Aerospace and Defense Thermoplastic Composite Market

Aerospace and Defense Thermoplastic Composite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700753 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

Aerospace and Defense Thermoplastic Composite Market Size

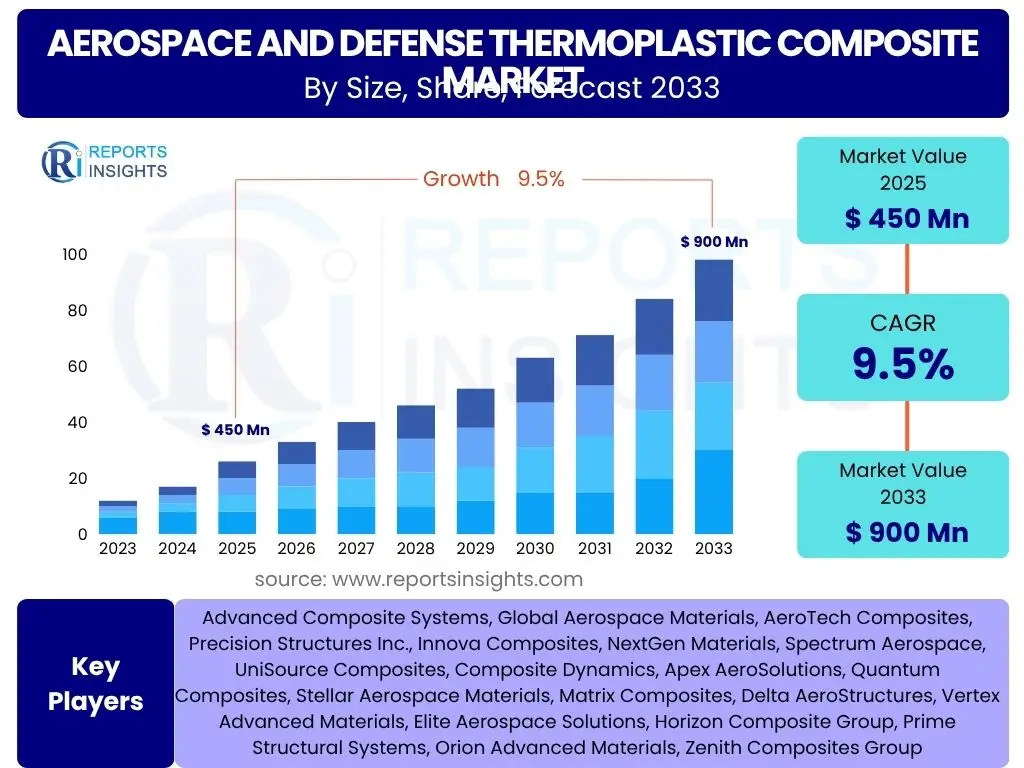

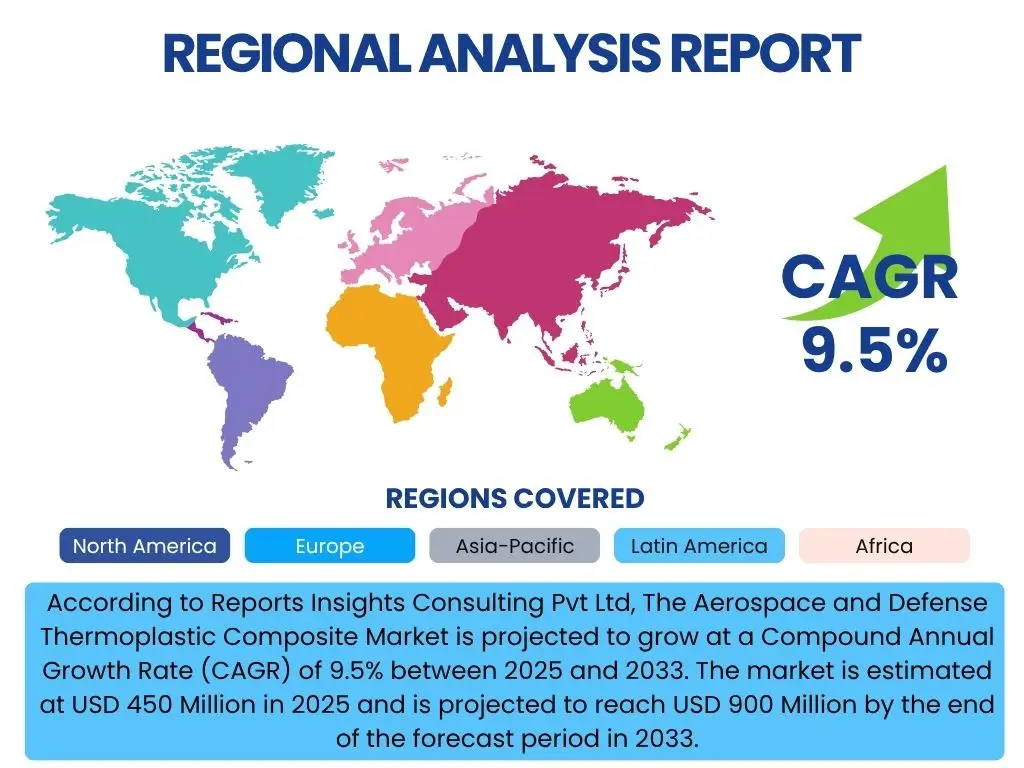

According to Reports Insights Consulting Pvt Ltd, The Aerospace and Defense Thermoplastic Composite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 900 Million by the end of the forecast period in 2033.

Key Aerospace and Defense Thermoplastic Composite Market Trends & Insights

The Aerospace and Defense Thermoplastic Composite market is experiencing transformative trends driven by the increasing demand for lightweight, high-performance materials in aviation and defense applications. Key user inquiries often revolve around the adoption of advanced manufacturing techniques, the push for enhanced fuel efficiency, and the integration of sustainable materials. There is a growing focus on automation in composite manufacturing, leading to faster production cycles and reduced costs, which is a significant factor in market expansion. Furthermore, the longevity and recyclability of thermoplastic composites are attracting considerable attention, aligning with global environmental objectives and industry sustainability initiatives. The continuous evolution of material science, particularly in fiber and resin combinations, is opening new possibilities for structural applications across diverse aerospace platforms.

Another prominent trend is the diversification of applications beyond traditional airframes, extending into space launch vehicles, unmanned aerial vehicles (UAVs), and missile systems. Users frequently inquire about the performance benefits of these composites in extreme operating conditions and their resistance to fatigue and impact. The ongoing development of regulatory frameworks supporting the use of advanced materials in critical aerospace structures also plays a crucial role. The industry is witnessing a shift towards multi-functional composites that can integrate sensors or provide thermal management, moving beyond purely structural roles. This convergence of material science with smart technologies is a key area of interest, reflecting the industry's drive for integrated solutions.

- Increasing adoption of Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) for complex geometries.

- Growing demand for lightweight materials to enhance fuel efficiency and reduce emissions in commercial and military aircraft.

- Expansion of applications in urban air mobility (UAM), drones, and space exploration.

- Development of high-performance thermoplastic resins offering superior strength-to-weight ratios and improved damage tolerance.

- Focus on sustainability and recyclability of thermoplastic composites reducing environmental footprint.

- Integration of smart features and multi-functional capabilities within composite structures.

AI Impact Analysis on Aerospace and Defense Thermoplastic Composite

The integration of Artificial intelligence (AI) is fundamentally reshaping the Aerospace and Defense Thermoplastic Composite market by enhancing design, manufacturing, and operational efficiencies. Common user questions often explore how AI contributes to optimizing material selection, predicting performance under various loads, and streamlining complex manufacturing processes. AI algorithms are increasingly employed in generative design, allowing for the rapid exploration of novel composite structures that maximize strength while minimizing weight. Furthermore, the application of machine learning in quality control and defect detection during production is a significant area of interest, promising to reduce waste and improve the reliability of composite components, directly addressing concerns about manufacturing precision and consistency.

Beyond design and manufacturing, AI's impact extends into the lifecycle management of thermoplastic composite components. Users are keen to understand how AI-powered predictive maintenance can monitor structural health, forecast potential failures, and optimize maintenance schedules, thereby extending the operational lifespan of aircraft and defense systems. The analysis of vast datasets generated during flight or mission operations, enabled by AI, provides invaluable insights into material degradation and performance characteristics under real-world conditions. This data-driven approach allows for continuous improvement in composite design and maintenance protocols. The ability of AI to simulate complex scenarios and optimize material lay-up for specific performance requirements is also enhancing the competitive edge of manufacturers, ensuring that future composite applications are both high-performing and cost-effective.

- Optimization of composite design and material selection through generative AI, reducing design cycles.

- Enhancement of manufacturing processes via AI-driven robotics and automated quality inspection, minimizing defects.

- Predictive maintenance and structural health monitoring using AI algorithms for extended component lifespan.

- Improved supply chain management and material inventory optimization through AI-powered forecasting.

- Advanced simulation and modeling for performance prediction and failure analysis of composite structures.

- Accelerated R&D by analyzing vast datasets to discover new material combinations and processing techniques.

Key Takeaways Aerospace and Defense Thermoplastic Composite Market Size & Forecast

Analyzing common user questions about the Aerospace and Defense Thermoplastic Composite market size and forecast reveals a strong emphasis on future growth prospects, the primary drivers for this expansion, and the factors that might restrain it. Users are keenly interested in understanding which application areas, such as commercial aviation or military, will exhibit the most significant growth, and how technological advancements will shape market trajectories. The shift towards lightweighting for fuel efficiency, coupled with the inherent benefits of thermoplastic composites like high strength-to-weight ratio and recyclability, are consistently highlighted as pivotal growth enablers. The market's resilience in the face of economic fluctuations and its long-term potential in emerging aerospace applications are also frequent subjects of inquiry, indicating a forward-looking perspective among stakeholders.

Another crucial area of inquiry for market stakeholders revolves around identifying the most impactful technological breakthroughs and the competitive landscape. There is significant interest in understanding how new manufacturing techniques, such as additive manufacturing for composites, or novel material formulations will influence market shares and open new revenue streams. Questions also frequently address the regional growth dynamics, with a particular focus on the expanding aerospace manufacturing capabilities in Asia Pacific and the continued innovation in North America and Europe. The forecast underscores a robust expansion, driven by continuous innovation in material science and an increasing global fleet demand, positioning thermoplastic composites as indispensable materials for the future of aerospace and defense.

- Significant market growth driven by demand for lightweight, high-performance materials in aviation.

- Commercial aircraft segment anticipated to be a major revenue contributor due to fleet modernization and expansion.

- Military and space applications are showing robust growth due to advanced defense programs and space exploration initiatives.

- Technological advancements in manufacturing processes, such as AFP/ATL, are crucial for market scalability.

- North America and Europe currently dominate, but Asia Pacific is emerging as a high-growth region.

- The market is poised for sustained expansion, emphasizing material innovation and application diversification.

Aerospace and Defense Thermoplastic Composite Market Drivers Analysis

The aerospace and defense thermoplastic composite market is significantly propelled by the global imperative for enhanced fuel efficiency and reduced operational costs in both commercial and military aircraft. As fuel prices remain a volatile factor and environmental regulations become stricter, the demand for lightweight materials capable of lowering an aircraft's overall weight is intensifying. Thermoplastic composites offer a superior strength-to-weight ratio compared to traditional metallic alloys, directly contributing to substantial fuel savings and a reduced carbon footprint, making them an attractive alternative for new aircraft programs and retrofit initiatives. This inherent benefit drives widespread adoption across various structural and interior components.

Furthermore, the increasing production rates for new generation aircraft, particularly in the commercial sector, alongside robust investments in defense modernization programs globally, are key market accelerators. Major aircraft manufacturers are integrating thermoplastic composites into their designs to meet stringent performance requirements, including higher impact resistance, fatigue strength, and damage tolerance. The ease of processing, repairability, and recyclability of thermoplastic composites also contribute to their appeal, offering manufacturing efficiencies and lifecycle cost benefits over thermoset counterparts. This comprehensive set of advantages positions them as a critical enabler for the aerospace and defense sectors' future growth and innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Materials for Fuel Efficiency | +2.5% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Rise in Aircraft Production and Fleet Modernization | +2.0% | Global, with emphasis on Commercial Aviation hubs | 2025-2033 |

| Advancements in Composite Manufacturing Technologies (e.g., AFP, ATL) | +1.8% | North America, Europe, China | 2025-2030 |

| Enhanced Performance Characteristics (e.g., Durability, Damage Tolerance) | +1.5% | Global, especially for critical structural applications | 2025-2033 |

| Focus on Sustainability and Recyclability of Materials | +1.2% | Europe, North America | 2028-2033 |

Aerospace and Defense Thermoplastic Composite Market Restraints Analysis

Despite the numerous advantages, the Aerospace and Defense Thermoplastic Composite market faces significant restraints, primarily revolving around the high cost associated with raw materials and complex manufacturing processes. The specialized nature of high-performance thermoplastic resins like PEEK and PEKK, coupled with the intricate production techniques such as Automated Fiber Placement (AFP) or Automated Tape Laying (ATL), results in higher upfront costs compared to traditional metallic alloys or even thermoset composites. This elevated cost can be a substantial barrier, particularly for budget-sensitive defense programs or smaller aircraft manufacturers, limiting wider adoption and market penetration, especially for non-critical components where cost-efficiency is paramount.

Another prominent restraint is the limited availability of skilled labor and the significant capital investment required for establishing or upgrading manufacturing facilities capable of processing thermoplastic composites. The specialized expertise needed for design, manufacturing, and repair of these advanced materials is not readily available, leading to training challenges and higher labor costs. Furthermore, the standardization of testing methods and certification processes for thermoplastic composites in critical aerospace applications is still evolving. The stringent regulatory requirements and the time-consuming qualification processes for new materials in aerospace can delay market entry and widespread commercialization, posing a challenge for manufacturers seeking faster integration into existing supply chains. These factors collectively contribute to a cautious approach by some industry players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Raw Material and Processing Costs | -2.0% | Global | 2025-2033 |

| Complex Manufacturing and Processing Techniques | -1.5% | Global | 2025-2030 |

| Limited Skilled Workforce and High Capital Investment | -1.0% | Global, particularly developing regions | 2025-2033 |

| Stringent Certification and Qualification Processes | -0.8% | North America, Europe | 2025-2030 |

Aerospace and Defense Thermoplastic Composite Market Opportunities Analysis

The Aerospace and Defense Thermoplastic Composite market is poised for significant growth through emerging opportunities in urban air mobility (UAM), advanced air mobility (AAM), and drone applications. As these nascent industries evolve, there is an inherent demand for materials that offer extreme lightweighting, structural integrity, and efficient manufacturing at scale. Thermoplastic composites, with their superior mechanical properties and ability to be rapidly processed and recycled, are ideally suited to meet the unique design and performance requirements of electric vertical takeoff and landing (eVTOL) aircraft, autonomous drones, and other next-generation aerial vehicles. This expansion into new air vehicle segments represents a substantial greenfield market for composite manufacturers.

Furthermore, the increasing focus on sustainable manufacturing practices and the circular economy within the aerospace industry presents a compelling opportunity for thermoplastic composites. Unlike thermosets, thermoplastics can be melted and reformed, making them inherently recyclable and reducing waste during production and at end-of-life. This environmental advantage aligns with global sustainability goals and offers a competitive edge in a market increasingly prioritizing eco-friendly solutions. Opportunities also exist in developing multi-functional composites that integrate sensors, heating elements, or electromagnetic shielding, moving beyond purely structural applications. These innovations will open up new revenue streams and enhance the value proposition of thermoplastic composites, driving their adoption in high-value, integrated aerospace systems and broadening their market reach beyond traditional applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Urban Air Mobility (UAM) and Drone Applications | +2.8% | North America, Europe, Asia Pacific (e.g., China, South Korea) | 2028-2033 |

| Increasing Demand for Sustainable and Recyclable Materials | +2.2% | Europe, North America | 2025-2033 |

| Development of Multi-functional Composites and Smart Structures | +1.9% | Global, particularly advanced R&D hubs | 2027-2033 |

| Expansion into Space Exploration and Satellite Applications | +1.5% | North America, Europe, China, India | 2026-2033 |

Aerospace and Defense Thermoplastic Composite Market Challenges Impact Analysis

The Aerospace and Defense Thermoplastic Composite market faces significant challenges related to the relatively high processing temperatures and pressures required for some thermoplastic resins. This necessitates specialized equipment and energy-intensive manufacturing processes, which can escalate production costs and limit the size or complexity of components that can be efficiently produced. The high viscosity of thermoplastic melts also poses difficulties in fiber impregnation, potentially leading to void formation or incomplete consolidation, which can compromise the structural integrity of the final composite part. Overcoming these technical hurdles requires continuous innovation in processing technologies and material formulations, adding to research and development expenses and extending product development cycles.

Another substantial challenge is the existing infrastructure and established supply chains for traditional thermoset composites and metallic structures. The aerospace industry has heavily invested in manufacturing capabilities, tooling, and repair networks optimized for these conventional materials. Transitioning to thermoplastic composites requires significant retooling, new capital expenditures, and retraining of the workforce, which can be a slow and costly process for manufacturers. Furthermore, the long qualification and certification cycles for new materials in aerospace applications present a considerable barrier. Proving the long-term durability and performance of thermoplastic composites under extreme aerospace conditions requires extensive testing and validation, often delaying their widespread adoption and limiting market penetration, particularly for primary structural applications where risk aversion is highest.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Processing Temperatures and Pressures | -1.8% | Global | 2025-2030 |

| Lack of Standardization in Manufacturing and Testing | -1.3% | Global | 2025-2030 |

| Resistance to Change from Established Material Supply Chains | -1.0% | North America, Europe | 2025-2033 |

| Limited Repair and Maintenance Capabilities for Thermoplastics | -0.7% | Global | 2025-2030 |

Aerospace and Defense Thermoplastic Composite Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Aerospace and Defense Thermoplastic Composite Market, offering detailed insights into market size, growth trends, drivers, restraints, opportunities, and challenges across various segments and regions. It covers the market landscape from historical data to future projections, including the impact of emerging technologies like AI and sustainability initiatives. The scope encompasses detailed segmentation by fiber type, resin type, product type, application, and manufacturing process, providing a granular view of market dynamics and competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 900 Million |

| Growth Rate | 9.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Composite Systems, Global Aerospace Materials, AeroTech Composites, Precision Structures Inc., Innova Composites, NextGen Materials, Spectrum Aerospace, UniSource Composites, Composite Dynamics, Apex AeroSolutions, Quantum Composites, Stellar Aerospace Materials, Matrix Composites, Delta AeroStructures, Vertex Advanced Materials, Elite Aerospace Solutions, Horizon Composite Group, Prime Structural Systems, Orion Advanced Materials, Zenith Composites Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aerospace and Defense Thermoplastic Composite market is extensively segmented to provide a detailed understanding of its various facets, enabling stakeholders to identify key growth areas and niche opportunities. These segmentations are crucial for analyzing material adoption patterns, technological preferences, and application-specific demands across the global aerospace and defense landscape. The market's behavior varies significantly depending on the type of fiber, resin, and the specific manufacturing process employed, each offering distinct advantages in terms of performance, cost, and suitability for different components.

Further analysis by product type, encompassing prepregs, laminates, and finished components, reveals the preferred forms in which these materials are utilized by manufacturers. Application-based segmentation, ranging from commercial and military aircraft to burgeoning space and drone sectors, provides insights into the primary consumption hubs and future growth trajectories. Understanding these intricate segmentations is vital for strategic planning, product development, and market entry strategies within this highly specialized and evolving industry.

- By Fiber Type: Carbon Fiber, Glass Fiber, Aramid Fiber, Others (e.g., Basalt, Ceramic)

- By Resin Type: PEEK (Polyether Ether Ketone), PEKK (Polyetherketoneketone), PPS (Polyphenylene Sulfide), PA (Polyamide), PEI (Polyetherimide), Others (e.g., LCP, PSU)

- By Product Type: Prepreg, Laminates, Components (comprising parts and fully integrated structures)

- By Application: Commercial Aircraft (including structural components, interiors, secondary structures, control surfaces, and non-structural parts), Military Aircraft (fighters, transports, helicopters, unmanned military drones), Space (launch vehicles, satellites, re-entry vehicles, space stations), Drones (commercial drones, recreational drones, specialized industrial drones), Others (e.g., missiles, rockets, ground vehicles)

- By Manufacturing Process: Automated Fiber Placement (AFP), Automated Tape Laying (ATL), Compression Molding, Injection Molding, Extrusion, Others (e.g., Thermoforming, Welding, Additive Manufacturing)

Regional Highlights

- North America: Dominates the market due to the presence of major aircraft manufacturers, robust defense spending, and significant R&D investments in advanced materials. The U.S. remains a key contributor with ongoing commercial aircraft programs and military modernization initiatives.

- Europe: A strong market player driven by major aerospace original equipment manufacturers (OEMs), stringent environmental regulations fostering lightweight material adoption, and government support for composite research. Countries like France, Germany, and the UK are prominent.

- Asia Pacific (APAC): Emerging as the fastest-growing region due to increasing air passenger traffic, expanding commercial aircraft fleets, rising defense budgets in countries like China and India, and growing manufacturing capabilities. Significant investments in new airport infrastructure and domestic aircraft production further fuel growth.

- Latin America: Expected to show moderate growth, primarily driven by fleet expansion and modernization efforts in commercial aviation. However, limited domestic manufacturing capabilities for advanced composites may constrain rapid expansion.

- Middle East and Africa (MEA): Growing at a slower pace but with potential opportunities stemming from increasing air travel, airline fleet expansions, and strategic defense investments. The region is increasingly focusing on diversifying its industrial base, including aerospace manufacturing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aerospace and Defense Thermoplastic Composite Market.- Advanced Composite Systems

- Global Aerospace Materials

- AeroTech Composites

- Precision Structures Inc.

- Innova Composites

- NextGen Materials

- Spectrum Aerospace

- UniSource Composites

- Composite Dynamics

- Apex AeroSolutions

- Quantum Composites

- Stellar Aerospace Materials

- Matrix Composites

- Delta AeroStructures

- Vertex Advanced Materials

- Elite Aerospace Solutions

- Horizon Composite Group

- Prime Structural Systems

- Orion Advanced Materials

- Zenith Composites Group

Frequently Asked Questions

What are thermoplastic composites and why are they important for aerospace and defense?

Thermoplastic composites are high-performance materials made from fibers (like carbon or glass) embedded in a thermoplastic polymer matrix (like PEEK or PPS). They are crucial for aerospace and defense due to their superior strength-to-weight ratio, exceptional damage tolerance, resistance to chemicals, and ability to be re-formed and recycled. These properties contribute to lighter, more fuel-efficient aircraft and more durable defense systems.

How do thermoplastic composites contribute to aircraft fuel efficiency?

Thermoplastic composites significantly contribute to aircraft fuel efficiency by enabling substantial weight reduction. Lighter aircraft require less fuel to operate, leading to lower operating costs and reduced carbon emissions. Their high strength allows for thinner, yet stronger, structural components, further optimizing the design for minimal weight while maintaining safety and performance.

What are the key manufacturing processes used for aerospace thermoplastic composites?

Key manufacturing processes for aerospace thermoplastic composites include Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) for complex, large structures, Compression Molding for high-volume parts, and Injection Molding for intricate small components. These processes leverage the melt-processability of thermoplastics, often allowing for faster cycle times and automation.

What are the primary applications of thermoplastic composites in military aircraft?

In military aircraft, thermoplastic composites are primarily used in high-performance fighters, transport aircraft, and helicopters for structural components like wing skins, fuselage sections, control surfaces, and internal frames. Their high impact resistance and fatigue strength make them ideal for demanding combat environments and critical load-bearing structures.

What challenges does the adoption of thermoplastic composites face in the aerospace industry?

The adoption of thermoplastic composites faces challenges such as high raw material and processing costs, the need for specialized manufacturing equipment and skilled labor, and rigorous, time-consuming certification processes. Additionally, developing standardized repair techniques and establishing robust supply chains pose ongoing hurdles for widespread integration.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted