Concentrating Solar Power Market

Concentrating Solar Power Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700015 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

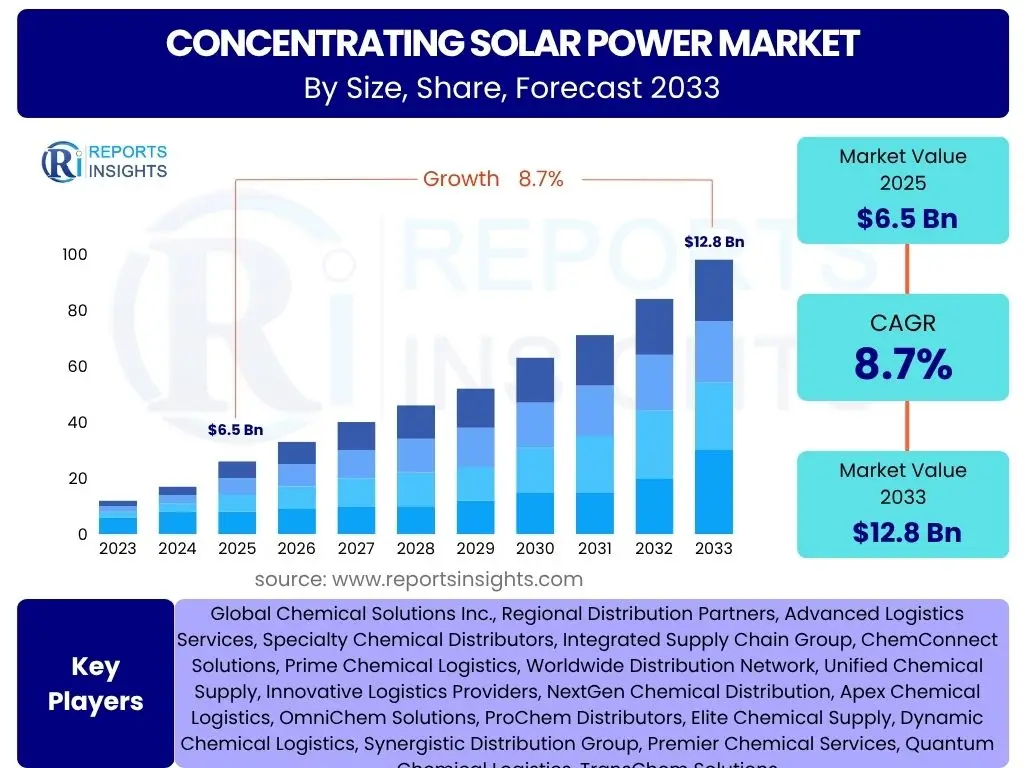

Concentrating Solar Power Market is projected to grow at a Compound annual growth rate (CAGR) of 8.7% between 2025 and 2033, reaching an estimated USD 6.5 Billion in 2025 and is projected to grow by USD 12.8 Billion By 2033 the end of the forecast period.

Key Concentrating Solar Power Market Trends & Insights

The Concentrating Solar Power (CSP) market is currently witnessing a transformative phase, driven by a confluence of technological advancements, policy shifts, and increasing global commitments to renewable energy. A pivotal trend is the continuous decline in the Levelized Cost of Electricity (LCOE) for CSP projects, making them increasingly competitive against traditional fossil fuel sources. This cost reduction is largely attributable to economies of scale, improved manufacturing processes, and enhanced operational efficiencies. Furthermore, the integration of thermal energy storage (TES) systems is becoming a standard feature in modern CSP plants, significantly enhancing their dispatchability and grid stability contributions by allowing electricity generation even after sunset or during periods of low solar irradiance.

Another significant trend is the growing interest in hybrid CSP solutions, which combine CSP technology with other renewable energy sources like photovoltaics (PV) or even conventional fossil fuels, to optimize power generation and ensure a consistent supply. Digitalization, including the adoption of advanced analytics, artificial intelligence, and Internet of Things (IoT) technologies, is also playing a crucial role in optimizing plant performance, predictive maintenance, and overall operational management. Geographically, there's a sustained shift towards regions with high direct normal irradiance (DNI) and supportive policy frameworks, such as the Middle East, North Africa, and parts of Asia, which are emerging as global hubs for large-scale CSP deployment.

- Declining Levelized Cost of Electricity (LCOE) for CSP projects.

- Increased integration of advanced thermal energy storage (TES) systems.

- Growing adoption of hybrid CSP solutions with other energy sources.

- Expansion of digitalization, AI, and IoT for operational optimization.

- Shift towards high direct normal irradiance (DNI) regions for deployment.

- Emphasis on dispatchable renewable energy solutions.

- Development of advanced CSP technologies like molten salt towers and parabolic troughs.

AI Impact Analysis on Concentrating Solar Power

Artificial Intelligence (AI) is set to revolutionize the Concentrating Solar Power (CSP) market by enhancing efficiency, optimizing operations, and improving the overall economic viability of projects. AI algorithms can analyze vast datasets from weather patterns, solar irradiance, and historical plant performance to predict energy output with greater accuracy, allowing grid operators to better integrate CSP into the existing power infrastructure and optimize energy trading strategies. Furthermore, AI-powered predictive maintenance systems can monitor the health of CSP components, such as mirrors, receivers, and turbines, identifying potential failures before they occur. This proactive approach minimizes downtime, reduces maintenance costs, and extends the operational lifespan of critical assets, thereby improving the plant's capacity factor and revenue generation.

Beyond operational enhancements, AI also plays a crucial role in the design and planning phases of new CSP projects. Machine learning models can optimize the layout of solar fields, the sizing of thermal storage systems, and the selection of optimal sites by evaluating complex environmental and geographical data. Real-time optimization of heliostat or parabolic trough aiming, based on dynamic solar tracking and cloud movement predictions, can significantly boost energy collection efficiency. The integration of AI tools for demand-side management and smart grid functionalities will further enable CSP plants to respond dynamically to grid needs, thereby increasing their value proposition in a highly interconnected energy landscape and accelerating the transition towards a more intelligent and sustainable power system.

- Enhanced energy output prediction and forecasting for grid integration.

- Optimized plant operations through real-time data analysis and control.

- Predictive maintenance for critical components, reducing downtime.

- Improved site selection and solar field design optimization.

- Automated fault detection and diagnostic capabilities.

- Intelligent thermal energy storage management for enhanced dispatchability.

- AI-driven energy trading and market participation strategies.

Key Takeaways Concentrating Solar Power Market Size & Forecast

- The global Concentrating Solar Power market is experiencing robust growth, driven by increasing demand for dispatchable renewable energy.

- Significant market expansion is projected from 2025 to 2033, indicating strong investment potential.

- The market is expected to nearly double in value over the forecast period, reflecting widespread adoption and technological advancements.

- Cost reductions in CSP technology and integration of thermal energy storage are key factors underpinning this growth trajectory.

- Emerging economies, particularly in regions with high solar irradiation, are anticipated to be major contributors to market size expansion.

- Policy support and incentives for renewable energy deployment are critical in sustaining and accelerating market growth.

Concentrating Solar Power Market Drivers Analysis

The global Concentrating Solar Power (CSP) market is significantly propelled by a confluence of macroeconomic, technological, and policy-driven factors. One of the primary drivers is the escalating global imperative to transition towards sustainable and low-carbon energy sources. Governments worldwide are setting ambitious renewable energy targets and implementing supportive policies, including feed-in tariffs, tax incentives, and carbon pricing mechanisms, which create a favorable investment climate for CSP projects. The unique ability of CSP to integrate thermal energy storage systems allows it to provide dispatchable power, addressing the intermittency challenges associated with other renewable sources like wind and photovoltaic solar, thereby enhancing grid stability and reliability. This makes CSP a highly attractive option for energy planners seeking robust and flexible solutions for their national grids.

Technological advancements also play a critical role in driving market expansion. Continuous innovation in receiver technologies, mirror designs, and heat transfer fluids has led to improved efficiency and reduced the Levelized Cost of Electricity (LCOE) for CSP plants. The decreasing cost of financing for renewable energy projects, coupled with the proven long-term operational performance of CSP facilities, further enhances their appeal to investors. Moreover, the growing demand for industrial process heat, especially in sectors requiring high temperatures, presents a significant untapped market for CSP, offering opportunities beyond conventional electricity generation. As global energy consumption continues to rise, and the urgency to mitigate climate change intensifies, the fundamental strengths of CSP in providing clean, reliable, and dispatchable power solidify its position as a vital component of the future energy mix.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Push for Renewable Energy & Decarbonization Goals | +2.1% | Global (Europe, Asia Pacific, North America) | Short- to Long-Term (2025-2033) |

| Advancements in Thermal Energy Storage (TES) Integration | +1.8% | Global, particularly MEA & Europe | Mid- to Long-Term (2027-2033) |

| Declining Levelized Cost of Electricity (LCOE) for CSP | +1.6% | Global (Emerging Markets & Developed Economies) | Short- to Mid-Term (2025-2030) |

| Supportive Government Policies and Incentives | +1.5% | Specific Countries (China, US, Spain, UAE, Morocco) | Short- to Long-Term (2025-2033) |

| Increasing Demand for Dispatchable Power Generation | +1.3% | Regions with High Grid Instability/Renewable Penetration | Short- to Long-Term (2025-2033) |

Concentrating Solar Power Market Restraints Analysis

Despite its significant potential, the Concentrating Solar Power (CSP) market faces several notable restraints that can impede its growth trajectory. A primary challenge is the relatively high upfront capital cost associated with building large-scale CSP plants compared to other renewable technologies like photovoltaic (PV) solar. The complex infrastructure involving large mirror fields, sophisticated tracking systems, and thermal energy storage units requires substantial initial investment, which can be a barrier for potential investors and developers, particularly in regions with limited access to affordable financing. While LCOE has decreased, the initial capital expenditure remains a hurdle, often necessitating significant government subsidies or unique financing models to make projects viable.

Another significant restraint is the reliance of CSP technology on high Direct Normal Irradiance (DNI) levels. This geographical limitation restricts CSP deployment to specific arid or semi-arid regions with abundant, consistent direct sunlight, such as deserts in the Middle East, North Africa, parts of the US, and China. While these regions offer ideal conditions, they are not universally available, limiting the global applicability and widespread adoption of CSP compared to PV, which can function effectively under a broader range of solar conditions. Furthermore, the operational complexity and water intensity of some CSP technologies, particularly wet-cooled systems, pose environmental concerns and operational challenges in water-scarce desert environments, necessitating the adoption of more expensive dry-cooling solutions or careful water management strategies, adding to the overall cost and complexity of projects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Costs Compared to Other Renewables | -1.9% | Global (Especially Developing Economies) | Short- to Mid-Term (2025-2030) |

| Geographical Limitations Due to High DNI Requirement | -1.5% | Regions Outside High Solar Resource Zones | Long-Term (Ongoing) |

| Competition from Cheaper Photovoltaic (PV) Technology | -1.2% | Global (Particularly Decentralized Markets) | Short- to Mid-Term (2025-2030) |

| Water Consumption Concerns in Arid Regions | -0.8% | MEA, Southwestern US, Australia, China | Mid- to Long-Term (2027-2033) |

Concentrating Solar Power Market Opportunities Analysis

The Concentrating Solar Power (CSP) market is ripe with significant opportunities that can accelerate its growth and expand its application scope. One major opportunity lies in the increasing global demand for dispatchable, base-load renewable energy. As countries integrate higher percentages of variable renewable energy sources like wind and PV into their grids, the need for stable and on-demand power generation becomes critical. CSP, with its inherent ability to incorporate large-scale thermal energy storage, is uniquely positioned to fill this gap, offering a reliable power supply even when the sun is not shining. This characteristic positions CSP as a crucial component for achieving ambitious renewable energy targets and ensuring grid stability in a decarbonized energy future.

Another promising opportunity for CSP is its application in industrial process heat generation. Many industrial sectors, such as food and beverage, chemicals, mining, and textiles, require high-temperature heat for their processes, traditionally supplied by fossil fuels. CSP systems can efficiently deliver this heat at various temperature ranges, offering a clean and sustainable alternative to industrial decarbonization. Furthermore, hybrid CSP-PV projects are gaining traction, allowing developers to leverage the cost-effectiveness of PV for direct power generation during sunlight hours and utilize CSP's storage capabilities for dispatchable power. Emerging markets with vast solar resources, particularly in the Middle East, North Africa, and Latin America, present substantial untapped potential for large-scale CSP deployment, driven by industrialization and growing energy demand. Advancements in molten salt technology, parabolic trough improvements, and tower systems are also continually unlocking new efficiencies and cost reductions, making CSP an increasingly attractive investment for diversifying energy portfolios.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Need for Dispatchable and Stable Renewable Energy | +2.3% | Global (Especially Grids with High Variable RE Penetration) | Short- to Long-Term (2025-2033) |

| Expansion into Industrial Process Heat Applications | +1.7% | Industrialized Regions (Europe, North America, Asia Pacific) | Mid- to Long-Term (2027-2033) |

| Hybridization with Photovoltaics (PV) and Other Renewables | +1.4% | Global (Project Development & Utility Scale) | Short- to Mid-Term (2025-2030) |

| Untapped Market Potential in Emerging Economies with High DNI | +1.1% | MEA, Latin America, Parts of Asia | Mid- to Long-Term (2027-2033) |

Concentrating Solar Power Market Challenges Impact Analysis

The Concentrating Solar Power (CSP) market, while promising, faces a unique set of challenges that demand strategic responses from stakeholders to sustain growth. One significant hurdle is the intense competition from other mature and rapidly deploying renewable technologies, particularly photovoltaic (PV) solar and wind power. PV, with its rapidly falling costs, modularity, and ease of deployment, often presents a more economically attractive option for utility-scale solar generation, especially for projects without the immediate need for dispatchable power. This competitive pressure necessitates continuous innovation and cost reduction efforts within the CSP sector to maintain its market share and demonstrate its unique value proposition, particularly regarding dispatchability and storage capabilities.

Another key challenge is the complexity of site selection and environmental considerations. CSP plants require large tracts of land with high and consistent Direct Normal Irradiance (DNI), which are often located in remote, arid, or ecologically sensitive regions. This can lead to challenges related to land acquisition, environmental impact assessments (EIA), and the need for robust infrastructure development for grid connection and water supply. Furthermore, the long project development cycles and high capital intensity of CSP projects mean they are sensitive to policy changes and regulatory uncertainties. A lack of consistent, long-term policy support or sudden shifts in government priorities can significantly impact investment decisions and the overall project pipeline, making it crucial for the industry to advocate for stable and predictable policy frameworks that acknowledge CSP's strategic role in grid decarbonization and stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Other Renewable Technologies (e.g., PV) | -1.8% | Global (Utility-Scale Projects) | Short- to Mid-Term (2025-2030) |

| Long Project Development Cycles and High Project Complexity | -1.4% | Global (Investment & Project Pipeline) | Short- to Mid-Term (2025-2030) |

| Policy and Regulatory Uncertainties & Lack of Consistent Support | -1.1% | Specific Countries/Regions with Policy Shifts | Short- to Long-Term (2025-2033) |

| Environmental Concerns & Land Use Requirements | -0.9% | Regions with Strict Environmental Regulations/Land Scarcity | Mid- to Long-Term (2027-2033) |

Concentrating Solar Power Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Concentrating Solar Power market, offering strategic insights into its current landscape and future growth trajectories. The report meticulously covers key market dynamics, including drivers, restraints, opportunities, and challenges, alongside a detailed assessment of market segmentation, regional performance, and the competitive landscape. Designed to empower business professionals and decision-makers, it delivers actionable intelligence to navigate the evolving energy sector and capitalize on emerging trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 12.8 Billion |

| Growth Rate | 8.7% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Solar Power Solutions, Renewable Energy Systems Group, Horizon Solar Technologies, GreenVolt Energy Partners, Sustainable Power Inc., SunPeak Renewables, Atlas Renewable Energy, Energen Solar, Helios Power Systems, NovaVolt Solutions, TerraWatt Energy, Quantum Solar Innovations, Phoenix Renewables, BrightStar Energy, Apex Solar Generation, EcoPower Global, Radiant Energy Developers, ClearSky Renewables, Infinite Solar Systems, Prime Renewables Holdings |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis:

The Concentrating Solar Power (CSP) market is meticulously segmented to provide a granular understanding of its diverse facets, enabling stakeholders to identify specific growth areas and strategic opportunities. These segmentations are critical for analyzing market dynamics across different technological advancements, end-use applications, capacity requirements, and operational characteristics. Understanding these distinctions allows for targeted investment, product development, and policy formulation to maximize the market's potential.

The segmentation by technology type differentiates between the core methods used to concentrate sunlight, each with unique advantages in terms of efficiency, scalability, and thermal energy storage integration. Application-based segmentation highlights the versatility of CSP beyond traditional electricity generation, revealing its growing importance in industrial processes and water treatment. Capacity and end-use segmentations further refine the analysis, providing insights into preferred project sizes and the primary consumers of CSP-generated energy or heat, thereby offering a holistic view of the market's intricate structure and potential avenues for expansion.

- Technology Type: This segment focuses on the different designs utilized to collect and concentrate solar radiation.

- Parabolic Trough: The most mature and widely deployed CSP technology, using U-shaped mirrors to focus sunlight onto a receiver tube containing heat transfer fluid. Sub-segments include molten salt (for higher temperatures and storage) and synthetic oil (traditional heat transfer fluid).

- Solar Tower: Employs a field of sun-tracking mirrors (heliostats) that concentrate sunlight onto a central receiver atop a tower, typically using molten salt or steam/water as the heat transfer medium for higher operating temperatures and more efficient storage.

- Dish/Engine Systems: Utilizes a parabolic dish to concentrate sunlight onto a receiver at the focal point, powering a Stirling engine for electricity generation, often used for smaller, modular applications.

- Fresnel Reflectors: Uses a series of long, flat, or slightly curved mirrors to focus sunlight onto a fixed receiver, offering simpler construction and potentially lower costs.

- Application: This segmentation explores the primary uses for the energy generated by CSP plants.

- Power Generation: The largest application segment, where concentrated solar energy is converted into electricity for grid supply.

- Utility Scale: Large-scale plants connected to the national or regional grid, typically exceeding 50 MW.

- Distributed Generation: Smaller-scale CSP systems for local power supply, often for industrial or commercial sites.

- Industrial Process Heat: Focuses on CSP systems designed to provide high-temperature heat directly for industrial processes, reducing reliance on fossil fuels in sectors like manufacturing, food processing, and chemicals.

- Desalination: CSP-powered systems used to convert saline water into fresh water, a crucial application in water-scarce regions.

- Power Generation: The largest application segment, where concentrated solar energy is converted into electricity for grid supply.

- Capacity: This segment categorizes CSP projects based on their installed power output.

- Below 50 MW: Typically smaller utility-scale or industrial applications.

- 50 MW - 100 MW: Medium-sized utility-scale projects.

- Above 100 MW: Large-scale, often multi-tower or extensive parabolic trough plants designed for significant grid contribution.

- End-Use: This segment identifies the primary consumers of CSP-generated energy or heat.

- Utilities: National and regional power grids are the primary off-takers for large-scale CSP electricity generation.

- Industrial: Direct consumers of CSP-generated process heat or electricity for their operational needs.

- Commercial: Businesses and institutions that utilize CSP for their energy requirements, including heating, cooling, or power.

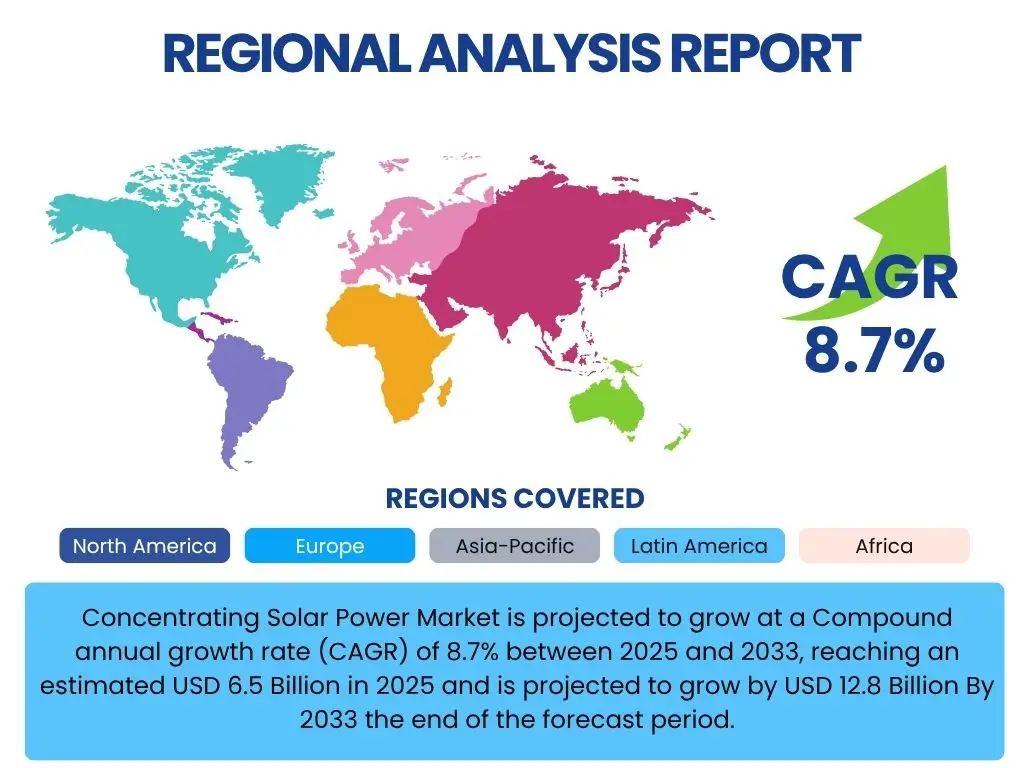

Regional Highlights

The global Concentrating Solar Power (CSP) market exhibits distinct regional dynamics, with specific geographies demonstrating leadership in deployment, technological innovation, and policy support. Understanding these regional nuances is vital for strategic market engagement and identifying high-growth opportunities. While CSP projects require high direct normal irradiance (DNI), the presence of supportive regulatory frameworks, access to financing, and industrial demand significantly influence regional market performance.

The Middle East and Africa (MEA) region, particularly countries like the UAE, Morocco, and Saudi Arabia, stands out as a critical hub for CSP development. These nations possess vast desert lands with exceptional solar resources and are actively pursuing diversification from fossil fuels, backed by ambitious national renewable energy targets and substantial government investments in large-scale CSP projects with integrated storage. Similarly, parts of Asia Pacific, especially China, have emerged as strong contenders, driven by robust domestic policies, significant manufacturing capabilities, and a push for energy independence and decarbonization. China, in particular, has developed and deployed several large-scale CSP projects, leveraging domestic technological advancements and substantial state support. These regions are poised for continued significant growth, setting benchmarks for future global deployments.

Europe, spearheaded by Spain, remains a mature but strategically important market. Spain was an early pioneer in CSP technology and still hosts a significant installed capacity, serving as a vital knowledge base for the industry. While new large-scale projects have slowed due to policy shifts and increased competition from PV, the region continues to contribute through R&D, component manufacturing, and project financing expertise. North America, with the United States as a key player, also shows significant potential, particularly in the arid Southwestern states. Past installations have demonstrated the technical feasibility and dispatchability benefits of CSP, and renewed policy interest in long-duration energy storage could reignite significant investment in the region, focusing on integrating CSP with existing grid infrastructure and leveraging its dispatchable power capabilities to enhance grid resilience.

- Middle East and Africa (MEA): This region is a global leader in CSP development, propelled by abundant direct normal irradiance (DNI), ambitious renewable energy targets (e.g., UAE's Energy Strategy 2050, Morocco's Noor Ouarzazate Complex), and significant government investments. Countries like the UAE, Morocco, Saudi Arabia, and Egypt are actively pursuing large-scale CSP projects with integrated thermal storage to diversify their energy mix and meet growing power demand.

- Asia Pacific (APAC): China is a dominant force in this region, driven by its massive energy demand, strong government support for renewable energy, and advancements in domestic CSP technology. India and Australia are also emerging markets, with growing interest in CSP for both power generation and industrial heat applications, leveraging their substantial solar resources.

- Europe: Spain remains the historical leader in Europe for CSP deployment, with a significant installed base. While new projects have seen slower growth, the region continues to be crucial for research and development, component manufacturing, and policy advocacy for dispatchable renewables. Southern European countries and those focused on grid stability show potential for niche or hybrid CSP applications.

- North America: The Southwestern United States, with its high DNI, has hosted pioneering CSP projects. Future growth in this region is expected to be driven by policies promoting long-duration energy storage and the increasing need for grid reliability and stability, positioning CSP as a valuable asset for flexible power generation.

- Latin America: Chile, with its exceptional solar resources in the Atacama Desert, is a notable emerging market for CSP, particularly for its mining industry and grid stabilization. Other countries like Mexico and Brazil also possess significant potential for future CSP development.

Top Key Players:

The market research report covers the analysis of key stake holders of the Concentrating Solar Power Market. Some of the leading players profiled in the report include -

- Global Solar Power Solutions

- Renewable Energy Systems Group

- Horizon Solar Technologies

- GreenVolt Energy Partners

- Sustainable Power Inc.

- SunPeak Renewables

- Atlas Renewable Energy

- Energen Solar

- Helios Power Systems

- NovaVolt Solutions

- TerraWatt Energy

- Quantum Solar Innovations

- Phoenix Renewables

- BrightStar Energy

- Apex Solar Generation

- EcoPower Global

- Radiant Energy Developers

- ClearSky Renewables

- Infinite Solar Systems

- Prime Renewables Holdings

Frequently Asked Questions:

What is Concentrating Solar Power (CSP)?

Concentrating Solar Power (CSP) is a renewable energy technology that uses mirrors or lenses to concentrate a large area of sunlight onto a small area. This concentrated sunlight is then converted into heat, which drives a heat engine (like a steam turbine) to generate electricity. Unlike photovoltaic (PV) solar panels, CSP systems can integrate thermal energy storage, allowing them to generate electricity even when the sun is not shining, providing dispatchable power.

How does CSP differ from standard Photovoltaic (PV) solar?

The primary difference lies in their energy conversion methods. Photovoltaic (PV) solar panels directly convert sunlight into electricity using semiconductors (the photoelectric effect). In contrast, Concentrating Solar Power (CSP) systems first convert sunlight into heat using mirrors to concentrate sunlight, and then this heat is used to generate electricity through a conventional thermal power cycle. CSP's ability to store thermal energy is a key differentiator, offering dispatchable power generation that PV typically cannot provide without separate battery storage.

What are the main types of CSP technologies?

The main types of Concentrating Solar Power (CSP) technologies include parabolic trough systems, solar tower systems, dish/engine systems, and Fresnel reflectors. Parabolic troughs are the most common, using U-shaped mirrors. Solar towers use a field of mirrors (heliostats) to reflect sunlight onto a central receiver atop a tower. Dish/engine systems use a single parabolic dish to focus sunlight onto a Stirling engine. Fresnel reflectors use flat or slightly curved mirrors to concentrate light onto a linear receiver.

What are the key advantages of Concentrating Solar Power (CSP)?

Key advantages of Concentrating Solar Power (CSP) include its ability to provide dispatchable power due to integrated thermal energy storage, allowing for electricity generation on demand, even after sunset or during cloudy periods. CSP also offers high efficiency in large-scale applications and can provide ancillary services to the grid, enhancing stability. Furthermore, it can be combined with other energy sources (hybridization) and is suitable for industrial process heat applications.

Where is the Concentrating Solar Power market expected to grow most significantly?

The Concentrating Solar Power (CSP) market is expected to grow most significantly in regions with high direct normal irradiance (DNI) and supportive renewable energy policies. This primarily includes the Middle East and Africa (MEA), particularly the UAE, Morocco, and Saudi Arabia, due to vast desert resources and ambitious energy diversification goals. Asia Pacific, especially China, is also a key growth region owing to strong government backing and increasing energy demand. Latin America, especially Chile, presents emerging opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted