Combat System Integration Market

Combat System Integration Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708239 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

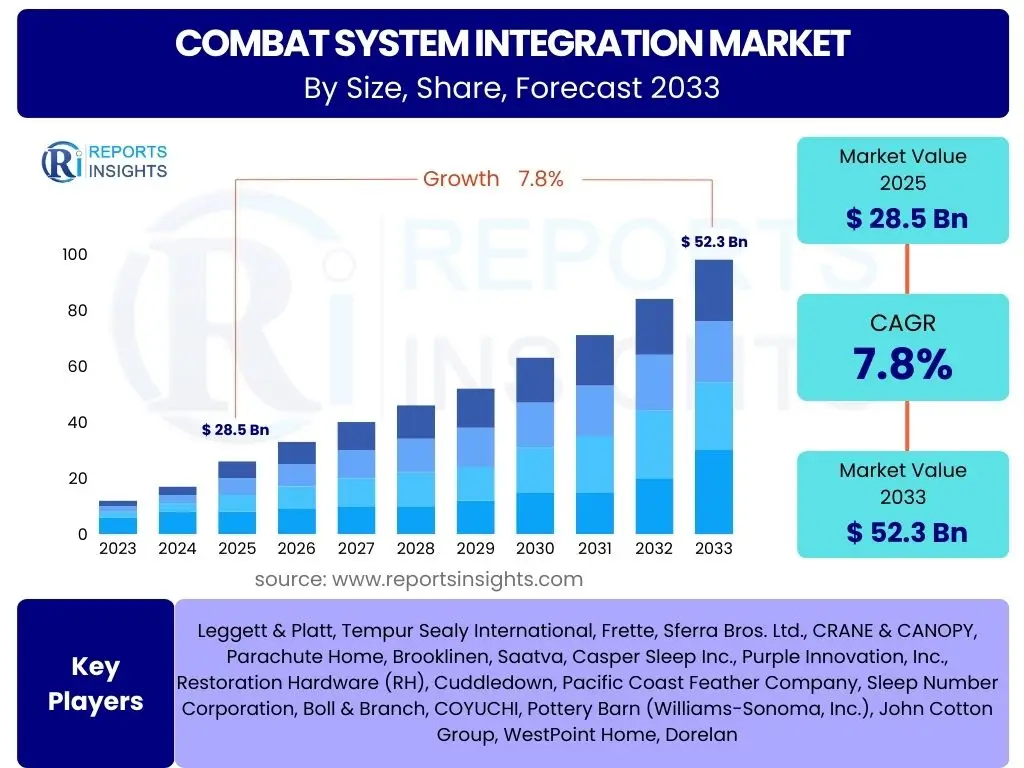

Combat System Integration Market Size

The Combat System Integration Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 52.3 Billion by the end of the forecast period in 2033. This robust growth is primarily driven by an escalating global defense expenditure, a persistent demand for advanced warfare capabilities, and the increasing complexity of modern threat landscapes requiring highly integrated and interoperable defense systems.

This expansion underscores a global shift towards network-centric warfare, where the effectiveness of military operations relies heavily on the seamless exchange of information and coordinated action across diverse platforms. Nations are investing significantly in upgrading their existing combat systems and acquiring new, more sophisticated ones that can communicate and operate cohesively. The market's trajectory also reflects a strategic emphasis on enhancing situational awareness, decision-making speed, and overall operational efficiency through comprehensive system integration across air, land, sea, and cyber domains.

Key Combat System Integration Market Trends & Insights

User inquiries regarding Combat System Integration market trends frequently highlight the shift towards digital warfare, the adoption of autonomous capabilities, and the need for resilient, multi-domain operations. There is significant interest in how modern militaries are adapting to hybrid threats and the role of advanced technologies in enhancing interoperability and tactical superiority. Concerns often revolve around the challenges of integrating disparate systems, cybersecurity vulnerabilities, and the rapid pace of technological evolution requiring constant upgrades.

Emerging trends indicate a strong focus on enhancing data fusion capabilities, leveraging artificial intelligence for predictive analytics and decision support, and the development of open-architecture systems to facilitate easier upgrades and integration. The market is also witnessing a surge in demand for modular and scalable solutions that can be adapted to various operational scenarios and platforms. Furthermore, the push for greater automation and remote-controlled systems is reshaping the future of combat operations, demanding more sophisticated integration frameworks.

- Multi-Domain Integration: Seamless connectivity and interoperability across air, land, sea, space, and cyber domains are becoming paramount for comprehensive situational awareness and synchronized response.

- Increased Adoption of Open Architectures: The shift towards open, modular system designs allows for easier integration of new technologies, faster upgrades, and reduced vendor lock-in, fostering greater flexibility and cost-effectiveness.

- Advanced Data Fusion and Analytics: Enhanced capabilities to aggregate, process, and analyze vast amounts of data from diverse sensors, providing commanders with superior real-time intelligence for decision-making.

- Focus on Cybersecurity in Integration: As systems become more interconnected, robust cybersecurity measures are integrated from the design phase to protect against sophisticated cyber threats and ensure system integrity.

- Proliferation of Autonomous and Unmanned Systems: Integration of autonomous platforms (UAVs, UUVs, UGVs) into broader combat networks, requiring advanced communication and control integration for coordinated operations.

- AI and Machine Learning for Enhanced Decision Support: AI algorithms are increasingly being used to process complex combat scenarios, offer predictive analysis, and provide commanders with optimized tactical recommendations.

- Miniaturization and Swarm Technologies: Development of smaller, interconnected systems and swarm capabilities that enhance survivability, reconnaissance, and offensive actions through distributed, coordinated operations.

AI Impact Analysis on Combat System Integration

Common user questions regarding AI's impact on Combat System Integration frequently center on its ability to enhance decision-making, automate complex tasks, and the ethical implications of autonomous weapon systems. Users are keen to understand how AI can improve the speed and accuracy of target recognition, threat assessment, and resource allocation in highly dynamic combat environments. There is also significant interest in AI's role in data overload management, predicting maintenance needs, and optimizing logistical operations, transforming the efficiency of integrated combat systems.

The integration of artificial intelligence is fundamentally transforming the landscape of combat systems by introducing unparalleled levels of automation, precision, and cognitive support. AI-powered systems are capable of processing vast quantities of sensor data in real-time, identifying patterns, and generating actionable intelligence far more rapidly than human operators alone. This capability significantly improves situational awareness and shortens the OODA (Observe, Orient, Decide, Act) loop, offering a critical advantage in modern warfare. Furthermore, AI contributes to predictive maintenance, optimizing the operational readiness of complex integrated platforms and reducing overall lifecycle costs.

- Enhanced Data Fusion and Situational Awareness: AI algorithms process and integrate disparate data streams from multiple sensors, providing a cohesive and comprehensive operational picture for commanders, significantly improving situational awareness.

- Accelerated Decision-Making: AI-powered decision support systems analyze complex combat scenarios and provide rapid, optimized recommendations, reducing the cognitive load on human operators and accelerating response times.

- Predictive Analytics for System Readiness: AI monitors the health and performance of integrated combat systems, predicting potential failures and enabling proactive maintenance, thereby maximizing operational uptime and reliability.

- Autonomous Operations and Swarm Intelligence: AI facilitates the control and coordination of autonomous unmanned systems, including swarm tactics, which enhances reconnaissance, target engagement, and force multiplication while minimizing human exposure to danger.

- Intelligent Threat Detection and Classification: Machine learning models improve the accuracy and speed of identifying and classifying threats, reducing false positives and allowing for more efficient resource allocation and defensive measures.

- Optimized Logistics and Supply Chain Management: AI algorithms can predict demand, optimize routes, and manage inventories for critical combat system components, ensuring timely supply and reducing operational bottlenecks.

- Adaptive Electronic Warfare (EW) and Cyber Defense: AI enhances the adaptability and responsiveness of electronic warfare systems and cyber defense mechanisms, allowing them to dynamically counter evolving threats and maintain secure communication channels within integrated systems.

Key Takeaways Combat System Integration Market Size & Forecast

User questions about key takeaways from the Combat System Integration market often focus on the primary growth drivers, the most promising geographic regions for investment, and the technological advancements set to define future market dynamics. There is a strong interest in understanding which segments, such as naval or aerial platforms, are expected to exhibit the most significant growth, and what are the overarching strategic implications for defense procurement and national security. Users also seek to identify the major challenges that could impede market progression and how these are being addressed by industry players.

The market is poised for substantial growth, driven by an urgent need for advanced defense capabilities in response to global geopolitical instabilities and the rapid evolution of modern warfare. Key insights reveal a robust demand for interoperable and multi-domain integrated systems, particularly within naval and aerial platforms. The focus on leveraging cutting-edge technologies like AI, advanced sensors, and secure communication networks is paramount to achieving tactical superiority. Furthermore, defense modernization initiatives across developed and emerging economies will be critical in sustaining this growth trajectory, emphasizing the market's strategic importance in global security landscapes.

- Significant Market Expansion: The Combat System Integration market is projected for strong growth, driven by increasing global defense budgets and the imperative for advanced, interconnected military capabilities.

- Technological Advancements as Core Drivers: Innovation in AI, machine learning, advanced sensor fusion, and secure communication technologies will continue to be central to market expansion and system effectiveness.

- Strategic Importance of Multi-Domain Operations: The push towards integrating capabilities across air, land, sea, cyber, and space domains is a key strategic priority, driving demand for comprehensive integration solutions.

- Defense Modernization Initiatives: Ongoing and planned modernization programs by major and emerging military powers are a primary catalyst for new system procurements and upgrades, fueling market growth.

- Rise of Open Architectures: The adoption of open-architecture standards is simplifying system upgrades, enhancing interoperability, and reducing total cost of ownership, making systems more adaptable to future threats.

- North America and Asia Pacific Lead Growth: These regions are expected to contribute significantly to market revenue, with North America driving R&D and advanced deployments, and Asia Pacific focusing on robust defense modernization.

- Persistent Cybersecurity Focus: As integration deepens, ensuring the cybersecurity of interconnected combat systems remains a critical concern and a significant investment area for national defense.

Combat System Integration Market Drivers Analysis

The Combat System Integration market is primarily driven by several critical factors reflecting the evolving global security landscape and technological advancements. A paramount driver is the escalating geopolitical tensions and regional conflicts worldwide, which compel nations to bolster their defense capabilities with more sophisticated and integrated systems. This environment necessitates robust command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) systems that can operate seamlessly across various domains.

Furthermore, the continuous modernization efforts by defense forces globally, particularly in developed and emerging economies, significantly contribute to market expansion. These initiatives focus on replacing aging legacy systems with advanced, network-centric platforms capable of real-time data exchange and collaborative operations. The increasing demand for interoperable defense systems that can facilitate joint operations among allied forces also plays a crucial role, emphasizing the importance of standardized integration frameworks and open architectures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Geopolitical Tensions & Conflicts: Heightened global instability drives increased defense spending and demand for advanced, integrated combat capabilities for deterrence and effective response. | +2.5% | Global, particularly Asia Pacific, Middle East, Europe | Short to Mid-term (2025-2029) |

| Modernization of Defense Forces: Nations are actively upgrading outdated military hardware and software with advanced, network-centric combat systems to enhance operational efficiency and superiority. | +2.0% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Demand for Multi-Domain Operations: The strategic imperative for forces to operate seamlessly across land, sea, air, cyber, and space domains necessitates robust integration solutions. | +1.8% | North America, Europe | Mid to Long-term (2026-2033) |

| Advancements in Network-Centric Warfare: Evolution of technologies enabling real-time information sharing and coordinated action across distributed military units enhances operational effectiveness and decision-making. | +1.5% | Global, particularly technologically advanced nations | Long-term (2027-2033) |

| Increased Focus on Cybersecurity: The growing sophistication of cyber threats mandates the integration of advanced cybersecurity measures within combat systems, driving investment in secure integration platforms. | +1.0% | Global | Short to Mid-term (2025-2029) |

Combat System Integration Market Restraints Analysis

Despite significant growth prospects, the Combat System Integration market faces several notable restraints that could impede its expansion. One primary restraint is the exceptionally high cost associated with the research, development, procurement, and deployment of advanced integrated combat systems. These systems often require substantial capital investment, extended development cycles, and considerable expenditure on maintenance and upgrades, posing a significant challenge for nations with limited defense budgets.

Another major restraint involves the stringent regulatory frameworks and complex certification processes inherent in the defense sector. These regulations, designed to ensure safety, reliability, and security, often lead to prolonged project timelines and increased costs. Furthermore, the inherent complexity of integrating legacy systems with new technologies, coupled with issues of interoperability between different vendors' products and national systems, creates significant technical and operational hurdles. Concerns over cybersecurity vulnerabilities in highly integrated networks also act as a constraint, demanding continuous investment in robust protective measures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Procurement Costs: The substantial financial outlay required for advanced combat system integration projects can deter nations with constrained defense budgets. | -1.5% | Global, particularly developing nations | Long-term (2025-2033) |

| Stringent Regulatory Frameworks & Certification: Strict national and international defense regulations impose complex compliance requirements, leading to longer development cycles and higher costs. | -1.2% | North America, Europe | Mid to Long-term (2026-2033) |

| Interoperability Challenges with Legacy Systems: Integrating diverse, older military platforms with new, advanced systems presents significant technical hurdles and compatibility issues. | -1.0% | Global, particularly countries with aging fleets | Short to Mid-term (2025-2029) |

| Cybersecurity Threats & Data Vulnerabilities: The increasing interconnectedness of combat systems creates larger attack surfaces, necessitating constant investment in robust cyber defenses to prevent breaches. | -0.8% | Global | Short to Mid-term (2025-2028) |

| Technological Obsolescence and Upgrade Cycles: The rapid pace of technological innovation means systems can become obsolete quickly, requiring continuous and costly upgrades to maintain effectiveness. | -0.7% | Global | Long-term (2027-2033) |

Combat System Integration Market Opportunities Analysis

The Combat System Integration market presents numerous opportunities for growth and innovation, driven by evolving technological landscapes and strategic defense priorities. A significant opportunity lies in the continued development and integration of emerging technologies such as quantum computing, advanced materials, and directed energy weapons, which promise to revolutionize warfare capabilities. Companies that can effectively integrate these cutting-edge innovations into existing and new combat systems will gain a substantial competitive advantage.

Furthermore, the increasing focus on public-private partnerships offers a fertile ground for collaboration, allowing defense contractors to leverage commercial technological advancements and share development costs and risks. Expanding defense budgets in emerging economies, particularly in Asia Pacific and the Middle East, also represent a considerable opportunity for market players seeking to penetrate new markets and offer tailored integration solutions. The growing emphasis on developing resilient and secure command and control systems, especially in light of increasing cyber threats, creates a sustained demand for advanced integration solutions that prioritize cybersecurity from the ground up.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced & Disruptive Technologies: Integration of technologies like quantum computing, hypersonics, and advanced sensor arrays into combat systems offers superior capabilities. | +1.7% | North America, Europe, Asia Pacific (China, India) | Mid to Long-term (2027-2033) |

| Increased Defense Spending in Emerging Economies: Growing defense budgets in countries across Asia Pacific and the Middle East create new markets for advanced combat system integration. | +1.5% | Asia Pacific, Middle East & Africa | Short to Mid-term (2025-2030) |

| Public-Private Partnerships (PPPs): Collaboration between government defense agencies and private industry fosters innovation, shares development risks, and accelerates technology adoption. | +1.3% | Global | Mid to Long-term (2026-2033) |

| Expansion into Space and Cyber Domains: The increasing militarization of space and the growing importance of cyber warfare create new frontiers for combat system integration and defense. | +1.1% | Global, particularly major space-faring nations | Long-term (2028-2033) |

| Retrofit & Upgrade Market for Existing Systems: Significant opportunities exist in modernizing and integrating new capabilities into existing defense platforms to extend their operational life and enhance effectiveness. | +0.9% | Global | Short to Mid-term (2025-2029) |

Combat System Integration Market Challenges Impact Analysis

The Combat System Integration market is not without its significant challenges, which necessitate innovative solutions and strategic planning from market participants. A critical challenge involves the inherent complexity of integrating disparate systems from various manufacturers and generations into a single, cohesive combat network. This often leads to compatibility issues, software conflicts, and extensive testing requirements, increasing project timelines and costs substantially.

Moreover, the global shortage of highly skilled professionals with expertise in defense electronics, software engineering, and systems integration poses a significant impediment to market growth. This talent gap can hinder the pace of development and deployment of advanced integrated systems. Additionally, the increasing sophistication of cyber threats demands continuous innovation in cybersecurity measures, adding another layer of complexity and cost to integration projects. Supply chain disruptions, often exacerbated by geopolitical events and reliance on specialized components, also present a considerable challenge to timely project delivery and cost control.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of System Interoperability: Achieving seamless communication and data exchange between diverse hardware and software components from multiple vendors and generations is a persistent technical hurdle. | -1.8% | Global | Long-term (2025-2033) |

| Shortage of Skilled Workforce: A global deficit of specialized engineers and technicians with expertise in defense electronics, software development, and systems integration slows innovation and deployment. | -1.5% | North America, Europe | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Disruptions: Reliance on complex global supply chains for specialized components makes projects susceptible to geopolitical events, material shortages, and logistical delays. | -1.3% | Global | Short to Mid-term (2025-2028) |

| Ethical & Legal Considerations of AI & Autonomy: Developing and deploying AI-driven autonomous combat systems raises significant ethical, legal, and regulatory questions that require careful navigation. | -1.0% | Global, particularly Western democracies | Mid to Long-term (2027-2033) |

| Budgetary Constraints & Prioritization: Despite increasing defense spending, national budgets remain finite, leading to difficult choices in prioritizing integration projects over other military procurements. | -0.9% | Global | Short to Mid-term (2025-2029) |

Combat System Integration Market - Updated Report Scope

This market research report provides an exhaustive analysis of the Combat System Integration market, covering market sizing, growth forecasts, key trends, and a detailed examination of market drivers, restraints, opportunities, and challenges. The scope encompasses a comprehensive review of technological advancements, the impact of AI, and regional market dynamics, offering strategic insights for stakeholders. The report aims to furnish a granular understanding of market segmentation by platform, application, component, and system type, along with profiles of leading industry players to provide a holistic view of the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 52.3 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems plc, Northrop Grumman Corporation, General Dynamics Corporation, Thales Group, L3Harris Technologies, Inc., Leonardo S.p.A., Saab AB, Rheinmetall AG, Hanwha Systems Co. Ltd., Israel Aerospace Industries (IAI), Indra Sistemas S.A., Elbit Systems Ltd., Bharat Electronics Limited (BEL), Damen Schelde Naval Shipbuilding, Naval Group, Huntington Ingalls Industries (HII), General Atomics, Boeing Defense, Space & Security |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

A thorough segmentation analysis of the Combat System Integration market is crucial for understanding its diverse dynamics and identifying key growth areas. The market is broadly categorized by platform, application, component, and system type, reflecting the varied requirements and technological complexities across different military domains. Each segment reveals specific trends and investment patterns, allowing for a more granular assessment of market opportunities and competitive landscapes. Understanding these distinctions is vital for stakeholders to tailor their strategies and product offerings effectively.

The segmentation highlights that while naval and aerial platforms traditionally dominate, the increasing proliferation of unmanned systems and the strategic importance of space and cyber domains are rapidly creating new sub-segments with significant growth potential. The shift towards software-defined capabilities and comprehensive services, rather than solely hardware, also indicates an evolution in market value propositions. This detailed breakdown enables market players to pinpoint high-growth niches, understand customer needs, and develop targeted solutions that address the specific integration challenges of each segment.

- By Platform

- Naval Vessels: Integration for surface combatants, submarines, and aircraft carriers, focusing on anti-submarine warfare, anti-surface warfare, and air defense systems.

- Aerial Platforms: Integration for fighter jets, bombers, surveillance aircraft, and helicopters, emphasizing avionics, weapon management, and electronic warfare suites.

- Land Platforms: Integration for tanks, armored vehicles, artillery systems, and infantry systems, including C4ISR, fire control, and active protection systems.

- Unmanned Systems: Integration for UAVs, UUVs, and UGVs, focusing on autonomous navigation, sensor payloads, and data link security.

- Space-Based Platforms: Integration for satellites and orbital assets, primarily for communication, surveillance, and navigation support to ground forces.

- By Application

- Command & Control (C2): Systems for strategic and tactical decision-making, including battle management and mission planning.

- Intelligence, Surveillance, & Reconnaissance (ISR): Integration of sensors and data analytics for real-time intelligence gathering and dissemination.

- Weapon Systems Integration: Connecting diverse weapon platforms with targeting and fire control systems.

- Electronic Warfare (EW): Integration of systems for electronic attack, support, and protection.

- Navigation & Targeting: Precision navigation and accurate targeting capabilities for various platforms.

- Communication Systems: Secure and reliable communication networks for inter-platform and intra-platform data exchange.

- Cyber Defense: Integration of cybersecurity measures to protect combat systems from cyber threats.

- By Component

- Hardware: Physical components like sensors (radar, sonar, EO/IR), processors, displays, data links, and actuating mechanisms.

- Software: Operational software, middleware for interoperability, AI/ML algorithms, and mission-specific applications.

- Services: Professional services including consulting, system design, integration and installation, training, and ongoing maintenance and support.

- By System Type

- New Build Integration: Integration solutions for newly developed or acquired defense platforms.

- Retrofit & Upgrade Integration: Modernizing and enhancing capabilities of existing legacy systems through integration.

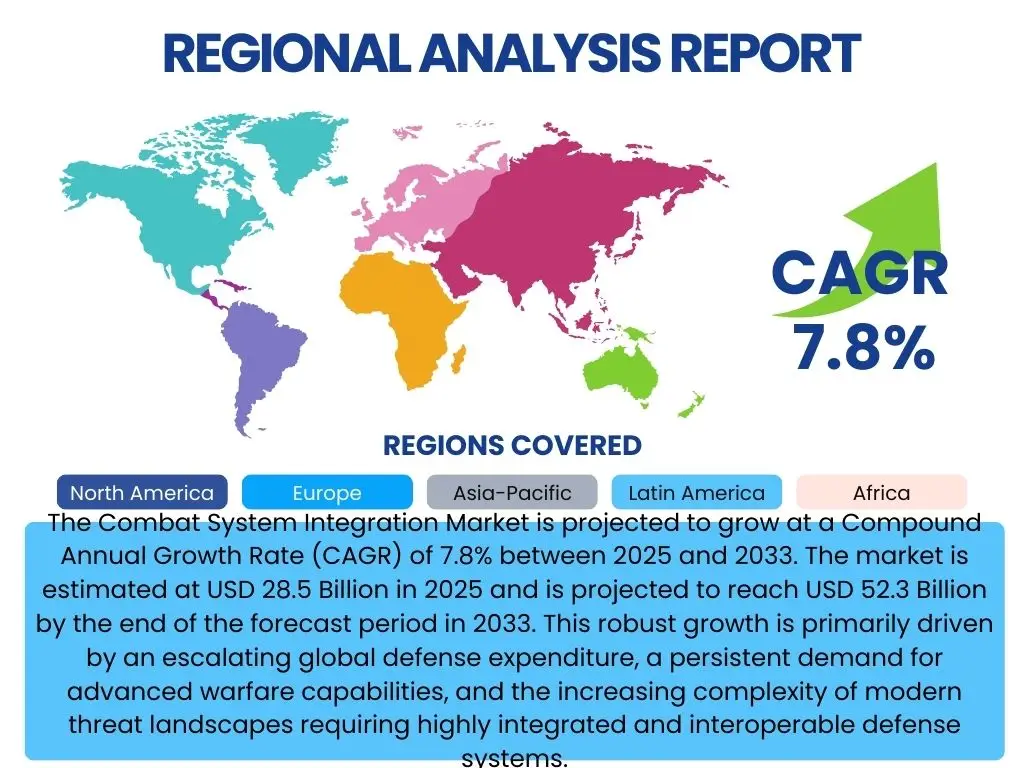

Regional Highlights

The Combat System Integration market exhibits distinct regional dynamics, influenced by defense budgets, geopolitical priorities, and technological readiness. North America, led by the United States, continues to be a dominant force, driven by substantial defense investments, advanced research and development capabilities, and a continuous push for technological superiority across all military domains. The region is a hub for innovation in AI, autonomous systems, and multi-domain integration, setting global benchmarks for combat system complexity and effectiveness.

The Asia Pacific region is rapidly emerging as a significant growth engine, fueled by the aggressive military modernization programs of countries like China, India, and South Korea, coupled with increasing defense spending in response to regional tensions. Europe also represents a mature market, with strong emphasis on naval and air defense system integration, driven by collaborative defense initiatives and NATO requirements. The Middle East and Africa are characterized by robust demand for advanced integrated systems to counter regional threats, while Latin America shows nascent growth primarily through naval and air force upgrades.

- North America: Dominant market share due to high defense expenditure, robust R&D, and early adoption of advanced technologies like AI, autonomous systems, and multi-domain integration by the United States and Canada.

- Asia Pacific (APAC): Fastest-growing region, driven by rapid military modernization, increasing defense budgets, and growing geopolitical tensions in countries like China, India, Japan, South Korea, and Australia.

- Europe: Significant market for naval, air, and ground system integration, propelled by collaborative defense programs (e.g., EU, NATO), technological advancements, and the need to counter evolving regional threats.

- Middle East & Africa (MEA): Growing demand for integrated combat systems, particularly for air defense, border security, and naval capabilities, driven by regional conflicts and substantial defense investments from oil-rich nations.

- Latin America: Moderate growth, primarily focused on upgrading existing naval and air force platforms, and modernizing command and control systems to enhance national security and surveillance capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Combat System Integration Market.- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- BAE Systems plc

- Northrop Grumman Corporation

- General Dynamics Corporation

- Thales Group

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Saab AB

- Rheinmetall AG

- Hanwha Systems Co. Ltd.

- Israel Aerospace Industries (IAI)

- Indra Sistemas S.A.

- Elbit Systems Ltd.

- Bharat Electronics Limited (BEL)

- Damen Schelde Naval Shipbuilding

- Naval Group

- Huntington Ingalls Industries (HII)

- General Atomics

- Boeing Defense, Space & Security

Frequently Asked Questions

Analyze common user questions about the Combat System Integration market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Combat System Integration?

Combat system integration is the process of connecting disparate hardware, software, and human elements of a military platform or network to function as a unified, cohesive system. This enables seamless information exchange, coordinated action, and enhanced operational efficiency across various domains like air, land, sea, cyber, and space.

Why is Combat System Integration important for modern militaries?

It is crucial for modern militaries to achieve superior situational awareness, accelerate decision-making, and enhance tactical effectiveness in complex, multi-domain warfare scenarios. Integration ensures that diverse assets can share real-time data and operate cohesively, maximizing combat power and survivability against sophisticated threats.

What are the key technologies driving Combat System Integration?

Key technologies include Artificial Intelligence (AI) and Machine Learning (ML) for data fusion and decision support, advanced sensors (radar, sonar, EO/IR), secure communication networks, open architecture software, and advanced C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems. These innovations facilitate real-time data exchange and autonomous capabilities.

What are the main challenges in Combat System Integration?

Primary challenges involve achieving interoperability between legacy and new systems, managing high development and procurement costs, addressing complex cybersecurity threats, and navigating stringent regulatory frameworks. Additionally, the shortage of skilled engineers and managing rapid technological obsolescence pose significant hurdles.

Which regions are leading in Combat System Integration investments?

North America, particularly the United States, leads in investments due to extensive R&D and defense spending. The Asia Pacific region is also a rapidly growing market, driven by military modernization efforts in countries like China and India. Europe maintains a strong focus on advanced naval and air defense system integration.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted