Commercial Vehicle Telematics Solution Market

Commercial Vehicle Telematics Solution Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678270 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

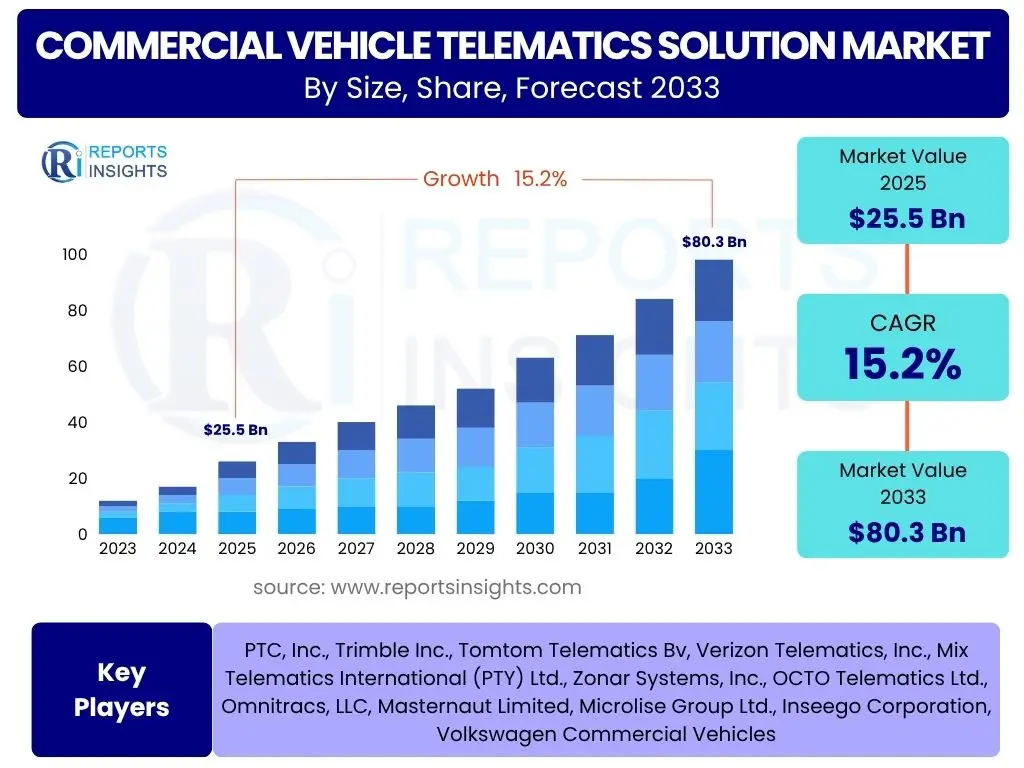

Commercial Vehicle Telematics Solution Market is projected to grow at a Compound annual growth rate (CAGR) of 15.2% between 2025 and 2033, reaching USD 25.5 billion in 2025 and is projected to grow to USD 80.3 billion by 2033 the end of the forecast period.

Key Commercial Vehicle Telematics Solution Market Trends & Insights

The commercial vehicle telematics solution market is undergoing significant transformation, driven by a confluence of technological advancements and evolving operational demands within the logistics and transportation sectors. Key trends shaping this dynamic landscape include the widespread adoption of IoT devices for enhanced connectivity, the integration of advanced analytics for predictive insights, and a growing emphasis on sustainability. These developments are enabling fleet operators to achieve unprecedented levels of efficiency, safety, and regulatory compliance, thereby redefining industry best practices.

- Increased adoption of IoT and advanced sensor integration

- Rising demand for predictive maintenance and real-time diagnostics

- Growing focus on driver behavior monitoring and safety enhancements

- Expansion of fleet electrification and charging infrastructure management

- Development of advanced routing and optimization algorithms

- Integration with enterprise resource planning (ERP) systems

- Emphasis on data security and privacy compliance

- Surge in demand for last-mile delivery optimization

AI Impact Analysis on Commercial Vehicle Telematics Solution

Artificial intelligence (AI) is poised to revolutionize the commercial vehicle telematics solution market by transforming raw data into actionable intelligence, thereby enabling smarter decision-making and autonomous operations. AI-powered algorithms are enhancing predictive capabilities, optimizing complex logistical processes, and improving safety standards across various fleet operations. This transformative influence extends to every aspect of telematics, from real-time asset tracking to sophisticated risk assessment, marking a paradigm shift in how commercial fleets are managed and operated.

- Enabling highly accurate predictive maintenance for vehicle longevity

- Optimizing complex route planning with dynamic traffic and weather analysis

- Automating driver behavior analysis for safety improvements and training

- Facilitating the development of autonomous and semi-autonomous commercial vehicles

- Enhancing fuel efficiency through intelligent driving recommendations

- Improving freight matching and load optimization for logistics providers

- Automating regulatory compliance checks and reporting

- Providing advanced risk assessment for insurance telematics

Key Takeaways Commercial Vehicle Telematics Solution Market Size & Forecast

- The global commercial vehicle telematics solution market is projected to reach USD 80.3 billion by 2033.

- The market is expanding at a robust CAGR of 15.2% from 2025 to 2033, indicating strong growth potential.

- Increasing demand for operational efficiency and fuel management is a primary growth driver.

- Regulatory mandates for vehicle safety and emissions contribute significantly to market expansion.

- Technological advancements in IoT, AI, and cloud computing are accelerating market development.

- North America and Europe currently dominate the market, driven by established infrastructure and early adoption.

- Asia Pacific is expected to witness the highest growth, fueled by rapid industrialization and logistics expansion.

- Key opportunities lie in integrating telematics with electric vehicles and developing advanced predictive analytics.

- Challenges include high initial investment costs and concerns regarding data security and privacy.

Commercial Vehicle Telematics Solution Market Drivers Impact Analysis

The commercial vehicle telematics solution market is propelled by a multitude of factors, each contributing to its sustained growth and broader adoption across various industries. A significant driver is the increasing global emphasis on operational efficiency and cost reduction within logistics and transportation sectors. Businesses are actively seeking solutions that can provide real-time insights into fleet performance, optimize routes, and manage fuel consumption more effectively. This pursuit of greater productivity directly fuels the demand for advanced telematics systems that offer comprehensive data analytics and management capabilities. Moreover, stringent regulatory frameworks related to driver safety, working hours, and environmental emissions are compelling fleet operators to integrate telematics solutions for compliance and risk mitigation.

Beyond efficiency and compliance, the inherent benefits of enhanced safety and security for both drivers and assets play a crucial role. Telematics systems offer features like emergency assistance, geo-fencing, and vehicle diagnostics, which significantly improve fleet safety profiles and reduce accident rates. The rapid advancements in connectivity technologies, such as 5G and IoT, are also making telematics solutions more robust and accessible, enabling seamless data flow and real-time monitoring. Furthermore, the expansion of the e-commerce sector and the burgeoning demand for efficient last-mile delivery services are creating a fertile ground for telematics adoption, as these systems are indispensable for optimizing complex delivery networks and meeting tight schedules. These multifaceted drivers collectively underscore the essential role of telematics in modern commercial vehicle operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Operational Efficiency and Cost Reduction | +3.5% | Global, particularly North America, Europe, Asia Pacific | Short to Long Term |

| Stringent Regulatory Mandates and Compliance Requirements | +2.8% | North America (ELD), Europe (Tachograph), Global Emissions Standards | Short to Medium Term |

| Growing Focus on Vehicle and Driver Safety | +2.3% | Global, especially developed economies | Medium to Long Term |

| Advancements in IoT, AI, and Cloud Technologies | +3.0% | Global, particularly tech-forward regions | Short to Long Term |

| Expansion of E-commerce and Logistics Industry | +2.5% | Asia Pacific, North America, Europe (Urban areas) | Short to Medium Term |

| Rising Fuel Costs and Need for Fuel Efficiency | +1.5% | Global | Short Term |

| Increase in Vehicle Theft and Need for Asset Tracking | +0.8% | Developing economies, high-value cargo routes | Short to Medium Term |

Commercial Vehicle Telematics Solution Market Restraints Impact Analysis

Despite the robust growth prospects, the commercial vehicle telematics solution market faces several significant restraints that could potentially impede its full expansion. One of the primary barriers is the high initial investment required for adopting comprehensive telematics systems. For small and medium-sized enterprises (SMEs), the upfront costs associated with hardware, software licenses, installation, and integration can be prohibitive, especially when combined with ongoing subscription fees for data services. This financial burden often delays or deters adoption, particularly in cost-sensitive markets. Furthermore, the complexity of integrating telematics solutions with existing fleet management systems and diverse vehicle types can present significant technical challenges, requiring specialized expertise and considerable downtime, which many operators are reluctant to incur.

Another critical restraint is the pervasive concern regarding data privacy and security. Telematics systems collect vast amounts of sensitive data, including location, driving behavior, and operational metrics, raising fears among fleet owners and drivers about potential misuse, unauthorized access, or cyber-attacks. The absence of universal data protection standards and the evolving regulatory landscape surrounding data privacy further exacerbate these concerns, making some potential adopters hesitant. Additionally, resistance from drivers and certain segments of the workforce, who may view telematics as an intrusive monitoring tool rather than a safety or efficiency aid, also poses a significant adoption hurdle. Overcoming these restraints requires a concerted effort to demonstrate clear return on investment, ensure robust data security measures, and foster a culture of transparency and trust around telematics implementation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Ongoing Costs | -2.0% | Global, particularly SMEs in developing regions | Short to Medium Term |

| Concerns Regarding Data Privacy and Security | -1.5% | Global, especially Europe (GDPR) and North America | Short to Long Term |

| Complexity of Integration with Existing Systems | -1.2% | Global, particularly older fleets and diverse operations | Short to Medium Term |

| Lack of Standardization and Interoperability Issues | -0.8% | Global | Medium Term |

| Resistance to Adoption from Drivers and Employees | -0.5% | Global, particularly in traditional transport sectors | Short to Medium Term |

Commercial Vehicle Telematics Solution Market Opportunities Impact Analysis

The commercial vehicle telematics solution market is brimming with promising opportunities that are set to drive its future expansion and innovation. A significant avenue for growth lies in the accelerating global shift towards electric vehicles (EVs) within commercial fleets. As businesses adopt EVs to meet sustainability goals and reduce operating costs, telematics solutions specifically designed to manage battery health, charging infrastructure, and optimized routing for electric fleets will become indispensable. This emerging segment presents a substantial market for specialized telematics services that can address the unique challenges and requirements of EV operations. Furthermore, the continuous evolution of 5G networks and vehicle-to-everything (V2X) communication technologies offers a robust platform for more advanced and real-time telematics applications, enabling enhanced safety features, autonomous driving capabilities, and truly connected fleet ecosystems.

Another compelling opportunity arises from the increasing demand for advanced data analytics and predictive insights. Beyond basic tracking, fleet operators are keen to leverage telematics data for predictive maintenance, fraud detection, and precise supply chain optimization. Solutions that can transform raw data into actionable intelligence, such as AI-powered forecasting and risk assessment tools, will command premium value. The expansion into emerging markets, particularly in Asia Pacific and Latin America, also presents vast untapped potential. As these regions experience rapid industrialization, urbanization, and growth in logistics infrastructure, the demand for efficient and compliant fleet management solutions will surge. Tailored solutions that address the specific needs and regulatory environments of these markets will be key to unlocking significant market share. Moreover, the integration of telematics with broader smart city initiatives and intelligent transportation systems opens up collaborative opportunities for public-private partnerships, further broadening the scope and impact of these solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Electric Vehicles (EVs) and Charging Infrastructure | +3.0% | Global, particularly Europe, North America, China | Medium to Long Term |

| Development of 5G and V2X Communication Technologies | +2.5% | Global, especially developed economies | Medium to Long Term |

| Increasing Demand for Advanced Analytics and Predictive Maintenance | +2.0% | Global, particularly large fleets and logistics companies | Short to Medium Term |

| Expansion into Emerging Markets (Asia Pacific, Latin America) | +1.8% | Asia Pacific (India, China), Latin America (Brazil, Mexico) | Medium to Long Term |

| Growth of Usage-Based Insurance (UBI) and Pay-As-You-Drive Models | +1.0% | North America, Europe | Short to Medium Term |

| Rise of Autonomous and Semi-Autonomous Commercial Vehicles | +1.5% | North America, Europe (testing grounds) | Long Term |

Commercial Vehicle Telematics Solution Market Challenges Impact Analysis

The commercial vehicle telematics solution market, while promising, is not without its share of significant challenges that stakeholders must navigate for successful growth and widespread adoption. One of the primary hurdles is the complex issue of interoperability. The market features a wide array of telematics hardware, software platforms, and data formats from numerous providers, leading to a lack of standardization. This fragmentation makes it difficult for fleet operators to integrate different systems seamlessly or switch providers without incurring substantial costs and operational disruptions. Ensuring that various telematics components can communicate effectively with different vehicle types and existing IT infrastructures remains a persistent technical challenge, hindering broader market penetration and user satisfaction.

Another critical challenge stems from the rapid pace of technological change within the industry. While innovation drives opportunities, it also creates an environment where telematics solutions can quickly become obsolete, requiring continuous updates and investments from fleet operators. Keeping pace with these advancements, particularly for smaller businesses with limited IT resources, can be overwhelming. Furthermore, there is a notable shortage of skilled professionals who possess the expertise to install, maintain, and effectively utilize advanced telematics systems. This talent gap impacts everything from initial deployment to data analysis and strategic decision-making, potentially limiting the full benefits derived from these sophisticated solutions. Addressing these challenges will require collaborative efforts among industry players to foster standardization, develop more user-friendly and future-proof solutions, and invest in training and workforce development programs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization and Interoperability Issues | -1.8% | Global | Medium to Long Term |

| Rapid Technological Advancements Leading to Obsolescence | -1.5% | Global, particularly for early adopters | Short to Medium Term |

| Shortage of Skilled Workforce for Installation and Data Analysis | -1.0% | Global, especially developing regions | Medium Term |

| Regulatory Complexities and Varying Compliance Landscapes | -0.7% | Global, varies by region/country | Short to Medium Term |

| Economic Downturns and Budgetary Constraints | -0.5% | Global, cyclical economic impact | Short Term |

Commercial Vehicle Telematics Solution Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Commercial Vehicle Telematics Solution Market, offering valuable insights into its current size, future growth projections, key trends, and competitive landscape. It serves as an essential resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and formulate strategic business decisions within this rapidly evolving industry. The report encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, along with detailed segmentation analysis across various parameters and regional perspectives.

| Report Attributes | Report Details |

|---|---|

| Report Name | Commercial Vehicle Telematics Solution Market |

| Market Size in 2025 | USD 25.5 billion |

| Market Forecast in 2033 | USD 80.3 billion |

| Growth Rate | CAGR of 2025 to 2033 15.2% |

| Number of Pages | 250 |

| Key Companies Covered | PTC, Inc., Trimble Inc., Tomtom Telematics Bv, Verizon Telematics, Inc., Mix Telematics International (PTY) Ltd., Zonar Systems, Inc., OCTO Telematics Ltd., Omnitracs, LLC, Masternaut Limited, Microlise Group Ltd., Inseego Corporation, Volkswagen Commercial Vehicles |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:- Fleet Tracking and Monitoring

- Driver Management

- Insurance Telematics

- Safety and Compliance

- V2X Solutions

- Others

- Transportation and Logistics

- Media and Entertainment

- Government and Utilities

- Travel and Tourism

- Construction

- Healthcare

- Education

Regional Highlights

The global commercial vehicle telematics solution market exhibits varied growth trajectories across different geographical regions, each influenced by unique regulatory landscapes, technological adoption rates, and economic development. Understanding these regional dynamics is crucial for stakeholders to identify key growth pockets and tailor their market strategies effectively. Leading regions typically showcase robust infrastructure, a strong regulatory push for fleet efficiency and safety, and a higher propensity for technological adoption.

North America is a dominant force in the commercial vehicle telematics market, primarily driven by stringent regulatory mandates such as the Electronic Logging Device (ELD) mandate, which has significantly boosted the adoption of telematics solutions for compliance. The region also benefits from a technologically advanced infrastructure, early adoption of IoT and cloud technologies, and a large logistics and transportation sector constantly seeking efficiency improvements. The presence of major telematics solution providers and a high demand for fleet optimization across various industries further solidify North America's leading position. This established market continues to innovate, especially in areas like predictive analytics, autonomous vehicle integration, and comprehensive fleet management platforms, leveraging its mature technological ecosystem and competitive market landscape.

Europe also holds a significant share in the market, propelled by its strong focus on road safety, environmental regulations, and intelligent transport systems initiatives. Countries like Germany, the UK, and France are at the forefront of telematics adoption due to well-established logistics networks and a supportive regulatory environment, including digital tachograph requirements. The region emphasizes green logistics and the integration of telematics with electric vehicle fleets, reflecting its commitment to sustainability. European market growth is further fueled by the need for cross-border fleet management solutions and the increasing adoption of telematics in various end-use industries beyond traditional logistics, such as construction and utilities, driven by a desire for enhanced operational visibility and compliance across a diverse range of commercial vehicle operations.

Asia Pacific is projected to be the fastest-growing market for commercial vehicle telematics solutions during the forecast period. This rapid growth is attributed to the burgeoning e-commerce sector, increasing industrialization, and significant investments in infrastructure development across countries like China, India, Japan, and Australia. While the adoption rate was historically lower, governments in these regions are increasingly promoting smart city initiatives and intelligent transportation systems, creating a conducive environment for telematics penetration. The expanding logistics and transportation industry, coupled with the rising awareness among fleet operators about the benefits of telematics in terms of cost savings, fuel efficiency, and asset management, are key factors driving this acceleration. The market in Asia Pacific is also witnessing increased localized product development and competitive pricing, making telematics more accessible to a wider range of businesses, from large logistics providers to small and medium-sized enterprises eager to modernize their fleets and improve operational efficiency to meet growing regional demands.

- North America: Leading the market due to stringent regulatory mandates (e.g., ELD mandate), advanced technological infrastructure, high adoption rates in logistics, and a strong emphasis on fleet safety and efficiency. Countries like the United States and Canada are key contributors.

- Europe: A significant market driven by strong road safety regulations, digital tachograph requirements, and a focus on environmental sustainability. Countries such as Germany, the UK, France, and Spain are vital, showcasing mature telematics adoption across diverse industries.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by rapid economic development, increasing e-commerce penetration, growing logistics and transportation sectors, and rising awareness of telematics benefits in emerging economies like China, India, and Australia.

- Latin America: Experiencing steady growth as fleet operators seek to improve security, reduce operational costs, and enhance vehicle tracking capabilities in countries like Brazil and Mexico. Regulatory push for cargo security also plays a role.

- Middle East and Africa (MEA): Showing nascent but promising growth, driven by increasing infrastructure projects, demand for efficient fleet management in oil and gas sectors, and a growing recognition of telematics' role in logistics and supply chain optimization, particularly in Gulf Cooperation Council (GCC) countries and South Africa.

Top Key Players:

The market research report covers the analysis of key stake holders of the Commercial Vehicle Telematics Solution Market. Some of the leading players profiled in the report include -:- PTC, Inc.

- Trimble Inc.

- Tomtom Telematics Bv

- Verizon Telematics, Inc.

- Mix Telematics International (PTY) Ltd.

- Zonar Systems, Inc.

- OCTO Telematics Ltd.

- Omnitracs, LLC

- Masternaut Limited

- Microlise Group Ltd.

- Inseego Corporation

- Volkswagen Commercial Vehicles

Frequently Asked Questions:

What is commercial vehicle telematics?

Commercial vehicle telematics refers to the integrated use of telecommunications and informatics to send, receive, and store information related to commercial vehicles and their operations. It typically involves GPS technology, onboard diagnostics (OBD), and communication systems to provide real-time data on vehicle location, performance, driver behavior, and safety, enhancing overall fleet management.

Why is commercial vehicle telematics important for businesses?

Commercial vehicle telematics is crucial for businesses as it significantly improves operational efficiency, reduces costs, and enhances safety. It enables real-time tracking, optimizes routing for fuel savings, facilitates predictive maintenance to minimize downtime, ensures regulatory compliance, and provides valuable insights into driver performance, leading to a more productive, secure, and profitable fleet.

What are the primary benefits of implementing telematics in a commercial fleet?

The primary benefits of implementing telematics include significant improvements in fuel efficiency through optimized routes and reduced idling, enhanced driver safety via behavior monitoring and alerts, better vehicle maintenance scheduling reducing breakdowns, improved asset utilization and security with real-time tracking, and simplified compliance with industry regulations. It also offers comprehensive data for strategic decision-making.

How does AI impact the commercial vehicle telematics market?

AI profoundly impacts the commercial vehicle telematics market by transforming raw data into actionable intelligence. It enables advanced predictive maintenance, optimizing vehicle uptime; facilitates dynamic route optimization considering real-time variables; enhances driver behavior analysis for safety improvements; and supports the development of autonomous vehicle capabilities. AI-driven insights lead to smarter, more efficient, and safer fleet operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted