Compound Semiconductor Market

Compound Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701239 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Compound Semiconductor Market Size

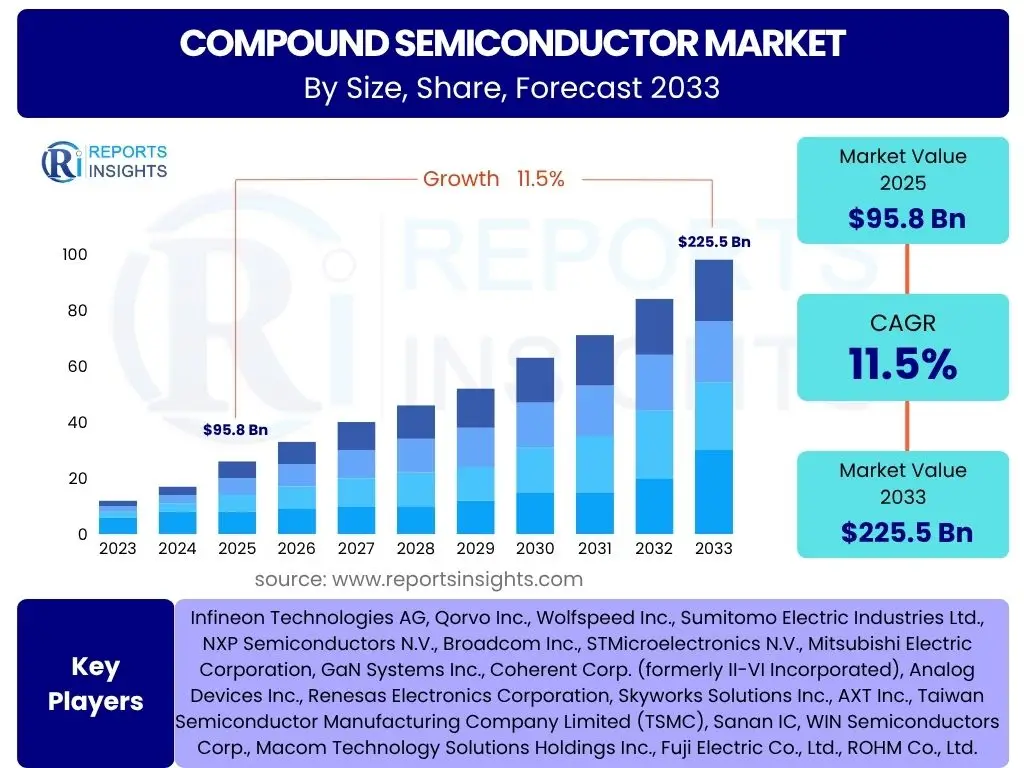

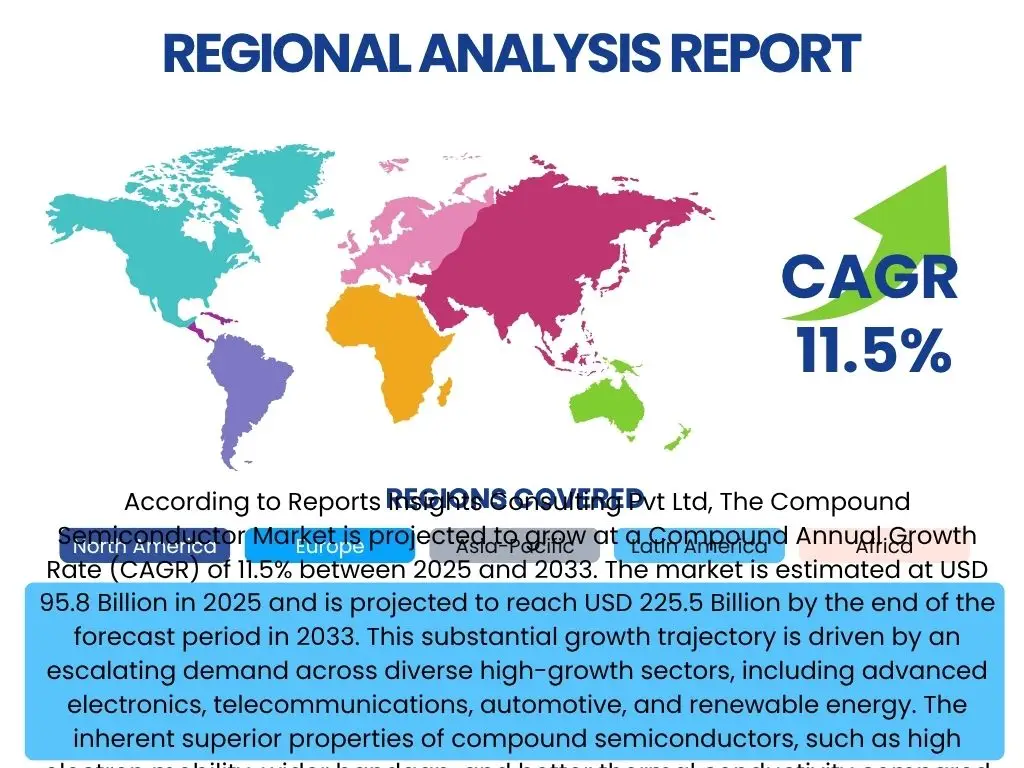

According to Reports Insights Consulting Pvt Ltd, The Compound Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 95.8 Billion in 2025 and is projected to reach USD 225.5 Billion by the end of the forecast period in 2033. This substantial growth trajectory is driven by an escalating demand across diverse high-growth sectors, including advanced electronics, telecommunications, automotive, and renewable energy. The inherent superior properties of compound semiconductors, such as high electron mobility, wider bandgap, and better thermal conductivity compared to traditional silicon, position them as critical enablers for next-generation technological advancements.

The market's expansion is predominantly fueled by the increasing adoption of Gallium Nitride (GaN) and Silicon Carbide (SiC) in power electronics and Radio Frequency (RF) applications. These materials are pivotal for enhancing energy efficiency, reducing device size, and improving performance in various systems, from electric vehicles and fast chargers to 5G infrastructure and data centers. The transition away from silicon in specific high-power and high-frequency applications marks a significant paradigm shift, contributing to the robust market valuation and sustained growth.

Key Compound Semiconductor Market Trends & Insights

The compound semiconductor market is experiencing transformative trends, largely driven by the imperative for enhanced performance, energy efficiency, and miniaturization across critical applications. Users frequently inquire about the leading technological shifts and commercial adoptions that are redefining the industry landscape. Key insights reveal a significant migration towards wide-bandgap materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) due to their superior electrical characteristics, enabling devices to operate at higher voltages, frequencies, and temperatures with greater efficiency than traditional silicon. This material transition is not merely a replacement but an enabler of entirely new capabilities and product designs, addressing the escalating demands of modern electronics for higher power density and reduced energy losses.

Another prominent trend is the explosive growth in applications such as 5G communication infrastructure and electric vehicles (EVs). The deployment of 5G networks necessitates high-performance RF components, where compound semiconductors, particularly GaN, offer unparalleled benefits in terms of power output and efficiency for base stations and mobile devices. Similarly, the automotive industry's electrification trend heavily relies on SiC power devices for EV inverters, onboard chargers, and DC-DC converters, which are critical for extending battery range and reducing charging times. These sector-specific demands are accelerating research, development, and mass production efforts for compound semiconductor devices, driving significant investment and innovation within the ecosystem.

Furthermore, the market is witnessing increased integration and system-level innovation. Beyond discrete components, there is a growing focus on integrating compound semiconductor functionalities into more complex modules and systems, enabling higher levels of performance and functionality in a compact footprint. This includes integrated power modules, RF front-end modules, and advanced sensor solutions, which simplify design for end-users and expand the addressable market for these technologies. Supply chain robustness and strategic partnerships are also becoming increasingly vital, as companies seek to secure material sourcing, manufacturing capacity, and market access in a rapidly expanding and strategically important industry.

- Dominance of Wide-Bandgap Materials: Significant shift towards Gallium Nitride (GaN) and Silicon Carbide (SiC) for high-power and high-frequency applications.

- Rapid Adoption in Electric Vehicles (EVs): SiC power devices are becoming standard in EV powertrain components for improved efficiency and range.

- Expansion in 5G Infrastructure: GaN-based RF devices are crucial for high-performance and efficient 5G base stations and active antenna systems.

- Miniaturization and Integration: Trend towards smaller form factors and higher levels of integration in modules and systems.

- Increased Investment in Wafer Manufacturing: Significant investments in larger wafer sizes (e.g., 6-inch and 8-inch SiC) to achieve economies of scale.

AI Impact Analysis on Compound Semiconductor

The intersection of Artificial Intelligence (AI) and the compound semiconductor market is multifaceted, driving both demand for specialized hardware and fostering revolutionary advancements in design and manufacturing processes. Users often inquire about how AI influences the development of next-generation semiconductors and what new opportunities or challenges arise. AI's insatiable demand for processing power, particularly for complex neural networks and machine learning algorithms, necessitates chips that can perform high-speed computations with exceptional energy efficiency. Compound semiconductors, with their superior electron mobility and power handling capabilities, are uniquely positioned to meet these stringent requirements, especially in high-frequency AI accelerators and edge AI devices, where low latency and power consumption are critical.

Beyond being a consumer of advanced chips, AI is increasingly being leveraged as a transformative tool within the compound semiconductor industry itself. AI and machine learning algorithms are optimizing various stages of the semiconductor lifecycle, from material science research and device design to manufacturing and quality control. For instance, AI can simulate material properties, predict device performance under various conditions, and optimize fabrication processes to reduce defects and improve yield. This capability accelerates the research and development cycles, lowers production costs, and enhances the overall efficiency and reliability of compound semiconductor devices, addressing complex engineering challenges that are difficult to tackle with traditional methods.

Furthermore, the emergence of AI at the edge, where processing occurs closer to the data source rather than solely in centralized cloud data centers, creates new demands for compact, low-power, and high-performance compound semiconductor solutions. Devices like GaN-based power converters can ensure efficient power delivery to AI accelerators in constrained environments, while advanced photonics using compound semiconductors are vital for high-speed optical interconnects within AI data centers. The symbiotic relationship between AI and compound semiconductors is expected to deepen, with AI driving demand for more advanced chips, and in turn, AI tools enabling more sophisticated and efficient production of these very chips, fostering a continuous cycle of innovation and market growth.

- Increased Demand for AI Hardware: Compound semiconductors are critical for high-performance, energy-efficient AI accelerators and edge AI devices due to their superior speed and power handling.

- Optimized Design and Simulation: AI algorithms enhance the efficiency and accuracy of compound semiconductor material design, device modeling, and circuit simulation, reducing development cycles.

- Enhanced Manufacturing Processes: AI-driven analytics and control systems improve manufacturing yield, reduce defects, and optimize processes in wafer fabrication and packaging.

- Energy Efficiency for AI Data Centers: GaN-based power components are crucial for efficient power delivery to power-hungry AI servers, contributing to lower operational costs.

- New Opportunities in AI-Specific Photonics: Compound semiconductor photonics are enabling high-bandwidth optical interconnects essential for AI clusters and data communication.

Key Takeaways Compound Semiconductor Market Size & Forecast

Users frequently seek concise summaries of the most impactful insights from the compound semiconductor market size and forecast. The primary takeaway is the market's robust and sustained growth, driven by the indispensable role of compound semiconductors in powering next-generation technologies. The projected doubling of market value within the forecast period underscores a fundamental shift in the electronics industry, moving towards materials that offer superior performance characteristics over traditional silicon. This growth is not merely incremental but represents a foundational transition towards more efficient, faster, and reliable electronic systems across various sectors, promising significant opportunities for innovation and investment.

A crucial insight is the accelerating adoption of wide-bandgap materials, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials are not just niche components but are becoming mainstream in high-volume applications such as electric vehicles, 5G communication infrastructure, and advanced power electronics. Their ability to deliver enhanced energy efficiency, higher power density, and superior thermal performance is directly addressing critical industry challenges like energy consumption, device miniaturization, and operational reliability. This widespread integration indicates that compound semiconductors are no longer emerging technologies but are established drivers of technological evolution.

Finally, the market forecast highlights the importance of strategic investments in research, development, and manufacturing capacity. To capitalize on this growth, companies must focus on scaling production, innovating new material combinations, and forging strategic partnerships across the value chain. The regional distribution of growth further indicates that Asia Pacific, with its robust manufacturing ecosystem and burgeoning electronics demand, will continue to be a dominant force, while North America and Europe will drive innovation and high-value applications. Understanding these dynamics is essential for stakeholders looking to navigate and capitalize on the significant opportunities within this rapidly expanding market.

- Significant Market Expansion: The compound semiconductor market is set for strong growth, with a projected CAGR of 11.5% from 2025 to 2033, reaching USD 225.5 Billion.

- Pivotal Role in Next-Gen Tech: Compound semiconductors are fundamental enablers for emerging technologies like 5G, EVs, AI, and advanced power solutions.

- Wide-Bandgap Materials Lead Growth: SiC and GaN are the primary growth engines due to their superior performance in high-power and high-frequency applications.

- Application-Driven Demand: Strong demand from automotive, IT & telecom, and industrial sectors is propelling market expansion.

- Strategic Investment Focus: Continuous investment in R&D, manufacturing capacity, and supply chain resilience is crucial for market stakeholders.

Compound Semiconductor Market Drivers Analysis

The compound semiconductor market is propelled by a confluence of technological advancements and increasing demands across various high-growth industries. The inherent superior properties of these materials, such as higher electron mobility, wider bandgap, and better thermal conductivity compared to silicon, make them indispensable for applications requiring high efficiency, power density, and operational reliability. Key drivers include the global rollout of 5G networks, the accelerating adoption of electric vehicles, and the continuous innovation in consumer electronics and data centers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Expansion of 5G Infrastructure | +2.5% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 |

| Growing Adoption of Electric Vehicles (EVs) | +2.0% | Global, particularly China, Europe, North America | 2025-2033 |

| Increasing Demand for Energy-Efficient Power Electronics | +1.8% | Global, strong in industrialized nations | 2025-2033 |

| Advancements in Consumer Electronics (e.g., fast chargers) | +1.5% | Global, particularly Asia Pacific | 2025-2030 |

| Rising Investment in Data Centers and AI | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

Compound Semiconductor Market Restraints Analysis

Despite significant growth potential, the compound semiconductor market faces several notable restraints that could temper its expansion. These challenges often revolve around the inherent complexities of manufacturing and the higher costs associated with these advanced materials. Overcoming these hurdles will be crucial for the industry to realize its full market potential and achieve broader adoption across various applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Complex Production Processes | -1.5% | Global, impacting smaller players | 2025-2030 |

| Supply Chain Vulnerabilities and Raw Material Scarcity | -1.0% | Global, particularly regions dependent on specific suppliers | 2025-2028 |

| Design and Integration Challenges | -0.8% | Global, particularly for new adopters | 2025-2029 |

Compound Semiconductor Market Opportunities Analysis

The compound semiconductor market presents significant opportunities driven by emerging technologies, increasing demand for high-performance solutions, and the ongoing push for energy efficiency. These opportunities allow for market diversification and penetration into new, high-value applications, offering substantial long-term growth prospects for industry participants.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Space and Defense Applications | +1.5% | North America, Europe, Asia Pacific (Defense-focused) | 2025-2033 |

| Emergence of Quantum Computing and Advanced Photonics | +1.2% | Global, particularly R&D hubs | 2028-2033 |

| Increasing Focus on Renewable Energy Systems (Solar Inverters, Grid) | +1.0% | Europe, Asia Pacific, North America | 2025-2033 |

| Growth of Advanced Sensing and Imaging Technologies | +0.8% | Global | 2025-2031 |

Compound Semiconductor Market Challenges Impact Analysis

The compound semiconductor market, while promising, must navigate several inherent challenges that could impede its growth and widespread adoption. These challenges range from technical complexities and the need for specialized expertise to broader market dynamics and competitive pressures. Addressing these issues effectively will be crucial for sustained success and market penetration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Entry Barriers and Significant Capital Investment | -0.9% | Global, particularly for new entrants | 2025-2033 |

| Lack of Skilled Workforce and Technical Expertise | -0.7% | Global, impacting R&D and manufacturing | 2025-2033 |

| Reliability and Quality Assurance for Mass Production | -0.5% | Global | 2025-2030 |

Compound Semiconductor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Compound Semiconductor Market, offering a detailed segmentation by material type, application, end-use industry, and wafer size, alongside a thorough regional and country-level breakdown. The report covers historical market performance, current market dynamics, and future projections, aiming to equip stakeholders with actionable insights into market size, growth drivers, restraints, opportunities, and competitive landscape. It also includes an extensive analysis of the impact of emerging technologies such as Artificial Intelligence on the market's trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 95.8 Billion |

| Market Forecast in 2033 | USD 225.5 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, Qorvo Inc., Wolfspeed Inc., Sumitomo Electric Industries Ltd., NXP Semiconductors N.V., Broadcom Inc., STMicroelectronics N.V., Mitsubishi Electric Corporation, GaN Systems Inc., Coherent Corp. (formerly II-VI Incorporated), Analog Devices Inc., Renesas Electronics Corporation, Skyworks Solutions Inc., AXT Inc., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Sanan IC, WIN Semiconductors Corp., Macom Technology Solutions Holdings Inc., Fuji Electric Co., Ltd., ROHM Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Compound Semiconductor Market is comprehensively segmented to provide granular insights into its diverse components, enabling a precise understanding of market dynamics across various dimensions. This segmentation allows stakeholders to identify key growth pockets, assess competitive landscapes within specific niches, and tailor strategies to address distinct market needs. The detailed breakdown covers the foundational material types, the functional applications of these semiconductors, the specific end-use industries leveraging them, and the critical manufacturing aspect of wafer sizes.

- By Material Type:

- Gallium Nitride (GaN): Highly efficient for high-frequency RF and power applications, including 5G base stations, fast chargers, and data centers.

- Silicon Carbide (SiC): Essential for high-power, high-voltage applications such as electric vehicle inverters, industrial power supplies, and renewable energy systems due to its superior thermal conductivity and breakdown voltage.

- Gallium Arsenide (GaAs): Predominantly used in high-speed RF applications for mobile devices, optical communications, and satellite communications.

- Indium Phosphide (InP): Critical for fiber optic communication systems, high-speed data transfer, and specialized photonic devices.

- Other Compound Semiconductor Materials: Includes materials like Silicon Germanium (SiGe), Zinc Oxide (ZnO), and others used for niche applications such as advanced sensors and niche optoelectronics.

- By Application:

- Power Electronics: Devices like power switches, rectifiers, and converters used in power management for various systems.

- RF Devices: Components for wireless communication, radar, and broadcasting, including power amplifiers and low noise amplifiers.

- Photonics: Devices that generate, manipulate, or detect light, such as LEDs, laser diodes, and optical sensors.

- Sensors: Advanced sensors for environmental monitoring, industrial control, and automotive safety systems.

- Others: Including specialized devices for quantum computing, medical imaging, and scientific research.

- By End-Use Industry:

- Automotive: Electric vehicles (EVs), hybrid electric vehicles (HEVs), autonomous driving systems, and advanced driver-assistance systems (ADAS).

- Consumer Electronics: Smartphones, laptops, gaming consoles, and various smart home devices requiring efficient power and RF solutions.

- IT & Telecom: 5G infrastructure, data centers, enterprise networks, and cloud computing equipment.

- Industrial: Power supplies, motor drives, robotics, and automation equipment.

- Aerospace & Defense: Radar systems, satellite communications, electronic warfare, and avionics.

- Healthcare: Medical imaging equipment, diagnostic devices, and wearable health monitors.

- Others: Including energy, smart grid, and research sectors.

- By Wafer Size:

- 2-inch, 4-inch, 6-inch, 8-inch, Above 8-inch: Reflecting the evolution of manufacturing scale and efficiency for different compound semiconductor materials and applications.

Regional Highlights

The global compound semiconductor market exhibits distinct regional dynamics, influenced by local technological advancements, industrial ecosystems, and government policies. Asia Pacific consistently leads the market, primarily driven by its robust electronics manufacturing base, significant investments in 5G infrastructure, and the burgeoning electric vehicle market in countries like China, Japan, and South Korea. This region not only serves as a major consumer but also as a critical production hub for various compound semiconductor devices, benefiting from extensive supply chains and substantial government support for semiconductor industries. The rapid urbanization and increasing disposable income also fuel demand for advanced consumer electronics, further boosting market growth in this region.

North America is a pivotal region for innovation and high-value applications, characterized by strong research and development activities, particularly in aerospace and defense, advanced computing, and telecommunications. The presence of leading semiconductor companies and a significant focus on next-generation technologies like AI and quantum computing contribute to its market share. Government initiatives aimed at bolstering domestic semiconductor manufacturing and supply chain resilience are also expected to drive investment and growth. Europe, while smaller in market size compared to Asia Pacific, is a key player in automotive electronics and industrial applications, especially with its stringent energy efficiency regulations and strong push for electric vehicle adoption, which drives demand for SiC power devices. Countries like Germany and France are investing heavily in semiconductor research and manufacturing capabilities.

Latin America and the Middle East & Africa (MEA) are emerging markets for compound semiconductors, albeit with slower adoption rates. Latin America's growth is primarily tied to the expansion of telecommunications infrastructure and increasing industrialization, particularly in Brazil and Mexico. The MEA region is witnessing growing investments in smart city projects, renewable energy, and telecommunications, which are creating new opportunities for compound semiconductors in power management and communication systems. However, these regions often rely on imports and face challenges related to technological expertise and infrastructure development, which may moderate their growth compared to more established markets.

- Asia Pacific (APAC): Dominant market share driven by extensive electronics manufacturing, rapid 5G deployment, and large-scale EV adoption in China, Japan, South Korea, and Taiwan. Significant government support and robust supply chains characterize this region.

- North America: A leader in R&D and high-value applications, with strong demand from aerospace & defense, IT & telecom, and advanced computing sectors. Focus on domestic manufacturing and innovation for AI and specialized high-frequency components.

- Europe: Key region for automotive electronics (especially SiC in EVs), industrial power applications, and renewable energy. Driven by stringent energy efficiency standards and a growing focus on sustainable technologies.

- Latin America: Emerging market with growing demand in telecommunications infrastructure and industrial applications, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Gradual adoption of compound semiconductors driven by investments in smart infrastructure, renewable energy projects, and expanding telecom networks.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Compound Semiconductor Market.- Infineon Technologies AG

- Qorvo Inc.

- Wolfspeed Inc.

- Sumitomo Electric Industries Ltd.

- NXP Semiconductors N.V.

- Broadcom Inc.

- STMicroelectronics N.V.

- Mitsubishi Electric Corporation

- GaN Systems Inc.

- Coherent Corp.

- Analog Devices Inc.

- Renesas Electronics Corporation

- Skyworks Solutions Inc.

- AXT Inc.

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Sanan IC

- WIN Semiconductors Corp.

- Macom Technology Solutions Holdings Inc.

- Fuji Electric Co., Ltd.

- ROHM Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Compound Semiconductor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the Compound Semiconductor Market size and its projected growth?

The Compound Semiconductor Market is estimated at USD 95.8 Billion in 2025 and is projected to reach USD 225.5 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 11.5%. This robust growth is driven by increasing adoption in electric vehicles, 5G infrastructure, and energy-efficient power electronics.

Which are the key materials driving the compound semiconductor market?

The market is primarily driven by the increasing adoption of wide-bandgap materials such as Silicon Carbide (SiC) and Gallium Nitride (GaN). SiC is vital for high-power applications like electric vehicle inverters, while GaN excels in high-frequency RF applications for 5G and fast chargers.

How is AI impacting the compound semiconductor industry?

AI significantly impacts the compound semiconductor industry in two ways: it drives demand for high-performance, energy-efficient chips required for AI accelerators and edge AI devices, and it optimizes the design, manufacturing, and testing processes of compound semiconductors through advanced algorithms.

What are the main applications of compound semiconductors?

Compound semiconductors find extensive applications in power electronics (e.g., power converters, inverters), RF devices (e.g., 5G base stations, mobile phones), photonics (e.g., LEDs, laser diodes, optical sensors), and various advanced sensors used across automotive, consumer electronics, IT & telecom, and industrial sectors.

Which regions are leading the growth in the Compound Semiconductor Market?

Asia Pacific is the dominant region due to its strong manufacturing base and high demand from consumer electronics, 5G, and EV sectors. North America and Europe are also significant players, leading in R&D, high-value applications, and automotive electrification.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted