Commercial Internal Combustion Engine Market

Commercial Internal Combustion Engine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702339 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

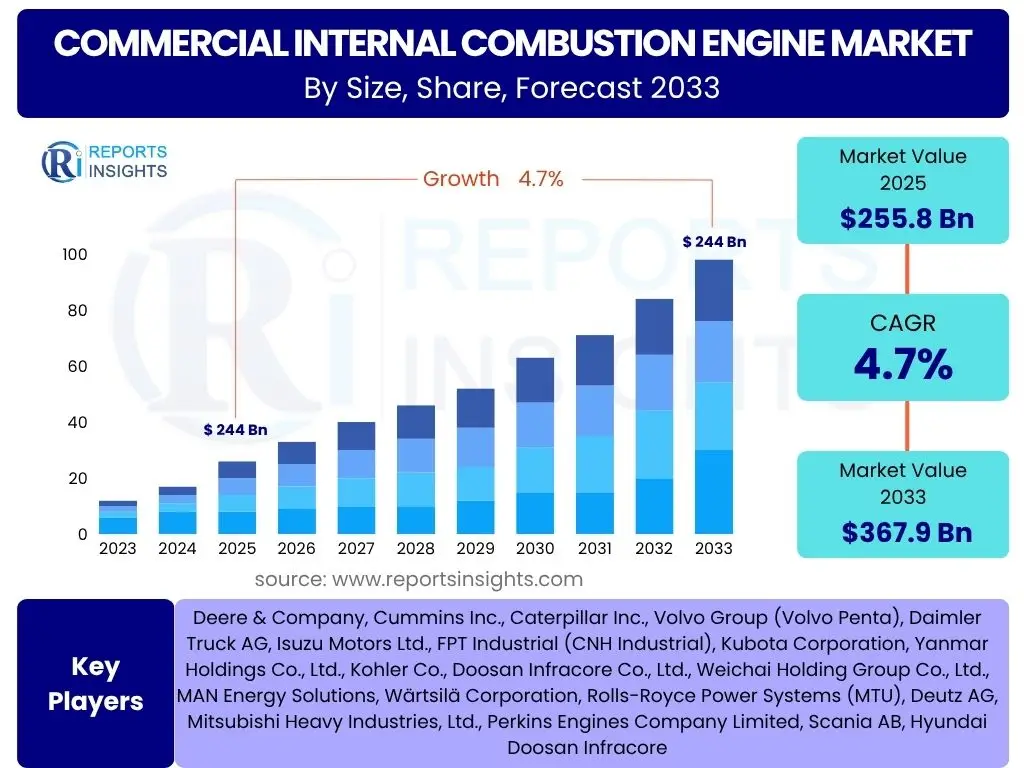

Commercial Internal Combustion Engine Market Size

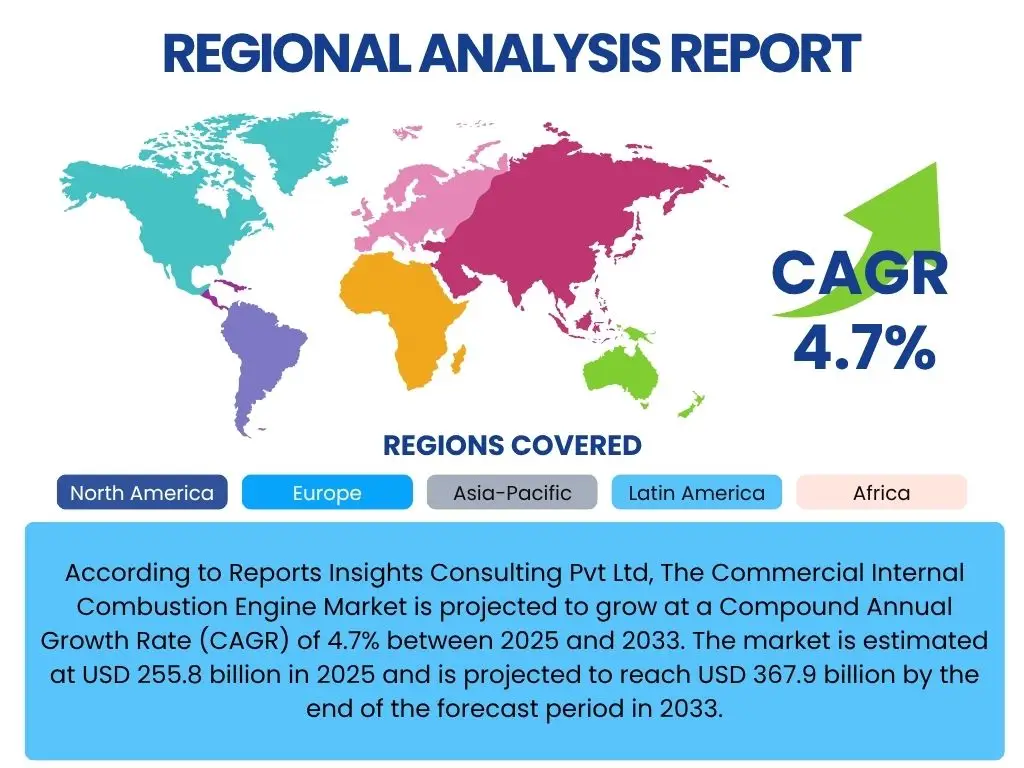

According to Reports Insights Consulting Pvt Ltd, The Commercial Internal Combustion Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.7% between 2025 and 2033. The market is estimated at USD 255.8 billion in 2025 and is projected to reach USD 367.9 billion by the end of the forecast period in 2033.

Key Commercial Internal Combustion Engine Market Trends & Insights

The Commercial Internal Combustion Engine (ICE) market is undergoing significant transformation driven by evolving regulatory landscapes, technological advancements, and shifting operational demands across various industries. Common user inquiries often revolve around the sustainability of ICE technology in an era of electrification, the adoption of alternative fuels, and the integration of digital solutions to enhance performance and efficiency. Market participants are keen to understand how traditional ICE technology will adapt to meet stringent emission standards while maintaining the reliability and power output essential for commercial applications.

A notable trend is the continuous emphasis on improving fuel efficiency and reducing emissions, leading to innovations in engine design, combustion processes, and exhaust after-treatment systems. There is also a growing interest in hybridizing ICEs with electric powertrains to offer a bridge solution between conventional and fully electric propulsion, particularly in heavy-duty and long-haul applications where range and payload are critical. Furthermore, the digitalization of commercial fleets is driving demand for intelligent engine management systems capable of real-time diagnostics, predictive maintenance, and optimized operational parameters.

The market is witnessing a diversification of fuel options, with increasing exploration and adoption of natural gas, propane, and even hydrogen as viable alternatives to traditional diesel and gasoline. This shift is primarily influenced by the desire for lower operational costs, reduced carbon footprint, and compliance with environmental regulations. Additionally, the robustness and established infrastructure for ICEs continue to make them indispensable for sectors such as construction, agriculture, marine, and power generation, where high power density and extended operational hours are paramount, supporting their sustained relevance despite the rise of electric alternatives.

- Advanced Fuel Efficiency Technologies: Development of more efficient combustion systems, turbocharging, and lightweight materials.

- Emissions Reduction Systems: Integration of selective catalytic reduction (SCR), diesel particulate filters (DPF), and exhaust gas recirculation (EGR).

- Hybridization and Electrification: Pairing ICEs with electric motors for improved performance, fuel economy, and lower emissions in specific commercial vehicle segments.

- Alternative Fuel Adoption: Increasing use of compressed natural gas (CNG), liquefied natural gas (LNG), propane, and hydrogen as fuel sources.

- Digital Integration and Telematics: Implementation of IoT sensors, telematics, and data analytics for predictive maintenance, fleet management, and performance optimization.

- Modular Engine Designs: Focus on flexible and scalable engine architectures to meet diverse application requirements.

- Aftermarket and Servicing Growth: Emphasis on robust support and maintenance networks to extend engine lifespan and operational efficiency.

AI Impact Analysis on Commercial Internal Combustion Engine

The integration of Artificial Intelligence (AI) into the commercial internal combustion engine sector is a topic of significant user interest, particularly concerning its potential to revolutionize engine performance, maintenance, and operational efficiency. Common questions focus on how AI can contribute to predictive analytics for engine health, optimize fuel consumption, and enhance the overall reliability of commercial vehicle fleets. Users are keen to understand if AI can prolong the relevance of ICE technology in the face of environmental pressures and electrification trends by making them smarter and more efficient.

AI's impact extends beyond mere data collection to intelligent data analysis, enabling sophisticated engine management. It facilitates the development of algorithms that can learn from operational data to predict component failures, optimize fuel injection timing, and adjust engine parameters in real-time for peak performance under varying conditions. This capability minimizes downtime, reduces maintenance costs, and significantly improves fuel economy, directly addressing key concerns for commercial operators regarding total cost of ownership and operational continuity.

Furthermore, AI plays a crucial role in the design and development phases of new engines, employing machine learning to simulate and optimize combustion processes, material selection, and structural integrity, leading to more robust and efficient designs. In the aftermarket, AI-powered diagnostic tools can quickly pinpoint issues, reducing repair times and ensuring that commercial ICEs remain highly productive assets. This broad application of AI supports the continued viability and competitiveness of internal combustion engines by making them "smarter" and more adaptive to diverse operational demands.

- Predictive Maintenance: AI algorithms analyze sensor data to forecast potential component failures, enabling proactive maintenance and reducing unscheduled downtime.

- Fuel Efficiency Optimization: AI systems dynamically adjust engine parameters (e.g., fuel injection, ignition timing) in real-time based on operational conditions, load, and environment, leading to significant fuel savings.

- Performance Optimization: AI-driven engine control units (ECUs) can optimize power output, torque delivery, and emissions control by continuously learning from operational data.

- Design and Development: AI and machine learning accelerate the design process, simulate engine performance under various conditions, and optimize component geometries for efficiency and durability.

- Automated Diagnostics: AI-powered diagnostic tools can quickly identify complex engine issues, improving troubleshooting accuracy and reducing repair times.

- Supply Chain and Logistics Optimization: AI enhances inventory management for engine parts and optimizes service schedules across large fleets.

- Driver Assistance and Training: AI provides real-time feedback to drivers on optimal driving behaviors for fuel efficiency and reduced engine wear.

Key Takeaways Commercial Internal Combustion Engine Market Size & Forecast

Common user questions regarding the key takeaways from the Commercial Internal Combustion Engine market size and forecast often focus on the market's resilience and its ability to adapt amidst the global push for decarbonization. Stakeholders are particularly interested in understanding the factors that will sustain growth, the segments offering the most promising opportunities, and the influence of regulatory pressures on future market trajectory. There's a strong emphasis on identifying where traditional ICE technology will retain its competitive edge and how innovation will drive its evolution over the forecast period.

A primary takeaway is that despite the increasing focus on electric vehicles, the commercial ICE market demonstrates robust growth, primarily due to its indispensable role in heavy-duty applications, long-haul logistics, and off-highway sectors like construction and agriculture where battery-electric solutions currently face practical limitations regarding range, payload, and charging infrastructure. The market's growth is largely underpinned by the ongoing demand for efficient and powerful engines that can operate reliably in diverse and demanding environments globally. Continuous innovation in fuel efficiency, alternative fuel compatibility, and emissions reduction technologies is crucial for maintaining this momentum.

Furthermore, the market's future growth is not solely dependent on new vehicle sales but also on the extensive existing fleet requiring maintenance, upgrades, and component replacements. Opportunities arise from retrofitting older engines with modern emission control systems, the development of engines compatible with renewable and synthetic fuels, and the integration of advanced digital technologies for enhanced operational intelligence. The sustained demand from emerging economies, coupled with strategic investments in cleaner ICE technologies by established manufacturers, solidifies a positive outlook for the market, highlighting its adaptability and enduring significance across various commercial applications.

- Sustained Demand in Heavy-Duty Sectors: Commercial ICEs remain critical for long-haul transport, construction, agriculture, and marine industries due to power, range, and operational demands.

- Innovation-Driven Resilience: Continuous investment in cleaner fuels, higher efficiency, and advanced emissions control technologies is enabling market adaptation.

- Hybridization as a Bridge Technology: The integration of ICEs with electric powertrains offers a pragmatic solution for many commercial applications, balancing performance with environmental goals.

- Market Value Growth: Despite pressures, the market is projected for significant value growth, indicating ongoing investment and development in this sector.

- Emerging Market Contribution: Developing economies will significantly contribute to market expansion due to infrastructure development and increasing commercial activity.

- Focus on Total Cost of Ownership: Operators prioritize fuel efficiency, durability, and reduced maintenance, driving manufacturers to innovate in these areas.

Commercial Internal Combustion Engine Market Drivers Analysis

The commercial internal combustion engine market is propelled by several fundamental drivers that underscore its continued relevance despite the global shift towards electrification. These drivers are rooted in economic expansion, infrastructure development, and the inherent operational advantages that ICEs offer in demanding commercial applications. The robust demand for goods transportation, construction, and agricultural output globally necessitates power solutions that are reliable, high-performing, and adaptable to various operational environments, which ICEs are uniquely positioned to provide.

Furthermore, the ongoing industrialization and urbanization in emerging economies worldwide significantly contribute to the market's growth. As these regions expand their manufacturing capabilities, develop extensive infrastructure, and increase agricultural productivity, the demand for commercial vehicles and heavy equipment powered by internal combustion engines escalates. This sustained demand, coupled with the existing widespread fueling infrastructure and the maturity of ICE technology, solidifies its position as a preferred power source for a vast array of commercial and industrial applications, including those requiring sustained high power and long operational hours.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Economic Growth & Trade Expansion | +1.5% | Asia Pacific, North America, Europe | Short to Mid-Term (2025-2029) |

| Infrastructure Development & Construction Boom | +1.2% | Asia Pacific (China, India), Latin America, MEA | Mid to Long-Term (2027-2033) |

| Increased Demand for Logistics & Freight Transport | +1.0% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-Term (2025-2029) |

| Growth in Agriculture & Mining Sectors | +0.8% | Latin America, Africa, Australia, parts of North America | Mid to Long-Term (2027-2033) |

| Technological Advancements in Engine Efficiency & Emissions | +0.7% | Global, particularly developed regions | Continuous (2025-2033) |

Commercial Internal Combustion Engine Market Restraints Analysis

Despite robust drivers, the commercial internal combustion engine market faces significant restraints, primarily stemming from the global push towards environmental sustainability and the emergence of alternative propulsion technologies. Stringent emission regulations imposed by governments worldwide are forcing manufacturers to invest heavily in research and development for cleaner engines, often leading to increased production costs that can impact market competitiveness. This regulatory pressure is a major hurdle, requiring continuous innovation and significant capital expenditure to comply with evolving standards.

Furthermore, the rising adoption and technological maturity of electric and fuel cell vehicles present a substantial long-term threat to the dominance of commercial ICEs. While current electric solutions may not fully cater to all heavy-duty applications, ongoing advancements in battery technology, charging infrastructure, and fuel cell efficiency are steadily expanding their applicability. This growing competition necessitates that ICE manufacturers not only comply with regulations but also continue to demonstrate superior cost-effectiveness and operational advantages to retain market share.

Volatility in fuel prices, particularly for diesel and gasoline, also acts as a restraint. Unpredictable fuel costs can significantly impact the operational budgets of commercial fleets, pushing operators to explore more stable and potentially cheaper energy sources. This economic uncertainty, combined with public perception favoring greener technologies, creates a challenging environment for the sustained, unimpeded growth of the commercial internal combustion engine market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations & Environmental Policies | -1.8% | Europe, North America, China, India | Continuous (2025-2033) |

| Increasing Adoption of Electric & Fuel Cell Vehicles | -1.5% | Global, particularly developed economies | Mid to Long-Term (2027-2033) |

| Volatile Fuel Prices & Operational Costs | -0.9% | Global | Short to Mid-Term (2025-2029) |

| High Research & Development Costs for Compliance | -0.6% | Global | Continuous (2025-2033) |

| Limited Infrastructure for Alternative Fuels (e.g., Hydrogen) | -0.4% | Early adoption regions | Short to Mid-Term (2025-2029) |

Commercial Internal Combustion Engine Market Opportunities Analysis

The commercial internal combustion engine market presents several compelling opportunities for growth and innovation, particularly through adaptation to new environmental paradigms and leveraging technological advancements. A significant opportunity lies in the development and widespread adoption of engines capable of running on alternative and renewable fuels. As industries seek to reduce their carbon footprint, engines compatible with natural gas, biogas, synthetic fuels, and even hydrogen (in hydrogen ICE configurations) offer a viable pathway to cleaner operations without a complete overhaul of existing infrastructure or extensive fleet replacement, thus extending the lifespan and relevance of ICE technology.

Furthermore, the integration of advanced digital technologies, such as IoT, AI, and predictive analytics, offers substantial opportunities to enhance the operational efficiency and longevity of commercial ICEs. These technologies enable real-time monitoring, proactive maintenance, and optimized performance, translating into reduced downtime and lower operational costs for fleet operators. This digital transformation not only improves current engine performance but also opens avenues for new service models centered around data-driven insights and smart fleet management, creating value beyond the hardware itself.

Another key opportunity resides in addressing specific niche markets and applications where electrification remains challenging, such as heavy-duty off-highway equipment (construction, mining, agriculture), marine propulsion, and standby power generation. In these sectors, the high power density, reliability, and long operational hours provided by ICEs are difficult to match by current battery-electric or fuel cell technologies. Developing highly specialized, efficient, and low-emission ICEs for these segments allows manufacturers to capitalize on enduring demand, ensuring sustained growth and market leadership in these critical commercial areas.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Alternative & Renewable Fuels | +1.3% | Global, particularly Europe, North America, Asia Pacific | Mid to Long-Term (2027-2033) |

| Retrofit & Aftermarket Solutions for Emissions Compliance | +1.0% | Developed regions with large existing fleets | Short to Mid-Term (2025-2029) |

| Integration of Digital Technologies (IoT, AI) for Efficiency | +0.9% | Global | Continuous (2025-2033) |

| Growth in Emerging Markets for Commercial Vehicles & Equipment | +0.8% | Asia Pacific, Latin America, MEA | Short to Long-Term (2025-2033) |

| Specialization for Niche, High-Power Applications (e.g., Marine, Mining) | +0.6% | Global, specialized industrial hubs | Mid to Long-Term (2027-2033) |

Commercial Internal Combustion Engine Market Challenges Impact Analysis

The commercial internal combustion engine market faces several substantial challenges that demand continuous innovation and strategic adaptation from manufacturers. One of the foremost challenges is navigating the increasingly stringent global emission regulations. Governments worldwide are imposing stricter limits on pollutants like NOx, PM, and CO2, requiring significant investment in advanced after-treatment systems and fundamental engine redesigns. Meeting these evolving standards without compromising engine performance or significantly increasing costs is a complex balancing act that can slow market growth and increase time-to-market for new products.

Another critical challenge is the intense competition from emerging alternative propulsion technologies, particularly battery-electric and hydrogen fuel cell powertrains. While ICEs currently dominate many heavy-duty sectors, the rapid advancements in these cleaner alternatives, coupled with growing public and political support for zero-emission vehicles, present a formidable threat. Manufacturers must continually innovate to demonstrate the long-term viability and competitiveness of ICEs, either through hybridization or by achieving near-zero emissions with conventional fuels, to retain market share against these burgeoning technologies.

Furthermore, the high research and development costs associated with developing cleaner, more efficient, and digitally integrated commercial ICEs pose a significant hurdle. These costs, coupled with the need to attract and retain skilled engineering talent specializing in complex engine systems, can strain manufacturers' financial resources. Economic downturns or supply chain disruptions can exacerbate these challenges, impacting production schedules and profitability. Addressing these multifaceted challenges requires a strategic approach that balances innovation, cost-effectiveness, and responsiveness to market and regulatory demands.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving Global Emission Standards & Regulatory Compliance | -1.7% | Europe, North America, China | Continuous (2025-2033) |

| Intensifying Competition from Alternative Propulsion Technologies | -1.4% | Global, particularly developed economies | Mid to Long-Term (2027-2033) |

| High R&D Investment for Cleaner & More Efficient Engines | -0.8% | Global | Continuous (2025-2033) |

| Supply Chain Volatility & Raw Material Price Fluctuations | -0.5% | Global | Short to Mid-Term (2025-2029) |

| Public Perception & Investor Pressure for Decarbonization | -0.4% | Global, particularly developed regions | Mid to Long-Term (2027-2033) |

Commercial Internal Combustion Engine Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Commercial Internal Combustion Engine market, encompassing historical data, current trends, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view for stakeholders. It segments the market by various parameters, providing granular insights into demand patterns across different applications, fuel types, and power outputs. The report also highlights key regional dynamics and profiles major industry players to offer competitive intelligence and strategic recommendations for market entry and expansion.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 255.8 Billion |

| Market Forecast in 2033 | USD 367.9 Billion |

| Growth Rate | 4.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, Cummins Inc., Caterpillar Inc., Volvo Group (Volvo Penta), Daimler Truck AG, Isuzu Motors Ltd., FPT Industrial (CNH Industrial), Kubota Corporation, Yanmar Holdings Co., Ltd., Kohler Co., Doosan Infracore Co., Ltd., Weichai Holding Group Co., Ltd., MAN Energy Solutions, Wärtsilä Corporation, Rolls-Royce Power Systems (MTU), Deutz AG, Mitsubishi Heavy Industries, Ltd., Perkins Engines Company Limited, Scania AB, Hyundai Doosan Infracore |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Commercial Internal Combustion Engine market is extensively segmented to provide granular insights into its diverse applications and technological nuances. This segmentation allows for a detailed understanding of demand patterns, technological preferences, and regional variations across different industry verticals. The market is primarily categorized based on fuel type, power output, and a broad range of applications, reflecting the varied needs of commercial operations globally.

Further segmentation includes a detailed breakdown by key engine components, offering insights into the supply chain and manufacturing landscape, as well as by end-use industry, which illuminates the specific requirements and growth trajectories of sectors relying heavily on ICE technology. This multi-dimensional approach to segmentation is crucial for identifying emerging trends, competitive dynamics, and untapped opportunities within this complex market. Understanding these segments is vital for manufacturers to tailor their product offerings and for investors to identify high-growth areas.

- By Fuel Type:

- Diesel

- Gasoline

- Natural Gas (CNG, LNG)

- Others (Propane, Biogas, Hydrogen)

- By Power Output:

- Below 100 HP

- 100-300 HP

- 301-500 HP

- Above 500 HP

- By Application:

- Commercial Vehicles

- Light Commercial Vehicles

- Medium & Heavy Commercial Vehicles

- Construction Equipment

- Excavators

- Loaders

- Dozers

- Graders

- Agricultural Equipment

- Tractors

- Harvesters

- Marine Vessels

- Ferries

- Cargo Ships

- Workboats

- Power Generation

- Generators

- Backup Power

- Material Handling Equipment

- Other Industrial Applications

- Commercial Vehicles

- By Component:

- Engine Block

- Cylinder Heads

- Crankshafts

- Connecting Rods

- Pistons

- Fuel Injection Systems

- Turbochargers

- Valves

- Exhaust Systems

- Electronic Control Units (ECUs)

- By End-Use Industry:

- Transportation & Logistics

- Construction

- Agriculture

- Marine

- Mining

- Oil & Gas

- Power Generation

- Manufacturing

Regional Highlights

- North America: A mature market characterized by stringent emission standards and a strong emphasis on fuel efficiency. The region sees significant demand from the transportation and logistics sectors, as well as a robust agricultural and construction equipment market. Innovation in telematics and predictive maintenance is prominent.

- Europe: Leading the charge in emissions reduction and the adoption of alternative fuels. Europe exhibits a strong preference for highly efficient engines and is at the forefront of exploring hybrid and hydrogen-powered ICE solutions. Regulations like Euro VI are key drivers for technological advancements.

- Asia Pacific (APAC): The largest and fastest-growing market, driven by rapid industrialization, infrastructure development, and increasing commercial vehicle sales, particularly in China and India. While emissions standards are tightening, the sheer volume of demand and ongoing economic expansion fuel significant market expansion.

- Latin America: Characterized by growth in agricultural and mining sectors, leading to steady demand for robust commercial ICEs. Economic stability and infrastructure investments are key factors influencing market expansion, with a growing focus on cost-effective and durable solutions.

- Middle East and Africa (MEA): Emerging market with growing demand from construction, mining, and oil & gas sectors. Investments in infrastructure projects and economic diversification initiatives are driving the need for commercial ICEs, particularly those capable of operating in harsh environments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Internal Combustion Engine Market.- Deere & Company

- Cummins Inc.

- Caterpillar Inc.

- Volvo Group (Volvo Penta)

- Daimler Truck AG

- Isuzu Motors Ltd.

- FPT Industrial (CNH Industrial)

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Kohler Co.

- Doosan Infracore Co., Ltd.

- Weichai Holding Group Co., Ltd.

- MAN Energy Solutions

- Wärtsilä Corporation

- Rolls-Royce Power Systems (MTU)

- Deutz AG

- Mitsubishi Heavy Industries, Ltd.

- Perkins Engines Company Limited

- Scania AB

- Hyundai Doosan Infracore

Frequently Asked Questions

What is the projected growth rate of the Commercial Internal Combustion Engine Market?

The Commercial Internal Combustion Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.7% between 2025 and 2033.

What are the primary drivers for the Commercial Internal Combustion Engine Market?

Key drivers include global economic growth, extensive infrastructure development, increasing demand for logistics and freight transport, and growth in the agriculture and mining sectors. Technological advancements in engine efficiency also play a significant role.

How do emission regulations impact the Commercial Internal Combustion Engine Market?

Stringent emission regulations globally are a significant restraint, compelling manufacturers to invest heavily in R&D for cleaner engines and advanced after-treatment systems, often increasing production costs and driving innovation in sustainable engine solutions.

What opportunities exist for the Commercial Internal Combustion Engine Market?

Opportunities include the development and adoption of alternative fuels (like natural gas and hydrogen), integration of digital technologies for efficiency, and specialized engines for niche, high-power applications where electrification is less viable.

Which regions are key contributors to the Commercial Internal Combustion Engine Market?

Asia Pacific is the largest and fastest-growing region due to industrialization, while North America and Europe are mature markets focused on advanced technologies and emissions compliance. Latin America and MEA are emerging markets driven by infrastructure and resource development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted