Commercial Flour Market

Commercial Flour Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704138 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

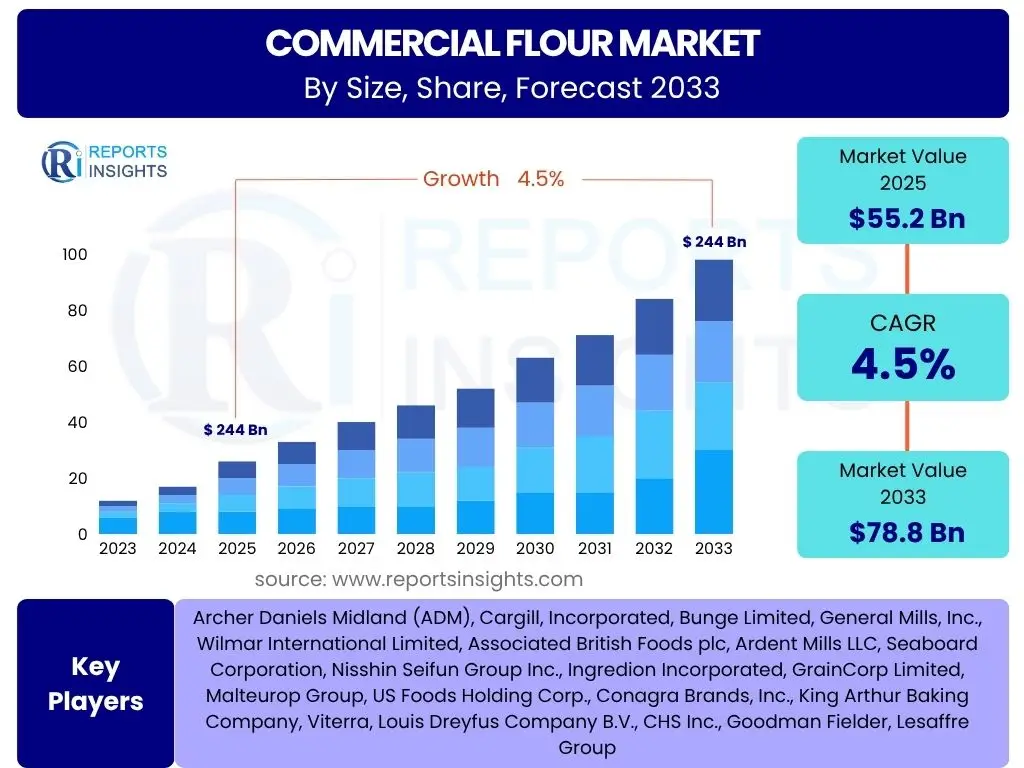

Commercial Flour Market Size

According to Reports Insights Consulting Pvt Ltd, The Commercial Flour Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 55.2 billion in 2025 and is projected to reach USD 78.8 billion by the end of the forecast period in 2033.

Key Commercial Flour Market Trends & Insights

User inquiries frequently center on understanding the evolving landscape of the commercial flour market, particularly concerning shifts in consumer preferences, technological advancements in milling, and the increasing demand for specialized flour types. The market is witnessing a significant pivot towards health-conscious alternatives, with a growing emphasis on gluten-free, organic, and fortified flours. Furthermore, advancements in food processing technologies are enabling the production of flours with enhanced functional properties, catering to diverse industrial applications. Supply chain resilience and sustainability are also emerging as critical strategic considerations for market players, driving innovations in sourcing and production methods.

The burgeoning global population coupled with increasing disposable incomes, particularly in emerging economies, is fueling the demand for baked goods and processed foods, directly impacting flour consumption. This trend is reinforced by the expansion of the food service sector and the proliferation of industrial bakeries. Additionally, rising awareness regarding nutritional benefits and dietary restrictions is prompting manufacturers to diversify their product portfolios, offering a wider array of specialty flours derived from various grains beyond traditional wheat, such as rice, corn, and ancient grains. The integration of advanced analytics and automation within milling operations is enhancing efficiency and product consistency, further shaping the market dynamics.

- Rising demand for specialty and functional flours (gluten-free, organic, fortified).

- Increased consumption of convenience foods and baked products globally.

- Technological advancements in milling and processing techniques.

- Growing focus on sustainable sourcing and production practices.

- Expansion of the food service and industrial bakery sectors.

AI Impact Analysis on Commercial Flour

Common user questions regarding AI's impact on the commercial flour market frequently explore how artificial intelligence can optimize operational efficiencies, enhance product quality, and revolutionize supply chain management. AI is increasingly being recognized as a transformative force, capable of providing predictive insights for demand forecasting, thereby reducing waste and improving inventory management. Its application extends to quality control, where AI-driven vision systems can meticulously inspect grain batches and finished flour for defects, ensuring consistency and adherence to stringent quality standards. This precision minimizes human error and significantly boosts production reliability.

Beyond quality control and demand prediction, AI offers profound capabilities in optimizing milling processes. Machine learning algorithms can analyze vast datasets from production lines to fine-tune machinery settings, leading to improved yield, reduced energy consumption, and more consistent flour characteristics. Furthermore, AI can aid in the development of new flour blends by simulating ingredient interactions and predicting their functional properties, accelerating product innovation. The integration of AI in agricultural practices, from soil analysis to crop monitoring, also indirectly impacts the commercial flour market by ensuring a more stable and high-quality supply of raw materials, addressing concerns related to climate volatility and resource management.

- Enhanced demand forecasting and supply chain optimization through predictive analytics.

- Automated quality control and inspection for raw grains and finished flour products.

- Optimization of milling processes for improved efficiency, yield, and energy consumption.

- Facilitation of new product development through AI-driven formulation and simulation.

- Improved agricultural practices impacting raw material quality and supply stability.

Key Takeaways Commercial Flour Market Size & Forecast

User queries regarding key takeaways from the Commercial Flour Market size and forecast highlight the desire for concise insights into the market's trajectory, primary growth drivers, and segments offering the most potential. The market is positioned for steady expansion, driven by foundational consumer demand for bakery products and processed foods, alongside an accelerating shift towards diversified and specialty flour types. The projected growth indicates resilience within the sector, underpinned by global population increases and evolving dietary patterns that prioritize specific nutritional profiles or functional attributes in food ingredients.

A significant takeaway is the strong contribution of the bakery and confectionery sectors to the overall market growth, reflecting sustained consumer preferences for these staple and indulgent items. Furthermore, the rising awareness of health and wellness is creating distinct sub-markets for flours catering to dietary restrictions, such as gluten-free options, or those offering enhanced nutritional value through fortification. This diversification not only broadens the market scope but also presents new revenue streams for manufacturers. Geographically, Asia Pacific is anticipated to be a key growth engine, leveraging its large population base and expanding food processing industry, while North America and Europe will continue to be significant revenue contributors due to established consumption patterns and innovation in specialty flour products.

- The market is projected to grow steadily at a CAGR of 4.5% from 2025 to 2033, reaching USD 78.8 billion.

- Strong demand from bakery, confectionery, and processed food industries underpins market expansion.

- Growing consumer preference for specialty, organic, and gluten-free flours is a significant growth driver.

- Technological advancements in milling and processing enhance product quality and market competitiveness.

- Asia Pacific is expected to exhibit robust growth, while established markets maintain significant shares.

Commercial Flour Market Drivers Analysis

The commercial flour market is primarily driven by the consistent and expanding global demand for staple food products, especially baked goods and processed foods. Population growth, particularly in developing regions, directly correlates with an increased need for basic food ingredients like flour. Additionally, urbanization and changing dietary habits, which include a higher consumption of convenience foods and out-of-home dining, significantly contribute to the market's expansion. Manufacturers are also innovating to meet diverse consumer preferences, introducing new flour types and blends that cater to health trends and specific culinary requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Population Growth | +1.5% | Global, particularly Asia Pacific, Africa | Long-term (2025-2033) |

| Rising Demand for Baked Goods & Processed Foods | +1.2% | Global, especially North America, Europe, Asia Pacific | Mid-term to Long-term |

| Increasing Disposable Income | +0.8% | Emerging Economies (China, India, Brazil) | Mid-term |

| Innovation in Specialty & Fortified Flours | +0.7% | North America, Europe, Developed Asia Pacific | Short-term to Mid-term |

Commercial Flour Market Restraints Analysis

Despite robust growth drivers, the commercial flour market faces several restraints that could impede its expansion. Volatility in raw material prices, primarily grains like wheat, rice, and corn, poses a significant challenge, impacting production costs and profit margins for flour manufacturers. Climate change and unpredictable weather patterns can lead to crop failures or reduced yields, further exacerbating price instability and supply chain disruptions. Additionally, stringent food safety regulations and quality standards in various regions require substantial investment in compliance, potentially increasing operational complexities and costs for market players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.0% | Global | Short-term to Mid-term |

| Stringent Food Safety Regulations | -0.6% | North America, Europe | Ongoing |

| Health Concerns (e.g., Gluten Intolerance) | -0.5% | North America, Europe, Oceania | Long-term |

| Supply Chain Disruptions & Logistics Challenges | -0.4% | Global | Short-term |

Commercial Flour Market Opportunities Analysis

Significant opportunities exist within the commercial flour market for companies willing to innovate and adapt to evolving consumer landscapes. The burgeoning demand for gluten-free, organic, and other specialty flours presents a lucrative avenue for product diversification and market penetration. As consumers become more health-conscious and seek specific dietary benefits, manufacturers can capitalize on this trend by offering a wider range of alternative grain flours or fortified options. Furthermore, the expansion into developing economies with their rapidly growing populations and increasing urbanization offers substantial untapped market potential for established and emerging players. Technological advancements in milling can also enhance efficiency and open doors for new product developments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Specialty & Gluten-Free Flour Market | +1.3% | North America, Europe, Developed Asia Pacific | Mid-term to Long-term |

| Expansion in Emerging Economies | +1.1% | Asia Pacific, Latin America, Africa | Long-term |

| Technological Advancements in Milling & Processing | +0.9% | Global | Ongoing |

| Increasing Application in Fortified Food Products | +0.7% | Global, especially regions with nutritional deficiencies | Mid-term |

Commercial Flour Market Challenges Impact Analysis

The commercial flour market encounters several challenges that necessitate strategic planning and adaptive measures from industry participants. Intense competition among a large number of local and international players often leads to price wars, exerting pressure on profit margins. The susceptibility of grain harvests to climate change, including droughts, floods, and extreme temperatures, poses a significant threat to raw material supply stability and quality, leading to supply chain uncertainties. Furthermore, shifting consumer preferences, especially towards alternative diets or reduced carbohydrate intake, require continuous market monitoring and product innovation to remain relevant and competitive. Logistics and transportation complexities, particularly in geographically diverse markets, also present ongoing operational hurdles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition | -0.8% | Global | Ongoing |

| Impact of Climate Change on Crop Yields | -0.7% | Global, particularly major grain-producing regions | Long-term |

| Changing Consumer Dietary Preferences | -0.5% | North America, Europe | Long-term |

| Logistics and Transportation Costs | -0.4% | Global | Short-term to Mid-term |

Commercial Flour Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global commercial flour market, offering an in-depth analysis of its current state and future growth trajectory. It provides a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033. The scope includes a meticulous segmentation analysis by flour type, application, and region, along with competitive landscape profiling of key industry players, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 78.8 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Archer Daniels Midland (ADM), Cargill, Incorporated, Bunge Limited, General Mills, Inc., Wilmar International Limited, Associated British Foods plc, Ardent Mills LLC, Seaboard Corporation, Nisshin Seifun Group Inc., Ingredion Incorporated, GrainCorp Limited, Malteurop Group, US Foods Holding Corp., Conagra Brands, Inc., King Arthur Baking Company, Viterra, Louis Dreyfus Company B.V., CHS Inc., Goodman Fielder, Lesaffre Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The commercial flour market is intricately segmented to reflect the diverse applications and types of flour demanded across various industries and consumer groups. Understanding these segmentations is crucial for identifying specific market niches, strategic investment opportunities, and tailoring product development initiatives. The market's complexity is defined by factors such as the grain source, its intended end-use, the processing method, and consumer preferences for attributes like organic or gluten-free. This granular analysis provides a clear roadmap for stakeholders aiming to optimize their market positioning and maximize revenue generation within the evolving food landscape.

The primary segmentation revolves around flour type, encompassing a broad spectrum from conventional wheat flour, which remains dominant, to a growing array of specialty and alternative flours derived from rice, corn, rye, oats, and ancient grains. Application-wise, the market is heavily influenced by the bakery and confectionery industries, but also extends to noodles, pasta, animal feed, and other processed foods. Furthermore, the end-use segmentation differentiates between industrial food manufacturers, food service establishments, and retail consumers, each with distinct volume and quality requirements. The increasing consumer inclination towards healthier options has also led to a significant distinction between conventional and organic flour categories, highlighting a premiumization trend within the market.

- By Type: Wheat Flour (All-Purpose, Bread, Cake, Pastry, Self-Rising), Rice Flour, Corn Flour, Rye Flour, Barley Flour, Oat Flour, Ancient Grain Flours (Quinoa, Spelt, Amaranth, Sorghum), Legume Flours (Chickpea, Lentil), Other Specialty Flours

- By Application: Bakery Products (Breads, Cakes, Pastries, Biscuits, Cookies), Noodles & Pasta, Confectionery, Animal Feed, Breakfast Cereals, Soups & Sauces, Other Food Processing

- By End-Use: Food Service (Restaurants, Cafes, Bakeries), Industrial (Food & Beverage Manufacturers), Retail/Household

- By Nature: Organic, Conventional

- By Form: Powder, Granular

Regional Highlights

- North America: A mature market characterized by high consumption of processed foods and a strong demand for specialty flours, including organic and gluten-free varieties. Innovation in bakery and convenience food products is a key driver.

- Europe: Similar to North America, Europe shows strong demand for traditional and specialty flours. Strict food safety regulations and a growing emphasis on sustainable sourcing and healthier options influence market dynamics.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid urbanization, increasing disposable incomes, and the expanding food processing industry. Traditional flour consumption remains high, alongside a rising appetite for international baked goods and convenience foods. Countries like China, India, and Japan are significant contributors.

- Latin America: Experiences steady growth driven by population expansion and the increasing penetration of organized retail and food service sectors. The market is influenced by both traditional culinary uses and the adoption of Western dietary patterns.

- Middle East and Africa (MEA): Emerging markets with significant growth potential, fueled by population growth, urbanization, and changing lifestyles. Demand for both basic and value-added flour products is on the rise, particularly in countries with expanding food industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Flour Market.- Archer Daniels Midland (ADM)

- Cargill, Incorporated

- Bunge Limited

- General Mills, Inc.

- Wilmar International Limited

- Associated British Foods plc

- Ardent Mills LLC

- Seaboard Corporation

- Nisshin Seifun Group Inc.

- Ingredion Incorporated

- GrainCorp Limited

- Malteurop Group

- US Foods Holding Corp.

- Conagra Brands, Inc.

- King Arthur Baking Company

- Viterra

- Louis Dreyfus Company B.V.

- CHS Inc.

- Goodman Fielder

- Lesaffre Group

Frequently Asked Questions

What is the projected growth rate for the Commercial Flour Market?

The Commercial Flour Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, reaching an estimated USD 78.8 billion by the end of the forecast period.

What are the primary drivers influencing the Commercial Flour Market?

Key drivers include global population growth, rising demand for baked goods and processed foods, increasing disposable incomes in emerging economies, and continuous innovation in specialty and fortified flour products to meet diverse consumer preferences.

How is artificial intelligence impacting the Commercial Flour industry?

AI is significantly impacting the industry by enhancing demand forecasting and supply chain optimization, automating quality control for raw materials and finished products, optimizing milling processes for improved efficiency, and facilitating new product development through advanced formulation and simulation.

Which regions are key contributors to the Commercial Flour Market?

North America and Europe are significant contributors due to high consumption and innovation, while Asia Pacific is anticipated to be the fastest-growing region, driven by rapid urbanization and expanding food processing industries in countries like China and India.

What are the major segments within the Commercial Flour Market?

The market is primarily segmented by flour type (e.g., Wheat, Rice, Corn, Specialty Flours), application (e.g., Bakery Products, Noodles & Pasta, Confectionery), end-use (e.g., Food Service, Industrial, Retail), nature (Organic, Conventional), and form (Powder, Granular).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted