Coprocessor Market

Coprocessor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709654 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

Coprocessor Market Size

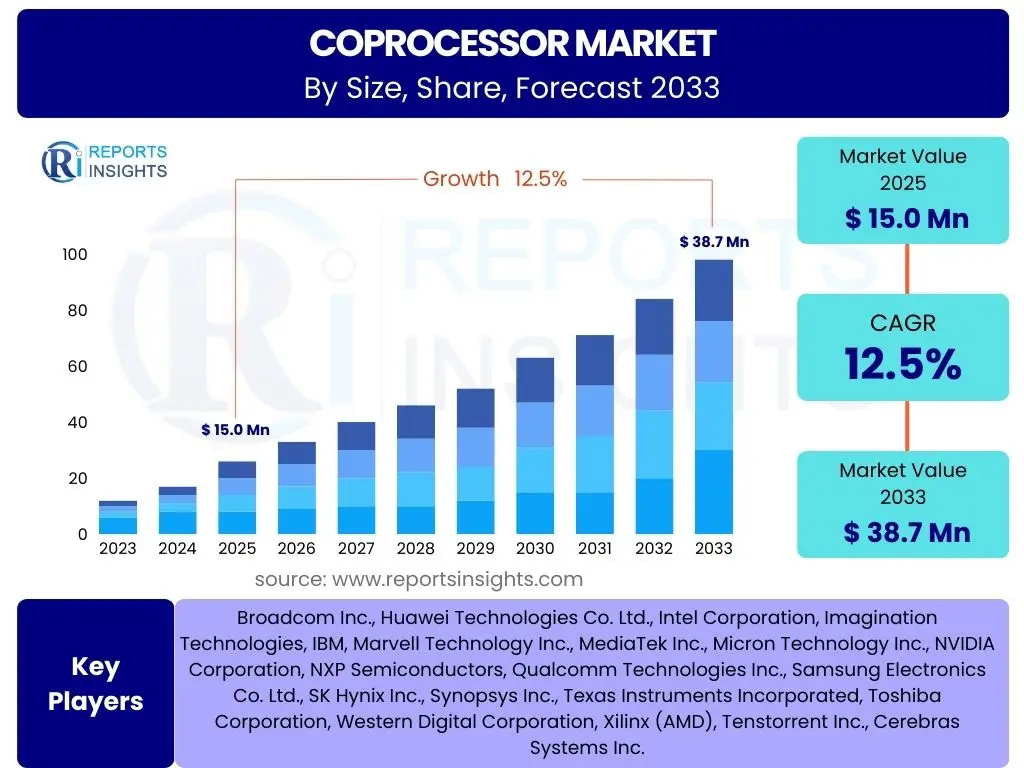

According to Reports Insights Consulting Pvt Ltd, The Coprocessor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 15.0 Billion in 2025 and is projected to reach USD 38.7 Billion by the end of the forecast period in 2033.

Key Coprocessor Market Trends & Insights

User inquiries frequently highlight the escalating demand for specialized processing units capable of handling complex computational tasks more efficiently than general-purpose CPUs. This includes a strong focus on acceleration for artificial intelligence and machine learning workloads, driven by the proliferation of data and the need for faster model training and inference. The shift towards heterogeneous computing architectures, where CPUs work in conjunction with various coprocessors, is a dominant theme, reflecting the industry's pursuit of optimal performance and power efficiency across diverse applications.

Another significant trend is the increasing adoption of coprocessors in edge computing devices and the Internet of Things (IoT). As more data is generated at the edge, there is a critical need for local processing capabilities to reduce latency, conserve bandwidth, and enhance privacy. Users are keenly interested in how these smaller, more power-efficient coprocessors are enabling new applications and services in sectors such as autonomous vehicles, smart manufacturing, and advanced robotics, driving innovation in embedded systems and real-time analytics.

- Accelerated adoption of AI/ML coprocessors for training and inference.

- Increasing integration of specialized processing units in edge computing and IoT devices.

- Growing emphasis on heterogeneous computing architectures to optimize performance and power.

- Development of custom coprocessors for specific industry verticals, such as automotive and healthcare.

- Advancements in power efficiency and miniaturization for embedded and mobile applications.

AI Impact Analysis on Coprocessor

User questions related to the impact of AI on the Coprocessor market predominantly revolve around the capabilities of AI-specific hardware accelerators and their role in the evolving computational landscape. There is a keen interest in how Artificial Intelligence is driving the development of new coprocessor types, such as Neural Processing Units (NPUs) and AI-optimized GPUs, to handle the unique demands of deep learning and machine learning algorithms. Users are also concerned with the performance gains, energy efficiency, and cost implications of these specialized units compared to traditional CPU-centric approaches for AI workloads.

Furthermore, user queries frequently touch upon the integration challenges and the software ecosystem required to fully leverage AI coprocessors. They seek to understand the frameworks, libraries, and tools that support programming and deployment on these specialized hardware architectures. The expectation is that AI will not only redefine the types of coprocessors developed but also fundamentally alter how computing resources are architected, with a stronger emphasis on parallel processing and highly optimized data pipelines to meet the insatiable demands of advanced AI models and applications.

- AI is the primary driver for the innovation and market expansion of specialized coprocessors like NPUs and AI-optimized GPUs.

- Increased demand for energy-efficient coprocessors to handle large-scale AI model training and real-time inference at the edge.

- Development of new architectural paradigms to support AI workloads, emphasizing parallelism and data flow.

- Growing importance of software toolchains and frameworks optimized for AI coprocessors to facilitate adoption and deployment.

- AI is enabling novel applications in autonomous systems, robotics, and smart cities, fueling specific coprocessor requirements.

Key Takeaways Coprocessor Market Size & Forecast

User queries frequently highlight the robust growth trajectory of the Coprocessor market, driven by the relentless pursuit of enhanced computational performance and efficiency across diverse applications. A key takeaway is the increasing recognition of coprocessors as indispensable components for handling data-intensive tasks, particularly in the realm of artificial intelligence, machine learning, and high-performance computing. The market's forecast reflects a sustained demand for specialized hardware that can offload and accelerate specific workloads, thereby augmenting the capabilities of general-purpose processors.

Another significant insight derived from user questions is the strategic importance of coprocessors in enabling next-generation technologies such as autonomous driving, advanced robotics, and sophisticated IoT deployments. The market's expansion is not merely about incremental improvements but about enabling entirely new paradigms of computing. Companies are investing heavily in research and development to create more powerful, energy-efficient, and versatile coprocessors, positioning them as critical enablers for innovation and competitive advantage in the digital economy.

- The Coprocessor market exhibits substantial growth, driven by specialized computational needs across various industries.

- AI and ML applications are pivotal in accelerating the adoption and development of new coprocessor technologies.

- Significant investment in research and development is focused on enhancing power efficiency and performance density.

- Coprocessors are becoming critical enablers for emerging technologies such as autonomous systems and advanced edge computing.

- Market expansion indicates a shift towards heterogeneous computing as a standard for optimal system performance.

Coprocessor Market Drivers Analysis

The global demand for high-performance computing (HPC) across various sectors, including scientific research, financial modeling, and engineering simulations, is a significant driver for the coprocessor market. Modern computational challenges often require massive parallel processing capabilities that traditional CPUs cannot efficiently provide on their own. Coprocessors, such as GPUs and FPGAs, are specifically designed to excel in these parallel tasks, offloading intensive computations from the main processor and dramatically reducing processing times, thereby fostering innovation and driving market growth.

The explosive growth of Artificial Intelligence (AI) and Machine Learning (ML) applications serves as another powerful driver. AI workloads, particularly deep learning training and inference, are inherently compute-intensive and benefit immensely from specialized hardware accelerators. Coprocessors like Neural Processing Units (NPUs) and AI-optimized GPUs are designed to perform the massive matrix multiplications and convolutions required by AI models with high efficiency and low power consumption, making them essential for the widespread deployment of AI across cloud and edge environments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for AI and Machine Learning Acceleration | +4.0% | Global, particularly North America, Asia Pacific (China, India), Europe | Short to Mid-term (2025-2030) |

| Expansion of High-Performance Computing (HPC) and Data Centers | +3.5% | North America, Europe, Asia Pacific | Mid-term (2025-2033) |

| Proliferation of Edge Computing and IoT Devices | +3.0% | Global, especially developing Asia Pacific, Latin America | Short to Mid-term (2025-2030) |

| Growth in Autonomous Vehicles and Advanced Robotics | +2.0% | North America, Europe, Japan, China | Mid to Long-term (2027-2033) |

Coprocessor Market Restraints Analysis

One significant restraint on the coprocessor market is the inherent complexity associated with programming and integrating these specialized hardware units. Unlike general-purpose CPUs which benefit from mature, broadly compatible software ecosystems, coprocessors often require specific programming languages, specialized libraries, and custom development tools. This steep learning curve and the need for highly skilled engineers can increase development costs and time-to-market, thereby hindering broader adoption, especially for smaller enterprises or those with limited technical resources.

Another challenge stems from the rapidly evolving technological landscape and the high research and development costs involved in creating cutting-edge coprocessors. The short product lifecycles in the semiconductor industry mean that significant investments in R&D must be recouped quickly, which can translate to higher prices for end-users. Furthermore, interoperability issues and a lack of universal standards across different coprocessor architectures can lead to vendor lock-in and complicate system design, potentially slowing market expansion by limiting flexibility and increasing integration hurdles for developers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity in Programming and Software Ecosystem Development | -2.0% | Global | Short to Mid-term (2025-2030) |

| High Research and Development Costs and Short Product Lifecycles | -1.5% | Global, particularly impacting smaller innovators | Mid-term (2025-2033) |

| Interoperability Issues and Lack of Universal Standards | -1.0% | Global | Short to Mid-term (2025-2030) |

| Dependency on Fabrication Capabilities and Supply Chain Volatility | -0.8% | Global, particularly North America, Europe, China, Taiwan | Short-term (2025-2027) |

Coprocessor Market Opportunities Analysis

The emergence of 5G technology and the increasing demand for real-time data processing at the network edge present a significant opportunity for the coprocessor market. 5G enables ultra-low latency and massive connectivity, which in turn fuels the need for powerful yet energy-efficient coprocessors embedded within base stations, edge servers, and end-user devices. These coprocessors can accelerate tasks such as network function virtualization, signal processing, and AI inference directly at the source, significantly enhancing the efficiency and responsiveness of 5G-enabled applications and services across various industries.

Another compelling opportunity lies in the development of specialized coprocessors for niche applications within growing industries such as healthcare, aerospace, and advanced manufacturing. For instance, medical imaging, drug discovery, and genomic sequencing require immense computational power for data analysis and simulation, which can be optimally handled by custom-designed coprocessors. Similarly, in aerospace and manufacturing, complex simulations, real-time control systems, and predictive maintenance leverage specialized processing units to achieve unprecedented levels of precision and efficiency, opening new avenues for market expansion and technological innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of 5G Technology and Edge Network Processing | +2.5% | Global, especially North America, Asia Pacific (China, South Korea), Europe | Short to Mid-term (2025-2030) |

| Development of Specialized Coprocessors for Niche Industries (e.g., Healthcare, Aerospace) | +2.0% | North America, Europe, Japan | Mid to Long-term (2027-2033) |

| Advancements in Quantum Computing Coprocessors and Hybrid Systems | +1.5% | North America, Europe, Australia | Long-term (2030-2033) |

| Increased Adoption in Data-Intensive Consumer Electronics (e.g., AR/VR, Gaming) | +1.0% | Global, particularly Asia Pacific, North America, Europe | Short to Mid-term (2025-2030) |

Coprocessor Market Challenges Impact Analysis

A significant challenge impacting the coprocessor market is the issue of power consumption and thermal management, particularly in high-density computing environments like data centers and in compact, power-constrained edge devices. While coprocessors are designed for efficiency in specific tasks, their aggregated power draw and heat generation can be substantial, leading to increased operational costs and complex cooling requirements. Balancing performance with energy efficiency remains a critical engineering hurdle, influencing design choices and limiting the scale of deployment in certain applications.

Another key challenge is the rapidly evolving technological landscape and the threat of technological obsolescence. The semiconductor industry is characterized by fast-paced innovation, with new architectures and processing techniques emerging frequently. This constant evolution means that coprocessors developed today might become less competitive within a few years, requiring continuous investment in research and development to stay relevant. Furthermore, ensuring interoperability with existing CPU architectures and maintaining a robust, accessible software ecosystem across various coprocessor types remains a persistent hurdle for broad market adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Power Consumption and Thermal Management in High-Density Deployments | -1.8% | Global, particularly data centers in all regions | Short to Mid-term (2025-2030) |

| Rapid Technological Obsolescence and Continuous R&D Demands | -1.5% | Global | Mid-term (2025-2033) |

| Shortage of Skilled Workforce for Specialized Hardware and Software Development | -1.2% | North America, Europe, East Asia | Short to Mid-term (2025-2030) |

| Interoperability and Standardization Across Diverse Architectures | -1.0% | Global | Short to Mid-term (2025-2030) |

Coprocessor Market - Updated Report Scope

This report provides an in-depth analysis of the global Coprocessor market, offering a comprehensive understanding of its current state, key trends, and future growth prospects. It encompasses a detailed examination of market size, drivers, restraints, opportunities, and challenges across various segments and geographical regions. The scope includes an assessment of the competitive landscape, highlighting the strategies of leading market players and providing strategic recommendations for stakeholders navigating this dynamic industry. The objective is to equip businesses with actionable insights to inform their strategic decision-making and investment plans within the coprocessor ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.0 Billion |

| Market Forecast in 2033 | USD 38.7 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Broadcom Inc., Huawei Technologies Co. Ltd., Intel Corporation, Imagination Technologies, IBM, Marvell Technology Inc., MediaTek Inc., Micron Technology Inc., NVIDIA Corporation, NXP Semiconductors, Qualcomm Technologies Inc., Samsung Electronics Co. Ltd., SK Hynix Inc., Synopsys Inc., Texas Instruments Incorporated, Toshiba Corporation, Western Digital Corporation, Xilinx (AMD), Tenstorrent Inc., Cerebras Systems Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The coprocessor market is extensively segmented to reflect the diverse technological approaches and application areas. This comprehensive segmentation allows for a granular understanding of market dynamics, revealing specific growth pockets and demand trends within different product types, end-user industries, and geographical regions. The primary segmentation distinguishes between various coprocessor types such as GPUs, FPGAs, ASICs, DSPs, NPUs, and DPUs, each catering to distinct computational requirements and performance benchmarks.

Further segmentation is performed based on critical applications, including Artificial Intelligence & Machine Learning, High-Performance Computing, Data Centers, Automotive, and IoT & Edge Computing, highlighting the broad utility of coprocessors across modern industries. End-user industries such as IT & Telecommunications, Healthcare, and Manufacturing are also delineated, providing insights into sector-specific adoption patterns. This multi-faceted segmentation framework is crucial for identifying market opportunities, understanding competitive landscapes, and tailoring product development strategies to meet evolving market demands.

- By Type: Graphics Processing Unit (GPU), Field-Programmable Gate Array (FPGA), Application-Specific Integrated Circuit (ASIC), Digital Signal Processor (DSP), Neural Processing Unit (NPU), Data Processing Unit (DPU), and Others.

- By Application: Artificial Intelligence (AI) & Machine Learning (ML), High-Performance Computing (HPC), Data Centers & Cloud Computing, Automotive & Autonomous Driving, Internet of Things (IoT) & Edge Computing, Consumer Electronics, Gaming, Medical & Healthcare, Telecommunications, Industrial Automation, and Aerospace & Defense.

- By End-User Industry: IT & Telecommunications, Automotive, Healthcare, Manufacturing, Government & Defense, Education & Research, Financial Services, and Retail.

- By Architecture: x86-based, ARM-based, RISC-V-based, and Proprietary Architectures.

Regional Highlights

- North America: Expected to maintain a significant market share due to substantial investments in advanced R&D, robust presence of key technology companies, and early adoption of AI, ML, and HPC solutions, particularly in data centers and autonomous vehicle development.

- Europe: Anticipated to experience steady growth, driven by strong industrial automation, automotive innovation, and increasing focus on edge computing and IoT applications across various sectors, coupled with initiatives in quantum computing research.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by rapid digital transformation, expanding consumer electronics market, extensive manufacturing base, significant government investments in AI and 5G infrastructure, and a burgeoning data center industry, especially in China, India, Japan, and South Korea.

- Latin America: Emerging market with increasing adoption of cloud computing and digital services, leading to a gradual rise in demand for coprocessors in telecommunications and enterprise segments.

- Middle East and Africa (MEA): Showing nascent growth, driven by diversification efforts into technology, smart city initiatives, and developing data center infrastructure, particularly in the UAE and Saudi Arabia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Coprocessor Market.- Broadcom Inc.

- Huawei Technologies Co. Ltd.

- Intel Corporation

- Imagination Technologies

- IBM

- Marvell Technology Inc.

- MediaTek Inc.

- Micron Technology Inc.

- NVIDIA Corporation

- NXP Semiconductors

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- SK Hynix Inc.

- Synopsys Inc.

- Texas Instruments Incorporated

- Toshiba Corporation

- Western Digital Corporation

- Xilinx (AMD)

- Tenstorrent Inc.

- Cerebras Systems Inc.

Frequently Asked Questions

What is a coprocessor and how does it differ from a CPU?

A coprocessor is a specialized electronic circuit designed to perform specific computational tasks more efficiently than a general-purpose Central Processing Unit (CPU). While a CPU handles a broad range of tasks and general-purpose computations, a coprocessor offloads intensive, specific workloads like graphics rendering (GPU), AI inference (NPU), or data processing (DPU), allowing the CPU to focus on its primary functions. This specialization leads to significant performance gains and power efficiency for the designated tasks.

Why are coprocessors becoming increasingly important for Artificial Intelligence and Machine Learning?

Coprocessors are crucial for AI/ML because these workloads involve massive parallel computations, such as matrix multiplications and convolutions, which are not efficiently handled by traditional CPUs. Specialized coprocessors like Neural Processing Units (NPUs) and Graphics Processing Units (GPUs) are designed with thousands of processing cores optimized for parallel operations, enabling faster training of complex AI models and more efficient real-time inference at both cloud and edge environments, driving the rapid advancement and deployment of AI technologies.

What are the primary types of coprocessors in the market?

The primary types of coprocessors include Graphics Processing Units (GPUs) for graphics and general-purpose parallel computing, Field-Programmable Gate Arrays (FPGAs) for customizable hardware acceleration, Application-Specific Integrated Circuits (ASICs) for highly optimized single-purpose tasks, Digital Signal Processors (DSPs) for signal processing, Neural Processing Units (NPUs) specifically for AI workloads, and Data Processing Units (DPUs) for network and data infrastructure acceleration. Each type is tailored for distinct computational demands.

How do coprocessors contribute to the growth of edge computing and IoT?

Coprocessors are vital for edge computing and IoT by enabling local, real-time data processing and analysis on devices close to the data source. They provide the necessary computational power and energy efficiency to perform tasks like AI inference, sensor data fusion, and complex analytics directly on edge devices, reducing reliance on cloud connectivity. This allows for lower latency, enhanced privacy, reduced bandwidth usage, and greater autonomy for IoT devices and edge systems, fostering the expansion of smart environments.

What are the key challenges faced by the Coprocessor market?

Key challenges for the Coprocessor market include the inherent complexity of programming and integrating specialized hardware, demanding a highly skilled workforce. High research and development costs coupled with short product lifecycles pose financial risks. Furthermore, managing power consumption and thermal dissipation, especially in dense computing environments, remains a significant engineering hurdle. Interoperability issues and the need for greater standardization across diverse architectures also present persistent challenges to widespread adoption and market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted