Corrosion Inhibitor Market

Corrosion Inhibitor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704155 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

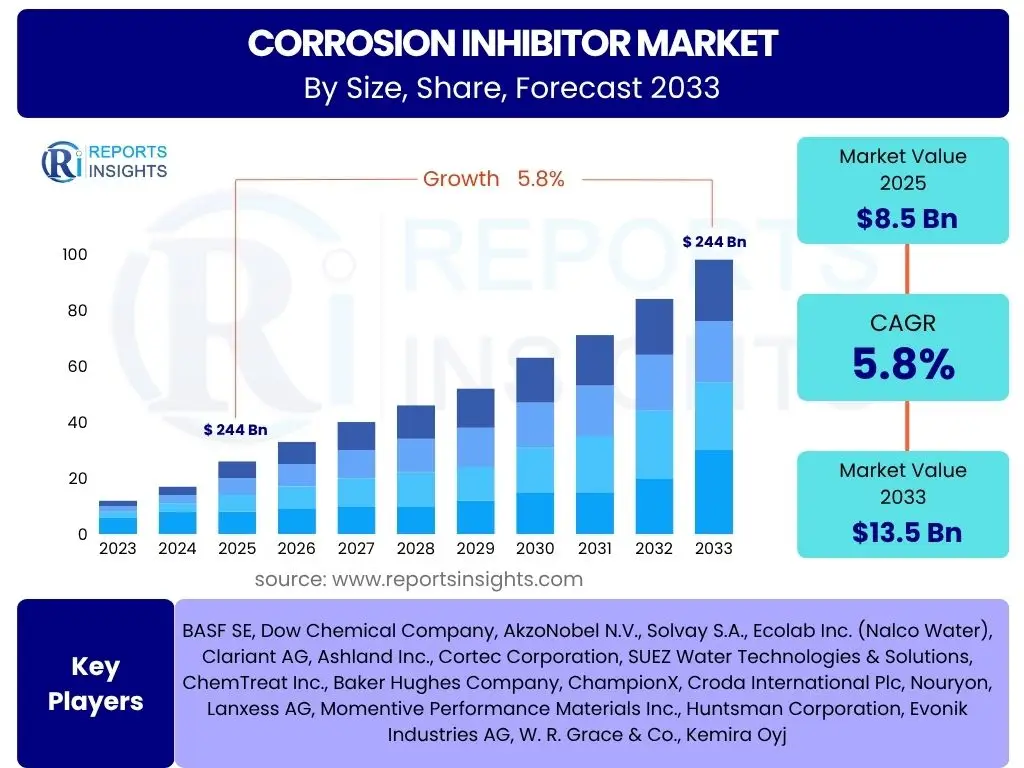

Corrosion Inhibitor Market Size

According to Reports Insights Consulting Pvt Ltd, The Corrosion Inhibitor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033. This growth is primarily driven by increasing industrialization, aging infrastructure requiring maintenance, and stringent regulatory frameworks aimed at preserving asset integrity across various sectors.

The consistent expansion in end-use industries such as oil and gas, power generation, and water treatment significantly contributes to the escalating demand for corrosion inhibitors. These industries heavily rely on effective corrosion prevention to ensure operational safety, extend equipment lifespan, and minimize costly downtime. Furthermore, the global emphasis on sustainability and the development of environmentally friendly corrosion solutions are shaping market dynamics, fostering innovation in product development and application methodologies.

Key Corrosion Inhibitor Market Trends & Insights

Analysis of common user inquiries regarding the Corrosion Inhibitor market reveals a strong interest in emerging technologies, sustainable solutions, and the integration of smart systems. Users frequently seek information on how environmental regulations are shaping product development and the shift towards bio-based or green inhibitors. There is also significant curiosity about the application of digitalization and real-time monitoring in corrosion management strategies.

The market is witnessing a profound transformation driven by advancements in material science and a global push for eco-conscious practices. Innovations are centered around developing more efficient and less hazardous chemical formulations, alongside a growing emphasis on predictive maintenance. This strategic shift is designed to enhance operational longevity and reduce environmental impact across industrial applications.

- Shift towards green and sustainable corrosion inhibitors, including bio-based and biodegradable formulations.

- Increased adoption of smart corrosion monitoring systems and digital solutions for predictive maintenance.

- Growing demand for multi-functional corrosion inhibitors offering enhanced protection and efficiency.

- Development of nanotechnology-based corrosion inhibitors for improved barrier properties and targeted delivery.

- Expansion of customized corrosion inhibitor solutions for specialized industrial applications.

AI Impact Analysis on Corrosion Inhibitor

User questions regarding the impact of Artificial Intelligence (AI) on the Corrosion Inhibitor market frequently revolve around its potential to revolutionize predictive maintenance, optimize chemical dosages, and enhance material selection. Users are keen to understand how AI algorithms can analyze vast datasets from sensors and historical performance to anticipate corrosion events, thereby enabling proactive intervention and reducing unforeseen failures. Expectations are high for AI to bring greater precision and efficiency to corrosion management strategies.

AI's influence in the corrosion inhibitor domain is poised to be transformative, particularly in data-driven decision-making and process optimization. By leveraging machine learning models, companies can gain deeper insights into corrosion mechanisms, predict inhibitor performance under various conditions, and dynamically adjust treatment protocols. This capability not only leads to more effective corrosion prevention but also optimizes resource utilization and reduces operational costs, marking a significant leap from traditional reactive maintenance approaches.

- Enhanced predictive modeling for corrosion risk assessment and inhibitor performance.

- Optimization of corrosion inhibitor dosage and application through real-time data analysis.

- Automated monitoring and diagnostic systems for early detection of corrosion and system anomalies.

- Improved material selection and design through AI-driven simulations and analysis.

- Development of smart coatings and self-healing materials with AI-integrated properties.

Key Takeaways Corrosion Inhibitor Market Size & Forecast

Common user questions concerning key takeaways from the Corrosion Inhibitor market size and forecast highlight a strong desire to understand the primary growth catalysts, the most influential regional markets, and the long-term sustainability of demand. Users are particularly interested in identifying sectors that will drive the most significant growth and how evolving environmental regulations will shape future market trajectories. The focus is on actionable insights that can inform strategic business decisions.

The market's robust growth trajectory is underpinned by an increasing global industrial footprint and the critical need to preserve existing infrastructure. Significant opportunities are emerging from the push towards sustainable and technologically advanced solutions, positioning the market for sustained expansion. Regional dynamics, particularly in rapidly industrializing economies, will play a crucial role in shaping demand patterns and investment priorities.

- The market is poised for significant growth driven by industrial expansion and infrastructure aging.

- Asia Pacific is expected to emerge as a dominant region due to rapid industrialization and urbanization.

- Sustainability and environmental compliance are becoming paramount, fostering innovation in green inhibitors.

- Technological advancements, including smart monitoring and AI integration, will redefine corrosion management practices.

- Strategic collaborations and mergers are anticipated to consolidate market leadership and expand product portfolios.

Corrosion Inhibitor Market Drivers Analysis

The global Corrosion Inhibitor market is propelled by several robust drivers, primarily the escalating need for asset preservation across diverse industrial sectors. Aging infrastructure in developed economies necessitates continuous maintenance and protection against degradation, ensuring operational longevity and safety. Concurrently, rapid industrialization in emerging markets, particularly in Asia Pacific and Latin America, leads to the establishment of new manufacturing facilities, power plants, and oil and gas installations, all requiring robust corrosion management solutions from inception.

Another significant driver is the increasing stringency of environmental regulations regarding industrial emissions and effluent discharge. This regulatory pressure compels industries to adopt more effective corrosion control measures to prevent leaks, spills, and equipment failures that could lead to environmental contamination. Furthermore, the growing demand for extending the lifespan of costly industrial equipment and machinery to optimize capital expenditure and reduce replacement costs directly fuels the adoption of high-performance corrosion inhibitors. These factors collectively create a strong and persistent demand for advanced corrosion protection solutions worldwide.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Infrastructure and Asset Preservation | +1.5% | North America, Europe, Asia Pacific | Medium-Term (2025-2029) |

| Growing Industrialization and Urbanization | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Long-Term (2025-2033) |

| Increasing Demand from Oil & Gas and Power Generation | +1.0% | North America, Middle East, Asia Pacific | Medium-Term (2025-2029) |

| Stringent Environmental Regulations and Safety Standards | +0.8% | Europe, North America, Global | Long-Term (2025-2033) |

| Technological Advancements in Inhibitor Formulations | +0.7% | Global | Long-Term (2025-2033) |

Corrosion Inhibitor Market Restraints Analysis

Despite robust growth drivers, the Corrosion Inhibitor market faces certain restraints that can temper its expansion. One significant challenge is the volatility in raw material prices, particularly for petrochemical derivatives and specialty chemicals used in inhibitor formulations. Fluctuations in these costs can directly impact manufacturing expenses, leading to increased product prices and potentially affecting market competitiveness and profit margins for manufacturers. This unpredictability makes long-term planning and stable pricing strategies difficult.

Another key restraint involves increasing environmental concerns and stringent regulations regarding the use of certain conventional corrosion inhibitors. Many traditional chemistries, such as chromates, are being phased out or heavily regulated due to their toxicity and environmental persistence, necessitating costly research and development into safer, greener alternatives. This transition not only requires significant investment but also presents technical challenges in developing substitutes that offer comparable performance. Furthermore, the high initial investment required for implementing comprehensive corrosion management programs, including specialized inhibitors and monitoring systems, can be a deterrent for smaller enterprises or those with limited capital, particularly in developing regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.7% | Global | Medium-Term (2025-2029) |

| Stringent Environmental Regulations on Certain Chemistries | -0.6% | Europe, North America | Long-Term (2025-2033) |

| High Research & Development Costs for Green Inhibitors | -0.5% | Global | Medium-Term (2025-2029) |

| Competition from Alternative Corrosion Protection Methods | -0.4% | Global | Long-Term (2025-2033) |

Corrosion Inhibitor Market Opportunities Analysis

Significant opportunities are emerging in the Corrosion Inhibitor market driven by the growing global emphasis on sustainability and the pursuit of advanced materials. The increasing demand for eco-friendly and biodegradable corrosion inhibitors presents a substantial avenue for growth, as industries strive to comply with stricter environmental mandates and improve their corporate social responsibility profiles. This trend encourages innovation in bio-based formulations and less toxic chemical alternatives that maintain high performance standards while minimizing ecological impact.

Furthermore, the expansion into specialized applications and emerging economies offers considerable potential for market players. Niche industries such as aerospace, electronics, and medical devices require highly specific corrosion solutions tailored to unique operational conditions and material sensitivities. Simultaneously, rapid industrial and infrastructural development in regions like Southeast Asia, Africa, and parts of Latin America creates new markets for corrosion inhibitors, as these regions modernize their industrial bases and invest in long-term asset protection. The integration of digitalization and smart technologies for real-time monitoring and predictive maintenance also opens new revenue streams for solution providers, offering value-added services beyond mere chemical supply.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-Friendly and Bio-Based Inhibitors | +1.3% | Global, particularly Europe and North America | Long-Term (2025-2033) |

| Expansion into Emerging Economies and Niche Applications | +1.1% | Asia Pacific, Latin America, MEA | Long-Term (2025-2033) |

| Integration of Smart Monitoring and Predictive Technologies | +0.9% | Global | Medium-Term (2025-2029) |

| Advancements in Nanotechnology for Enhanced Performance | +0.8% | Global | Long-Term (2025-2033) |

Corrosion Inhibitor Market Challenges Impact Analysis

The Corrosion Inhibitor market faces several significant challenges that necessitate strategic adaptation from market participants. One primary challenge is the complexity of achieving optimal corrosion protection across diverse industrial environments and material compositions. Different metals, alloys, and operating conditions (e.g., temperature, pH, fluid type) require specific inhibitor chemistries, making a one-size-fits-all solution largely impractical. This necessitates extensive research and development for customized solutions, increasing costs and development timelines for manufacturers.

Another hurdle is the increasing regulatory scrutiny and the evolving landscape of chemical substance regulations globally. Compliance with REACH, EPA, and similar regulations requires significant investment in testing, registration, and reformulation of products, particularly as substances are reclassified or restricted. This constant need for regulatory adherence can create barriers to market entry for new players and increase operational complexities for established ones. Furthermore, the competition from alternative corrosion protection methods, such as coatings, cathodic protection, and material selection, can challenge the market share of chemical inhibitors, prompting continuous innovation to maintain competitive advantage and demonstrate superior cost-effectiveness over the asset's lifespan.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Diverse Industrial Applications and Environments | -0.6% | Global | Long-Term (2025-2033) |

| Regulatory Compliance and Evolving Chemical Legislation | -0.5% | Europe, North America, Asia Pacific | Long-Term (2025-2033) |

| Need for High Performance and Cost-Effectiveness | -0.4% | Global | Medium-Term (2025-2029) |

| Limited Awareness and Adoption in Some SME Sectors | -0.3% | Emerging Economies | Medium-Term (2025-2029) |

Corrosion Inhibitor Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the Corrosion Inhibitor market, providing detailed insights into its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape. Furthermore, the report delves into various market segments, including types of inhibitors, their applications, and end-use industries, providing a holistic view of market dynamics across key geographical regions. The aim is to equip stakeholders with critical data and strategic recommendations for informed decision-making within this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Dow Chemical Company, AkzoNobel N.V., Solvay S.A., Ecolab Inc. (Nalco Water), Clariant AG, Ashland Inc., Cortec Corporation, SUEZ Water Technologies & Solutions, ChemTreat Inc., Baker Hughes Company, ChampionX, Croda International Plc, Nouryon, Lanxess AG, Momentive Performance Materials Inc., Huntsman Corporation, Evonik Industries AG, W. R. Grace & Co., Kemira Oyj |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Corrosion Inhibitor market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective market dynamics. This segmentation facilitates a granular analysis of product types, applications, and end-use industries, revealing specific growth drivers and opportunities within each category. The breakdown allows for a precise evaluation of consumer preferences, technological shifts, and regulatory impacts on various market niches.

Understanding these segments is crucial for strategic planning, enabling market players to identify high-growth areas, optimize product portfolios, and tailor marketing efforts. The interdependencies between these segments often dictate overall market trends, with innovations in one area frequently influencing demand and development in others. For instance, the demand for specific inhibitor types is directly influenced by the needs of particular end-use industries and the nature of the application.

- By Type:

- Organic Inhibitors: Includes Amines, Carboxylates, Azoles, Phosphonates, and other organic compounds designed to form a protective film on metal surfaces.

- Inorganic Inhibitors: Comprises Chromates, Phosphates, Nitrites, Silicates, Molybdates, and other inorganic salts that react with the metal surface to form a passive layer.

- Mixed Inhibitors: Formulations combining both organic and inorganic compounds to leverage synergistic effects and provide broader protection.

- By Application:

- Water Treatment: Used in cooling systems, boilers, and reverse osmosis plants to prevent scaling and corrosion.

- Process Industries: Critical for equipment protection in chemical processing, pulp & paper, and textile industries.

- Oil & Gas: Essential for pipelines, refineries, and drilling operations to combat corrosion in harsh environments.

- Power Generation: Applied in power plants, including thermal, nuclear, and renewable energy facilities, for turbine and boiler protection.

- Metalworking: Utilized in metal cutting fluids, lubricants, and rust preventives.

- Chemical Processing: Protects vessels, reactors, and piping handling corrosive chemicals.

- Pulp & Paper: Safeguards machinery and piping in paper manufacturing processes.

- Construction: Used in concrete admixtures and rebar coatings to prevent corrosion in buildings and infrastructure.

- Transportation: Applied in automotive cooling systems, marine vessels, and aircraft for engine and structural protection.

- By End-use Industry:

- Industrial: Broad category encompassing manufacturing, general industry, and various production facilities.

- Automotive: Specific to vehicles, covering parts, engines, and structural components.

- Marine: For ships, offshore platforms, and coastal infrastructure.

- Aerospace: For aircraft components, engines, and structural integrity.

- Infrastructure: Roads, bridges, tunnels, and public utilities.

- Energy: Power generation, oil & gas, and renewable energy sectors.

- Food & Beverage: For processing equipment and storage tanks, ensuring product integrity and safety.

Regional Highlights

- North America: This region is a mature market characterized by stringent environmental regulations and a strong focus on asset integrity across the oil and gas, power generation, and chemical processing sectors. The demand here is driven by the need to maintain aging infrastructure and adopt advanced, sustainable corrosion management solutions. Innovation in smart monitoring and digital integration is a key trend.

- Europe: Europe is at the forefront of adopting green and sustainable corrosion inhibitors, largely influenced by strict environmental policies and a robust chemical industry. The region emphasizes research and development into eco-friendly formulations and highly efficient solutions for its diverse industrial base, including automotive, marine, and water treatment.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to rapid industrialization, urbanization, and significant investments in infrastructure development across countries like China, India, and Southeast Asian nations. The burgeoning oil and gas, manufacturing, and construction industries are major consumers of corrosion inhibitors, driving substantial demand for both conventional and advanced solutions.

- Latin America: This region presents considerable growth opportunities, particularly in the oil and gas, mining, and agricultural sectors. Increasing industrial activity and investment in infrastructure development are fueling the demand for corrosion inhibitors, with a growing focus on cost-effective and efficient solutions.

- Middle East and Africa (MEA): The MEA region is dominated by the vast oil and gas industry, which is a primary driver for the corrosion inhibitor market. Large-scale upstream, midstream, and downstream operations necessitate robust corrosion protection. Infrastructure projects and growing industrial diversification also contribute to market demand, with a rising emphasis on advanced technologies for asset longevity.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Corrosion Inhibitor Market.- BASF SE

- Dow Chemical Company

- AkzoNobel N.V.

- Solvay S.A.

- Ecolab Inc. (Nalco Water)

- Clariant AG

- Ashland Inc.

- Cortec Corporation

- SUEZ Water Technologies & Solutions

- ChemTreat Inc.

- Baker Hughes Company

- ChampionX

- Croda International Plc

- Nouryon

- Lanxess AG

- Momentive Performance Materials Inc.

- Huntsman Corporation

- Evonik Industries AG

- W. R. Grace & Co.

- Kemira Oyj

Frequently Asked Questions

Analyze common user questions about the Corrosion Inhibitor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a corrosion inhibitor and how does it work?

A corrosion inhibitor is a chemical substance that, when added in small concentrations to an environment, effectively decreases the corrosion rate of a metal exposed to that environment. It works by forming a protective film on the metal surface, reacting with the metal to create a passive layer, or neutralizing corrosive agents in the environment, thereby preventing or slowing down the degradation process.

What are the primary types of corrosion inhibitors used in industry?

The primary types include organic inhibitors (e.g., amines, azoles, phosphonates), which form a protective film, and inorganic inhibitors (e.g., phosphates, nitrites, molybdates), which create a passive layer on the metal. Mixed inhibitors combine both types to leverage synergistic effects and provide broader protection in diverse industrial applications.

Which industries are the largest consumers of corrosion inhibitors?

The largest consumers of corrosion inhibitors are industries such as oil and gas, power generation, water treatment, chemical processing, and metalworking. These sectors rely heavily on inhibitors to protect critical infrastructure, pipelines, machinery, and equipment from degradation, ensuring operational safety and extending asset lifespan.

What are the key trends shaping the future of the corrosion inhibitor market?

Key trends include a significant shift towards green and sustainable formulations, the integration of smart monitoring systems and AI for predictive maintenance, the development of nanotechnology-based inhibitors, and an increasing demand for customized solutions tailored to specific industrial environments and materials.

How do environmental regulations impact the corrosion inhibitor market?

Environmental regulations significantly impact the market by driving the demand for safer, less toxic, and more eco-friendly inhibitor alternatives. Stricter rules on chemical usage and discharge compel manufacturers to invest in research and development of sustainable formulations, leading to the phasing out of traditional, hazardous chemistries and fostering innovation in green corrosion protection.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted