Water and Waste Water Market

Water and Waste Water Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700098 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

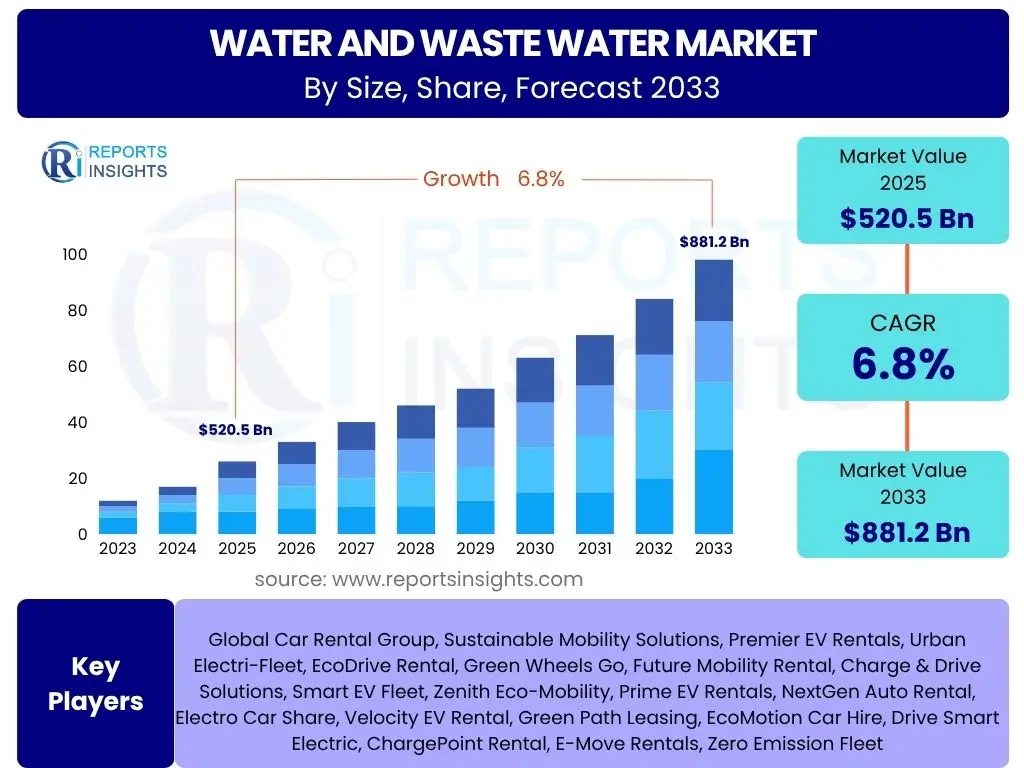

Water and Waste Water Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, valued at USD 520.5 Billion in 2025 and is projected to grow by USD 881.2 Billion by 2033, the end of the forecast period.

Key Water and Waste Water Market Trends & Insights

The global water and wastewater market is experiencing transformative shifts driven by increasing water scarcity, stringent environmental regulations, and a growing emphasis on sustainability. Key trends include the accelerated adoption of advanced treatment technologies, the integration of digital solutions for enhanced operational efficiency, and a pronounced move towards circular economy principles in water management. This paradigm shift aims to minimize water waste, promote resource recovery, and foster resilience in water infrastructure worldwide.

- Digitalization of water infrastructure with IoT, sensors, and data analytics.

- Increasing adoption of advanced purification and desalination technologies.

- Growing focus on water reuse and resource recovery (e.g., nutrient, energy from sludge).

- Rising public and private investment in sustainable water management solutions.

- Emergence of smart water grids for optimized distribution and leak detection.

- Stricter environmental regulations driving demand for efficient treatment.

- Decentralized water treatment solutions gaining traction in remote areas.

- Emphasis on energy efficiency in water and wastewater operations.

AI Impact Analysis on Water and Waste Water

Artificial Intelligence (AI) is poised to revolutionize the water and wastewater industry by enhancing operational efficiency, improving water quality management, and enabling predictive maintenance across complex infrastructure. AI algorithms can analyze vast datasets from sensors and meters to identify anomalies, predict equipment failures, optimize chemical dosing, and manage networks more effectively. This intelligent integration leads to reduced operational costs, minimized water losses, and more resilient water systems, ultimately contributing to better public health outcomes and environmental protection.

- Predictive maintenance for pumps and pipes, reducing downtime and costs.

- Optimized chemical dosing and treatment processes for improved efficiency.

- Real-time water quality monitoring and anomaly detection.

- Enhanced leak detection and network pressure management in distribution systems.

- Smart resource allocation and energy optimization in treatment plants.

- Automated decision-making for rapid response to operational issues.

- Improved forecasting of water demand and supply, aiding resource planning.

- Advanced analytics for assessing infrastructure health and prioritizing upgrades.

Key Takeaways Water and Waste Water Market Size & Forecast

- The market is projected for significant growth, driven by global water scarcity and infrastructure needs.

- A robust CAGR of 6.8% is anticipated from 2025 to 2033.

- The market is set to expand from USD 520.5 Billion in 2025 to USD 881.2 Billion by 2033.

- Key growth segments include advanced treatment technologies and smart water solutions.

- Emerging economies present substantial opportunities for infrastructure development and technology adoption.

Water and Waste Water Market Drivers Analysis

The burgeoning global population coupled with rapid urbanization is exerting unprecedented pressure on existing water resources and wastewater infrastructure. As urban centers expand, the demand for potable water escalates significantly, simultaneously increasing the volume of municipal and industrial wastewater requiring treatment. This demographic shift necessitates substantial investments in new water supply systems, advanced wastewater treatment plants, and robust distribution networks to ensure public health and environmental sustainability. The imperative to provide safe and reliable water services to a growing urban populace fuels continuous market expansion.

Furthermore, the escalating concern over water pollution and the increasing stringency of environmental regulations are pivotal drivers shaping the water and wastewater market. Governments worldwide are implementing stricter discharge limits for pollutants, mandates for industrial effluent treatment, and regulations promoting water reuse and resource recovery. These regulatory pressures compel industries and municipalities to adopt advanced treatment technologies and upgrade existing infrastructure to comply with environmental standards, thereby fostering demand for innovative solutions and services in the sector. The drive towards a circular economy in water management is also gaining momentum, encouraging technologies that reclaim valuable resources from wastewater, such as nutrients and energy, which further propels market growth.

Technological advancements, particularly in areas like membrane filtration, smart water solutions, and energy-efficient treatment processes, represent another crucial driver. Innovations in desalination technologies are making previously cost-prohibitive water sources viable for supply, addressing scarcity in arid regions. The integration of digital technologies, including IoT, AI, and big data analytics, is revolutionizing water management by enabling real-time monitoring, predictive maintenance, and optimized operational efficiency. These technological leaps reduce operational costs, enhance water quality, and improve the resilience of water infrastructure, making sophisticated solutions more accessible and attractive for broader adoption across diverse applications, from municipal utilities to industrial facilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization and Population Growth | +1.8% | Asia Pacific, Africa, Latin America | Long-term |

| Increasing Water Scarcity and Stress | +1.5% | Middle East, North Africa, parts of Asia and Europe | Mid-to-Long-term |

| Stringent Environmental Regulations | +1.2% | Europe, North America, rapidly industrializing Asian economies | Mid-term |

| Technological Advancements in Treatment | +1.0% | Global, particularly developed nations and innovators | Short-to-Mid-term |

| Aging Water Infrastructure Modernization | +0.8% | North America, Europe | Long-term |

Water and Waste Water Market Restraints Analysis

A significant impediment to the growth of the water and wastewater market is the substantial capital expenditure required for infrastructure development and technology adoption. Building new treatment plants, laying extensive pipeline networks, and implementing advanced digital solutions involve considerable upfront investment. Many municipalities, particularly in developing regions, face budget constraints and struggle to secure the necessary financing. This financial barrier often delays or prevents the implementation of critical projects, limiting market expansion and the adoption of more efficient, sustainable technologies. The long payback periods for water infrastructure projects further deter private investment without robust government support or innovative financing models.

Another prevalent restraint is the often-fragmented regulatory landscape and bureaucratic complexities that characterize the water sector. Diverse regulations across different regions and countries can create inconsistencies in standards, making it challenging for global solution providers to scale their operations efficiently. Permitting processes can be lengthy and cumbersome, delaying project approvals and increasing administrative costs. Furthermore, the inherent conservatism within some public utilities, coupled with resistance to adopting new technologies due to perceived risks or lack of technical expertise, can slow down innovation and market penetration for advanced solutions, even when their long-term benefits are clear.

The high operational and energy costs associated with certain water and wastewater treatment processes also pose a considerable challenge. Energy consumption, especially for pumping, aeration, and advanced membrane filtration or desalination, forms a significant portion of a treatment plant's operating budget. While there is a growing push for energy-efficient solutions and renewable energy integration, the initial investment for such systems can be high, and the immediate impact of energy price volatility can strain operational budgets. This economic pressure can force utilities to opt for less energy-intensive, albeit less efficient, older technologies or defer upgrades, thereby restraining the market's shift towards more sustainable and technologically advanced practices.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure Requirements | -1.5% | Global, particularly developing nations | Long-term |

| Stringent Regulatory Hurdles and Bureaucracy | -1.0% | North America, Europe, fragmented markets globally | Mid-term |

| High Operational and Energy Costs | -0.8% | Global, especially energy-intensive processes like desalination | Short-to-Mid-term |

| Lack of Skilled Workforce and Technical Expertise | -0.5% | Developing regions, remote areas globally | Mid-term |

Water and Waste Water Market Opportunities Analysis

The increasing global emphasis on water reuse and the circular economy presents a significant growth opportunity for the water and wastewater market. As freshwater resources become scarcer, industries and municipalities are increasingly looking to treat and reuse wastewater for non-potable applications such as agricultural irrigation, industrial processes, and even potable water supplementation. This shift away from traditional linear water consumption models opens avenues for advanced treatment technologies, including tertiary filtration and disinfection, as well as integrated systems that recover valuable resources like nutrients, energy, and valuable chemicals from wastewater streams. The drive towards a circular economy not only conserves resources but also creates new revenue streams and reduces operational costs for utilities, making these solutions highly attractive for future investments.

Furthermore, the significant gap in water and wastewater infrastructure, particularly in developing and emerging economies, offers vast opportunities for new investments and project development. Many regions still lack basic sanitation facilities, adequate access to clean drinking water, or sufficient wastewater treatment capacity to meet the demands of their growing populations and industrial activities. This infrastructure deficit necessitates massive public and private sector investments in building new water supply networks, expanding wastewater collection systems, and constructing modern treatment plants. International development aid, public-private partnerships, and sustainable financing mechanisms are crucial in unlocking these opportunities, driving demand for a wide range of water and wastewater solutions, from engineering and construction to operational services and equipment supply.

The digitalization of water management through smart water solutions, including IoT, AI, and big data analytics, is creating a burgeoning market for innovative technologies. These solutions enable real-time monitoring of water quality, efficient leak detection, optimized network pressure management, and predictive maintenance for critical infrastructure components. Smart sensors, automated control systems, and data-driven analytical platforms enhance operational efficiency, reduce water losses, and improve overall system resilience. As utilities seek to modernize their operations and improve service delivery, the adoption of these digital technologies will accelerate, presenting substantial opportunities for technology providers specializing in smart metering, intelligent network management, and advanced data processing capabilities, transforming how water is managed from source to tap.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Water Reuse & Resource Recovery | +1.3% | Arid regions globally, highly industrialized areas | Mid-to-Long-term |

| Infrastructure Development in Emerging Economies | +1.5% | Asia Pacific, Africa, Latin America | Long-term |

| Advancements in Smart Water Technologies (IoT, AI) | +1.0% | Developed economies, tech-forward utilities globally | Short-to-Mid-term |

| Decentralized Water & Wastewater Solutions | +0.7% | Rural areas, remote communities, specific industrial applications | Mid-term |

Water and Waste Water Market Challenges Impact Analysis

One of the most pressing challenges confronting the water and wastewater market is the persistent issue of aging infrastructure, particularly in developed regions. Decades-old pipes, treatment plants, and pumping stations are prone to leaks, inefficiencies, and frequent breakdowns, leading to significant water losses, increased maintenance costs, and compromised service reliability. The enormous investment required to repair, replace, or upgrade these vast networks often outstrips available funding for municipalities and utilities. This challenge is compounded by the fact that infrastructure degradation often occurs out of sight, making it less politically urgent to address until critical failures occur, thereby creating a backlog of necessary improvements that restrain market modernization efforts and hinder the adoption of new technologies.

Furthermore, the growing threat of climate change introduces a complex array of challenges to water management. Extreme weather events such as prolonged droughts, intense floods, and rising sea levels directly impact water availability and quality. Droughts deplete freshwater sources, necessitating expensive alternative supplies like desalination or advanced water reuse, while floods can overwhelm wastewater treatment systems, leading to untreated discharge and contamination. Rising sea levels can cause saltwater intrusion into coastal aquifers, diminishing potable water supplies. These climate-induced stressors demand significant investments in climate-resilient infrastructure, including flood barriers, enhanced stormwater management, and diversified water sources, which can strain budgets and divert resources from other essential upgrades, thus impacting market growth patterns.

The fragmented nature of governance and ownership within the water sector, particularly with numerous small and medium-sized utilities operating independently, presents another significant hurdle. This fragmentation can lead to a lack of standardization, limited economies of scale, and difficulties in implementing sector-wide best practices or adopting large-scale technological innovations. Smaller utilities often lack the financial resources, technical expertise, or political leverage to undertake major infrastructure projects or invest in cutting-edge solutions. This decentralization can hinder a cohesive national or regional approach to water management challenges, making it difficult to achieve broader market penetration for advanced technologies and integrated solutions, thus slowing overall market development and efficiency improvements.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging and Deteriorating Infrastructure | -1.2% | North America, Europe, parts of developed Asia | Long-term |

| Impact of Climate Change on Water Resources | -1.0% | Global, particularly vulnerable regions | Mid-to-Long-term |

| Fragmented Market Structure and Governance | -0.7% | North America, Europe, certain decentralized systems | Mid-term |

| Public Perception and Acceptance of Water Reuse | -0.5% | Global, varies by cultural context | Long-term |

Water and Waste Water Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global water and wastewater market, covering historical trends, current dynamics, and future projections. It offers strategic insights into market size, growth drivers, restraints, opportunities, and challenges, aiding stakeholders in making informed business decisions. The report delves into key market segments, regional performance, and the competitive landscape, incorporating the latest technological advancements and regulatory impacts. This report is designed to equip market participants with a robust understanding of the evolving industry, identifying growth avenues and potential risks across the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 520.5 Billion |

| Market Forecast in 2033 | USD 881.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Veolia, Suez, Xylem, Ecolab, Pentair, A. O. Smith, DuPont Water Solutions, Kemira, Grundfos, WSP Global, Jacobs Engineering Group, Black & Veatch, AECOM, Tetra Tech, Arcadis, Ramboll, Organo Corporation, Hitachi Zosen Corporation, Kurita Water Industries, Severn Trent |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Water and Waste Water Market is comprehensively segmented to provide a granular view of its diverse components and sub-sectors. This detailed segmentation allows for a precise understanding of market dynamics across various applications, technologies, and service offerings, enabling stakeholders to identify specific growth areas and tailor strategies effectively. Each segment contributes uniquely to the overall market landscape, driven by distinct needs and regulatory frameworks.

- By Type: This segment differentiates between the treatment of incoming water for various uses and the treatment of wastewater generated from different sources. Water Treatment focuses on making water suitable for consumption or industrial processes, while Wastewater Treatment addresses the purification of contaminated water before discharge or reuse. Water & Wastewater Infrastructure encompasses the physical networks supporting these processes.

- Water Treatment: Encompasses processes to improve water quality for specific end-uses, including potable water and industrial applications.

- Wastewater Treatment: Involves the removal of contaminants from domestic, commercial, and industrial wastewater.

- Water & Wastewater Infrastructure: Refers to the physical assets like pipelines, pumping stations, and reservoirs critical for water delivery and wastewater collection.

- By Application: This segmentation categorizes the market based on the primary end-user sectors, which exhibit varying demands and regulatory requirements for water and wastewater services. Municipal applications primarily serve residential and commercial establishments, whereas industrial applications cater to specific industry needs, each with unique contaminant profiles and treatment complexities.

- Municipal: Pertains to water and wastewater services for residential communities, commercial establishments, and public institutions.

- Industrial: Covers water and wastewater management solutions tailored for diverse industrial sectors such as chemicals, power generation, food & beverage, mining, and pharmaceuticals.

- By Technology: This segment highlights the diverse range of technological solutions employed across the water and wastewater treatment spectrum. From fundamental physical filtration methods to advanced chemical and biological processes, and cutting-edge digital solutions, these technologies underpin the efficiency and effectiveness of water management, continually evolving to meet higher standards and reduce operational footprints.

- Filtration: Includes methods like membrane filtration, sand filtration, and activated carbon filtration used for removing suspended solids and contaminants.

- Disinfection: Processes such as chlorination, UV disinfection, and ozonation employed to eliminate pathogenic microorganisms from water.

- Biological Treatment: Utilizes microorganisms to break down organic pollutants, including aerobic and anaerobic processes.

- Sludge Treatment: Technologies focused on managing and processing the solid by-products (sludge) from wastewater treatment.

- Desalination: Processes like Reverse Osmosis and Multi-Stage Flash Distillation for converting saline water into fresh water.

- Smart Water Management Solutions: Integration of sensors, IoT, SCADA systems, and data analytics software for intelligent monitoring and control.

- By Service: This segmentation focuses on the comprehensive range of services offered within the market beyond just equipment or infrastructure. These services are crucial for the planning, implementation, and ongoing operation of water and wastewater systems, providing specialized expertise and support throughout the lifecycle of projects.

- Design & Engineering: Services related to the planning, design, and development of water and wastewater facilities.

- Operation & Maintenance: Ongoing services for the efficient running, upkeep, and repair of water and wastewater systems.

- Consulting Services: Expert advice and strategic guidance on water resource management, regulatory compliance, and project feasibility.

- Equipment Supply & Installation: Provision and setup of various machinery and components required for water and wastewater treatment.

Regional Highlights

The global water and wastewater market exhibits significant regional variations in growth drivers, technological adoption, and infrastructure development, reflecting diverse socio-economic conditions, regulatory environments, and water resource availability. Each region presents unique opportunities and challenges that shape its market trajectory.

- Asia Pacific (APAC) stands out as the fastest-growing and largest market, primarily driven by rapid urbanization, massive industrial expansion, and an escalating population that intensifies demand for clean water and efficient wastewater treatment. Countries like China and India are undertaking large-scale infrastructure projects to address water scarcity and pollution, investing heavily in new treatment plants and smart water solutions. The region's focus on sustainable development goals and increasing environmental awareness also fuels the adoption of advanced technologies and water reuse initiatives.

- North America represents a mature yet dynamic market, characterized by the critical need for aging infrastructure rehabilitation and modernization. Strict environmental regulations, coupled with a strong emphasis on technological innovation and digital transformation, drive investments in smart water grids, leak detection systems, and advanced treatment processes. The U.S. and Canada are focusing on improving water quality, reducing non-revenue water, and enhancing system resilience against climate change impacts.

- Europe maintains a robust market, propelled by stringent EU directives on water quality, wastewater discharge, and circular economy principles. The region is at the forefront of adopting advanced biological treatment, nutrient recovery, and energy-efficient solutions. Investments are largely concentrated on upgrading existing facilities to meet higher standards, embracing digital twin technologies, and fostering public-private partnerships for sustainable water management across diverse national contexts.

- Latin America is a developing market with substantial growth potential, driven by expanding access to safe drinking water and sanitation services, particularly in urban areas. While facing challenges such as funding constraints and fragmented regulatory frameworks, increasing public awareness and international development aid are fostering investments in basic infrastructure and the adoption of more effective treatment solutions. Brazil, Mexico, and Argentina are key countries leading this expansion.

- Middle East & Africa (MEA) is characterized by severe water scarcity, making desalination a critical component of its water supply strategy, especially in the Arabian Gulf countries. High population growth rates and industrial development are also driving demand for comprehensive wastewater treatment and reuse solutions. Investments are substantial, often government-backed, focusing on large-scale projects that integrate advanced technologies to ensure long-term water security and sustainable resource management amidst arid conditions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Water and Waste Water Market. Some of the leading players profiled in the report include -

- Veolia

- Suez

- Xylem

- Ecolab

- Pentair

- A. O. Smith

- DuPont Water Solutions

- Kemira

- Grundfos

- WSP Global

- Jacobs Engineering Group

- Black & Veatch

- AECOM

- Tetra Tech

- Arcadis

- Ramboll

- Organo Corporation

- Hitachi Zosen Corporation

- Kurita Water Industries

- Severn Trent

Frequently Asked Questions:

What is the current market size of the Water and Waste Water Market?

The Water and Waste Water Market was valued at USD 520.5 Billion in 2025, reflecting significant global investments in sustainable water management and infrastructure development.What is the projected growth rate (CAGR) for the Water and Waste Water Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing water scarcity, urbanization, and stringent environmental regulations.Which key trends are shaping the Water and Waste Water Market?

Key trends include the rapid adoption of smart water technologies and digitalization, a strong focus on water reuse and circular economy principles, the implementation of advanced treatment solutions, and substantial investments in modernizing aging water infrastructure worldwide.What are the primary drivers for the growth of the Water and Waste Water Market?

The market is primarily driven by accelerating population growth and urbanization, rising global water scarcity, increasingly stringent environmental regulations, and continuous technological advancements in water and wastewater treatment processes.How does AI impact the Water and Waste Water Market?

AI significantly impacts the market by enabling predictive maintenance for infrastructure, optimizing treatment processes through real-time data analysis, enhancing leak detection, and improving overall operational efficiency and resource management in water utilities and industrial facilities.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted