Composite Rebar Market

Composite Rebar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701464 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Composite Rebar Market Size

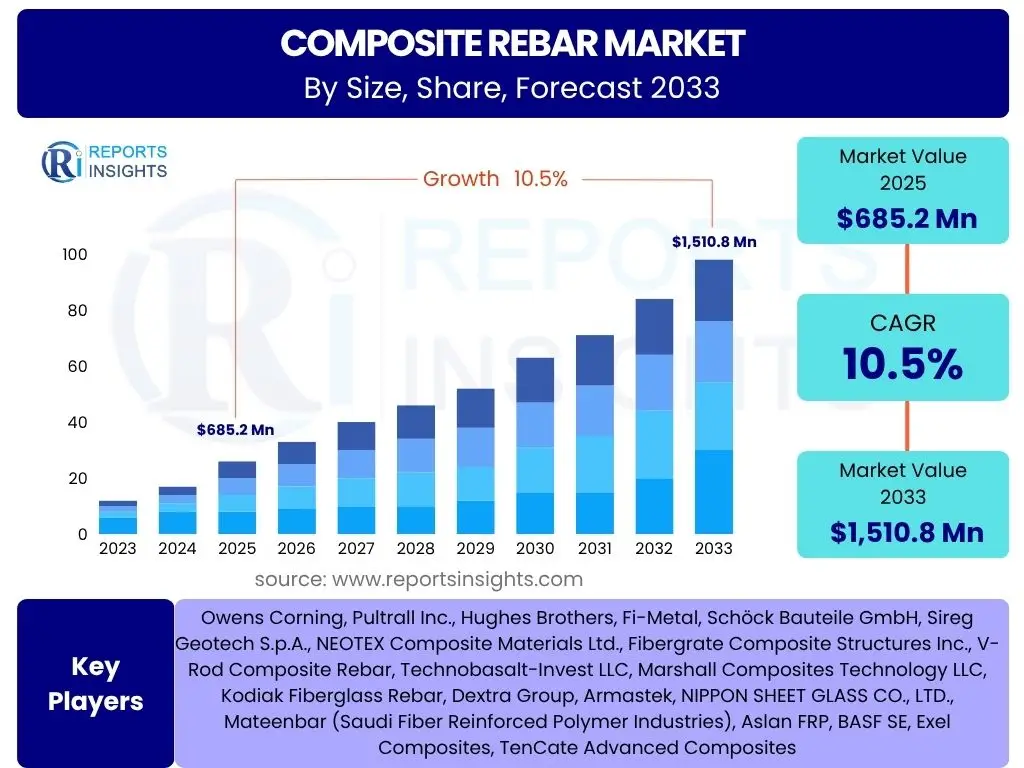

According to Reports Insights Consulting Pvt Ltd, The Composite Rebar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 685.2 Million in 2025 and is projected to reach USD 1,510.8 Million by the end of the forecast period in 2033.

Key Composite Rebar Market Trends & Insights

User inquiries frequently focus on the evolving applications and technological advancements within the composite rebar sector. Analysis reveals a prominent interest in the increasing adoption of these materials due to their superior corrosion resistance and lightweight properties, particularly in demanding environmental conditions such as marine and coastal infrastructure. Furthermore, there is a growing emphasis on sustainable construction practices, driving demand for materials with a lower environmental footprint, which composite rebar often offers through reduced energy consumption in manufacturing and longer lifespan. The market is also witnessing a diversification of composite types, including basalt and carbon fiber reinforced polymers, alongside traditional glass fiber options, to cater to specific performance requirements and cost considerations across various construction segments.

Another significant trend is the rise of prefabrication and modular construction methods, where composite rebar's lightweight nature and ease of handling provide distinct advantages, accelerating project timelines and reducing on-site labor. The integration of smart technologies for quality control and material tracking is also emerging as a key area of interest, enhancing the reliability and traceability of composite rebar in large-scale projects. Furthermore, standardization efforts and the development of more robust design codes for composite rebar are critical trends addressing previous concerns regarding regulatory acceptance and widespread adoption, thereby fostering greater confidence among engineers and contractors. The market is increasingly seeing bespoke solutions tailored for specific projects, indicating a shift towards performance-driven material selection rather than traditional commodity-based choices.

- Growing adoption in corrosion-prone environments (e.g., marine, coastal).

- Increased focus on sustainable and resilient infrastructure.

- Development of advanced composite material formulations (e.g., BFRP, CFRP).

- Integration into prefabricated and modular construction techniques.

- Rising demand from seismic-prone regions due to superior elastic properties.

- Advancements in manufacturing processes leading to cost reduction and quality improvement.

- Development of standardized building codes and industry specifications.

AI Impact Analysis on Composite Rebar

User questions regarding the impact of AI on the composite rebar market predominantly revolve around optimizing manufacturing processes, enhancing material properties through advanced design, and improving quality control. There is a strong expectation that AI will streamline production, reduce waste, and enable the creation of more customized and high-performance composite rebar solutions. Concerns often center on the initial investment required for AI integration and the need for specialized skills to manage these sophisticated systems, but the overall sentiment is positive regarding AI's potential to drive efficiency and innovation in material science and construction.

The application of artificial intelligence is anticipated to revolutionize various stages of the composite rebar lifecycle, from raw material selection to end-of-life considerations. AI-driven predictive analytics can optimize resin curing times and fiber lay-up patterns in the pultrusion process, ensuring consistent product quality and minimizing defects. Machine learning algorithms can analyze vast datasets of material properties and performance under stress, facilitating the design of novel composite formulations with enhanced strength, durability, and cost-effectiveness. Furthermore, AI-powered computer vision systems can conduct real-time inspections during manufacturing, identifying anomalies and ensuring adherence to stringent quality standards, thereby reducing the need for manual checks and improving overall reliability. This level of precision and optimization is crucial for high-performance construction materials like composite rebar.

- Optimization of manufacturing processes: AI algorithms can refine pultrusion parameters for enhanced efficiency and reduced material waste.

- Advanced material design: Machine learning assists in predicting and optimizing composite rebar properties based on varying fiber and resin compositions.

- Predictive maintenance for machinery: AI can anticipate equipment failures in production lines, minimizing downtime and increasing output.

- Enhanced quality control: Computer vision and AI analytics enable real-time defect detection and quality assurance during manufacturing.

- Supply chain optimization: AI-driven insights can improve logistics, inventory management, and raw material procurement for composite rebar manufacturers.

- Simulation and performance prediction: AI models can simulate rebar performance under various environmental conditions and loads, accelerating R&D.

Key Takeaways Composite Rebar Market Size & Forecast

Common user inquiries about the Composite Rebar market size and forecast highlight a strong interest in its rapid growth trajectory, driven by increasing awareness of its superior properties over traditional steel, particularly in corrosion-prone applications. Users often seek confirmation of the market's long-term viability and its potential to disrupt conventional construction practices. The insights suggest that the market is poised for substantial expansion, supported by significant infrastructure investments globally and a growing emphasis on resilient and sustainable building materials. The forecast indicates robust growth, primarily propelled by the material's benefits in challenging environments and its alignment with modern construction demands for durability and longevity, despite initial cost considerations.

The market's projected expansion is underpinned by several critical factors, including the global push for infrastructure modernization and the adoption of advanced materials in areas susceptible to corrosion, such as bridges, marine structures, and wastewater treatment facilities. The lightweight nature of composite rebar also contributes to reduced transportation costs and easier on-site handling, offering tangible economic benefits over the lifecycle of a project. Furthermore, the increasing stringency of environmental regulations and the desire for extended service life in critical infrastructure are compelling engineers and developers to specify composite rebar, thereby accelerating its market penetration. This comprehensive view reinforces the strong positive outlook for the composite rebar sector.

- The Composite Rebar Market is experiencing significant growth, projected to more than double in value by 2033.

- Corrosion resistance is the primary driver, making composite rebar indispensable for marine and high-salinity environments.

- Increased infrastructure spending globally, especially in developing regions, fuels demand for durable alternatives to steel.

- Sustainable construction practices and the need for long-life cycle materials are boosting adoption.

- Technological advancements in manufacturing are steadily reducing production costs, making composite rebar more competitive.

- North America and Asia Pacific are anticipated to be key growth engines due to extensive infrastructure development and renovation projects.

Composite Rebar Market Drivers Analysis

The Composite Rebar market is significantly propelled by its inherent advantages over conventional steel reinforcement, particularly its exceptional corrosion resistance. This characteristic makes it an ideal material for infrastructure projects in harsh environments, such as coastal regions, marine structures, and areas exposed to de-icing salts or aggressive chemicals, where steel rebar rapidly deteriorates. The growing global investment in resilient infrastructure, coupled with a focus on extending the service life of construction assets, directly contributes to the increasing adoption of composite rebar, as it substantially reduces maintenance costs and premature structural failures associated with corrosion.

Furthermore, the lightweight nature of composite rebar offers substantial logistical and operational benefits, leading to reduced transportation costs, easier handling on job sites, and faster installation times. This contributes to overall project efficiency and lower labor expenses. The high tensile strength-to-weight ratio of composite rebar also allows for innovative designs and potentially thinner concrete sections, optimizing material usage. Coupled with a growing emphasis on sustainable and green building practices, where materials with lower embodied energy and longer lifespans are preferred, composite rebar aligns well with contemporary construction demands, driving its market expansion across various application segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Superior Corrosion Resistance | +2.8% | Global, particularly Coastal & Marine Regions | 2025-2033 |

| Increasing Infrastructure Spending | +2.5% | North America, Asia Pacific, Europe | 2025-2033 |

| Lightweight Properties & Ease of Handling | +1.9% | Global, especially Urban Construction Zones | 2025-2033 |

| Demand for Sustainable Construction Materials | +1.5% | Europe, North America, Japan | 2027-2033 |

| Non-Conductive & Non-Magnetic Properties | +1.0% | Hospitals, Research Facilities, Power Plants | 2025-2030 |

Composite Rebar Market Restraints Analysis

Despite its numerous advantages, the Composite Rebar market faces significant restraints, primarily its higher initial material cost compared to traditional steel rebar. While composite rebar offers long-term savings through reduced maintenance and extended service life, the upfront investment can deter projects with limited budgets or those focused solely on immediate capital expenditure. This cost disparity is particularly pronounced in regions where steel prices are low or where project timelines do not factor in lifecycle cost analyses, thereby limiting widespread adoption in cost-sensitive applications and segments.

Another major restraint is the lack of comprehensive and universally accepted standardized building codes and design guidelines for composite rebar in some regions. While progress is being made, the absence of extensive regulatory frameworks and the relatively limited historical data compared to steel can create hesitancy among engineers, architects, and contractors. This perceived risk and the unfamiliarity with composite rebar design principles often lead to a preference for proven, traditional materials. Furthermore, the specialized knowledge and training required for handling and installing composite rebar, differing from steel, can pose a challenge, contributing to slower market penetration in areas with a less experienced workforce or limited access to such training.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Initial Material Cost | -2.0% | Global, particularly Developing Economies | 2025-2030 |

| Limited Awareness & Acceptance in Traditional Construction | -1.5% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Lack of Standardized Building Codes & Design Guidelines | -1.2% | Global, particularly less regulated markets | 2025-2028 |

| Perceived Bonding Issues with Concrete (compared to steel) | -0.8% | North America, Europe (historical concerns) | 2025-2027 |

| Manufacturing Complexity & Capacity Limitations | -0.5% | Global (impacts supply scalability) | 2025-2029 |

Composite Rebar Market Opportunities Analysis

The Composite Rebar market presents significant opportunities driven by the global imperative for infrastructure repair and upgrades, particularly in regions with aging structures susceptible to corrosion. Governments and private entities are increasingly allocating funds towards projects that demand long-term durability and minimal maintenance, thereby creating a substantial demand for materials like composite rebar. The expansion of smart city initiatives and the development of high-performance buildings also provide avenues for growth, as these projects often require materials that offer advanced properties beyond traditional steel, such as non-conductivity and non-magnetism for sensitive electrical installations.

Furthermore, the marine and coastal construction sectors represent a substantial growth opportunity, given the severe corrosive environments that necessitate a superior alternative to steel. This includes applications in seawalls, jetties, docks, and offshore platforms where the lifespan of traditional materials is significantly curtailed. Emerging applications in niche markets, such as tunnel boring projects where non-metallic reinforcement is crucial, and in specialized industrial facilities prone to chemical exposure, further diversify the opportunity landscape. Continued research and development in composite materials, focusing on cost reduction and enhanced bonding with concrete, will unlock even broader market potential and accelerate adoption in conventional construction segments currently dominated by steel.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure Rehabilitation & Renovation | +2.2% | North America, Europe | 2025-2033 |

| Growth in Marine & Coastal Construction | +1.8% | Global, especially Asia Pacific, Europe, Middle East | 2025-2033 |

| Development of Smart Cities & Advanced Building Concepts | +1.5% | North America, Europe, China | 2027-2033 |

| Niche Applications in Tunnels & Industrial Facilities | +1.0% | Global (project-specific) | 2025-2030 |

| Technological Advancements in Manufacturing & Material Composition | +0.8% | Global (improves competitiveness) | 2025-2033 |

Composite Rebar Market Challenges Impact Analysis

The Composite Rebar market faces significant challenges, particularly the entrenched preference for traditional steel reinforcement within the construction industry, largely due to its long history, established supply chains, and familiarity among engineers and contractors. Overcoming this inertia requires substantial educational efforts and demonstrations of long-term value, which can be a slow process. The construction sector's inherent resistance to change and its risk-averse nature mean that new materials, even with superior properties, often face an uphill battle for widespread acceptance, especially in critical structural applications where safety and reliability are paramount. This cultural barrier prolongs the market penetration cycle for composite rebar.

Another key challenge involves the scalability of production and the current limitations in manufacturing capacity for composite rebar compared to the massive output of steel mills. Meeting the demand for large-scale infrastructure projects requires significant investment in specialized manufacturing facilities, which can be a barrier to rapid market expansion. Additionally, the supply chain for specific fiber types and resins used in composite rebar can be less mature or more susceptible to fluctuations than that for steel, leading to potential cost volatility or supply disruptions. Furthermore, ensuring consistent quality across different manufacturers and maintaining competitive pricing while scaling up production remains a complex task for the industry. These factors collectively contribute to the challenges in achieving mainstream adoption and competing directly with the volume and price points of traditional steel reinforcement.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Traditional Steel Rebar | -1.8% | Global, especially developing markets | 2025-2033 |

| Limited Industry Expertise & Training | -1.3% | Global, particularly less developed construction markets | 2025-2030 |

| Need for Increased Capital Investment in Manufacturing | -1.0% | Global (impacts scalability) | 2025-2029 |

| Perceived High Risk by Conservative Construction Industry | -0.7% | Global (impacts adoption) | 2025-2033 |

| Supply Chain Vulnerabilities for Raw Materials | -0.5% | Global (impacts cost and availability) | 2025-2028 |

Composite Rebar Market - Updated Report Scope

This market insights report provides an in-depth analysis of the global Composite Rebar market, encompassing its current size, historical growth trends, and future projections up to 2033. It details key market dynamics, including drivers, restraints, opportunities, and challenges, and offers a comprehensive segmentation analysis by fiber type, resin type, application, end-use industry, and manufacturing process. The report also highlights regional market landscapes and profiles key industry players, offering a strategic overview for stakeholders seeking to understand market potential, competitive dynamics, and investment opportunities within the composite rebar sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.2 Million |

| Market Forecast in 2033 | USD 1,510.8 Million |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Owens Corning, Pultrall Inc., Hughes Brothers, Fi-Metal, Schöck Bauteile GmbH, Sireg Geotech S.p.A., NEOTEX Composite Materials Ltd., Fibergrate Composite Structures Inc., V-Rod Composite Rebar, Technobasalt-Invest LLC, Marshall Composites Technology LLC, Kodiak Fiberglass Rebar, Dextra Group, Armastek, NIPPON SHEET GLASS CO., LTD., Mateenbar (Saudi Fiber Reinforced Polymer Industries), Aslan FRP, BASF SE, Exel Composites, TenCate Advanced Composites |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Composite Rebar Market is extensively segmented to provide a granular view of its diverse applications and material compositions. This segmentation allows for a detailed understanding of market dynamics across different product types and end-use industries, facilitating targeted strategies for market entry and product development. Each segment represents a distinct market niche, influenced by specific performance requirements, regulatory landscapes, and economic factors, ultimately contributing to the overall market growth and evolution.

Further analysis within these segments highlights the dominance of Glass Fiber Reinforced Polymer (GFRP) rebar due to its cost-effectiveness and proven track record, while Basalt Fiber Reinforced Polymer (BFRP) and Carbon Fiber Reinforced Polymer (CFRP) are gaining traction in high-performance and specialized applications requiring superior strength or non-corrosive properties. The application segment reveals strong demand from infrastructure projects, particularly in marine and bridge construction, driven by the need for durable materials in aggressive environments. The various resin types, such as vinyl ester and epoxy, are selected based on the specific chemical resistance and mechanical properties required for the end-use, demonstrating the versatility of composite rebar solutions across a broad spectrum of construction and industrial needs.

- By Fiber Type:

- Glass Fiber Reinforced Polymer (GFRP)

- Basalt Fiber Reinforced Polymer (BFRP)

- Carbon Fiber Reinforced Polymer (CFRP)

- Aramid Fiber Reinforced Polymer (AFRP)

- By Resin Type:

- Vinyl Ester

- Polyester

- Epoxy

- Other Resins

- By Application:

- Infrastructure

- Bridges

- Roads

- Tunnels

- Highways

- Ports

- Marine Structures

- Railways

- Airports

- Building & Construction

- Residential Buildings

- Commercial Buildings

- Industrial Buildings

- Foundations

- Slabs

- Walls

- Water Management

- Wastewater Treatment Plants

- Water Tanks

- Drainage Systems

- Canals

- Industrial

- Chemical Plants

- Power Plants

- Mining

- Oil & Gas

- Others

- Precast Concrete

- Architectural Applications

- Seismic Zones

- Infrastructure

- By End-Use Industry:

- Transportation

- Construction

- Marine

- Chemical

- Energy

- By Manufacturing Process:

- Pultrusion

- Filament Winding

- Resin Transfer Molding (RTM)

Regional Highlights

The global Composite Rebar market exhibits distinct regional dynamics driven by varying levels of infrastructure development, regulatory environments, and adoption rates of advanced construction materials. North America is a prominent market, characterized by significant investments in rehabilitating aging infrastructure and a growing awareness of composite rebar's lifecycle benefits in corrosion-prone regions. The region's stringent building codes and emphasis on durable, low-maintenance solutions for bridges, highways, and marine structures further drive demand, with states like Florida and provinces in Canada leading the adoption.

Europe stands as another key region, propelled by strict environmental regulations and a strong focus on sustainable and resilient construction. Countries such as Germany, the UK, and Scandinavian nations are increasingly integrating composite rebar into their public and private infrastructure projects, particularly for projects requiring extended service life and reduced environmental impact. The Asia Pacific region is anticipated to demonstrate the highest growth rate, fueled by rapid urbanization, extensive infrastructure development in countries like China and India, and a burgeoning demand for advanced materials in new construction and seismic-resistant structures. Latin America and the Middle East & Africa are emerging markets, with specific applications in coastal development, oil & gas infrastructure, and areas requiring non-magnetic or corrosion-resistant reinforcement, presenting long-term growth opportunities as awareness and project investments increase.

- North America: Leads in adoption due to extensive infrastructure repair needs, high awareness of lifecycle costs, and applications in regions exposed to de-icing salts or coastal environments. Significant research and development activities also contribute to market growth.

- Europe: Driven by stringent environmental regulations, a strong focus on sustainable building practices, and demand for durable solutions in bridge rehabilitation and marine infrastructure. Germany, the UK, and Scandinavian countries are key contributors.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid urbanization, massive infrastructure development projects (e.g., in China, India, and Southeast Asian countries), and increasing emphasis on resilient construction in seismic zones.

- Latin America: Emerging market with growing potential, particularly in countries with significant coastal infrastructure or those investing in new public works projects where long-term durability is a priority.

- Middle East & Africa (MEA): Growth driven by large-scale construction projects, often in harsh desert or coastal environments, necessitating corrosion-resistant materials for critical infrastructure like desalination plants, bridges, and tunnels.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Composite Rebar Market.- Owens Corning

- Pultrall Inc.

- Hughes Brothers

- Fi-Metal

- Schöck Bauteile GmbH

- Sireg Geotech S.p.A.

- NEOTEX Composite Materials Ltd.

- Fibergrate Composite Structures Inc.

- V-Rod Composite Rebar

- Technobasalt-Invest LLC

- Marshall Composites Technology LLC

- Kodiak Fiberglass Rebar

- Dextra Group

- Armastek

- NIPPON SHEET GLASS CO., LTD.

- Mateenbar (Saudi Fiber Reinforced Polymer Industries)

- Aslan FRP

- BASF SE

- Exel Composites

- TenCate Advanced Composites

Frequently Asked Questions

Analyze common user questions about the Composite Rebar market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is composite rebar and how does it differ from traditional steel rebar?

Composite rebar, typically made from fibers like glass, basalt, or carbon embedded in a polymer resin, is a non-corrosive, lightweight, and high-strength alternative to steel rebar. Unlike steel, it does not rust, is non-conductive, and non-magnetic, offering superior durability in harsh environments and specific applications.

What are the primary benefits of using composite rebar in construction projects?

The main benefits include exceptional corrosion resistance, significantly extending the lifespan of concrete structures; lightweight properties, leading to reduced transportation costs and easier handling; high tensile strength; and its non-conductive nature, making it ideal for electrical or sensitive magnetic environments. It also contributes to sustainable construction due to its durability.

Is composite rebar more expensive than steel rebar, and is it cost-effective in the long run?

Composite rebar typically has a higher initial material cost than steel rebar. However, it offers substantial long-term cost savings by eliminating corrosion-related maintenance, repairs, and premature replacement of structures, especially in aggressive environments, thus proving more cost-effective over the lifecycle of a project.

In which applications is composite rebar most commonly used?

Composite rebar is predominantly used in infrastructure projects such as bridges, roads, tunnels, and marine structures (seawalls, jetties) due to its corrosion resistance. It also sees use in water treatment plants, industrial facilities exposed to chemicals, magnetic resonance imaging (MRI) rooms, and in seismic-resistant construction.

What are the future prospects for the composite rebar market?

The composite rebar market is projected for robust growth, driven by increasing global infrastructure investments, a strong focus on sustainable and resilient construction, and the ongoing need for durable materials in demanding environments. Advancements in manufacturing and growing awareness are expected to broaden its adoption across conventional and niche applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted