Copper Alloy Foil Market

Copper Alloy Foil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702775 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Copper Alloy Foil Market Size

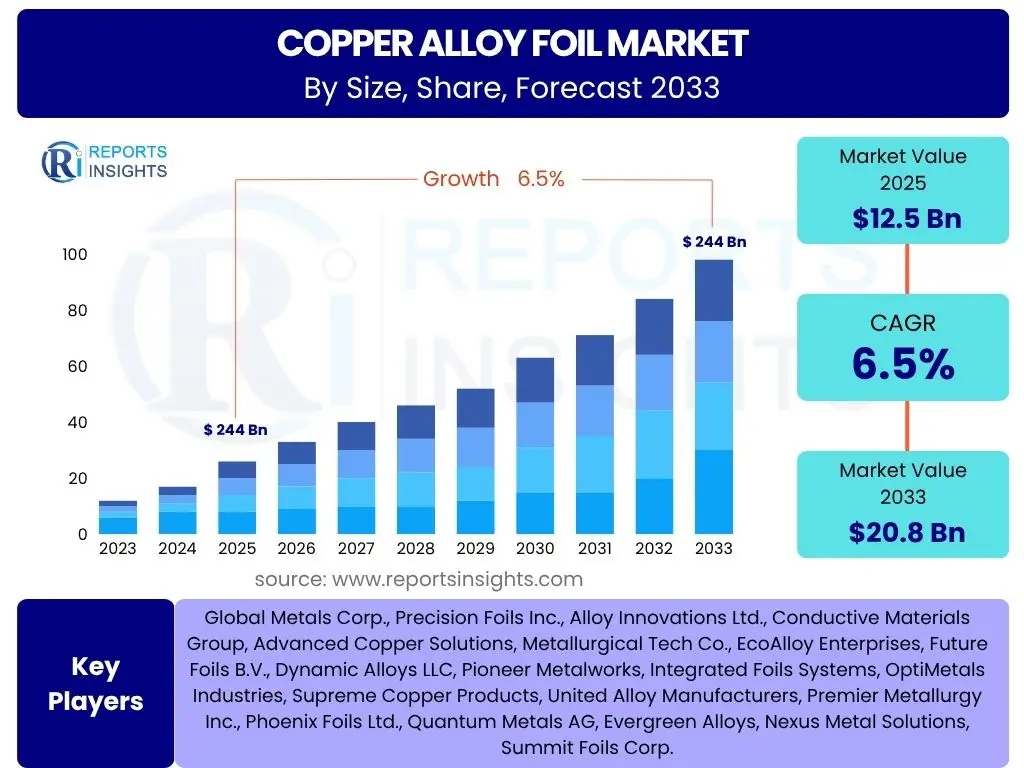

According to Reports Insights Consulting Pvt Ltd, The Copper Alloy Foil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 20.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by increasing demand across various end-use industries, including electronics, automotive, and industrial applications. The inherent properties of copper alloy foil, such as excellent electrical conductivity, thermal conductivity, corrosion resistance, and malleability, make it indispensable in modern technological advancements and traditional manufacturing processes.

The market's expansion is further bolstered by global trends towards miniaturization in electronic components, the rapid proliferation of electric vehicles (EVs), and significant investments in telecommunications infrastructure, particularly 5G networks. These sectors require high-performance, lightweight, and durable materials, which copper alloy foils effectively provide. Regional economic developments and governmental support for manufacturing sectors also contribute to the positive market outlook, fostering innovation and enhancing production capabilities.

Key Copper Alloy Foil Market Trends & Insights

Users frequently inquire about the evolving landscape of the Copper Alloy Foil market, seeking to understand the most impactful shifts and innovations. Common questions revolve around emerging applications, regulatory influences, and technological advancements. Analysis reveals a prominent trend towards ultra-thin foils driven by miniaturization in consumer electronics and advanced packaging solutions for semiconductors. The market is also heavily influenced by the transition to electric vehicles, which require significant amounts of copper alloy foil for battery components and electrical systems. Sustainability initiatives and the push for a circular economy are increasingly shaping production processes and material selection, with a growing emphasis on recyclable and energy-efficient manufacturing.

Furthermore, the rapid deployment of 5G infrastructure globally is creating substantial demand for high-frequency and high-performance copper alloy foils for telecommunication equipment. Automation and digitalization in manufacturing processes are improving efficiency and precision, leading to higher quality products. Geopolitical factors and supply chain resilience are also critical considerations, prompting market players to diversify sourcing and enhance operational flexibility. These converging trends highlight a dynamic market poised for sustained growth, albeit with evolving challenges related to material sourcing, environmental compliance, and technological integration.

- Miniaturization of electronic components driving demand for ultra-thin foils.

- Increased adoption of electric vehicles (EVs) boosting consumption in battery and electrical systems.

- Rapid deployment of 5G infrastructure creating new opportunities in telecommunications.

- Growing emphasis on sustainable and recyclable material solutions in manufacturing.

- Advancements in material science leading to specialized alloy formulations with enhanced properties.

- Integration of smart manufacturing processes for improved efficiency and quality control.

- Diversification of supply chains to mitigate geopolitical and trade risks.

AI Impact Analysis on Copper Alloy Foil

Users frequently explore the transformative potential of Artificial Intelligence (AI) within the Copper Alloy Foil industry, often asking how AI can optimize production, enhance quality, and influence market dynamics. The consensus indicates that AI is poised to revolutionize several aspects of the industry, from raw material inspection to final product quality assurance. AI-driven predictive analytics can forecast equipment failures, optimize maintenance schedules, and improve energy efficiency in production lines, leading to significant cost reductions and improved operational uptime. Furthermore, machine learning algorithms can analyze vast datasets from manufacturing processes to identify optimal parameters for alloying, rolling, and annealing, thereby enhancing material properties and reducing waste.

Beyond process optimization, AI is also impacting research and development by accelerating the discovery of new alloy compositions with tailored properties for emerging applications. Generative design and simulation tools powered by AI allow for rapid prototyping and testing of theoretical materials, significantly shortening development cycles. While concerns exist regarding the initial investment costs and the need for specialized skills, the long-term benefits of AI in terms of enhanced productivity, superior product quality, and improved resource utilization are widely acknowledged. AI’s influence extends to supply chain management, enabling more accurate demand forecasting, inventory optimization, and resilient logistics, ensuring a more responsive and efficient market overall.

- Enhanced material design and discovery through AI-powered simulation and generative design.

- Optimized manufacturing processes via predictive analytics for improved efficiency and reduced waste.

- Automated quality inspection systems utilizing computer vision for superior product consistency.

- Predictive maintenance for machinery, minimizing downtime and extending equipment lifespan.

- Improved supply chain predictability and resilience through AI-driven forecasting and logistics.

- Energy consumption optimization in production facilities for reduced operational costs and environmental impact.

- Development of smart materials with self-monitoring capabilities, enabled by embedded AI.

Key Takeaways Copper Alloy Foil Market Size & Forecast

Common user inquiries about the Copper Alloy Foil market size and forecast center on understanding the most significant growth drivers, the trajectory of market expansion, and the key regions poised for substantial development. Analysis indicates that the market is on a robust upward trajectory, primarily fueled by the relentless technological advancements in electronics and the transformative shift in the automotive industry towards electric mobility. The essential role of copper alloy foil in Printed Circuit Boards (PCBs), battery components, and advanced electronic packaging ensures sustained demand. Moreover, the global push for renewable energy infrastructure and smart city development further contributes to its long-term growth prospects, requiring high-performance conductive materials.

The market's resilience is also attributed to its versatility, with applications expanding into new sectors such as medical devices and aerospace lightweighting solutions. While raw material price volatility and environmental regulations present ongoing challenges, continuous innovation in material science and manufacturing processes is helping to mitigate these risks. Asia Pacific is expected to remain the dominant market, driven by its expansive electronics manufacturing base and burgeoning automotive sector, while North America and Europe will see steady growth supported by R&D investments and high-value applications. The overall outlook is highly positive, with strategic investments in technology and sustainable practices being crucial for market participants to capitalize on future opportunities.

- Strong market growth driven by electronics miniaturization and electric vehicle adoption.

- Asia Pacific retains dominance due to significant manufacturing capabilities and demand.

- Technological advancements in alloy composition and processing methods are crucial for market competitiveness.

- Sustainability and recycling initiatives are increasingly influencing production and material choices.

- Diversification into emerging applications like medical devices and aerospace offers new growth avenues.

- Supply chain resilience and stable raw material sourcing are critical success factors.

- The market is poised for long-term expansion, supported by global infrastructure development and digitalization.

Copper Alloy Foil Market Drivers Analysis

The Copper Alloy Foil market is experiencing significant propulsion from several key drivers, primarily stemming from the increasing sophistication and demand across various high-growth industries. The relentless miniaturization in the electronics sector mandates thinner, more conductive, and higher-performance materials for components like printed circuit boards and connectors. This push towards advanced electronic devices, coupled with the global rollout of 5G technology, creates an insatiable demand for specialized copper alloy foils capable of handling high frequencies and complex signal integrity requirements. Furthermore, the global automotive industry's rapid transition towards electric vehicles (EVs) is a monumental driver. EVs require substantial quantities of copper alloy foil for battery current collectors, busbars, and various electrical systems, significantly increasing per-vehicle copper content compared to traditional internal combustion engine vehicles.

Beyond electronics and automotive, the escalating global investment in renewable energy infrastructure, including solar panels and wind turbines, also necessitates durable and highly conductive copper materials. Industrial automation and robotics, driven by the Fourth Industrial Revolution, create demand for precise and reliable electrical contacts and components. Additionally, the inherent properties of copper alloy foils, such as superior thermal and electrical conductivity, excellent corrosion resistance, and high strength-to-weight ratio, make them indispensable for these critical applications. Continuous innovation in alloy formulations and manufacturing processes further enhances the performance characteristics of these foils, broadening their applicability and solidifying their market position. The synergistic effect of these drivers creates a strong foundation for sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand from Electric Vehicles (EVs) | +1.8-2.2% | North America, Europe, China, Japan | Mid-to-Long Term (2025-2033) |

| Miniaturization in Consumer Electronics | +1.5-1.9% | Asia Pacific (South Korea, Taiwan, China, Japan) | Mid-to-Long Term (2025-2033) |

| Global 5G Network Expansion | +1.2-1.6% | Global, particularly Asia Pacific, North America | Mid-to-Long Term (2025-2033) |

| Growth in Renewable Energy Infrastructure | +0.9-1.3% | Europe, North America, China, India | Mid-to-Long Term (2025-2033) |

| Advancements in Industrial Automation and Robotics | +0.7-1.1% | Germany, Japan, South Korea, USA | Mid-to-Long Term (2025-2033) |

| Increased Adoption of Medical Devices | +0.5-0.8% | North America, Europe | Mid-to-Long Term (2025-2033) |

| Investment in Smart Grid Technology | +0.4-0.7% | North America, Europe, India | Mid-to-Long Term (2025-2033) |

Copper Alloy Foil Market Restraints Analysis

Despite robust growth drivers, the Copper Alloy Foil market faces several notable restraints that could impact its expansion trajectory. One of the primary concerns is the volatility of raw material prices, particularly copper. Global copper prices are subject to fluctuations driven by supply-demand imbalances, geopolitical events, mining disruptions, and currency exchange rates. Such instability directly affects the production costs of copper alloy foils, leading to unpredictable pricing for end-users and potentially narrowing profit margins for manufacturers. This price volatility can deter long-term investment and planning within the industry. Furthermore, the energy-intensive nature of copper production and foil manufacturing processes contributes significantly to operational costs, especially in regions with high energy prices or limited access to sustainable energy sources, adding another layer of cost-related restraint.

Stringent environmental regulations regarding mining, smelting, and manufacturing processes, particularly in developed economies, pose another significant challenge. These regulations, aimed at reducing carbon emissions, waste generation, and pollution, necessitate substantial investments in cleaner technologies and compliance measures. While beneficial for the environment, they can increase operational expenditure for manufacturers and may restrict expansion in certain regions. Moreover, competition from alternative materials, such as aluminum, graphene, or advanced polymers, for certain applications, especially where lightweighting or specific non-conductive properties are paramount, presents a substitution threat. Although copper's unique combination of properties makes direct substitution difficult in many critical applications, ongoing R&D in alternative materials could erode market share in specific niches. Finally, trade barriers and protectionist policies enacted by various countries can disrupt global supply chains, increase import duties, and create market access challenges, hindering the free flow of goods and impacting market efficiency.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Copper Raw Material Prices | -1.5-1.9% | Global | Mid-to-Long Term (2025-2033) |

| Stringent Environmental Regulations | -1.0-1.4% | Europe, North America, China | Mid-to-Long Term (2025-2033) |

| Competition from Alternative Materials | -0.8-1.2% | Global | Mid-to-Long Term (2025-2033) |

| High Energy Consumption in Manufacturing | -0.7-1.1% | Europe, Asia Pacific | Mid-to-Long Term (2025-2033) |

| Geopolitical Tensions and Trade Barriers | -0.6-0.9% | Global, specific trade blocs | Short-to-Mid Term (2025-2028) |

| Supply Chain Disruptions | -0.5-0.8% | Global | Short-to-Mid Term (2025-2027) |

| Intellectual Property Infringement | -0.3-0.6% | Asia Pacific, Emerging Markets | Long Term (2028-2033) |

Copper Alloy Foil Market Opportunities Analysis

The Copper Alloy Foil market is presented with significant opportunities for growth and innovation, particularly through advancements in new application areas and the development of specialized materials. One major avenue lies in the burgeoning field of advanced packaging for semiconductors, where ultra-thin and high-purity copper alloy foils are crucial for improved performance and miniaturization of electronic devices. The continuous evolution of medical technology also offers a promising niche; copper alloy foils are increasingly being utilized in medical imaging equipment, diagnostic tools, and even antimicrobial surfaces due to copper's inherent antibacterial properties. Furthermore, the global drive towards lightweighting in aerospace and automotive industries, beyond just EVs, encourages the development of higher strength-to-weight ratio copper alloys, opening up new design possibilities for critical components.

Geographically, emerging economies in Southeast Asia, Latin America, and parts of Africa represent untapped markets with rapidly expanding industrial bases and increasing demand for electronics and infrastructure. Investment in these regions, coupled with localized manufacturing capabilities, can unlock substantial market potential. The growing focus on circular economy principles and sustainable manufacturing practices also presents an opportunity for companies to differentiate themselves by developing advanced recycling technologies for copper alloys and promoting the use of recycled content in their products. This not only aligns with environmental goals but also helps in mitigating raw material supply risks. Additionally, collaborative research and development efforts between material scientists, manufacturers, and end-users can lead to breakthrough innovations in alloy design and processing, creating new, high-value applications for copper alloy foils across diverse industries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advanced Packaging for Semiconductors | +1.7-2.1% | Asia Pacific (Taiwan, South Korea, China) | Mid-to-Long Term (2025-2033) |

| Emerging Medical Device Applications | +1.3-1.7% | North America, Europe, Japan | Mid-to-Long Term (2025-2033) |

| Aerospace and Defense Lightweighting Initiatives | +1.1-1.5% | North America, Europe | Mid-to-Long Term (2025-2033) |

| Expansion into Untapped Emerging Markets | +0.9-1.3% | Southeast Asia, Latin America, Africa | Long Term (2028-2033) |

| Development of Sustainable Recycling Technologies | +0.7-1.0% | Global | Mid-to-Long Term (2025-2033) |

| Smart City and IoT Infrastructure Development | +0.6-0.9% | Global, particularly China, Europe | Mid-to-Long Term (2025-2033) |

| High-Performance Computing (HPC) Systems | +0.5-0.8% | North America, Europe, Asia Pacific | Mid-to-Long Term (2025-2033) |

Copper Alloy Foil Market Challenges Impact Analysis

The Copper Alloy Foil market faces several complex challenges that demand strategic responses from industry players to maintain growth momentum and competitiveness. One significant challenge is the inherent fragility and long lead times associated with the global supply chain for raw copper and specialized alloy components. Geopolitical instability, natural disasters, or unexpected demand surges can lead to supply disruptions, impacting production schedules and delivery commitments. Ensuring a resilient and diversified supply network is paramount for manufacturers to mitigate these risks. Additionally, the increasing focus on Environmental, Social, and Governance (ESG) compliance presents both a challenge and an opportunity. While crucial for sustainability, adhering to evolving ESG standards, particularly concerning responsible sourcing of raw materials and reducing carbon footprint, often requires substantial investment in new technologies and operational adjustments, potentially increasing costs and complexity for businesses.

Another critical challenge lies in the high research and development (R&D) costs associated with developing new copper alloy formulations and advanced manufacturing techniques (e.g., ultra-thin foil production). To meet the stringent performance requirements of cutting-edge applications in electronics and automotive, continuous innovation is essential, but it comes with considerable financial outlay and long development cycles. Moreover, the scarcity of skilled labor, particularly experts in metallurgy, advanced manufacturing, and data analytics for AI integration, poses a significant hurdle. Companies struggle to find and retain talent capable of operating complex machinery, optimizing processes, and driving technological innovation. Finally, the growing threat of counterfeit products, particularly in high-value applications, undermines brand reputation, erodes market share, and poses safety risks, necessitating robust intellectual property protection and vigilant market monitoring strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Fragility and Disruptions | -1.3-1.7% | Global | Short-to-Mid Term (2025-2028) |

| Meeting Stringent ESG Compliance Standards | -1.0-1.4% | Europe, North America | Mid-to-Long Term (2025-2033) |

| High Research and Development Costs | -0.8-1.2% | Global | Mid-to-Long Term (2025-2033) |

| Scarcity of Skilled Labor and Talent | -0.7-1.1% | Global, particularly developed economies | Mid-to-Long Term (2025-2033) |

| Counterfeit Products and Intellectual Property Theft | -0.5-0.9% | Asia Pacific, Emerging Markets | Long Term (2028-2033) |

| Cybersecurity Risks in Automated Manufacturing | -0.4-0.7% | Global | Mid-to-Long Term (2025-2033) |

| Waste Management and Disposal of By-products | -0.3-0.6% | Global | Mid-to-Long Term (2025-2033) |

Copper Alloy Foil Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Copper Alloy Foil market, offering detailed insights into its current size, historical performance, and future growth projections. The scope includes a thorough examination of key market trends, significant drivers, limiting restraints, emerging opportunities, and prevailing challenges influencing the industry landscape. Special attention is paid to the impact of artificial intelligence on manufacturing processes and market dynamics. The report segments the market by various criteria, including alloy type, application, thickness, and end-use industry, to provide a granular understanding of market dynamics across different verticals. A detailed regional analysis highlights growth opportunities and market specifics across major geographical areas, while a competitive landscape section profiles key market players, their strategies, and recent developments. This report serves as a vital resource for stakeholders seeking to make informed strategic decisions and gain a competitive edge in the evolving Copper Alloy Foil market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 20.8 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Metals Corp., Precision Foils Inc., Alloy Innovations Ltd., Conductive Materials Group, Advanced Copper Solutions, Metallurgical Tech Co., EcoAlloy Enterprises, Future Foils B.V., Dynamic Alloys LLC, Pioneer Metalworks, Integrated Foils Systems, OptiMetals Industries, Supreme Copper Products, United Alloy Manufacturers, Premier Metallurgy Inc., Phoenix Foils Ltd., Quantum Metals AG, Evergreen Alloys, Nexus Metal Solutions, Summit Foils Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Copper Alloy Foil market is comprehensively segmented to provide granular insights into its diverse components, allowing for a precise understanding of market dynamics across various categories. This segmentation helps stakeholders identify key growth areas, understand specific demand drivers, and tailor their strategies to target particular niches within the broader market. The breakdown by alloy type addresses the specific material compositions that lend unique properties to the foils, dictating their suitability for different applications. By application, the market is categorized based on the end-use sectors where copper alloy foils are critically utilized, highlighting their functional importance in specific industries.

Further segmentation by thickness reflects the increasing demand for ultra-thin foils in advanced electronic applications, contrasting with standard foils used in more traditional industrial settings. This differentiation is crucial for understanding technological advancements and manufacturing capabilities required for different product specifications. Finally, the segmentation by end-use industry provides a broader view of the market's reliance on major industrial sectors, offering insights into long-term demand trends shaped by global economic and technological shifts within those industries. This multi-dimensional segmentation ensures a holistic and detailed market assessment, valuable for strategic planning and competitive analysis.

- By Alloy Type:

- Brass Alloy Foil: Known for good conductivity, strength, and formability, used in connectors and decorative applications.

- Bronze Alloy Foil: Offers higher strength and wear resistance, suitable for bearings and springs.

- Cupronickel Alloy Foil: Excellent corrosion resistance and strength, preferred in marine and coinage applications.

- Beryllium Copper Alloy Foil: High strength, conductivity, and fatigue resistance, critical for high-performance connectors and switches.

- Other Copper Alloys (e.g., Chromium Copper, Tellurium Copper): Specialized alloys with unique properties for specific niche applications.

- By Application:

- Electrical & Electronics: Dominant segment, including Printed Circuit Boards (PCBs), connectors, battery components (e.g., Lithium-ion battery current collectors), and electromagnetic shielding.

- Automotive: Utilized in heat exchangers, electrical systems, and increasingly in EV battery packs and associated wiring.

- Industrial: Applications such as transformer windings, gaskets & seals, and components in chemical processing equipment.

- Construction: Used in roofing, flashing, and piping due to corrosion resistance and malleability.

- Telecommunications: Essential for 5G infrastructure components, high-frequency circuits, and cable shielding.

- Medical Devices: Employed in surgical instruments, imaging equipment components, and antimicrobial surfaces.

- Aerospace & Defense: For lightweight wiring, precision components, and shielding in aircraft and satellite systems.

- Consumer Goods: Broad range of applications in everyday electronic devices and appliances.

- By Thickness:

- Ultra-thin Foil (<10 µm): Critical for advanced packaging, micro-electronics, and high-density PCBs.

- Thin Foil (10 µm - 50 µm): Widely used in flexible circuits, sensors, and smaller electronic components.

- Standard Foil (>50 µm): Employed in industrial applications, general electronics, and construction.

- By End-Use Industry:

- Electronics Industry: The largest consumer, driven by semiconductor, PCB, and component manufacturing.

- Automotive Industry: Significant growth propelled by EV production and traditional automotive electrical systems.

- Industrial Machinery: For various components in manufacturing equipment and industrial processes.

- Building & Construction: Used in architectural applications, plumbing, and electrical installations.

- Telecommunications Industry: Vital for network infrastructure and communication devices.

- Healthcare Industry: For medical equipment and devices requiring high purity and performance.

- Energy Industry: Applications in renewable energy systems, power generation, and distribution.

- Aerospace Industry: For lightweight and high-performance components in aircraft and spacecraft.

Regional Highlights

- Asia Pacific (APAC): Dominates the Copper Alloy Foil market, primarily driven by its robust electronics manufacturing hub, particularly in countries like China, South Korea, Taiwan, and Japan. The region accounts for a significant portion of global PCB production and semiconductor manufacturing. Rapid industrialization, expanding consumer electronics markets, and substantial investments in electric vehicle production in countries like China and India further propel market growth. The presence of numerous key market players and a large consumer base solidify APAC's leading position, making it a critical region for both production and consumption.

- North America: Represents a mature yet steadily growing market, characterized by significant R&D investments in advanced electronics, aerospace, and defense sectors. The region benefits from a strong automotive industry transitioning towards EVs, alongside a focus on high-performance computing and medical device manufacturing. Innovation in material science and increasing adoption of smart manufacturing technologies contribute to sustained demand for high-value copper alloy foils. The emphasis on high-precision and specialized applications drives market value.

- Europe: A significant market driven by stringent environmental regulations, a strong automotive sector, and advanced industrial manufacturing. Countries like Germany and France are pioneers in industrial automation and renewable energy initiatives, creating demand for high-quality copper alloy foils in these applications. The region also exhibits a growing interest in sustainable production methods and recycling technologies, influencing material sourcing and manufacturing processes. Investments in 5G infrastructure and smart grids further support market expansion.

- Latin America: An emerging market for Copper Alloy Foil, with growth largely influenced by expanding industrial sectors, infrastructure development, and increasing automotive production, particularly in Brazil and Mexico. While smaller in market share compared to APAC, North America, or Europe, the region presents opportunities for future growth as economic conditions improve and technological adoption increases. Local manufacturing expansion and foreign direct investment are key drivers in this region.

- Middle East and Africa (MEA): Currently represents a smaller share of the global market, but poised for growth due to ambitious infrastructure projects, diversification of economies away from oil, and increasing urbanization. Investments in telecommunications, renewable energy, and industrial development, particularly in countries like UAE, Saudi Arabia, and South Africa, are expected to drive demand for copper alloy foils in the long term. The region's potential lies in its nascent industrial growth and demand for fundamental conductive materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Copper Alloy Foil Market.- Global Metals Corp.

- Precision Foils Inc.

- Alloy Innovations Ltd.

- Conductive Materials Group

- Advanced Copper Solutions

- Metallurgical Tech Co.

- EcoAlloy Enterprises

- Future Foils B.V.

- Dynamic Alloys LLC

- Pioneer Metalworks

- Integrated Foils Systems

- OptiMetals Industries

- Supreme Copper Products

- United Alloy Manufacturers

- Premier Metallurgy Inc.

- Phoenix Foils Ltd.

- Quantum Metals AG

- Evergreen Alloys

- Nexus Metal Solutions

- Summit Foils Corp.

Frequently Asked Questions

Analyze common user questions about the Copper Alloy Foil market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Copper Alloy Foil primarily used for?

Copper alloy foil is primarily used in the electrical and electronics industries for printed circuit boards (PCBs), connectors, and battery components, alongside significant applications in automotive (especially EVs), industrial machinery, telecommunications (5G), and medical devices due to its excellent conductivity, ductility, and corrosion resistance.

What is the projected growth rate for the Copper Alloy Foil market?

The Copper Alloy Foil market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, driven by increasing demand from consumer electronics, electric vehicles, and 5G infrastructure development.

Which region dominates the Copper Alloy Foil market?

Asia Pacific (APAC) currently dominates the Copper Alloy Foil market, primarily due to its expansive electronics manufacturing base, significant investments in EV production, and rapid industrialization in countries like China, South Korea, and Japan.

How does AI impact the Copper Alloy Foil manufacturing industry?

AI significantly impacts the Copper Alloy Foil industry by optimizing production processes, enhancing quality control through automated inspection, enabling predictive maintenance for machinery, and accelerating the development of new alloy compositions with tailored properties.

What are the main challenges facing the Copper Alloy Foil market?

Key challenges for the Copper Alloy Foil market include volatile raw material prices (copper), stringent environmental regulations, potential supply chain disruptions, high research and development costs for advanced alloys, and the scarcity of skilled labor in specialized manufacturing processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted