Scale Inhibitor Market

Scale Inhibitor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702899 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Scale Inhibitor Market Size

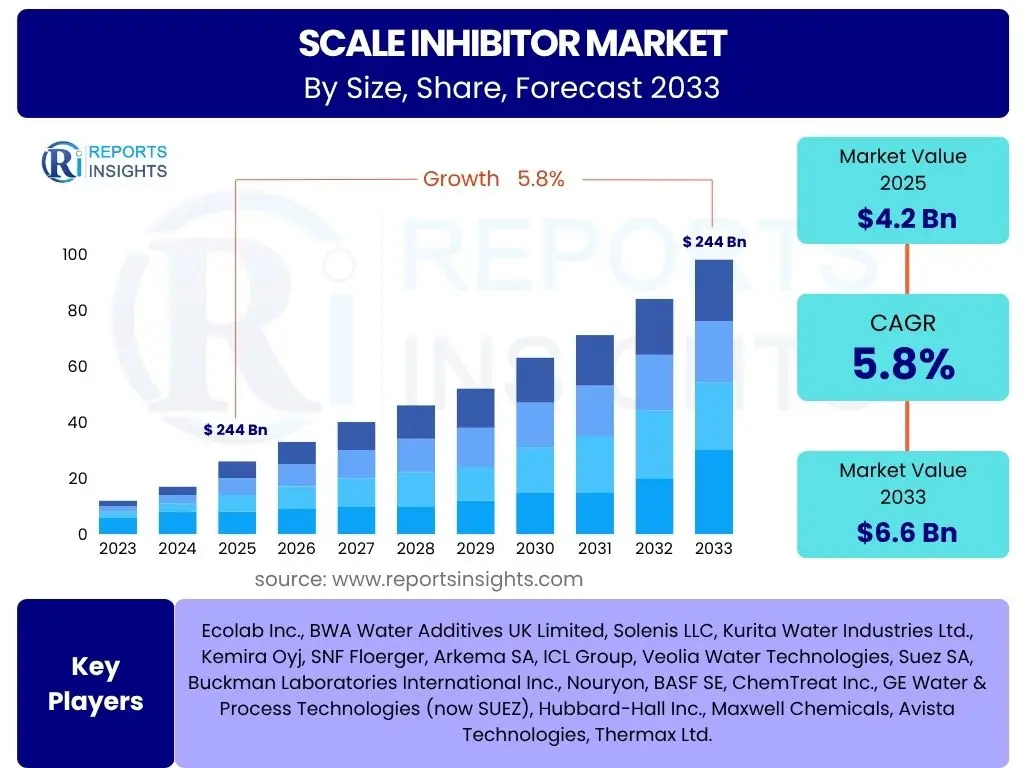

According to Reports Insights Consulting Pvt Ltd, The Scale Inhibitor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 4.2 billion in 2025 and is projected to reach USD 6.6 billion by the end of the forecast period in 2033.

Key Scale Inhibitor Market Trends & Insights

The global scale inhibitor market is experiencing a significant transformation driven by increasing industrialization and the growing demand for efficient water treatment solutions across various sectors. A key trend observed is the heightened focus on sustainable and environmentally friendly scale inhibition technologies. Industries are actively seeking solutions that not only prevent scale formation effectively but also comply with stringent environmental regulations, leading to a surge in demand for green chemistries and biodegradable inhibitors.

Another prominent trend is the rising adoption of smart water management systems and advanced monitoring technologies. These innovations allow for precise dosing and real-time performance evaluation of scale inhibitors, optimizing their usage and reducing operational costs. Furthermore, the expansion of the oil and gas industry, particularly in unconventional resources, coupled with the escalating need for clean water in power generation and industrial cooling, continues to underpin the market's growth trajectory, pushing manufacturers to innovate and offer specialized, high-performance solutions.

- Shift towards eco-friendly and biodegradable scale inhibitors.

- Integration of smart technologies and real-time monitoring for inhibitor optimization.

- Increasing demand from the oil and gas sector, especially unconventional resources.

- Growing application in industrial water treatment and cooling systems.

- Development of specialized inhibitors for diverse industrial applications.

AI Impact Analysis on Scale Inhibitor

Artificial intelligence (AI) is poised to revolutionize the scale inhibitor market by introducing unprecedented levels of efficiency, precision, and predictive capabilities. Users are increasingly curious about how AI can optimize chemical formulations, predict scaling tendencies in industrial systems, and enhance the overall effectiveness of inhibition programs. The primary expectation revolves around AI's ability to analyze vast datasets related to water chemistry, temperature, flow rates, and historical scaling patterns, thereby enabling proactive rather than reactive treatment strategies. This predictive power can significantly reduce chemical consumption, minimize downtime, and extend equipment lifespan.

Moreover, AI-driven platforms are anticipated to facilitate the development of novel scale inhibitor chemistries through advanced material science simulations and high-throughput screening. This could accelerate the discovery of more potent, cost-effective, and environmentally benign inhibitors. Concerns often revolve around the initial investment required for AI infrastructure, data privacy, and the need for specialized expertise to implement and manage these sophisticated systems. However, the long-term benefits in terms of operational efficiency and sustainability are expected to outweigh these challenges, driving gradual but impactful adoption across the industry.

- Predictive analytics for early scale detection and prevention.

- Optimization of inhibitor dosage and application based on real-time data.

- Accelerated R&D for new, more effective scale inhibitor formulations.

- Reduced operational costs through minimized chemical usage and equipment downtime.

- Enhanced decision-making for water treatment strategies.

Key Takeaways Scale Inhibitor Market Size & Forecast

The scale inhibitor market is on a robust growth trajectory, driven primarily by escalating industrial water usage and the imperative for efficient asset protection across diverse sectors. A significant takeaway is the consistent demand stemming from mature industries like oil and gas, power generation, and manufacturing, coupled with burgeoning needs from emerging economies experiencing rapid industrial expansion. The forecast highlights a sustained CAGR, indicating a stable and expanding market landscape with considerable opportunities for innovation and penetration.

Furthermore, the market's future growth is intrinsically linked to advancements in sustainable chemistry and digital integration. The shift towards greener alternatives and the adoption of smart technologies for water management are not merely trends but fundamental drivers shaping the industry's evolution. Stakeholders should recognize the critical balance between performance efficacy and environmental responsibility as a pivotal factor influencing market dynamics and long-term success. The projected market value underscores the continued economic significance of scale inhibition in global industrial operations.

- Steady growth projected, reaching USD 6.6 billion by 2033.

- Industrial water treatment and asset protection remain core growth drivers.

- Sustainable and smart technologies are key to future market expansion.

- Significant opportunities in both established and emerging industrial sectors.

- Market resilience driven by essential role in operational efficiency and maintenance.

Scale Inhibitor Market Drivers Analysis

The increasing demand for processed water across various industrial applications, including power generation, oil and gas, manufacturing, and municipal water treatment, is a primary driver for the scale inhibitor market. Industries require consistent water quality to prevent equipment damage, reduce maintenance costs, and ensure operational efficiency. Scale inhibitors play a crucial role in preventing mineral deposition, which can lead to reduced flow rates, heat transfer inefficiencies, and costly breakdowns, thereby ensuring the longevity and optimal performance of critical infrastructure. The continuous expansion of these industries globally directly correlates with the rising consumption of scale inhibitors.

Moreover, stringent environmental regulations regarding water discharge and industrial effluent treatment necessitate the use of effective scale management solutions. Companies are compelled to adopt advanced water treatment chemistries, including scale inhibitors, to comply with these regulations and mitigate their environmental footprint. The growth in unconventional oil and gas exploration, such as shale gas and tight oil, further amplifies the demand for specialized scale inhibitors due to the unique water chemistry involved in these processes. These factors collectively create a robust demand environment for scale inhibitor technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industrial Water Demand Growth | +1.5% | Global, particularly Asia Pacific, North America | 2025-2033 |

| Aging Infrastructure & Maintenance Needs | +0.8% | North America, Europe | 2025-2033 |

| Stringent Environmental Regulations | +1.2% | Europe, North America, Asia Pacific | 2025-2033 |

| Expansion of Oil & Gas Sector (Unconventional) | +0.7% | North America, Middle East, Asia Pacific | 2025-2030 |

| Technological Advancements in Water Treatment | +0.5% | Global | 2025-2033 |

Scale Inhibitor Market Restraints Analysis

One significant restraint impacting the scale inhibitor market is the fluctuating prices of raw materials, particularly those derived from petrochemicals. Many common scale inhibitors, such as phosphonates and acrylates, rely on these feedstocks, making their production costs susceptible to volatility in global oil and chemical markets. This instability can directly affect manufacturers' profit margins and lead to higher end-product costs, potentially limiting adoption, especially for smaller industrial players or in regions with constrained budgets. The challenge lies in maintaining competitive pricing while absorbing these variable costs, which can hinder overall market expansion.

Another crucial restraint is the increasing scrutiny and regulation of certain chemical compounds used in scale inhibitors due to environmental and health concerns. Some traditional inhibitors, especially those containing phosphorus, face restrictions due to their potential to contribute to eutrophication in water bodies. This necessitates costly research and development into new, greener alternatives, which can slow down market growth as companies transition to compliant formulations. Furthermore, a lack of awareness or understanding among some end-users regarding the long-term benefits of scale inhibition can also act as a soft restraint, leading to underinvestment in preventative maintenance measures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | 2025-2033 |

| Stringent Environmental Regulations on Chemicals | -0.7% | Europe, North America | 2025-2033 |

| High Initial Investment for Advanced Systems | -0.4% | Developing Regions | 2025-2030 |

| Limited Awareness in Small & Medium Enterprises | -0.3% | Asia Pacific, Latin America | 2025-2033 |

Scale Inhibitor Market Opportunities Analysis

The growing global emphasis on water scarcity and the increasing need for water reuse and recycling present significant opportunities for the scale inhibitor market. As industries and municipalities seek to minimize freshwater consumption and optimize water utility, advanced water treatment processes become critical. Scale inhibitors are indispensable in these processes, preventing fouling in membrane systems (e.g., reverse osmosis) and heat exchangers, thereby enabling efficient and continuous water reclamation. This shift towards a circular water economy creates a sustained and expanding demand for high-performance and specialized scale inhibition solutions.

Furthermore, the emergence of bio-based and green scale inhibitors offers a substantial growth avenue. With mounting environmental concerns and stricter regulations, there is a strong market pull for sustainable chemical alternatives that are biodegradable, non-toxic, and derived from renewable resources. Companies investing in research and development of such innovative, eco-friendly formulations can gain a competitive edge and tap into a rapidly expanding niche. Additionally, the industrialization of developing economies, particularly in Asia Pacific and Latin America, provides untapped potential as new manufacturing plants, power facilities, and water treatment infrastructure are established, requiring robust scale management solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Water Reuse & Recycling Initiatives | +1.0% | Global | 2025-2033 |

| Development of Bio-based & Green Inhibitors | +0.8% | Europe, North America | 2027-2033 |

| Industrialization in Emerging Economies | +0.7% | Asia Pacific, Latin America | 2025-2033 |

| Expansion of Membrane Separation Technologies | +0.6% | Global | 2025-2033 |

| Digitalization & IoT Integration in Water Treatment | +0.5% | Global | 2028-2033 |

Scale Inhibitor Market Challenges Impact Analysis

One primary challenge facing the scale inhibitor market is the increasing complexity of water matrices in various industrial applications. Water sources can contain a diverse range of contaminants and dissolved solids, making it difficult to formulate a single, universally effective scale inhibitor. This necessitates customized solutions for different industries and even specific sites, increasing the complexity and cost of product development and application. The need for highly specialized products means manufacturers must invest more in R&D and technical support, which can slow down market penetration and increase operational overheads.

Another significant challenge is the rising competition from alternative scale prevention technologies, such as physical water treatment methods (e.g., magnetic, electromagnetic, or ultrasonic devices) and advanced filtration systems. While these technologies do not entirely replace chemical inhibitors, they can reduce the reliance on them, particularly in certain applications. Additionally, the industry faces the challenge of educating end-users about the long-term cost benefits of using scale inhibitors versus the immediate perceived cost of chemical treatment. Overcoming resistance to adopting proactive maintenance strategies due to budgetary constraints remains a persistent hurdle, particularly in price-sensitive markets.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Water Chemistry & Customization Needs | -0.5% | Global | 2025-2033 |

| Competition from Alternative Technologies | -0.4% | North America, Europe | 2025-2033 |

| Disposal & Environmental Compliance Costs | -0.3% | Europe, Asia Pacific | 2025-2033 |

| Lack of End-user Awareness & Budget Constraints | -0.2% | Developing Regions | 2025-2033 |

Scale Inhibitor Market - Updated Report Scope

This report provides an in-depth analysis of the global scale inhibitor market, covering historical trends, current market dynamics, and future growth projections. It offers a comprehensive understanding of market size, segmentation by type, application, and end-use industry, alongside regional insights and competitive landscape analysis. The scope extends to critical market drivers, restraints, opportunities, and challenges, offering strategic recommendations for stakeholders to navigate the evolving market effectively. Emphasis is placed on technological advancements, sustainable solutions, and the impact of macro-economic factors influencing market expansion from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.2 billion |

| Market Forecast in 2033 | USD 6.6 billion |

| Growth Rate | 5.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ecolab Inc., BWA Water Additives UK Limited, Solenis LLC, Kurita Water Industries Ltd., Kemira Oyj, SNF Floerger, Arkema SA, ICL Group, Veolia Water Technologies, Suez SA, Buckman Laboratories International Inc., Nouryon, BASF SE, ChemTreat Inc., GE Water & Process Technologies (now SUEZ), Hubbard-Hall Inc., Maxwell Chemicals, Avista Technologies, Thermax Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The scale inhibitor market is comprehensively segmented by type, application, and end-use industry to provide granular insights into its diverse landscape. This detailed segmentation allows for a thorough understanding of the specific chemistries being utilized, the various industrial processes where scale formation is a concern, and the end-user sectors driving the demand. Each segment plays a crucial role in shaping market dynamics, reflecting different operational needs, regulatory environments, and technological preferences. Analyzing these segments provides a clear picture of where growth is concentrated and where specialized solutions are most impactful.

By understanding the nuances within each segment, stakeholders can identify high-potential areas for investment, tailor product development strategies, and optimize market entry approaches. For instance, the dominance of phosphonates in certain applications contrasts with the rising demand for greener carboxylates, reflecting the industry's evolving priorities. Similarly, the diverse applications from cooling towers to complex oil and gas operations highlight the need for a wide range of specialized inhibitor formulations. This multi-faceted segmentation ensures a comprehensive market overview and strategic planning.

- By Type: Phosphonates, Carboxylates/Polymers, Sulfonates, Natural Products, Blends & Other Formulations.

- By Application: Cooling Water Systems, Boiler Water Systems, Membrane Separation (RO/NF), Oil & Gas (Downhole, Production, Transport), Pulp & Paper, Mining & Metallurgy, Power Generation, Desalination, Others.

- By End-Use Industry: Industrial (Manufacturing, Chemicals, Food & Beverage), Oil & Gas, Power Generation, Water Treatment Facilities (Municipal & Industrial), Mining, Pulp & Paper, Textile, Agriculture.

Regional Highlights

- North America: A mature market characterized by significant industrial activity in oil and gas, power generation, and manufacturing. Strict environmental regulations and the adoption of advanced water treatment technologies drive demand for high-performance and environmentally compliant scale inhibitors. The region leads in technological innovation and investment in smart water management solutions.

- Europe: Driven by stringent environmental legislation (e.g., REACH regulations), pushing the demand for sustainable, biodegradable, and low-toxicity scale inhibitors. Robust industrial sectors, including chemicals, power, and manufacturing, contribute significantly. Focus on water reuse and circular economy initiatives further propels market growth.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid industrialization, urbanization, and increasing investments in infrastructure, power generation, and manufacturing facilities, particularly in China, India, and Southeast Asian countries. Growing water scarcity concerns and rising industrial water consumption are key drivers, albeit with varying regulatory landscapes.

- Latin America: Experiencing steady growth due to expanding mining operations, oil and gas exploration, and agricultural processing industries. Increasing foreign direct investment and development of industrial infrastructure contribute to the demand for water treatment chemicals, including scale inhibitors.

- Middle East and Africa (MEA): Dominated by the vast oil and gas industry and a high reliance on desalination plants for freshwater supply, which are significant consumers of scale inhibitors. Increasing industrial diversification and infrastructure development in countries like Saudi Arabia and UAE also contribute to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Scale Inhibitor Market.- Ecolab Inc.

- BWA Water Additives UK Limited

- Solenis LLC

- Kurita Water Industries Ltd.

- Kemira Oyj

- SNF Floerger

- Arkema SA

- ICL Group

- Veolia Water Technologies

- Suez SA

- Buckman Laboratories International Inc.

- Nouryon

- BASF SE

- ChemTreat Inc.

- GE Water & Process Technologies (now SUEZ)

- Hubbard-Hall Inc.

- Maxwell Chemicals

- Avista Technologies

- Thermax Ltd.

Frequently Asked Questions

What are scale inhibitors and why are they important?

Scale inhibitors are chemical compounds designed to prevent the formation and deposition of mineral scales (e.g., calcium carbonate, barium sulfate) on surfaces of industrial equipment, pipelines, and water systems. They are crucial for maintaining operational efficiency, preventing equipment damage, reducing maintenance costs, and ensuring the longevity of industrial assets by preserving heat transfer efficiency and fluid flow.

Which industries are the primary consumers of scale inhibitors?

The primary consumers of scale inhibitors include the oil and gas industry, power generation, manufacturing (chemicals, food & beverage, automotive), municipal and industrial water treatment facilities, mining, pulp & paper, and desalination plants. Any industry utilizing water in its processes where mineral deposition is a concern requires scale inhibition.

What are the key types of scale inhibitors available in the market?

Key types of scale inhibitors include phosphonates, carboxylates/polymers (such as polyacrylates and polymaleates), sulfonates, and natural products like tannins. The choice of inhibitor type depends on the specific water chemistry, operating conditions, and the type of scale being targeted.

How do environmental regulations impact the scale inhibitor market?

Environmental regulations significantly influence the scale inhibitor market by driving the demand for eco-friendly, biodegradable, and low-toxicity formulations. Regulations concerning phosphorus discharge and chemical effluent quality compel manufacturers to innovate and offer sustainable alternatives, fostering a shift away from traditional, less environmentally benign chemistries.

What role does technology play in the future of scale inhibition?

Technology plays a pivotal role in the future of scale inhibition, with advancements in smart dosing systems, real-time monitoring, and predictive analytics (including AI) optimizing inhibitor application and reducing consumption. Furthermore, innovative chemical synthesis and material science are accelerating the development of more effective and sustainable inhibitor formulations, enhancing overall water treatment efficacy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted