Cloud Object Storage Market

Cloud Object Storage Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706360 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

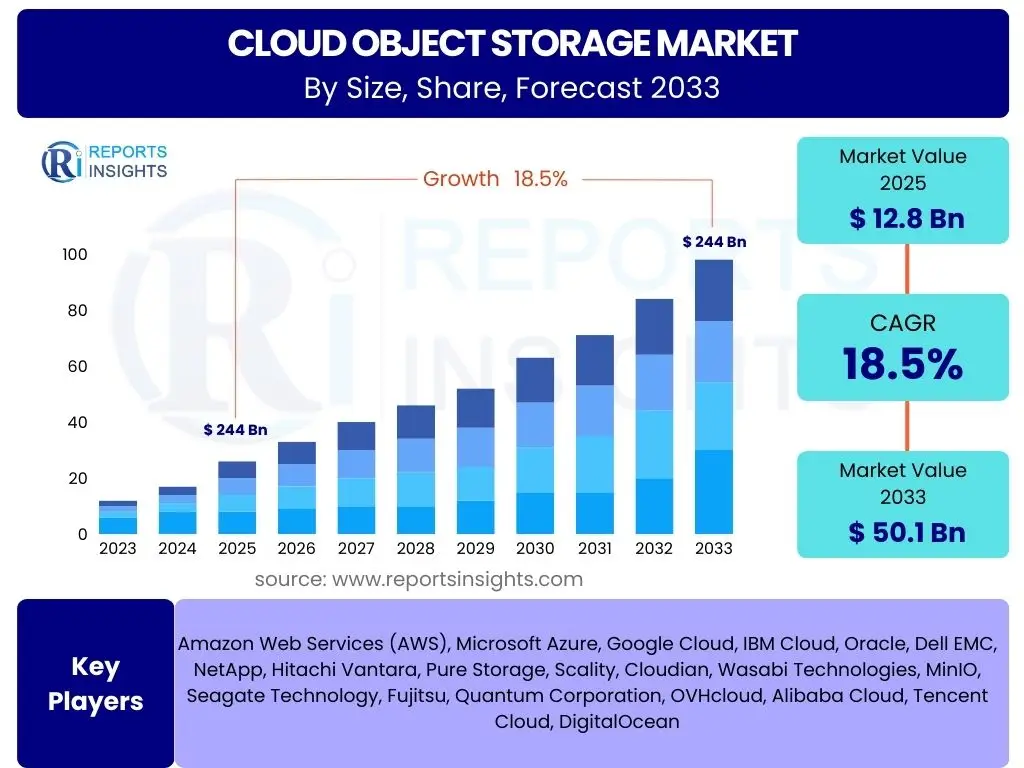

Cloud Object Storage Market Size

According to Reports Insights Consulting Pvt Ltd, The Cloud Object Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 12.8 billion in 2025 and is projected to reach USD 50.1 billion by the end of the forecast period in 2033.

Key Cloud Object Storage Market Trends & Insights

Users frequently inquire about the evolving landscape of cloud object storage, focusing on how technological advancements and shifting data demands are shaping its future. A primary area of interest revolves around the increasing adoption of hybrid and multi-cloud strategies, as organizations seek to optimize data placement for performance, cost, and compliance. Furthermore, the burgeoning volume of unstructured data, driven by IoT, big data analytics, and rich media content, necessitates scalable and cost-effective storage solutions, making object storage a critical component of modern data architectures.

Another significant trend gaining traction is the integration of advanced data management capabilities directly within object storage platforms. This includes features like intelligent tiering, enhanced data lifecycle management, and built-in analytics, which allow for more efficient data utilization and cost optimization. The emphasis on data sovereignty and resilience also drives demand for geo-distributed object storage and robust disaster recovery solutions. Enterprises are keenly observing how object storage evolves to support new application paradigms, including serverless computing and containerized environments, ensuring seamless data access and persistence.

- Proliferation of hybrid and multi-cloud architectures.

- Exponential growth of unstructured data from IoT and big data.

- Advancements in intelligent data tiering and lifecycle management.

- Increased demand for robust data security and compliance features.

- Integration with serverless and containerized application ecosystems.

- Rise of edge computing requiring distributed object storage capabilities.

AI Impact Analysis on Cloud Object Storage

Users frequently explore the symbiotic relationship between Artificial Intelligence (AI) and cloud object storage, particularly how AI advancements are both leveraging and transforming storage paradigms. Common questions revolve around the types of data AI processes and how object storage effectively handles the massive, diverse, and often unstructured datasets required for AI training and inferencing. AI's reliance on vast amounts of data, coupled with its need for high availability and scalable access, positions cloud object storage as an ideal foundational infrastructure due to its inherent scalability, durability, and cost-effectiveness for bulk data storage.

The impact of AI extends beyond mere data housing; AI capabilities are increasingly being integrated into object storage services themselves, enabling smarter data management. This includes AI-powered metadata tagging, automated data classification, and predictive analytics for storage optimization and anomaly detection. Furthermore, AI workloads are driving the need for higher performance object storage, especially for immediate data access during model training, leading to innovations in data caching and accelerated transfer mechanisms. The security implications are also significant, with AI being employed for advanced threat detection and access control within object storage environments, ensuring data integrity and compliance.

- Cloud object storage serves as a primary repository for AI training data.

- AI drives demand for scalable and cost-efficient unstructured data storage.

- AI-powered features enhance data management within object storage (e.g., metadata, classification).

- Performance demands from AI workloads influence object storage architecture.

- AI contributes to advanced security and compliance in object storage.

- Enables data lakes and analytics platforms foundational for AI initiatives.

Key Takeaways Cloud Object Storage Market Size & Forecast

User inquiries concerning the Cloud Object Storage market forecast highlight a strong interest in understanding the core factors driving its projected growth and the strategic implications for businesses. A primary takeaway is the persistent and accelerating growth of digital data, particularly unstructured formats, which intrinsically favors the scalable and cost-effective nature of object storage over traditional file or block storage. This fundamental driver is expected to sustain high CAGR throughout the forecast period, making object storage an indispensable component of enterprise IT strategies.

Another crucial insight is the increasing maturity and feature richness of cloud object storage services, moving beyond simple data repositories to offer integrated data lifecycle management, analytics capabilities, and enhanced security features. This evolution addresses complex enterprise needs, fostering broader adoption across diverse industries. The market forecast also underscores the significant role of hybrid and multi-cloud strategies, with object storage providing the necessary flexibility and interoperability across various deployment models. This flexibility, coupled with competitive pricing models, will continue to drive market expansion and innovation.

- Market size projected to reach USD 50.1 billion by 2033, indicating robust growth.

- Unstructured data growth remains a primary growth accelerator.

- Maturing services with advanced features enhance enterprise appeal.

- Hybrid and multi-cloud strategies are key adoption drivers.

- Cost efficiency and scalability are fundamental competitive advantages.

- Strategic importance for AI, big data, and IoT applications.

Cloud Object Storage Market Drivers Analysis

The Cloud Object Storage market is fundamentally driven by the exponential growth of digital data, particularly unstructured data generated from diverse sources such as social media, IoT devices, video surveillance, and enterprise applications. Traditional storage solutions often struggle to manage this scale and variety efficiently, making object storage, with its flat architecture and virtually unlimited scalability, an ideal solution. Organizations are increasingly recognizing the cost advantages and operational simplicity offered by object storage, especially for archive, backup, and data lake initiatives, which further propels its adoption.

Another significant driver is the widespread adoption of cloud-native application development and the increasing shift towards hybrid and multi-cloud environments. Cloud object storage seamlessly integrates with these modern architectural patterns, providing a highly available, durable, and accessible repository for application data. The demand for robust disaster recovery solutions, long-term data retention, and compliance archiving also contributes significantly, as object storage offers inherent data durability and advanced lifecycle management features that meet stringent regulatory requirements. Furthermore, the expansion of big data analytics and AI/ML workloads, which require massive datasets, directly fuels the demand for scalable object storage platforms.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Explosive Growth of Unstructured Data | +5.5% | Global, particularly North America, APAC | Long-term (2025-2033) |

| Rising Adoption of Cloud-Native Applications and Hybrid Cloud Strategies | +4.8% | Global, strong in North America, Europe | Mid-term (2025-2030) |

| Increasing Demand for Cost-Effective and Scalable Storage Solutions | +4.2% | Global | Long-term (2025-2033) |

| Enhanced Data Security and Compliance Requirements | +3.9% | Global, especially Europe (GDPR), North America | Mid to Long-term (2025-2033) |

| Proliferation of Big Data, AI, and IoT Workloads | +4.5% | Global, significant in APAC, North America | Long-term (2025-2033) |

Cloud Object Storage Market Restraints Analysis

Despite its significant advantages, the Cloud Object Storage market faces several restraints that could temper its growth trajectory. One key restraint is the complexity associated with data migration from legacy systems to object storage, especially for large, existing datasets. This process can be time-consuming, expensive, and may involve significant downtime, deterring some enterprises from making the full transition. Additionally, while object storage excels at scalability and cost-efficiency for large volumes of unstructured data, it may not be suitable for all types of workloads, particularly those requiring low-latency, high-transactional performance or strict file system semantics, which can lead to limited applicability in certain niche scenarios.

Another notable restraint is vendor lock-in concerns, particularly with major public cloud providers. While open standards exist, migrating large datasets between different object storage providers can be challenging due to API incompatibilities, data transfer costs, and the re-engineering of applications designed for a specific platform. This concern can lead organizations to diversify their storage solutions or proceed cautiously with large-scale object storage deployments. Furthermore, the perceived or actual complexity in managing data lifecycle policies, access controls, and security across vast object storage environments, especially in hybrid or multi-cloud setups, can pose a barrier for organizations with limited IT resources or expertise.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Migration Challenges from Legacy Systems | -2.1% | Global, particularly Mature Markets | Mid-term (2025-2028) |

| Performance Limitations for Certain Workloads (e.g., high-transactional) | -1.8% | Global | Long-term (2025-2033) |

| Vendor Lock-in Concerns with Public Cloud Providers | -2.5% | Global, strong in North America, Europe | Long-term (2025-2033) |

| Complexity in Data Management and Security for Hybrid/Multi-Cloud | -1.9% | Global | Mid-term (2025-2030) |

| Initial Cost of Integration and Training for New Deployments | -1.5% | Emerging Markets | Short-term (2025-2027) |

Cloud Object Storage Market Opportunities Analysis

The Cloud Object Storage market is poised for significant opportunities driven by emerging technologies and evolving enterprise needs. A major opportunity lies in the continued proliferation of edge computing, where vast amounts of data are generated closer to the source, requiring local object storage capabilities for immediate processing before selective transfer to central clouds. This distributed architecture necessitates robust object storage solutions that can operate efficiently at the edge, offering synchronization and integration with core cloud platforms. The increasing adoption of serverless computing and containerization also presents a ripe opportunity, as these ephemeral application environments require highly scalable and accessible data persistence layers, which object storage is inherently designed to provide.

Furthermore, the burgeoning market for advanced analytics, artificial intelligence, and machine learning creates substantial demand for large, accessible data lakes built upon object storage. As organizations seek to derive deeper insights from their unstructured data, the ability of object storage to cost-effectively store and serve these massive datasets becomes a critical enabler. Opportunities also exist in vertical-specific solutions, tailoring object storage offerings with industry-specific compliance, security, and integration features. This includes sectors such as healthcare for medical imaging, media and entertainment for content archives, and financial services for regulatory data retention, where specialized data handling requirements can be met by tailored object storage services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Edge Computing and IoT Data Storage | +3.2% | Global, particularly APAC, North America | Long-term (2025-2033) |

| Growing Adoption of Serverless and Containerized Workloads | +2.8% | Global | Mid-term (2025-2030) |

| Demand for Data Lakes for AI/ML and Big Data Analytics | +3.5% | Global, strong in North America, Europe | Long-term (2025-2033) |

| Development of Industry-Specific Object Storage Solutions | +2.5% | Global, targeted by industry | Mid-term (2025-2030) |

| Increased Focus on Data Archiving and Long-term Retention | +2.0% | Global | Long-term (2025-2033) |

Cloud Object Storage Market Challenges Impact Analysis

The Cloud Object Storage market faces several challenges that require strategic navigation by providers and users. One significant challenge is ensuring robust data security and compliance across diverse cloud environments, especially given the sensitive nature of data being stored. As data volumes grow and regulations evolve (e.g., GDPR, CCPA), maintaining strict access controls, encryption, and audit trails becomes increasingly complex, demanding sophisticated security features and expertise. Data governance and lifecycle management also pose challenges, particularly in hybrid and multi-cloud scenarios, where consistent policy application and data visibility across disparate storage locations can be difficult to achieve.

Another challenge stems from the perceived complexity of integrating object storage with existing enterprise applications and workflows. While many modern applications are built to leverage object storage APIs, integrating older, monolithic applications may require significant refactoring or the use of gateway solutions, adding to deployment time and cost. Furthermore, managing data egress costs from public cloud object storage providers remains a concern for enterprises, as these charges can accumulate rapidly with high data retrieval volumes, potentially eroding the initial cost benefits. This necessitates careful planning and optimization strategies to control operational expenditures, especially for applications with dynamic data access patterns.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Data Security and Regulatory Compliance | -2.3% | Global, particularly Europe, North America | Long-term (2025-2033) |

| Data Egress Costs from Public Cloud Providers | -2.6% | Global | Long-term (2025-2033) |

| Complexity of Integrating with Legacy Applications | -1.7% | Global, especially Traditional Enterprises | Mid-term (2025-2030) |

| Managing Data Governance and Lifecycle Across Multi-Cloud | -1.9% | Global | Long-term (2025-2033) |

| Availability of Skilled Professionals to Manage Object Storage Solutions | -1.5% | Global, particularly Emerging Markets | Mid-term (2025-2030) |

Cloud Object Storage Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Cloud Object Storage market, offering insights into its current size, historical performance, and future growth projections. The scope encompasses a detailed examination of key market trends, drivers, restraints, opportunities, and challenges that are shaping the industry landscape. The report also delivers a thorough AI impact analysis, illustrating how artificial intelligence is both a catalyst and a beneficiary of advancements in cloud object storage, influencing data management, security, and application development.

Furthermore, the study includes extensive market segmentation, dissecting the market by component, deployment model, organization size, industry vertical, and region, providing granular insights into specific market dynamics. A competitive landscape analysis profiles leading market players, offering insights into their strategies, product portfolios, and market positioning. The report serves as a strategic tool for stakeholders, enabling them to make informed decisions by understanding market dynamics, identifying growth avenues, and mitigating potential risks across the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 billion |

| Market Forecast in 2033 | USD 50.1 billion |

| Growth Rate | 18.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM Cloud, Oracle, Dell EMC, NetApp, Hitachi Vantara, Pure Storage, Scality, Cloudian, Wasabi Technologies, MinIO, Seagate Technology, Fujitsu, Quantum Corporation, OVHcloud, Alibaba Cloud, Tencent Cloud, DigitalOcean |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cloud Object Storage market is segmented to provide a granular view of its diverse landscape, categorized primarily by component, deployment model, organization size, and industry vertical. This detailed segmentation allows for a precise understanding of adoption patterns and growth opportunities across different market dimensions. Solutions, encompassing primary storage, backup and recovery, archiving, and disaster recovery, represent the core offerings, reflecting the broad utility of object storage across various data management needs. Services, including managed and professional services, complement these solutions by providing expertise in implementation, optimization, and ongoing support, crucial for complex enterprise deployments.

Deployment models further differentiate the market into public, private, and hybrid cloud, indicating the flexibility with which organizations can implement object storage based on their infrastructure preferences, security requirements, and cost considerations. Public cloud remains dominant due to its scalability and ease of use, while private and hybrid models cater to specific regulatory or control needs. Organization size distinguishes adoption patterns between Small and Medium-sized Enterprises (SMEs) and Large Enterprises, highlighting varying resource capacities and scale of data. Lastly, the industry vertical segmentation, including BFSI, Healthcare, IT & Telecommunication, Media & Entertainment, and others, illustrates how sector-specific data requirements and compliance mandates drive tailored object storage solutions.

- Component:

- Solutions (Primary Storage, Backup and Recovery, Archiving, Disaster Recovery)

- Services (Managed Services, Professional Services)

- Deployment Model:

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Organization Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- Industry Vertical:

- BFSI

- Healthcare & Life Sciences

- IT & Telecommunication

- Media & Entertainment

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Education

- Others

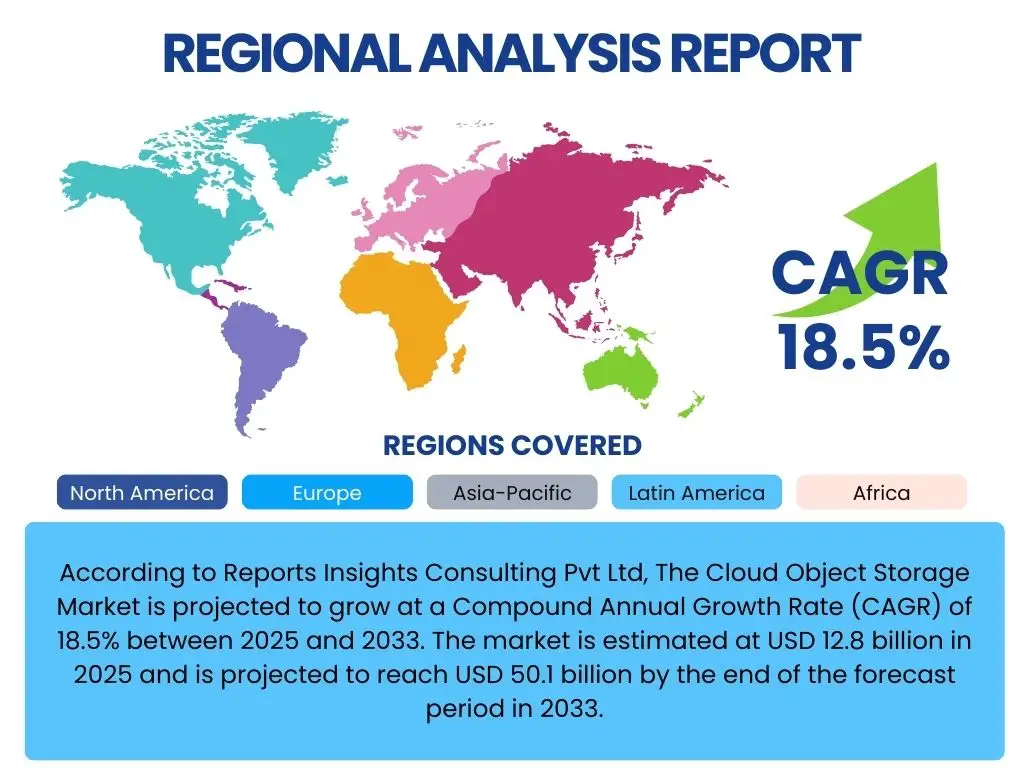

Regional Highlights

- North America: This region dominates the Cloud Object Storage market, primarily driven by the presence of major cloud service providers, early adoption of advanced technologies, and a high concentration of large enterprises with significant data storage needs. Strong regulatory frameworks also push the adoption of compliant and secure object storage solutions for various industries. The robust IT infrastructure and continuous investment in cloud technologies further solidify its leading position.

- Europe: Europe represents a substantial market share, influenced by stringent data privacy regulations like GDPR, which necessitate robust and compliant data storage solutions. The region shows increasing adoption of hybrid cloud models and a growing focus on data sovereignty, fueling demand for both public and private cloud object storage. Countries like Germany, the UK, and France are key contributors to market growth.

- Asia Pacific (APAC): APAC is projected to exhibit the highest growth rate due to rapid digital transformation across industries, increasing internet penetration, and the burgeoning volume of data generated by a large population base. Emerging economies like India and China are witnessing massive investments in cloud infrastructure and the accelerated adoption of cloud-native applications, driving significant demand for scalable object storage. The rise of IoT and AI initiatives further boosts market expansion.

- Latin America: This region is characterized by growing cloud adoption among SMEs and large enterprises seeking to modernize their IT infrastructure and achieve cost efficiencies. Increasing awareness of data backup, disaster recovery, and compliance requirements drives the market. Brazil and Mexico are leading the adoption curve, with investments in cloud services picking up pace.

- Middle East & Africa (MEA): The MEA region is experiencing steady growth, fueled by government-led digital initiatives, diversification from oil-dependent economies, and increasing foreign investment in technology infrastructure. Countries like UAE and Saudi Arabia are investing heavily in data centers and cloud services, leading to a rise in demand for secure and scalable object storage solutions across various sectors, including finance and government.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cloud Object Storage Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM Cloud

- Oracle

- Dell EMC

- NetApp

- Hitachi Vantara

- Pure Storage

- Scality

- Cloudian

- Wasabi Technologies

- MinIO

- Seagate Technology

- Fujitsu

- Quantum Corporation

- OVHcloud

- Alibaba Cloud

- Tencent Cloud

- DigitalOcean

Frequently Asked Questions

What is cloud object storage?

Cloud object storage is a method of storing data as objects in the cloud. Each object contains the data, metadata, and a unique identifier, allowing for massive scalability and cost-effective storage of unstructured data accessed via APIs over the internet.

What are the primary benefits of using cloud object storage?

Key benefits include virtually limitless scalability, high durability and availability, cost-effectiveness for large data volumes, built-in data lifecycle management, and global accessibility, making it ideal for backups, archives, and big data analytics.

How does AI impact cloud object storage?

AI significantly impacts cloud object storage by driving demand for massive unstructured datasets for training, enabling intelligent data management features within storage platforms (e.g., automated tagging), and influencing performance requirements for AI workloads.

Which industries are adopting cloud object storage most rapidly?

Industries rapidly adopting cloud object storage include Media & Entertainment (for content delivery), Healthcare (for medical imaging and patient data), IT & Telecommunications (for backups and archives), and BFSI (for compliance and data retention).

What are the main challenges in adopting cloud object storage?

Main challenges include data migration complexity from legacy systems, potential vendor lock-in, managing egress costs from public clouds, ensuring robust data security and compliance, and integrating with older applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted