, positions the market for sustained expansion over the forecast period, addressing a broad spectrum of procurement challenges globally.

- The market is set for substantial growth, driven by digital transformation and supply chain complexities.

- Cloud-based solutions and AI integration are pivotal in enhancing market expansion and innovation.

- Cost reduction and operational efficiency remain primary motivations for procurement software adoption.

- North America and Europe currently lead the market, with Asia Pacific exhibiting the fastest growth potential.

- The shift towards comprehensive, integrated procure-to-pay suites is a dominant market characteristic.

Procurement Software Market Drivers Analysis

The procurement software market is primarily driven by the escalating demand for operational efficiency and cost reduction across various industries. Businesses are increasingly seeking to automate and optimize their purchasing processes to eliminate manual errors, reduce lead times, and achieve significant savings. The global push towards digital transformation initiatives further propels the adoption of sophisticated procurement solutions, as organizations aim to centralize data, improve visibility, and enhance decision-making capabilities within their supply chains.

Moreover, the heightened focus on supply chain resilience and risk management, especially in the wake of recent global disruptions, is compelling companies to invest in robust procurement software. These platforms offer advanced analytics and real-time insights crucial for identifying and mitigating risks, ensuring business continuity. The growing complexity of global sourcing, coupled with regulatory compliance requirements, also necessitates the use of specialized software to manage contracts, enforce policies, and maintain ethical sourcing practices effectively.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for operational efficiency and cost reduction | +1.2% | Global, particularly developed economies | Short-term to Mid-term |

| Growing focus on supply chain resilience and risk management | +0.9% | Global, across all industries | Mid-term to Long-term |

| Rising adoption of digital transformation initiatives | +1.1% | North America, Europe, Asia Pacific | Ongoing, Mid-term |

| Need for enhanced transparency and compliance in procurement | +0.8% | Europe (GDPR), Global (ESG) | Short-term to Mid-term |

Procurement Software Market Restraints Analysis

Despite significant growth drivers, the procurement software market faces certain restraints that could impede its expansion. One major challenge is the high initial implementation cost associated with sophisticated procurement software solutions, especially for large enterprises. These costs include not only licensing fees but also extensive integration with existing enterprise resource planning (ERP) systems, data migration, and customization, making it a considerable investment for potential adopters.

Another significant restraint is the complexity of integrating new procurement platforms with legacy systems and diverse IT infrastructures. Many organizations operate with fragmented systems, and ensuring seamless data flow and functionality can be time-consuming and resource-intensive, leading to implementation delays and increased operational complexities. Furthermore, data security and privacy concerns remain a critical barrier, particularly for cloud-based solutions, as companies are hesitant to host sensitive financial and supplier data outside their controlled environments, despite robust security measures by providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial implementation costs and ongoing maintenance | -0.7% | SMEs, emerging markets | Short-term to Mid-term |

| Complexities of integration with existing legacy systems | -0.6% | Large enterprises, industries with old IT infrastructure | Ongoing |

| Concerns regarding data security and privacy in cloud environments | -0.5% | Global, highly regulated industries (e.g., healthcare, finance) | Ongoing |

| Resistance to change and lack of skilled personnel for adoption | -0.4% | Organizations with traditional work cultures | Short-term |

Procurement Software Market Opportunities Analysis

The procurement software market is rich with opportunities, particularly driven by the accelerating adoption of cloud-based solutions. Cloud deployment offers scalability, flexibility, and reduced infrastructure costs, making advanced procurement capabilities accessible to a broader range of businesses, including small and medium-sized enterprises (SMEs). This shift allows companies to quickly implement and adapt procurement software without significant upfront IT investments, fostering wider market penetration.

The integration of advanced technologies such as Artificial Intelligence (AI), Machine Learning (ML), and blockchain presents significant avenues for innovation and market expansion. AI and ML can enhance predictive analytics, automate complex tasks, and improve decision-making, offering new levels of efficiency and strategic value. Blockchain, on the other hand, provides opportunities for greater transparency and security in supply chain transactions, building trust and reducing fraud. Furthermore, the growing emphasis on sustainable and ethical sourcing creates a demand for software solutions that can track and report on environmental, social, and governance (ESG) compliance, opening new niches for specialized functionalities and services within the procurement software ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of cloud-based and SaaS procurement solutions | +1.5% | Global, particularly SMEs and startups | Mid-term to Long-term |

| Integration of AI, Machine Learning, and predictive analytics | +1.3% | Globally across all enterprise sizes | Mid-term to Long-term |

| Growing demand for sustainable and ethical sourcing functionalities | +1.0% | Europe, North America, corporations with strong ESG goals | Mid-term |

| Expansion into untapped markets, especially emerging economies | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

Procurement Software Market Challenges Impact Analysis

The procurement software market faces several challenges that can affect its growth trajectory and adoption rates. One prominent challenge is vendor lock-in, where organizations become heavily reliant on a single vendor's ecosystem, making it difficult and costly to switch providers or integrate solutions from other vendors. This can limit flexibility and hinder the adoption of best-of-breed solutions. Additionally, ensuring seamless integration with diverse existing enterprise systems, such as ERP, CRM, and accounting software, presents a significant technical hurdle for many organizations, often leading to prolonged implementation cycles and unexpected costs.

Another key challenge involves the rapid pace of technological advancements and the need for continuous innovation. Software providers must constantly update their offerings to incorporate new features like AI, blockchain, and advanced analytics, which demands significant R&D investment. For end-users, this translates to the challenge of keeping up with evolving functionalities and ensuring their teams are adequately trained. Furthermore, cybersecurity threats and data privacy regulations pose ongoing concerns, requiring robust security measures and strict compliance frameworks, which can add complexity and cost to software development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Vendor lock-in and challenges in multi-vendor integration | -0.5% | Global, large enterprises | Ongoing |

| Data privacy concerns and adherence to evolving regulations (e.g., GDPR, CCPA) | -0.6% | Europe, North America, industries handling sensitive data | Ongoing |

| Resistance to change and user adoption within organizations | -0.4% | Global, traditional industries | Short-term |

| Rapid technological changes and the need for continuous innovation | -0.3% | Global, all market players | Ongoing |

Procurement Software Market - Updated Report Scope

This market research report offers an in-depth analysis of the global Procurement Software Market, providing a comprehensive overview of market dynamics, segmentation, and regional landscapes. The scope includes detailed insights into market size, growth projections, key trends, drivers, restraints, opportunities, and challenges influencing the industry from 2025 to 2033. It further covers the impact of emerging technologies like AI and offers a competitive landscape analysis, identifying key players and their strategic initiatives, to provide a holistic understanding for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2033 | USD 17.5 Billion |

| Growth Rate | 10.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAP SE, Oracle Corporation, Jaggaer, Coupa Software Inc., Ivalua, Zycus Inc., GEP, Basware, IBM Corporation, Workday Inc., Microsoft Corporation, Adobe Systems Inc., Salesforce.com Inc., Infor, Tradeshift, Proactis, Bonfire Interactive Inc., Scout RFP, Determine Inc. (Corcentric), BirchStreet Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The procurement software market is intricately segmented to provide a granular view of its various facets, enabling a deeper understanding of market dynamics and growth opportunities. These segmentations are crucial for identifying specific market niches, understanding customer preferences, and tailoring solutions to meet diverse industry requirements. By analyzing the market across these dimensions, stakeholders can discern dominant trends and emerging areas of growth, from the adoption patterns of different software components to their deployment models and suitability for various organizational sizes and industry verticals.

The segmentation offers insights into which solutions are gaining traction, whether it's comprehensive suites or specialized standalone modules, and how cloud adoption is influencing market structure. Furthermore, examining the market by organization size reveals the varying needs and investment capacities of SMEs versus large enterprises, while industry vertical analysis highlights the unique procurement challenges and opportunities within sectors like manufacturing, retail, healthcare, and IT. This multi-dimensional segmentation provides a robust framework for strategic planning and competitive positioning within the dynamic procurement software landscape.

- By Component: This segment includes the software itself, which can be offered as a comprehensive suite covering multiple procurement functions or as standalone modules focusing on specific areas like e-procurement or contract management. Services, such as consulting, implementation, and support, form another crucial part of this segment, facilitating the successful deployment and ongoing operation of these software solutions.

- By Deployment: The market is broadly categorized into Cloud-based and On-premise deployments. Cloud-based solutions, often delivered as Software-as-a-Service (SaaS), offer flexibility, scalability, and reduced infrastructure costs. On-premise solutions, deployed within an organization's own infrastructure, provide greater control over data and customization, catering to specific security and compliance needs.

- By Organization Size: This segment differentiates between Small & Medium Enterprises (SMEs) and Large Enterprises. SMEs often prefer more agile, cost-effective, and easy-to-implement cloud-based solutions, while large enterprises require robust, highly scalable, and often customized solutions that can integrate with complex existing IT landscapes.

- By Industry Vertical: The market serves a wide range of industries, each with unique procurement requirements. Key verticals include Manufacturing (for supply chain optimization), Retail & E-commerce (for inventory and supplier management), Healthcare & Pharma (for compliance and specialized sourcing), IT & Telecom (for service and technology procurement), BFSI (for regulatory compliance and risk), and Government & Public Sector (for transparency and public tender management). The "Others" category encompasses diverse sectors such as education, logistics, and hospitality.

Regional Highlights

- North America: This region dominates the procurement software market, driven by early adoption of advanced technologies, the presence of major solution providers, and a strong emphasis on digital transformation and supply chain resilience across industries. The U.S. and Canada are key contributors, with robust IT infrastructure and a mature enterprise software market.

- Europe: Europe represents a significant market share, characterized by increasing awareness of digital procurement benefits, stringent regulatory compliance requirements (e.g., GDPR), and a growing focus on sustainable and ethical sourcing. Countries like Germany, the UK, and France are leading the adoption, particularly in manufacturing and automotive sectors.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, increasing digitalization initiatives in emerging economies like China, India, and Southeast Asian countries, and the growing presence of global and local enterprises. The rise of SMEs and focus on supply chain efficiency further contribute to market expansion.

- Latin America: This region is experiencing steady growth, driven by increasing foreign investments, expanding industrial sectors, and the adoption of cloud-based solutions to enhance operational efficiencies. Brazil and Mexico are key markets, showing growing interest in automating procurement processes to reduce costs and improve transparency.

- Middle East and Africa (MEA): The MEA market is gradually expanding, primarily due to government initiatives for digital transformation, diversification of economies away from oil, and increasing investments in infrastructure and technology. Countries like UAE, Saudi Arabia, and South Africa are leading the adoption of procurement software to modernize their business operations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Procurement Software Market.- SAP SE

- Oracle Corporation

- Jaggaer

- Coupa Software Inc.

- Ivalua

- Zycus Inc.

- GEP

- Basware

- IBM Corporation

- Workday Inc.

- Microsoft Corporation

- Adobe Systems Inc.

- Salesforce.com Inc.

- Infor

- Tradeshift

- Proactis

- Bonfire Interactive Inc.

- Scout RFP (Workday)

- Determine Inc. (Corcentric)

- BirchStreet Systems

Frequently Asked Questions

Analyze common user questions about the Procurement Software market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is procurement software?

Procurement software is a digital solution designed to automate, streamline, and optimize the entire procure-to-pay process, from sourcing and vendor management to purchase order creation, invoicing, and contract management. It helps organizations manage supplier relationships, control spending, and improve operational efficiency.

What are the primary benefits of implementing procurement software?

Key benefits include significant cost savings through optimized sourcing and reduced maverick spending, improved operational efficiency by automating manual tasks, enhanced transparency and compliance, better supplier relationship management, and increased data visibility for strategic decision-making and risk mitigation.

What are the key features to look for in procurement software?

Essential features typically include e-procurement capabilities, spend analysis, supplier management, contract management, requisition-to-pay automation, reporting and analytics, and integration capabilities with existing ERP or accounting systems. Advanced solutions may also offer AI-driven insights, risk assessment, and sustainability tracking.

Is cloud-based procurement software more beneficial than on-premise solutions?

Cloud-based (SaaS) procurement software generally offers greater flexibility, scalability, lower upfront costs, faster deployment, and automatic updates, making it highly beneficial for most organizations, especially SMEs. On-premise solutions, while offering greater control and customization, require significant upfront investment and in-house IT management.

How is AI transforming the procurement software market?

AI is revolutionizing procurement software by enabling intelligent automation of routine tasks, predictive analytics for demand forecasting and risk assessment, enhanced supplier selection, and negotiation support. It allows procurement teams to shift from transactional activities to more strategic roles, driving greater value and efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted