Construction Aggregate Market

Construction Aggregate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705436 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Construction Aggregate Market Size

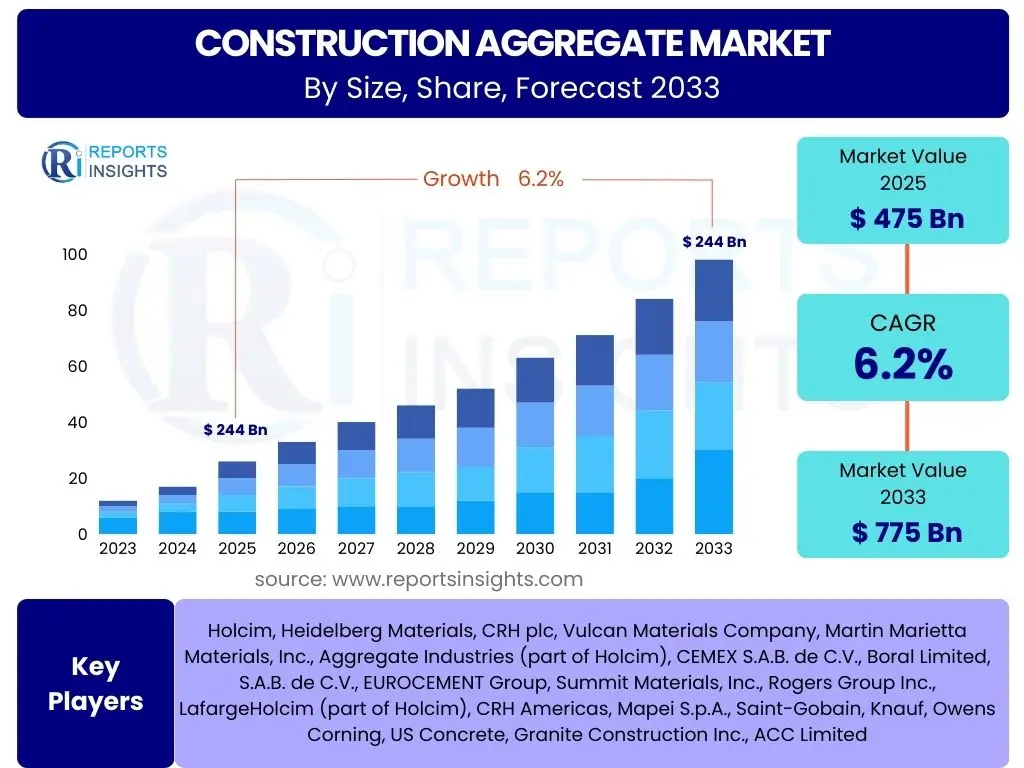

According to Reports Insights Consulting Pvt Ltd, The Construction Aggregate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 475 Billion in 2025 and is projected to reach USD 775 Billion by the end of the forecast period in 2033.

Key Construction Aggregate Market Trends & Insights

The construction aggregate market is currently experiencing significant shifts driven by global urbanization, sustained infrastructure investments, and an increasing focus on sustainable practices. Key market participants and stakeholders are keenly observing the growing adoption of recycled aggregates, the impact of digitalization on supply chain efficiencies, and the evolving regulatory landscape concerning environmental impact. There is a discernible trend towards higher quality, more specialized aggregate types to meet the demands of modern construction techniques and resilient infrastructure projects.

Furthermore, technological advancements are playing a pivotal role in shaping the market, from more efficient extraction methods to advanced material processing. The integration of data analytics for optimizing quarry operations and logistics is becoming more prevalent, aimed at reducing operational costs and improving material delivery times. These trends collectively underscore a market moving towards greater efficiency, sustainability, and technological integration to meet burgeoning global construction needs.

- Increasing adoption of recycled aggregates driven by environmental regulations and resource scarcity.

- Growth in smart city projects and urban infrastructure development demanding high-quality aggregates.

- Technological advancements in quarrying and processing, including automation and digitalization.

- Focus on sustainable and green construction practices influencing aggregate production.

- Rising demand for specialized aggregates for high-performance concrete and niche applications.

AI Impact Analysis on Construction Aggregate

Artificial Intelligence (AI) is poised to revolutionize the construction aggregate sector by enhancing operational efficiencies, optimizing resource management, and improving safety standards. Users frequently inquire about how AI can streamline logistics, predict equipment failures, and ensure consistent product quality. AI-driven solutions are expected to facilitate more precise demand forecasting, allowing aggregate producers to optimize production schedules and inventory levels, thereby reducing waste and improving profitability across the value chain.

The application of AI extends to predictive maintenance for heavy machinery, reducing costly downtimes and extending equipment lifespan. Furthermore, AI algorithms can analyze geological data to identify optimal quarrying locations, improve excavation patterns, and manage complex supply chains, leading to significant cost savings and operational enhancements. While the adoption rate is currently nascent, the industry anticipates AI to become an indispensable tool for data-driven decision-making, transforming traditional aggregate operations into more intelligent and responsive systems.

- Optimization of quarry operations and logistics through AI-driven analytics.

- Predictive maintenance for heavy machinery, reducing downtime and operational costs.

- Enhanced quality control and material sorting using AI-powered vision systems.

- Improved supply chain management and demand forecasting for aggregate products.

- Autonomous equipment operation in mining and transportation, boosting safety and efficiency.

Key Takeaways Construction Aggregate Market Size & Forecast

The construction aggregate market is poised for robust growth, primarily fueled by extensive global infrastructure development and rapid urbanization, particularly in emerging economies. A significant takeaway is the increasing emphasis on sustainable practices, compelling market players to invest in recycled aggregates and environmentally friendly production methods. The forecast indicates sustained demand across residential, commercial, and infrastructure sectors, with Asia Pacific maintaining its dominance as a major consumption hub due to ongoing large-scale development projects.

Another crucial insight is the evolving competitive landscape, characterized by strategic partnerships, mergers, and acquisitions aimed at expanding geographic reach and enhancing product portfolios. The market will continue to be influenced by fluctuating raw material costs, stringent environmental regulations, and the imperative for technological innovation to improve efficiency and reduce environmental footprints. These factors collectively highlight a dynamic market that requires adaptability and a forward-looking approach from all stakeholders.

- Significant market growth driven by global infrastructure development and urbanization.

- Asia Pacific is expected to remain the largest and fastest-growing regional market.

- Increased focus on sustainable practices and the use of recycled aggregates.

- Technological advancements in production and logistics will shape market efficiency.

- Market expansion influenced by government investments in public works and smart city initiatives.

Construction Aggregate Market Drivers Analysis

The construction aggregate market is significantly propelled by several macro and microeconomic factors that collectively foster demand and expansion. A primary driver is the accelerating pace of global urbanization, which necessitates the development of extensive residential, commercial, and public infrastructure to accommodate growing populations. This continuous urban expansion directly translates into higher demand for aggregates for building foundations, roads, bridges, and utilities.

Furthermore, substantial government investments in infrastructure projects worldwide serve as a critical catalyst. Governments are increasingly allocating funds towards modernizing existing infrastructure and constructing new facilities, including highways, railways, airports, and dams. These large-scale projects are inherently aggregate-intensive, ensuring a steady and robust demand for various types of aggregates. The ongoing industrialization in developing countries also contributes significantly, with new factories, industrial parks, and commercial complexes requiring vast quantities of construction materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Population Growth | +1.8% | Asia Pacific, Africa, Latin America | 2025-2033 (Long-term) |

| Increased Government Infrastructure Spending | +1.5% | North America, Europe, China, India | 2025-2030 (Mid-term) |

| Growth in Commercial & Residential Construction | +1.2% | Global, particularly Emerging Economies | 2025-2033 (Long-term) |

| Industrialization & Economic Development | +0.9% | Southeast Asia, Middle East, Africa | 2025-2033 (Long-term) |

Construction Aggregate Market Restraints Analysis

Despite the robust growth drivers, the construction aggregate market faces several significant restraints that could impede its expansion. Stringent environmental regulations and policies are a major concern, as they often impose limitations on quarrying operations, demand extensive environmental impact assessments, and enforce costly remediation measures. Compliance with these regulations can lead to increased operational costs and delays in project approvals, thereby impacting profitability and market supply.

Another prominent restraint is the volatility in the prices of raw materials, energy, and transportation. The aggregate industry is highly dependent on heavy machinery and logistics, making it susceptible to fluctuations in fuel prices and other operational expenditures. Additionally, challenges related to land acquisition and permitting for new quarry sites are escalating. As urban areas expand, suitable land for new aggregate extraction becomes scarce and more expensive, leading to protracted legal processes and higher upfront investments for market players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -0.8% | Europe, North America, Developed Asia | 2025-2033 (Long-term) |

| Volatility in Raw Material & Energy Prices | -0.7% | Global | 2025-2028 (Short-term) |

| Land Acquisition & Permitting Challenges | -0.6% | Highly Populated & Developed Regions | 2025-2033 (Long-term) |

| Logistics & Transportation Costs | -0.5% | Global, particularly Remote Areas | 2025-2030 (Mid-term) |

Construction Aggregate Market Opportunities Analysis

The construction aggregate market presents several promising opportunities for growth and innovation. A significant opportunity lies in the burgeoning trend towards sustainable construction practices, which is driving increased demand for recycled aggregates. The utilization of construction and demolition waste as a source for aggregates not only addresses environmental concerns but also offers a cost-effective alternative to virgin materials, opening new revenue streams for market participants.

Moreover, the expansion of smart city initiatives and the development of high-performance infrastructure create demand for specialized and high-quality aggregates. Innovations in material science and processing technologies allow for the production of aggregates with enhanced properties, catering to the specific requirements of modern, resilient, and aesthetically pleasing structures. Furthermore, the digitalization and automation of quarrying and supply chain operations present an opportunity to significantly improve efficiency, reduce operational costs, and enhance overall market competitiveness.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Recycled Aggregates | +1.0% | Europe, North America, Japan | 2025-2033 (Long-term) |

| Advancements in Sustainable Construction & Green Building | +0.9% | Global | 2025-2033 (Long-term) |

| Emergence of Smart City & High-Performance Infrastructure Projects | +0.8% | China, India, Middle East, Developed Countries | 2025-2030 (Mid-term) |

| Digitalization & Automation in Operations | +0.7% | Global, particularly Large Players | 2025-2033 (Long-term) |

Construction Aggregate Market Challenges Impact Analysis

The construction aggregate market faces several inherent challenges that can impact its growth trajectory and operational stability. One significant challenge is the susceptibility to supply chain disruptions, which can stem from various factors such as geopolitical conflicts, natural disasters, or global health crises. These disruptions can lead to material shortages, increased lead times, and escalated transportation costs, severely affecting project timelines and profitability for aggregate suppliers.

Another persistent challenge is the shortage of skilled labor within the mining and construction sectors. The aggregate industry requires specialized expertise for operating heavy machinery, managing quarry sites, and maintaining complex processing equipment. A dwindling pool of qualified personnel can lead to operational inefficiencies, higher labor costs, and difficulties in scaling production. Additionally, the industry must continuously navigate complex and evolving environmental compliance requirements, which demand significant investments in technology and operational adjustments to mitigate ecological impacts and avoid penalties.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions & Geopolitical Instability | -0.6% | Global | 2025-2028 (Short-term) |

| Shortage of Skilled Labor | -0.5% | North America, Europe, parts of Asia | 2025-2033 (Long-term) |

| Navigating Evolving Environmental Compliance | -0.4% | Global | 2025-2033 (Long-term) |

| High Capital Investment & Maintenance Costs | -0.3% | Global | 2025-2033 (Long-term) |

Construction Aggregate Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Construction Aggregate Market, covering market size estimations, historical data, and future growth projections from 2025 to 2033. It includes a detailed examination of key market trends, drivers, restraints, opportunities, and challenges influencing the industry landscape. The report segments the market by various types, applications, and regional landscapes, offering granular insights into the market dynamics across different geographies. Additionally, it profiles leading market players, providing an understanding of the competitive environment and strategic initiatives undertaken by industry leaders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 475 Billion |

| Market Forecast in 2033 | USD 775 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Holcim, Heidelberg Materials, CRH plc, Vulcan Materials Company, Martin Marietta Materials, Inc., Aggregate Industries (part of Holcim), CEMEX S.A.B. de C.V., Boral Limited, S.A.B. de C.V., EUROCEMENT Group, Summit Materials, Inc., Rogers Group Inc., LafargeHolcim (part of Holcim), CRH Americas, Mapei S.p.A., Saint-Gobain, Knauf, Owens Corning, US Concrete, Granite Construction Inc., ACC Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Construction Aggregate Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. These segments allow for a detailed analysis of market performance across different aggregate types, end-use applications, and geographical regions. Such segmentation is crucial for stakeholders to identify specific growth areas, understand demand patterns, and tailor their strategies to target particular market niches effectively.

Understanding these segments helps in recognizing the varied requirements of different construction projects, from residential buildings requiring a mix of sand and gravel to large-scale infrastructure projects demanding significant volumes of crushed stone. The growing emphasis on sustainability also highlights the importance of the recycled aggregate segment, which is expected to witness substantial growth. Each segment possesses unique drivers and challenges, necessitating a comprehensive approach to market analysis and strategic planning.

- By Type:

- Crushed Stone

- Sand

- Gravel

- Recycled Aggregate

- Manufactured Sand

- By Application:

- Residential

- Commercial

- Industrial

- Infrastructure

- Roads

- Bridges

- Dams

- Railways

- Airports

Regional Highlights

- Asia Pacific (APAC): Expected to be the largest and fastest-growing market due to massive infrastructure development projects, rapid urbanization, and industrialization in countries like China, India, and Southeast Asian nations.

- North America: Driven by significant investments in infrastructure upgrades (e.g., roads, bridges) and a steady residential and commercial construction sector, with a growing emphasis on sustainable practices.

- Europe: Characterized by mature markets with stringent environmental regulations, driving the adoption of recycled aggregates and sustainable construction methods. Infrastructure modernization and urban renewal projects also contribute to demand.

- Latin America: Showing promising growth fueled by increasing government spending on public infrastructure, housing development, and foreign investments, particularly in Brazil and Mexico.

- Middle East and Africa (MEA): Experiencing substantial growth due to large-scale development projects, including smart cities, commercial complexes, and tourism infrastructure, especially in the GCC countries and parts of Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Construction Aggregate Market.- Holcim

- Heidelberg Materials

- CRH plc

- Vulcan Materials Company

- Martin Marietta Materials, Inc.

- Aggregate Industries (part of Holcim)

- CEMEX S.A.B. de C.V.

- Boral Limited

- EUROCEMENT Group

- Summit Materials, Inc.

- Rogers Group Inc.

- LafargeHolcim (part of Holcim)

- CRH Americas

- Mapei S.p.A.

- Saint-Gobain

- Knauf

- Owens Corning

- US Concrete

- Granite Construction Inc.

- ACC Limited

Frequently Asked Questions

What is the projected growth for the Construction Aggregate market?

The Construction Aggregate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033, reaching an estimated USD 775 Billion by 2033.

What are the primary drivers of the Construction Aggregate market?

Key drivers include rapid urbanization, substantial government investments in infrastructure development, and continuous growth in commercial and residential construction worldwide.

How do environmental regulations impact the Construction Aggregate market?

Stringent environmental regulations can act as a restraint by increasing operational costs, delaying project approvals, and necessitating greater adoption of sustainable practices like using recycled aggregates.

What role does recycled aggregate play in the market?

Recycled aggregate plays a crucial role by offering a sustainable and often cost-effective alternative to virgin materials, driven by environmental concerns and a growing focus on green building practices.

Which regions are expected to show significant growth in construction aggregate demand?

Asia Pacific is anticipated to be the largest and fastest-growing market due to extensive infrastructure development and urbanization, while North America and Europe also show steady demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted