CMP Consumable Market

CMP Consumable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704994 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

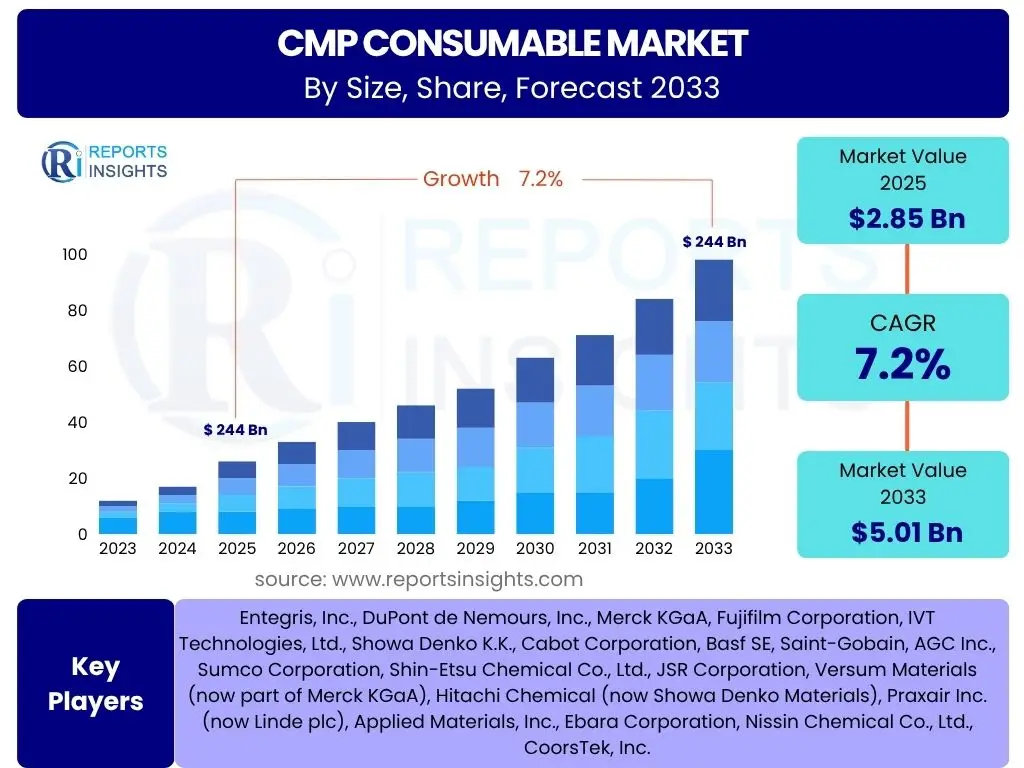

CMP Consumable Market Size

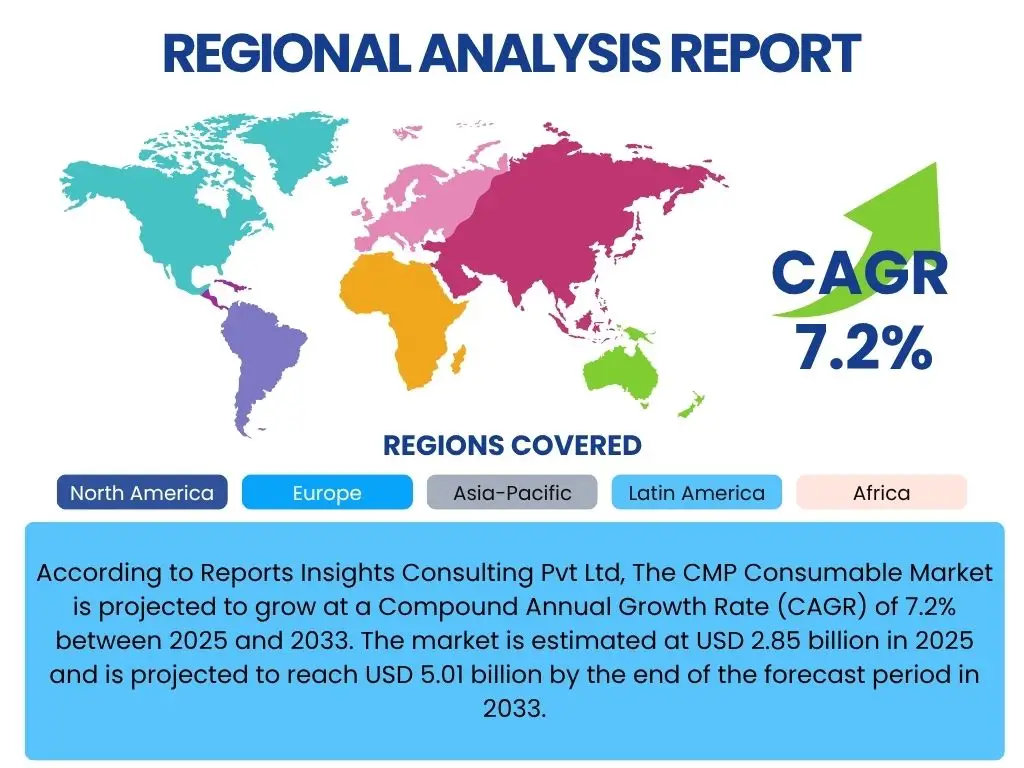

According to Reports Insights Consulting Pvt Ltd, The CMP Consumable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 5.01 billion by the end of the forecast period in 2033.

Key CMP Consumable Market Trends & Insights

The CMP (Chemical Mechanical Planarization) consumable market is profoundly shaped by the relentless drive for smaller, more powerful, and energy-efficient semiconductor devices. Common user inquiries often revolve around the adoption of advanced materials, the impact of next-generation packaging technologies, and the industry's response to environmental sustainability. A key trend identified is the increasing demand for high-performance slurries and pads capable of achieving ultra-flat surfaces with minimal defects on novel materials like silicon carbide (SiC) and gallium nitride (GaN), crucial for power electronics and 5G applications. Furthermore, the integration of advanced analytics and AI in CMP processes is becoming a critical differentiator, enabling real-time process optimization and predictive maintenance, thereby reducing waste and improving yield.

Another significant trend is the growing emphasis on sustainable manufacturing practices within the semiconductor industry. This includes the development of environmentally friendly CMP consumables, such as greener slurries with reduced chemical usage and recyclable or reusable pad materials, addressing concerns about waste generation and chemical disposal. The market also observes a shift towards more customized consumable solutions designed for specific process nodes and device architectures, moving away from generic products. This customization is driven by the complex requirements of 3D ICs, heterogeneous integration, and advanced memory technologies, which demand precise planarization control across diverse material stacks. These evolving needs necessitate continuous innovation in consumable formulations and designs to maintain competitive edge and meet stringent performance criteria.

- Development of high-performance slurries and pads for advanced nodes (e.g., sub-7nm).

- Increased demand for CMP consumables in advanced packaging (e.g., 3D IC, Wafer-Level Packaging).

- Growing adoption of AI and machine learning for CMP process optimization and defect reduction.

- Emphasis on sustainable and eco-friendly CMP consumables and processes.

- Customization of consumables for specific material stacks and device architectures.

- Expansion into new materials like SiC and GaN for power and RF applications.

AI Impact Analysis on CMP Consumable

Users frequently inquire about the transformative potential of artificial intelligence (AI) in the CMP consumable sector, with common questions centering on how AI improves efficiency, enhances quality, and potentially automates processes. AI's influence on CMP consumable manufacturing and application is multifaceted, primarily by enabling more precise control, predictive capabilities, and optimized material usage. AI algorithms can analyze vast datasets from CMP processes, including slurry flow, pad wear, and wafer surface conditions, to identify patterns and anomalies that are imperceptible to human operators. This leads to predictive maintenance for equipment and consumables, anticipating wear and optimizing replacement schedules, thereby minimizing downtime and maximizing consumable lifespan.

Furthermore, AI-driven process control systems are revolutionizing CMP by providing real-time adjustments to polishing parameters, such as pressure, speed, and slurry composition, to achieve desired planarization targets with higher accuracy and consistency. This capability significantly reduces material waste due to over-polishing or under-polishing and improves overall yield, directly impacting the consumption rates and specifications of CMP materials. Concerns often include the initial investment in AI infrastructure, the need for specialized data scientists, and ensuring data security. However, the long-term benefits of enhanced throughput, reduced defects, and optimized consumable performance are driving widespread adoption, pushing consumable manufacturers to design materials compatible with smart, AI-integrated CMP tools.

- Predictive Maintenance: AI analyzes equipment and consumable wear patterns, predicting optimal replacement times for pads and conditioning disks, extending lifespan and reducing unplanned downtime.

- Real-time Process Optimization: AI algorithms monitor CMP parameters (e.g., slurry flow, pressure, temperature) and make real-time adjustments to achieve precise planarization, reducing material waste and improving yield.

- Enhanced Defect Detection and Classification: AI-powered vision systems improve the accuracy and speed of identifying surface defects on wafers, allowing for immediate process correction and better consumable quality control.

- Optimized Consumable Formulation: AI can accelerate the R&D of new slurries and pads by simulating material interactions and predicting performance characteristics, leading to more efficient product development.

- Supply Chain Efficiency: AI and machine learning are used to forecast demand for specific consumables, optimize inventory levels, and enhance supply chain resilience, ensuring timely availability.

Key Takeaways CMP Consumable Market Size & Forecast

Common user questions regarding the CMP consumable market size and forecast often focus on the primary growth drivers, the impact of technological shifts, and the long-term sustainability of demand. The analysis reveals that the market's robust growth trajectory is fundamentally underpinned by the continuous expansion of the global semiconductor industry, particularly driven by advancements in artificial intelligence, 5G technology, high-performance computing, and the proliferation of IoT devices. These applications necessitate increasingly complex chip architectures and smaller process nodes, which in turn require more advanced and precise CMP processes and, consequently, higher-quality consumables. The forecast indicates sustained demand across various wafer types and end-use applications, solidifying the market's resilience against economic fluctuations in specific sectors.

Moreover, a critical insight from the market forecast is the pronounced regional disparity in growth, with the Asia Pacific region continuing to dominate due to its concentration of leading semiconductor manufacturing foundries and integrated device manufacturers (IDMs). This geographical concentration implies significant opportunities for consumable suppliers to establish or expand their presence in this region. Furthermore, the market is expected to witness ongoing innovation in consumable materials, driven by the need to support novel chip materials and packaging techniques. This continuous evolution in product offerings, coupled with a focus on cost-efficiency and environmental compliance, will be pivotal for market players to capture growth opportunities and maintain competitive advantage through the forecast period.

- The market is poised for significant and consistent growth, primarily fueled by the burgeoning semiconductor industry.

- Technological advancements in chip manufacturing, such as smaller process nodes and 3D packaging, are key catalysts for consumable demand.

- Asia Pacific (APAC) is projected to remain the dominant region, driven by its expansive manufacturing infrastructure.

- Innovation in slurry and pad materials will be crucial for meeting the evolving demands of advanced wafer materials and processes.

- Emphasis on sustainability and efficiency will drive the development of greener and more cost-effective consumable solutions.

CMP Consumable Market Drivers Analysis

The CMP consumable market is significantly propelled by several synergistic factors, primarily stemming from the advancements and expansion within the global semiconductor industry. The relentless pursuit of miniaturization in electronic devices necessitates finer process control and superior surface planarization, directly increasing the demand for high-quality CMP slurries, pads, and conditioning disks. As chip manufacturers move towards advanced process nodes (e.g., 7nm, 5nm, and beyond), the complexity of multi-layered structures escalates, requiring more precise and selective polishing materials to achieve the required flatness and defectivity levels. This technological push underpins a fundamental demand for sophisticated consumables.

Another pivotal driver is the explosive growth in emerging technologies such as Artificial Intelligence (AI), 5G, IoT, and high-performance computing (HPC), all of which rely heavily on advanced semiconductor components. The burgeoning adoption of these technologies across various sectors, from automotive to consumer electronics and data centers, translates directly into increased wafer fabrication volumes and, consequently, a higher consumption of CMP consumables. Furthermore, the increasing complexity of advanced packaging technologies like 3D ICs and heterogeneous integration, which involve multiple stacking layers, mandates multiple CMP steps, thus amplifying the market for specialized consumable solutions capable of handling diverse materials and intricate designs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Semiconductor Industry & Miniaturization | +1.5% | Global, especially APAC (China, Taiwan, South Korea) | 2025-2033 (Long-term) |

| Increase in Advanced Packaging Technologies (3D IC, Wafer-Level Packaging) | +1.2% | Global, particularly APAC (Taiwan, South Korea) | 2025-2033 (Mid- to Long-term) |

| Rising Demand for AI, 5G, and IoT Devices | +1.0% | Global, North America, APAC (China) | 2025-2030 (Short- to Mid-term) |

| Technological Advancements in Wafer Materials (SiC, GaN) | +0.8% | Global, North America, Europe, Japan | 2028-2033 (Mid- to Long-term) |

| Increased Investment in Foundry Expansion and Capacity | +0.7% | APAC, North America, Europe | 2025-2030 (Short- to Mid-term) |

CMP Consumable Market Restraints Analysis

Despite robust growth drivers, the CMP consumable market faces specific restraints that could temper its expansion. One significant challenge revolves around the high capital investment required for developing and manufacturing advanced CMP consumables. The complexity of formulating slurries with precise chemical compositions and designing pads with specific mechanical properties demands extensive research and development, along with specialized manufacturing facilities. This high entry barrier can limit new entrants and stifle innovation, potentially leading to slower market adaptation to rapidly evolving semiconductor manufacturing needs. Furthermore, the inherent technological complexity involved in achieving ultra-flat surfaces with minimal defects at advanced nodes requires continuous material innovation, which often comes with high R&D costs that can impact profitability and market pricing.

Another major restraint is the increasing stringency of environmental regulations concerning the disposal of CMP waste, particularly slurries containing abrasive particles and various chemicals. The semiconductor industry is under growing pressure to adopt more sustainable practices, leading to higher costs associated with waste treatment, recycling, and compliance. This regulatory burden can escalate operational expenses for consumable manufacturers and end-users alike, potentially influencing material choices and process efficiencies. Additionally, supply chain disruptions, as evidenced by recent global events, pose a significant challenge. The specialized nature of raw materials and the globalized supply network for CMP consumables mean that geopolitical tensions, trade disputes, or natural disasters can lead to material shortages, price volatility, and delays in production, impacting market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development and Manufacturing Costs | -0.8% | Global | 2025-2033 (Long-term) |

| Stringent Environmental Regulations and Waste Management Costs | -0.7% | Europe, North America, Japan, China | 2025-2033 (Long-term) |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.5% | Global | 2025-2028 (Short- to Mid-term) |

| Technological Obsolescence and Rapid Product Cycles | -0.4% | Global | 2028-2033 (Mid- to Long-term) |

| Intense Price Competition Among Key Players | -0.3% | Global | 2025-2033 (Long-term) |

CMP Consumable Market Opportunities Analysis

The CMP consumable market is ripe with opportunities driven by the dynamic shifts within the semiconductor industry and broader technological landscape. A significant opportunity lies in the burgeoning adoption of advanced packaging technologies such as 3D ICs, fan-out wafer-level packaging (FOWLP), and heterogeneous integration. These complex architectures require multiple precise planarization steps, often involving diverse materials, leading to an increased demand for specialized and high-performance CMP slurries and pads. Consumable manufacturers who can develop innovative solutions tailored to these intricate packaging demands stand to gain substantial market share and solidify their position as key enablers of next-generation devices.

Furthermore, the global imperative for sustainability presents a compelling opportunity for market players to develop and commercialize eco-friendly CMP consumables. This includes initiatives such as creating greener slurries with biodegradable components, reducing hazardous chemical content, and designing pads that are recyclable or have extended lifespans, thereby minimizing waste. The increasing focus on new materials beyond traditional silicon, such as Silicon Carbide (SiC) and Gallium Nitride (GaN) for power electronics and optoelectronics, also opens up new avenues. These materials have unique chemical and mechanical properties, necessitating novel CMP consumable formulations that can achieve superior surface quality without damaging the substrate. Companies that invest in R&D for these specialized consumables can tap into emerging, high-growth niche markets within the semiconductor ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Consumables for 3D IC & Heterogeneous Integration | +1.0% | Global, particularly APAC (Taiwan, South Korea) | 2025-2033 (Long-term) |

| Growing Demand for SiC and GaN Wafers in Power Electronics & EV | +0.9% | Global, North America, Europe, Japan | 2028-2033 (Mid- to Long-term) |

| Emphasis on Green & Sustainable CMP Solutions | +0.8% | Europe, North America, Japan | 2025-2033 (Long-term) |

| Expansion into Emerging Economies with Growing Semiconductor Manufacturing | +0.7% | Southeast Asia, India, China (inland) | 2025-2030 (Short- to Mid-term) |

| Leveraging AI/ML for Consumable Performance Optimization | +0.6% | Global | 2025-2030 (Short- to Mid-term) |

CMP Consumable Market Challenges Impact Analysis

The CMP consumable market confronts several intrinsic challenges that necessitate constant innovation and strategic adaptation from market players. One primary challenge is the requirement for maintaining stringent process uniformity and achieving zero defects at increasingly smaller process nodes. As semiconductor geometries shrink, the tolerance for defects diminishes drastically, making the CMP process, and by extension, the consumables, critically responsible for final device yield. This demands extremely consistent performance from slurries and pads, which can be difficult to achieve across large-scale manufacturing and diverse process conditions. Any slight variation in consumable quality can lead to significant financial losses for chip manufacturers, placing immense pressure on consumable suppliers.

Another significant challenge is the ongoing pressure for cost optimization within the highly competitive semiconductor industry. While CMP consumables are crucial, they also represent a significant operational expense for wafer fabrication plants. Manufacturers are constantly seeking ways to reduce overall cost of ownership without compromising quality, leading to continuous negotiation and demand for more cost-effective consumable solutions. This pressure forces consumable suppliers to innovate not only in performance but also in manufacturing efficiency and material sourcing to offer competitive pricing. Furthermore, the rapid pace of technological change in semiconductor manufacturing means that consumable formulations and designs can quickly become obsolete, requiring continuous investment in research and development to keep pace with evolving wafer materials, device architectures, and polishing requirements, adding to operational complexity and financial burden.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-High Uniformity and Defectivity Control at Advanced Nodes | -0.5% | Global | 2025-2033 (Long-term) |

| Cost Pressure from Semiconductor Manufacturers | -0.4% | Global | 2025-2033 (Long-term) |

| Rapid Technological Obsolescence & Need for Continuous R&D | -0.3% | Global | 2025-2033 (Long-term) |

| Management of Hazardous Waste and Byproducts | -0.2% | Europe, North America, Japan | 2025-2033 (Long-term) |

| Skilled Workforce Shortage in Advanced Materials and Processes | -0.1% | Global | 2025-2030 (Short- to Mid-term) |

CMP Consumable Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global CMP (Chemical Mechanical Planarization) Consumable Market, offering a detailed understanding of its current landscape, historical performance, and future growth projections. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges that collectively influence market dynamics. It segments the market extensively by consumable type, application, and end-use industry, providing granular insights into demand patterns across various categories. Furthermore, the report offers a robust regional analysis, highlighting key market trends and growth prospects across major geographical regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The competitive landscape is also critically assessed, profiling leading market players and their strategic initiatives, including product innovation, partnerships, and mergers & acquisitions, to provide a holistic view of the market's structure and competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 5.01 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Entegris, Inc., DuPont de Nemours, Inc., Merck KGaA, Fujifilm Corporation, IVT Technologies, Ltd., Showa Denko K.K., Cabot Corporation, Basf SE, Saint-Gobain, AGC Inc., Sumco Corporation, Shin-Etsu Chemical Co., Ltd., JSR Corporation, Versum Materials (now part of Merck KGaA), Hitachi Chemical (now Showa Denko Materials), Praxair Inc. (now Linde plc), Applied Materials, Inc., Ebara Corporation, Nissin Chemical Co., Ltd., CoorsTek, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The CMP consumable market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a detailed analysis of demand patterns, technological preferences, and growth opportunities across various product types, applications, and end-use industries. Such a comprehensive breakdown is crucial for stakeholders to identify high-growth segments, tailor product strategies, and make informed investment decisions within this intricate ecosystem.

- By Type: This segment categorizes CMP consumables based on their fundamental composition and function within the polishing process.

- CMP Slurries: These are suspensions of abrasive particles in a chemical solution, designed to achieve both mechanical removal and chemical etching of wafer surfaces. Sub-segments include Alumina Slurry, Silica Slurry, Ceria Slurry, and Other specialized slurries tailored for specific materials or layers.

- CMP Pads: These are the polishing surfaces that hold the slurry and come into direct contact with the wafer. They are crucial for dictating the polishing rate, uniformity, and defectivity. Main types include Polyurethane Pads and Composite Pads, among others.

- CMP Conditioning Disks: Tools used to maintain the surface roughness and flatness of the CMP pads throughout the polishing process, ensuring consistent performance. Categories include Diamond Conditioning Disks and Non-Diamond Conditioning Disks.

- By Application: This segmentation focuses on the specific types of wafers or device layers where CMP consumables are utilized.

- Silicon Wafers, Sapphire Wafers, Memory Devices, Logic Devices, MEMS (Micro-Electro-Mechanical Systems), and Others (e.g., Power Devices, Optoelectronics, Advanced Interconnects). Each application often demands unique consumable properties due to varying material hardness, chemical reactivity, and desired planarization outcomes.

- By End-Use Industry: This segment classifies the market based on the primary sectors that drive demand for semiconductor devices, and consequently, CMP consumables.

- Semiconductor Manufacturing (Foundries, IDMs), Consumer Electronics (Smartphones, PCs, Wearables), Automotive (Infotainment, ADAS, EVs), Healthcare (Medical Devices, Diagnostics), Aerospace & Defense, and Others (e.g., Telecommunications, Industrial).

Regional Highlights

- Asia Pacific (APAC): Dominates the CMP consumable market due to the high concentration of semiconductor manufacturing facilities, including major foundries (Taiwan, South Korea), leading IDMs, and expanding fabs in China and Japan. The region benefits from significant investments in advanced process nodes and packaging technologies, driving robust demand for high-performance slurries and pads. Countries like Taiwan, South Korea, China, and Japan are pivotal.

- North America: A key region driven by strong research and development activities, presence of major semiconductor equipment manufacturers, and a focus on advanced logic, memory, and specialized semiconductor devices. The demand here is often for highly specialized and innovative CMP consumable solutions to support cutting-edge R&D and high-value production.

- Europe: Characterized by a growing focus on niche semiconductor applications, particularly in automotive electronics, industrial IoT, and power management (SiC/GaN). While not as large in volume as APAC, Europe represents a market for high-performance and specialized consumables, alongside a strong emphasis on sustainable manufacturing practices.

- Latin America & Middle East and Africa (MEA): These regions currently hold smaller shares but are emerging markets with increasing investments in localized electronics manufacturing and assembly. Growth is anticipated as governments prioritize domestic semiconductor capabilities and as global players expand their footprint, though demand for advanced CMP consumables remains comparatively nascent.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the CMP Consumable Market.- Entegris, Inc.

- DuPont de Nemours, Inc.

- Merck KGaA

- Fujifilm Corporation

- IVT Technologies, Ltd.

- Showa Denko K.K.

- Cabot Corporation

- Basf SE

- Saint-Gobain

- AGC Inc.

- Sumco Corporation

- Shin-Etsu Chemical Co., Ltd.

- JSR Corporation

- Applied Materials, Inc.

- Ebara Corporation

- Nissin Chemical Co., Ltd.

- CoorsTek, Inc.

- Versum Materials (now part of Merck KGaA)

- Hitachi Chemical (now Showa Denko Materials)

- Praxair Inc. (now Linde plc)

Frequently Asked Questions

Analyze common user questions about the CMP Consumable market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is CMP and why are consumables essential?

CMP (Chemical Mechanical Planarization) is a critical process in semiconductor manufacturing that combines chemical etching with mechanical polishing to achieve ultra-flat and defect-free wafer surfaces. Consumables, including slurries, pads, and conditioning disks, are essential because they directly facilitate the material removal process, ensuring precise planarization and low defectivity, which are vital for device performance and yield at advanced process nodes.

What are the primary types of CMP consumables?

The primary types of CMP consumables are slurries, pads, and conditioning disks. Slurries, typically composed of abrasive particles in a chemical solution, perform the material removal. Pads provide the mechanical polishing surface and hold the slurry. Conditioning disks are used to maintain the optimal surface texture of the pads for consistent polishing performance.

How is the demand for CMP consumables influenced by technological advancements?

Technological advancements, such as the miniaturization of integrated circuits, the adoption of 3D ICs and advanced packaging, and the rise of new materials like SiC and GaN, directly drive the demand for more sophisticated CMP consumables. These advancements require consumables capable of higher precision, selectivity, and lower defectivity, pushing continuous innovation in material science and engineering for slurries and pads.

Which regions are leading the growth in the CMP consumable market?

The Asia Pacific (APAC) region, particularly countries like Taiwan, South Korea, China, and Japan, currently leads the growth in the CMP consumable market. This dominance is due to the concentration of major semiconductor manufacturing foundries and significant ongoing investments in expanding fabrication capacities and advanced process technologies within these nations.

What are the key challenges faced by CMP consumable manufacturers?

Key challenges for CMP consumable manufacturers include the need to achieve ultra-high uniformity and defectivity control at shrinking process nodes, intense cost pressure from semiconductor manufacturers, and the rapid pace of technological obsolescence demanding continuous R&D investment. Additionally, managing hazardous waste and complying with stringent environmental regulations present significant operational challenges.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted