Backtesting Software Market

Backtesting Software Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706473 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

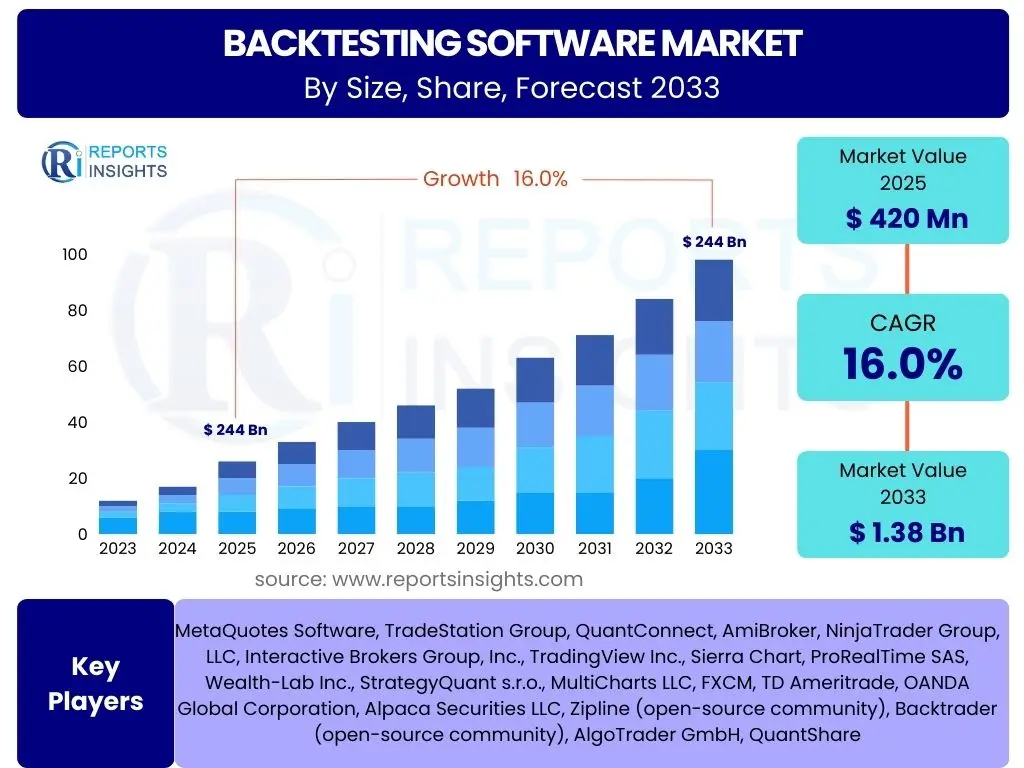

Backtesting Software Market Size

According to Reports Insights Consulting Pvt Ltd, The Backtesting Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.0% between 2025 and 2033. The market is estimated at USD 420 Million in 2025 and is projected to reach USD 1.38 Billion by the end of the forecast period in 2033.

Key Backtesting Software Market Trends & Insights

User inquiries into Backtesting Software market trends frequently center on the evolution of analytical capabilities, accessibility, and integration within broader trading ecosystems. The market is increasingly characterized by a shift towards more sophisticated, data-driven solutions that cater to both institutional and individual traders. There is a growing demand for platforms that offer not just historical testing but also forward-looking simulations, enhanced visualization, and seamless integration with live trading environments.

Another significant trend involves the democratization of complex financial tools, making advanced backtesting capabilities available to a wider audience, including retail investors. Cloud-based solutions are gaining traction due to their scalability, accessibility, and reduced infrastructure requirements, fostering innovation and competition. Furthermore, the emphasis on robust data quality and the ability to process large datasets efficiently is paramount, as users seek to minimize errors and maximize the reliability of their trading strategies.

- Increased adoption of cloud-based backtesting platforms for scalability and accessibility.

- Integration of advanced analytics and machine learning techniques for predictive modeling.

- Rising demand for multi-asset class backtesting capabilities.

- Enhanced user interfaces and low-code/no-code solutions for broader accessibility.

- Focus on real-time data feeds and high-fidelity historical data for accurate simulations.

AI Impact Analysis on Backtesting Software

Common user questions regarding AI's impact on Backtesting Software often explore its potential to revolutionize strategy development, optimize existing algorithms, and automate parts of the testing process. Users are keen to understand how AI can move backtesting beyond mere historical validation to predictive modeling and adaptive strategy generation. The primary expectation is that AI will significantly enhance the efficiency and accuracy of identifying profitable trading strategies, reducing the manual effort involved in iterative testing.

AI's influence extends to enabling more complex and nuanced analysis of market data, identifying patterns that human analysts might miss, and dynamically adjusting strategies based on evolving market conditions. This capability allows for the development of adaptive trading systems that can learn and improve over time, potentially leading to more robust and resilient strategies. However, concerns also exist around the interpretability of AI-generated strategies ("black box" problem), the ethical implications of autonomous trading, and the substantial computational resources required for advanced AI models.

Despite these challenges, the integration of AI is widely seen as a transformative force, pushing the boundaries of what backtesting can achieve. It promises to deliver higher levels of optimization, predictive power, and automation, thereby empowering traders with more sophisticated tools for risk management and performance enhancement. The ongoing development of AI algorithms tailored for financial markets is set to redefine the scope and capabilities of future backtesting software.

- Enhanced predictive accuracy and pattern recognition in market data.

- Automated generation and optimization of trading strategies.

- Development of adaptive and self-learning algorithms for dynamic market conditions.

- Improved risk management through AI-driven scenario analysis.

- Increased computational efficiency for processing vast datasets and complex simulations.

Key Takeaways Backtesting Software Market Size & Forecast

Analysis of user inquiries about key takeaways from the Backtesting Software market size and forecast consistently points to a clear understanding of its robust growth trajectory and increasing strategic importance. Users recognize the market's expansion as a direct reflection of the growing complexity in financial markets and the escalating need for empirical validation of trading strategies. The market's projected growth indicates a sustained demand for sophisticated tools that can mitigate risk and optimize returns in volatile environments.

A significant takeaway is the ongoing shift towards more technologically advanced solutions, driven by innovations in cloud computing, big data analytics, and artificial intelligence. This technological evolution is not only expanding the market but also democratizing access to powerful analytical capabilities, making professional-grade tools available to a broader spectrum of users, from large financial institutions to individual retail traders. The forecast underscores the essential role backtesting software plays in fostering data-driven decision-making and enhancing algorithmic trading capabilities across the financial industry.

- The Backtesting Software market exhibits significant growth, driven by increasing financial market complexity.

- Technological advancements, particularly AI and cloud computing, are key enablers of market expansion.

- Growing adoption across both institutional and retail segments signals broader market penetration.

- The software is pivotal for validating trading strategies, managing risk, and optimizing portfolio performance.

- Market evolution is characterized by a demand for greater accuracy, speed, and integration capabilities.

Backtesting Software Market Drivers Analysis

The proliferation of algorithmic and high-frequency trading strategies serves as a primary driver for the Backtesting Software market. As financial markets become increasingly automated, the imperative to rigorously test and validate complex algorithms against historical data becomes paramount. This ensures that strategies are robust, reliable, and capable of performing under various market conditions before deployment, minimizing potential losses and optimizing returns.

Another significant driver is the increasing participation of retail investors in financial markets, coupled with their growing sophistication. Accessible online brokerage platforms and educational resources have empowered individual traders to adopt more advanced trading techniques. Consequently, there is a heightened demand for user-friendly yet powerful backtesting tools that enable retail investors to develop and refine their own strategies effectively, without requiring extensive programming knowledge.

Furthermore, heightened market volatility and the need for stringent risk management across all trading entities contribute substantially to market growth. Financial institutions and independent traders alike seek to stress-test their strategies under diverse historical scenarios, including periods of extreme volatility, to understand potential vulnerabilities and manage risk exposure. Robust backtesting capabilities are indispensable for comprehensive risk assessment, compliance with internal guidelines, and overall portfolio resilience.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rise of Algorithmic and High-Frequency Trading | +0.7% | Global, particularly North America, Europe, Asia Pacific | Short-term to Long-term |

| Increased Retail Investor Participation and Sophistication | +0.5% | North America, Asia Pacific, Europe | Mid-term |

| Growing Need for Robust Risk Management and Strategy Validation | +0.6% | Global | Short-term to Long-term |

| Advancements in Data Analytics and Computing Power | +0.4% | Global | Mid-term to Long-term |

Backtesting Software Market Restraints Analysis

One of the primary restraints in the Backtesting Software market is the challenge associated with data availability and quality. Accurate and comprehensive historical market data, especially high-frequency data, is often expensive, difficult to obtain, and can suffer from issues like survivorship bias, look-ahead bias, or inconsistent formatting. Poor data quality can lead to misleading backtesting results, undermining the reliability of strategy validation and eroding user confidence in the software.

Another significant barrier is the high computational requirements and complexity associated with running sophisticated backtesting simulations. Advanced strategies, particularly those involving machine learning or multi-asset analysis, demand substantial processing power and memory, which can be prohibitive for individual users or smaller firms without access to cloud infrastructure or high-performance computing resources. This complexity can also translate into longer simulation times, limiting the efficiency of iterative strategy development.

Furthermore, the steep learning curve and the need for specialized quantitative skills pose a restraint on broader market adoption. While some platforms offer user-friendly interfaces, effectively utilizing backtesting software for complex strategy development and interpretation of results often requires a deep understanding of financial markets, statistical methods, and programming languages. This skill gap limits the potential user base and necessitates significant investment in training or hiring specialized talent.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Availability, Quality, and Biases | -0.4% | Global | Short-term to Mid-term |

| High Computational Requirements and Infrastructure Costs | -0.3% | Global, particularly for smaller firms | Mid-term |

| Steep Learning Curve and Need for Specialized Skills | -0.3% | Global | Long-term |

| Over-optimization and Curve Fitting Risks | -0.2% | Global | Short-term to Mid-term |

Backtesting Software Market Opportunities Analysis

The continued expansion of cloud computing presents a significant opportunity for the Backtesting Software market. Cloud-based platforms offer unparalleled scalability, allowing users to run complex simulations with vast datasets without the need for extensive local hardware investments. This democratizes access to powerful backtesting capabilities for a wider range of users, from individual traders to large institutions, facilitating faster iteration and broader experimentation with trading strategies. The pay-as-you-go model of cloud services also reduces upfront costs, making advanced tools more accessible.

Another major opportunity lies in the deeper integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities into backtesting platforms. AI/ML can enhance strategy discovery, optimize existing algorithms, and identify non-obvious patterns in market data, leading to more robust and adaptive trading systems. The development of AI-driven tools for dynamic portfolio rebalancing and predictive risk analysis will create new functionalities and user segments, expanding the utility and value proposition of backtesting software beyond traditional historical simulations.

Furthermore, the growth of emerging markets and the increasing sophistication of financial instruments within these regions offer new avenues for market expansion. As capital markets in Asia Pacific, Latin America, and Africa mature, there will be a rising demand for reliable backtesting solutions to support local trading strategies and regulatory compliance. Tailored solutions that address specific regional market structures, data availability, and asset classes represent a lucrative opportunity for market players to diversify their offerings and penetrate untapped customer bases.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud-Based Backtesting Solutions | +0.8% | Global | Short-term to Long-term |

| Integration of AI and Machine Learning Capabilities | +0.7% | Global | Mid-term to Long-term |

| Development of Multi-Asset Class and Cross-Market Backtesting | +0.6% | Global | Mid-term |

| Growth in Emerging Markets and Niche Financial Instruments | +0.5% | Asia Pacific, Latin America, Africa | Long-term |

Backtesting Software Market Challenges Impact Analysis

One significant challenge facing the Backtesting Software market is the risk of overfitting and survivorship bias. Overfitting occurs when a trading strategy is excessively optimized to historical data, leading to excellent simulated performance but poor real-world results. Survivorship bias arises when a dataset only includes assets that have survived to the present, ignoring those that failed or were delisted, creating an unrealistic view of historical performance. Addressing these biases requires sophisticated methodologies and careful data handling, posing a constant challenge for software developers and users alike to ensure the validity of backtest results.

Another formidable challenge is keeping pace with rapidly evolving market conditions and the introduction of new financial instruments. Market dynamics, regulatory frameworks, and technological landscapes are constantly shifting, requiring backtesting software to be continuously updated to reflect these changes accurately. Integrating new data types, accommodating novel trading venues, and adapting to changes in liquidity or microstructure demand agile development cycles and significant investment in research and development, which can strain resources for providers.

Furthermore, ensuring the integrity and authenticity of historical data, especially concerning high-frequency and tick-level data, presents a complex challenge. Data providers must guarantee that their feeds accurately represent market conditions at the time, free from errors, gaps, or adjustments that could distort backtest outcomes. Users face the challenge of verifying data veracity, and the financial implications of flawed data can be severe, making data integrity a critical concern that impacts user trust and software reliability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Mitigating Overfitting and Survivorship Bias | -0.3% | Global | Short-term to Long-term |

| Keeping Pace with Evolving Market Conditions and New Instruments | -0.2% | Global | Short-term |

| Ensuring Data Integrity and High-Fidelity Historical Data | -0.2% | Global | Mid-term |

| Regulatory Scrutiny and Compliance Requirements | -0.1% | North America, Europe | Mid-term |

Backtesting Software Market - Updated Report Scope

This report provides an in-depth analysis of the global Backtesting Software market, encompassing comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges. It segments the market by deployment model, application, end-user, and asset class, offering a detailed understanding of key trends and regional dynamics. The report also highlights the competitive landscape, profiling key market players and their strategic initiatives to provide a holistic view of the industry's current state and future prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 420 Million |

| Market Forecast in 2033 | USD 1.38 Billion |

| Growth Rate | 16.0% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | MetaQuotes Software, TradeStation Group, QuantConnect, AmiBroker, NinjaTrader Group, LLC, Interactive Brokers Group, Inc., TradingView Inc., Sierra Chart, ProRealTime SAS, Wealth-Lab Inc., StrategyQuant s.r.o., MultiCharts LLC, FXCM, TD Ameritrade, OANDA Global Corporation, Alpaca Securities LLC, Zipline (open-source community), Backtrader (open-source community), AlgoTrader GmbH, QuantShare |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Backtesting Software market is comprehensively segmented to provide granular insights into its diverse components and evolving user needs. These segmentations allow for a precise understanding of adoption patterns, technological preferences, and growth opportunities across various deployment models, application areas, end-user categories, and asset classes. Analyzing these segments is crucial for identifying niche markets, tailoring product offerings, and formulating effective market entry strategies for both established and emerging players.

Understanding the demand drivers and specific requirements within each segment helps stakeholders to prioritize development efforts and allocate resources efficiently. For instance, the differing needs of retail investors versus institutional firms necessitate distinct feature sets and pricing models. Similarly, the complexities associated with backtesting various asset classes, such as cryptocurrencies compared to traditional equities, influence software design and data integration strategies. This detailed segmentation analysis reveals the multifaceted nature of the market and its potential for specialized solutions.

- By Deployment:

- On-premise: Traditional software installation on local servers or individual computers, favored by institutions requiring maximum data control and customization.

- Cloud-based: Software accessed via the internet, offering scalability, reduced infrastructure costs, and greater accessibility, appealing to both retail and institutional users.

- By Application:

- Algorithmic Trading: Core application for developing and validating automated trading strategies.

- Portfolio Management: Used to test portfolio rebalancing strategies and diversification techniques.

- Risk Management: Essential for stress-testing portfolios under various historical market scenarios to assess risk exposure.

- Strategy Development & Optimization: Broad application covering the iterative process of creating, testing, and refining trading rules.

- Others: Includes academic research, regulatory compliance testing, and educational purposes.

- By End-user:

- Retail Investors: Individual traders utilizing the software for personal strategy validation and improvement.

- Institutional Investors: Includes:

- Hedge Funds: For complex quantitative strategy development and high-frequency trading.

- Asset Management Firms: For long-term portfolio strategy testing and rebalancing.

- Prop Trading Firms: For rapid development and deployment of proprietary trading algorithms.

- Banks & Financial Institutions: For risk analysis, compliance, and large-scale quantitative research.

- By Asset Class:

- Equities: Testing strategies on stocks and equity derivatives.

- Forex: Analyzing currency pair trading strategies.

- Commodities: Backtesting strategies for raw materials like oil, gold, and agricultural products.

- Futures: Evaluating strategies for standardized contracts to buy or sell an asset at a predetermined price and date.

- Options: Complex strategies involving calls and puts.

- Cryptocurrencies: Emerging segment for digital asset trading strategy validation.

- Others: Includes bonds, indices, and other specialized financial instruments.

Regional Highlights

- North America: Dominates the Backtesting Software market, driven by advanced financial markets, high adoption of algorithmic trading, and the presence of numerous fintech innovations. The U.S. and Canada lead in technological advancements and institutional investment in sophisticated trading tools.

- Europe: Exhibits significant growth, propelled by robust regulatory frameworks demanding rigorous risk management and the increasing embrace of automated trading across key financial centers like London, Frankfurt, and Paris. Emphasis on data privacy and compliance is also a major factor.

- Asia Pacific (APAC): Emerging as the fastest-growing region, fueled by the rapid expansion of capital markets, increasing retail investor participation, and growing awareness of quantitative trading strategies in countries like China, India, Japan, and Australia. The region presents substantial opportunities for cloud-based and mobile-first backtesting solutions.

- Latin America: Showing nascent but steady growth, with increasing interest in financial technology and digital transformation within its developing economies. Brazil and Mexico are key markets where financial institutions and educated retail traders are exploring backtesting capabilities.

- Middle East and Africa (MEA): Represents a smaller but evolving market, with gradual adoption driven by efforts to modernize financial infrastructure and attract foreign investment. The UAE and Saudi Arabia are investing in fintech, creating new demand for sophisticated trading and analysis tools.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Backtesting Software Market.- MetaQuotes Software

- TradeStation Group

- QuantConnect

- AmiBroker

- NinjaTrader Group, LLC

- Interactive Brokers Group, Inc.

- TradingView Inc.

- Sierra Chart

- ProRealTime SAS

- Wealth-Lab Inc.

- StrategyQuant s.r.o.

- MultiCharts LLC

- FXCM

- TD Ameritrade

- OANDA Global Corporation

- Alpaca Securities LLC

- Zipline (open-source community)

- Backtrader (open-source community)

- AlgoTrader GmbH

- QuantShare

Frequently Asked Questions

What is backtesting software?

Backtesting software is a tool that allows traders and investors to simulate the performance of a trading strategy using historical market data. It applies the rules of a chosen strategy to past price movements and conditions, generating hypothetical results that indicate how the strategy would have performed. This process helps users to evaluate a strategy's profitability, risk, and consistency before risking real capital, providing crucial insights into its viability and potential weaknesses.

Who primarily uses backtesting software?

Backtesting software is utilized by a wide range of market participants. This includes institutional investors such as hedge funds, asset management firms, and proprietary trading desks for developing and validating complex quantitative strategies. Retail investors and individual traders also extensively use these tools to refine their personal trading systems, manage risk, and make data-driven decisions. Additionally, academic researchers and financial analysts leverage backtesting for market research and theoretical modeling.

What are the key benefits of using backtesting software?

The primary benefits of backtesting software include the ability to rigorously validate trading strategies against historical performance, thereby reducing risk by identifying potential flaws before live deployment. It allows for the optimization of strategy parameters, leading to improved profitability and efficiency. Users can also gain deeper insights into their strategy's behavior under various market conditions, assess risk metrics like drawdown and volatility, and build confidence in their trading approach through empirical evidence rather than relying on intuition alone.

What are the main challenges associated with backtesting?

Key challenges in backtesting include ensuring the accuracy and completeness of historical data, as poor data quality can lead to misleading results. The risk of "overfitting," where a strategy performs well on historical data but poorly in live trading due to excessive optimization, is a significant concern. Other challenges involve accounting for transaction costs, market impact, slippage, and handling biases such as survivorship bias or look-ahead bias, all of which can distort the true performance of a strategy.

How is AI impacting backtesting software?

AI is profoundly impacting backtesting software by enabling more sophisticated strategy development and optimization. AI algorithms can identify complex patterns in vast datasets that are invisible to human analysis, leading to novel strategy generation. They can also dynamically adapt strategies to changing market conditions and enhance predictive modeling for more accurate simulations. This integration allows for automated strategy refinement, advanced risk assessment, and the potential for developing self-learning trading systems, pushing the boundaries of what traditional backtesting can achieve.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted