Copper Pipe and Tube Market

Copper Pipe and Tube Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709199 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

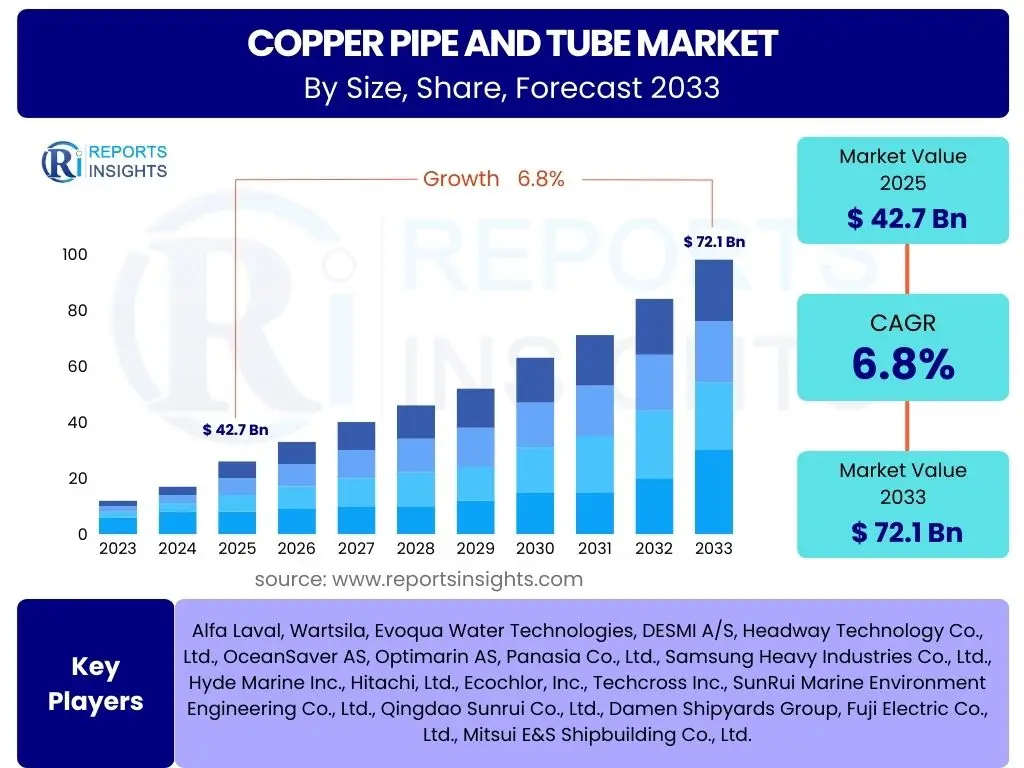

Copper Pipe and Tube Market Size

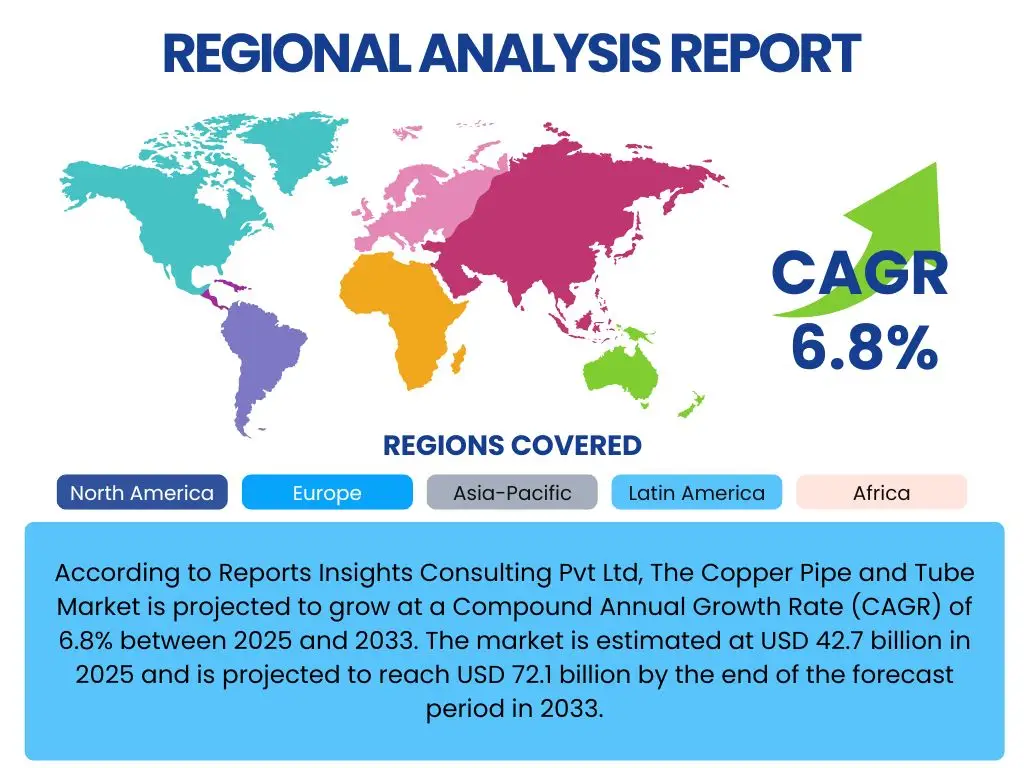

According to Reports Insights Consulting Pvt Ltd, The Copper Pipe and Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 42.7 billion in 2025 and is projected to reach USD 72.1 billion by the end of the forecast period in 2033.

Key Copper Pipe and Tube Market Trends & Insights

The copper pipe and tube market is currently shaped by several dynamic trends reflecting global economic shifts, technological advancements, and evolving consumer and industrial demands. Primary user queries often revolve around the market's response to fluctuating raw material prices, the increasing adoption of sustainable building practices, and the impact of rapid urbanization in emerging economies. There is also significant interest in how technological innovations, particularly in manufacturing processes and material science, are influencing product development and market competitiveness.

Furthermore, the drive towards energy efficiency and the expansion of the HVACR (Heating, Ventilation, Air Conditioning, and Refrigeration) sector are major themes, with users seeking insights into how these factors are driving demand for specialized copper products. The shift towards electrification in various industries, coupled with renewed investment in infrastructure projects, presents both opportunities and challenges that define the current market trajectory. Understanding these underlying trends is crucial for stakeholders navigating the complexities of the copper pipe and tube industry.

- Increasing demand from HVACR systems due to global warming and urbanization.

- Growth in sustainable and green building initiatives driving demand for durable materials.

- Technological advancements in manufacturing leading to enhanced product performance and efficiency.

- Fluctuating copper prices influencing market stability and procurement strategies.

- Expansion of plumbing and electrical infrastructure in developing economies.

- Rising adoption of pre-insulated copper pipes for energy conservation.

AI Impact Analysis on Copper Pipe and Tube

The integration of Artificial Intelligence (AI) across industrial sectors, including the copper pipe and tube manufacturing domain, is a recurring theme in user inquiries. Common questions address AI's role in optimizing production processes, enhancing quality control, and improving supply chain management. Stakeholders are particularly interested in how AI algorithms can predict equipment failures, minimize waste, and streamline inventory, thereby reducing operational costs and increasing overall efficiency within manufacturing facilities.

Beyond manufacturing, AI is also being explored for its potential in predictive analytics for market demand forecasting and raw material price fluctuations, which is crucial given copper's volatility. Its application in designing new alloys or optimizing pipe geometries for specific performance requirements is an emerging area. While the direct, widespread adoption is still in early stages, the expectation is that AI will play a transformative role in driving automation, smart factories, and data-driven decision-making, ultimately impacting product quality, cost-efficiency, and market responsiveness.

- Enhanced predictive maintenance for manufacturing equipment, reducing downtime.

- Optimized production scheduling and resource allocation for increased efficiency.

- Improved quality control through AI-powered visual inspection systems.

- Advanced demand forecasting and inventory management, minimizing waste and holding costs.

- Supply chain optimization, from raw material sourcing to final product distribution.

- Facilitation of digital twins for virtual prototyping and process simulation.

Key Takeaways Copper Pipe and Tube Market Size & Forecast

Key takeaways from the Copper Pipe and Tube market size and forecast consistently highlight the robust growth trajectory, driven by fundamental industrial and societal needs. User questions frequently focus on the underlying drivers for this expansion, particularly in the context of global construction booms and the persistent demand for efficient heat transfer solutions. The projected market value and Compound Annual Growth Rate (CAGR) underscore a resilient sector poised for sustained expansion through the forecast period, reflecting ongoing urbanization, industrialization, and infrastructure development worldwide.

Furthermore, critical insights emphasize the increasing importance of sustainability and energy efficiency in driving product innovation and market acceptance. The market's future is strongly linked to advancements in HVACR technologies, the push for greener buildings, and the stability of global economic conditions. Understanding these core elements is essential for strategic planning, investment decisions, and navigating the evolving landscape of copper pipe and tube manufacturing and distribution.

- Significant market expansion expected, driven by infrastructure and building sectors.

- HVACR applications remain a primary growth engine for copper tube demand.

- Technological innovations in copper alloys and manufacturing processes will enhance market value.

- Sustainability trends are influencing material choices and product development.

- Volatile raw material prices require robust risk management strategies for market participants.

Copper Pipe and Tube Market Drivers Analysis

The copper pipe and tube market is significantly propelled by several key drivers, primarily the escalating global demand from the construction and infrastructure sectors. Rapid urbanization, particularly in emerging economies, necessitates extensive plumbing, heating, and cooling systems in both residential and commercial buildings. This consistent requirement for reliable and durable fluid conveyance solutions underpins a substantial portion of the market's growth, making it less susceptible to short-term economic fluctuations.

Another crucial driver is the burgeoning HVACR industry, where copper tubes are indispensable for their excellent thermal conductivity and corrosion resistance. As global temperatures rise and living standards improve, the adoption of air conditioning and refrigeration units increases, directly translating into higher demand for copper components. Additionally, the shift towards energy-efficient systems and environmentally friendly refrigerants often favors copper for its performance characteristics and recyclability, further stimulating market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Construction and Infrastructure Development | +2.1% | Asia Pacific, Middle East & Africa | 2025-2033 (Long-term) |

| Rising Demand from HVACR Industry | +1.8% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Increasing Focus on Energy Efficiency and Green Buildings | +1.5% | Europe, North America | 2025-2030 (Medium-term) |

| Expansion of Industrial Sector and Automotive Production | +1.4% | Asia Pacific, Europe | 2025-2033 (Long-term) |

Copper Pipe and Tube Market Restraints Analysis

Despite its robust growth drivers, the copper pipe and tube market faces significant restraints that can temper its expansion. Foremost among these is the volatility in raw copper prices, which are subject to global supply-demand dynamics, geopolitical events, and speculative trading. These price fluctuations directly impact manufacturing costs and product pricing, leading to uncertainty for both producers and consumers, and can sometimes prompt a shift towards alternative materials when copper becomes prohibitively expensive.

Furthermore, intense competition from alternative materials such as PEX, PVC, stainless steel, and aluminum poses a continuous challenge. While copper offers superior properties for many applications, these substitutes often present lower cost, easier installation, or specific advantages in certain niches. Stringent environmental regulations and high initial investment costs for setting up advanced manufacturing facilities also act as significant barriers, particularly for new entrants or smaller players trying to scale operations effectively.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Copper Prices | -1.7% | Global | 2025-2033 (Continuous) |

| Competition from Alternative Materials (PEX, Stainless Steel) | -1.2% | North America, Europe | 2025-2030 (Medium-term) |

| High Capital Investment for Manufacturing Facilities | -0.9% | Emerging Markets | 2025-2033 (Long-term) |

| Stringent Environmental Regulations on Mining and Production | -0.8% | Europe, North America | 2025-2030 (Medium-term) |

Copper Pipe and Tube Market Opportunities Analysis

The copper pipe and tube market is rich with opportunities stemming from evolving technological landscapes and increasing global demands. One significant area is the growing adoption of smart building technologies and integrated IoT systems, which require reliable and durable conduits for efficient energy transfer and data communication. This trend creates a niche for specialized copper products that can integrate seamlessly with advanced infrastructure, driving innovation in material properties and connectivity solutions.

Moreover, the global push towards renewable energy sources and electric vehicles presents a substantial long-term opportunity. Copper's excellent electrical conductivity makes it indispensable in wind turbines, solar panels, and electric vehicle charging infrastructure, as well as in the vehicles themselves. Furthermore, the expansion of district heating and cooling systems in urban areas, driven by sustainability goals, offers new avenues for high-performance copper tubing. These opportunities require market players to invest in research and development, adapt to new technical specifications, and forge strategic partnerships to capitalize on these emerging sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Renewable Energy and Electric Vehicle Sectors | +1.9% | Global | 2026-2033 (Long-term) |

| Development of Smart Cities and Green Infrastructure Projects | +1.6% | Asia Pacific, Europe | 2025-2033 (Long-term) |

| Technological Advancements in HVACR Systems (e.g., Micro-channel coils) | +1.3% | North America, Europe, Asia Pacific | 2025-2030 (Medium-term) |

| Increasing Demand for Pre-insulated and Customized Copper Solutions | +1.0% | Global | 2025-2033 (Long-term) |

Copper Pipe and Tube Market Challenges Impact Analysis

The copper pipe and tube market faces several inherent challenges that demand strategic responses from industry participants. One prominent challenge is the increasingly complex global supply chain, which is susceptible to disruptions from geopolitical tensions, trade disputes, and natural disasters. These factors can lead to raw material shortages, increased logistics costs, and delays in product delivery, impacting manufacturing schedules and market stability. Maintaining a resilient and efficient supply chain is critical for mitigating these risks and ensuring consistent market operation.

Another significant challenge involves escalating environmental compliance costs and the pressure to adopt more sustainable manufacturing practices. While beneficial in the long term, adhering to stricter regulations regarding emissions, waste management, and resource efficiency often requires substantial investments in new technologies and processes. Additionally, the availability of skilled labor for specialized copper manufacturing and installation can be a bottleneck, particularly in regions experiencing rapid infrastructure development. Addressing these challenges necessitates continuous investment in innovation, workforce development, and strategic partnerships across the value chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Geopolitical Instability | -1.5% | Global | 2025-2030 (Medium-term) |

| Rising Energy and Operational Costs for Manufacturing | -1.1% | Europe, Asia Pacific | 2025-2033 (Long-term) |

| Availability and Cost of Skilled Labor | -0.8% | North America, Europe | 2025-2030 (Medium-term) |

| Product Substitution Risk in Price-Sensitive Applications | -0.7% | Emerging Markets | 2025-2033 (Long-term) |

Copper Pipe and Tube Market - Updated Report Scope

This market research report provides a comprehensive analysis of the global copper pipe and tube market, offering detailed insights into market dynamics, segmentation, regional landscapes, and competitive strategies. The scope encompasses an in-depth review of historical trends, current market performance, and future projections, aiming to equip stakeholders with a clear understanding of the industry's potential and challenges. The report evaluates market size, growth rate, key drivers, restraints, opportunities, and challenges across various segments and geographic regions to facilitate informed decision-making for businesses, investors, and policymakers.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 42.7 Billion |

| Market Forecast in 2033 | USD 72.1 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Major integrated copper product manufacturers, Specialized tube producers, HVACR component suppliers, Plumbing material providers, Electrical conduit manufacturers, Construction material distributors, Automotive component suppliers, Industrial heat exchanger fabricators, International commodity traders, Regional market leaders, Small and medium-sized enterprises (SMEs) focusing on niche applications, Recycling and re-processing companies, Innovative materials technology developers, Supply chain solution providers, Engineering and design firms. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The copper pipe and tube market is comprehensively segmented to provide a granular view of its diverse components and applications. This segmentation allows for precise analysis of market dynamics, identifying specific areas of growth, opportunity, and challenge within the industry. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions to specific market needs and demands, ensuring targeted and effective market penetration.

- By Type: Seamless, Welded, LWC (Level Wound Coils), ACR Tubes, Plumbing Tubes, Electrical Tubes

- By Material Grade: C101 (Oxygen-Free High Conductivity), C106 (Phosphor Deoxidized Non-Arsenical), C12200 (DHP Copper)

- By Application: HVAC & Refrigeration, Plumbing, Electrical & Electronics, Industrial Heat Exchangers, Automotive, Construction (Residential, Commercial, Industrial, Infrastructure)

- By End-Use Industry: Residential, Commercial, Industrial, Infrastructure, Automotive, Power Generation

- By Diameter: Small Diameter, Medium Diameter, Large Diameter

Regional Highlights

- Asia Pacific (APAC): Dominant market share due to rapid urbanization, extensive infrastructure development, and burgeoning manufacturing industries, particularly in China and India. High growth in HVACR and construction sectors.

- North America: Mature market with consistent demand driven by residential and commercial construction, HVACR upgrades, and automotive sector. Focus on energy efficiency and replacement of aging infrastructure.

- Europe: Strong emphasis on sustainable building practices, renovation projects, and district heating/cooling systems. Germany, UK, and France are key contributors, driven by environmental regulations and industrial applications.

- Latin America: Emerging growth driven by industrialization, housing projects, and expansion of refrigeration markets. Brazil and Mexico are significant regional players.

- Middle East & Africa (MEA): Significant investments in construction and tourism infrastructure, coupled with hot climates driving HVACR demand. Saudi Arabia, UAE, and South Africa are key growth areas.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Copper Pipe and Tube Market.- Integrated Copper Product Manufacturers

- Specialized Tube Producers

- HVACR Component Suppliers

- Plumbing Material Providers

- Electrical Conduit Manufacturers

- Construction Material Distributors

- Automotive Component Suppliers

- Industrial Heat Exchanger Fabricators

- International Commodity Traders

- Regional Market Leaders

- Small and Medium-sized Enterprises (SMEs) focusing on niche applications

- Recycling and Re-processing Companies

- Innovative Materials Technology Developers

- Supply Chain Solution Providers

- Engineering and Design Firms

- Advanced Manufacturing Solutions Providers

- Global Metallurgical Corporations

- Precision Tube Specialists

- Building Materials Conglomerates

- Infrastructure Project Suppliers

Frequently Asked Questions

What is the projected growth rate for the Copper Pipe and Tube Market?

The Copper Pipe and Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033.

Which factors are primarily driving the demand for copper pipes and tubes?

Key drivers include rapid growth in the construction and infrastructure sectors, increasing demand from the HVACR industry, and a global focus on energy efficiency and green building initiatives.

What are the main challenges faced by the copper pipe and tube market?

Major challenges include the volatility of raw copper prices, intense competition from alternative materials, and potential disruptions in the global supply chain.

How is AI expected to impact the copper pipe and tube industry?

AI is anticipated to enhance manufacturing efficiency through predictive maintenance, optimize production and supply chain management, and improve quality control processes.

Which region holds the largest market share for copper pipes and tubes?

The Asia Pacific region currently holds the largest market share, driven by extensive urbanization and infrastructure development, particularly in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted