Cloud Native SIEM Market

Cloud Native SIEM Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708260 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Cloud Native SIEM Market Size

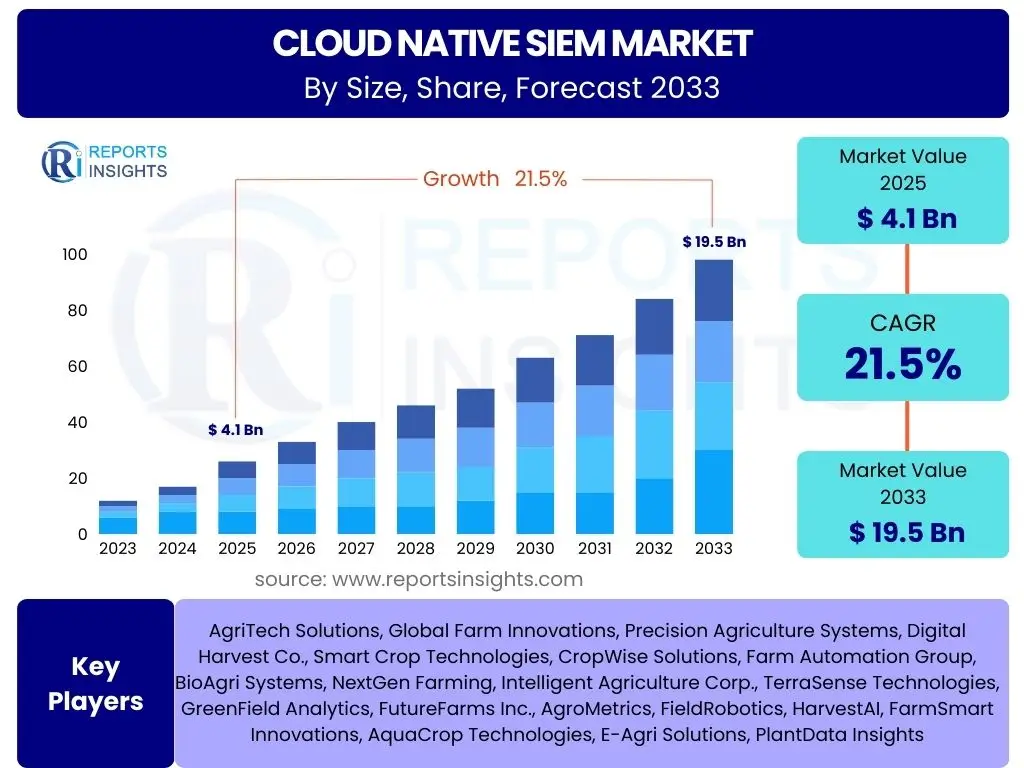

According to Reports Insights Consulting Pvt Ltd, The Cloud Native SIEM Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 4.1 Billion in 2025 and is projected to reach USD 19.5 Billion by the end of the forecast period in 2033.

Key Cloud Native SIEM Market Trends & Insights

The Cloud Native SIEM market is undergoing significant transformation, driven by the pervasive shift towards cloud infrastructure and the escalating complexity of cyber threats. Users are keenly interested in how these solutions offer enhanced scalability, agility, and cost-efficiency compared to traditional SIEM deployments, particularly in hybrid and multi-cloud environments. There is a strong focus on capabilities such as real-time threat detection, advanced analytics powered by artificial intelligence and machine learning, and seamless integration with other cloud-native security tools.

Emerging trends indicate a growing demand for simplified management, automation of security operations, and the consolidation of security data from disparate cloud services. Organizations are increasingly seeking platforms that can provide comprehensive visibility across their entire digital estate, enabling proactive threat hunting and accelerated incident response. Furthermore, the convergence of SIEM with Extended Detection and Response (XDR) capabilities and Security Orchestration, Automation, and Response (SOAR) functionalities is a key area of interest, promising more cohesive and automated security workflows.

- Accelerated migration to cloud-native architectures for enhanced scalability and flexibility.

- Integration of advanced Artificial Intelligence (AI) and Machine Learning (ML) for superior threat detection and anomaly identification.

- Convergence with XDR platforms to provide unified visibility and automated response across multiple security layers.

- Emphasis on real-time data ingestion and analytics for proactive security posture management.

- Increased demand for Security Orchestration, Automation, and Response (SOAR) capabilities within SIEM platforms.

- Focus on cost optimization and operational efficiency through subscription-based, consumption-driven pricing models.

- Expansion of threat intelligence integration to enrich contextual awareness and accelerate investigations.

- Growing adoption in Small and Medium-sized Enterprises (SMEs) due to ease of deployment and managed service options.

- Development of solutions specifically tailored for multi-cloud and hybrid cloud environments.

- Heightened importance of data privacy and compliance features in cloud-native deployments.

AI Impact Analysis on Cloud Native SIEM

User inquiries frequently highlight the transformative potential of AI in Cloud Native SIEM, focusing on its ability to enhance detection capabilities, reduce alert fatigue, and automate response actions. AI and Machine Learning (ML) are pivotal in processing the massive volumes of security data generated in cloud environments, identifying subtle patterns indicative of sophisticated threats that might elude rule-based systems. Concerns often revolve around the accuracy of AI models, the potential for false positives or negatives, and the need for explainable AI to ensure transparency and trust in automated decisions.

The integration of AI into Cloud Native SIEM platforms is fundamentally changing how security teams operate, shifting from reactive analysis to proactive threat intelligence and predictive security. Users expect AI to not only improve the speed and precision of threat identification but also to intelligently prioritize alerts, correlate disparate events across cloud services, and recommend or initiate automated remediation workflows. The goal is to elevate security operations center (SOC) efficiency, allowing human analysts to focus on more complex strategic tasks rather than manual alert triage.

- Enhanced Threat Detection: AI/ML algorithms improve the accuracy and speed of identifying advanced persistent threats (APTs), zero-day exploits, and insider threats by analyzing behavioral anomalies and vast datasets.

- Reduced False Positives: Machine learning models can differentiate between legitimate activities and malicious events with greater precision, significantly lowering the volume of erroneous alerts and combating alert fatigue.

- Automated Incident Response: AI capabilities facilitate automated responses to detected threats, such as isolating compromised systems, blocking malicious IP addresses, or triggering containment protocols, thereby minimizing dwell time.

- Predictive Analytics: AI enables the prediction of potential security incidents by analyzing historical data and current trends, allowing organizations to proactively strengthen defenses.

- Behavioral Anomaly Detection: ML excels at establishing baselines for normal user and system behavior, quickly flagging deviations that may indicate compromise or malicious intent.

- Contextual Enrichment: AI algorithms can correlate data from various sources, enriching alerts with crucial context to provide a clearer picture of an attack, including its scope and potential impact.

- Data Processing Efficiency: AI efficiently processes and analyzes petabytes of log and event data from diverse cloud sources, making it feasible to manage the scale and velocity of modern cloud environments.

- Dynamic Threat Intelligence: AI can continuously learn from new threat intelligence feeds and adapt its detection models, ensuring the SIEM remains effective against evolving attack techniques.

Key Takeaways Cloud Native SIEM Market Size & Forecast

The Cloud Native SIEM market is poised for substantial and sustained growth, primarily driven by the imperative for robust security solutions that can seamlessly integrate with and protect increasingly complex cloud environments. Organizations are recognizing that traditional, on-premise SIEMs often fall short in providing the scalability, agility, and comprehensive visibility required for modern cloud-first strategies. This understanding is accelerating the shift towards cloud-native alternatives, which offer a more efficient and effective approach to managing security information and events at scale.

The forecast indicates a strong market expansion, underpinned by the continuous digital transformation efforts of enterprises across all sizes and industries. Key factors contributing to this growth include the escalating volume and sophistication of cyberattacks, stringent regulatory compliance requirements, and the desire for operational efficiency through automation and advanced analytics. The market is not just growing in size but also evolving in terms of capability, with a strong emphasis on AI/ML integration, XDR convergence, and real-time threat detection to meet the dynamic demands of cloud security.

- The market is experiencing robust double-digit growth, highlighting a strong industry-wide shift towards cloud-first security paradigms.

- Increasing adoption of multi-cloud and hybrid cloud strategies is a primary catalyst for Cloud Native SIEM demand.

- Advanced cyber threats and the need for real-time, scalable security analytics are critical drivers.

- Regulatory compliance and data governance requirements are compelling organizations to invest in modern SIEM solutions.

- Operational cost efficiencies and reduced infrastructure management complexities offered by cloud-native platforms are key吸引 factors.

- Integration of artificial intelligence and machine learning is becoming a standard feature, enhancing detection and response capabilities.

- The market will witness significant innovation in terms of threat intelligence, automation, and user experience.

- Small and medium-sized enterprises (SMEs) represent an expanding segment, leveraging the accessibility and managed services inherent to cloud-native solutions.

Cloud Native SIEM Market Drivers Analysis

The Cloud Native SIEM market is propelled by a confluence of critical factors responding to the evolving cybersecurity landscape. A primary driver is the accelerating migration of enterprise workloads and infrastructure to cloud environments. As organizations increasingly adopt multi-cloud and hybrid cloud strategies, the need for security information and event management solutions natively designed for these dynamic, distributed ecosystems becomes paramount, surpassing the capabilities of traditional on-premise SIEMs. This shift is not merely about location but about leveraging cloud elasticity, scalability, and integration.

Furthermore, the relentless increase in sophistication and volume of cyber threats serves as a powerful impetus for Cloud Native SIEM adoption. Organizations face a growing array of advanced persistent threats, ransomware, and zero-day exploits that necessitate real-time threat detection, advanced analytics, and automated response capabilities. Cloud Native SIEMs are inherently better positioned to process vast quantities of data from diverse cloud sources, apply machine learning for anomaly detection, and provide rapid insights crucial for mitigating modern cyber risks.

Lastly, stringent regulatory compliance mandates and data privacy laws across various industries and geographies are compelling enterprises to invest in robust security solutions. Cloud Native SIEM platforms offer enhanced auditing, reporting, and incident management features that help organizations meet requirements such as GDPR, HIPAA, PCI DSS, and various national cybersecurity frameworks. The ability to centralize security data, demonstrate comprehensive logging, and quickly respond to incidents is a significant factor driving investment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Cloud Adoption & Digital Transformation | +5.5% | Global, particularly North America, Europe, Asia Pacific | Short-term to Long-term (2025-2033) |

| Rising Sophistication & Volume of Cyber Threats | +4.8% | Global, across all industries | Short-term to Long-term (2025-2033) |

| Strict Regulatory Compliance & Data Governance Requirements | +3.2% | Europe (GDPR), North America (HIPAA, PCI DSS), Asia Pacific (local regulations) | Mid-term to Long-term (2026-2033) |

| Demand for Scalable, Real-time Security Analytics & Automation | +4.0% | Global, especially large enterprises & BFSI | Short-term to Mid-term (2025-2030) |

| Cost Efficiency & Operational Benefits over Traditional SIEM | +2.5% | Global, particularly for SMEs and cost-conscious organizations | Mid-term to Long-term (2026-2033) |

Cloud Native SIEM Market Restraints Analysis

Despite significant growth drivers, the Cloud Native SIEM market faces several notable restraints that could impede its full potential. A primary challenge revolves around the perceived high initial migration costs and complexity associated with transitioning from existing on-premise SIEM solutions. Many organizations have substantial investments in legacy systems, and the effort required for data migration, re-integration with cloud services, and staff retraining can be a significant barrier, especially for large, entrenched enterprises.

Another significant restraint is the shortage of skilled cybersecurity professionals with expertise in cloud-native technologies and advanced SIEM platforms. The intricate nature of deploying, configuring, and managing these sophisticated solutions requires specialized knowledge in cloud architecture, security operations, and data analytics. This talent gap makes it difficult for organizations to fully leverage the capabilities of Cloud Native SIEM, leading to underutilization or increased reliance on expensive external consultants or managed security service providers.

Furthermore, concerns regarding data residency, privacy, and compliance across various geopolitical regions act as a restraint. While cloud-native solutions offer flexibility, organizations in highly regulated sectors or countries with strict data sovereignty laws may be hesitant to fully embrace public cloud-based SIEM deployments. Ensuring that sensitive security logs and event data remain within specific geographical boundaries or comply with local privacy regulations adds a layer of complexity and can slow down adoption rates in certain markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Migration Costs & Integration Complexities | -2.1% | Global, particularly large enterprises with legacy systems | Short-term to Mid-term (2025-2029) |

| Shortage of Skilled Cybersecurity Professionals | -1.7% | Global, particularly emerging economies | Long-term (2025-2033) |

| Data Residency, Privacy & Compliance Concerns | -1.5% | Europe, Asia Pacific, highly regulated industries (BFSI, Healthcare) | Mid-term to Long-term (2026-2033) |

| Vendor Lock-in Concerns for Multi-Cloud Environments | -0.8% | Global, enterprises with multi-cloud strategies | Mid-term (2026-2030) |

| Perceived Security Risks of Public Cloud Deployment | -0.5% | Industries with extreme sensitivity (Government, Defense) | Short-term (2025-2027) |

Cloud Native SIEM Market Opportunities Analysis

The Cloud Native SIEM market presents numerous opportunities for growth and innovation, particularly through expanding into underserved market segments. The Small and Medium-sized Enterprise (SME) sector, traditionally underserved by complex and expensive traditional SIEMs, offers a significant growth avenue. Cloud-native solutions, with their lower upfront costs, ease of deployment, and often managed service offerings, are becoming increasingly accessible and attractive to SMEs looking to enhance their cybersecurity posture without the burden of extensive in-house resources.

Another substantial opportunity lies in the continuous advancement and integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities within SIEM platforms. As AI models become more sophisticated, they can offer more precise threat detection, predictive analytics, and highly automated response mechanisms, moving beyond traditional alert correlation. This allows vendors to differentiate their offerings and provide superior value, appealing to enterprises seeking cutting-edge security intelligence and operational efficiency.

Furthermore, the development of specialized Cloud Native SIEM solutions tailored for specific industry verticals represents a key growth area. Different sectors, such as healthcare, finance, and critical infrastructure, have unique compliance requirements and threat landscapes. Providers who can offer industry-specific threat intelligence, pre-built compliance dashboards, and customized integration with vertical-specific applications will find significant market traction, addressing niche demands with highly relevant solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Small and Medium-sized Enterprises (SMEs) | +3.5% | Global, especially emerging markets & regions with high SME density | Mid-term to Long-term (2026-2033) |

| Advanced AI/ML Integration for Predictive Security & Automation | +4.2% | Global, particularly in advanced economies | Short-term to Long-term (2025-2033) |

| Managed SIEM Services & Hybrid Cloud Deployments | +2.8% | Global, for organizations with limited in-house resources | Short-term to Long-term (2025-2033) |

| Development of Industry-Specific Solutions (e.g., Healthcare, BFSI) | +2.0% | Global, highly regulated sectors | Mid-term (2026-2030) |

| Geographic Expansion into Emerging Markets | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2028-2033) |

Cloud Native SIEM Market Challenges Impact Analysis

The Cloud Native SIEM market, despite its rapid growth, grapples with several significant challenges that impact adoption and effectiveness. A primary obstacle is the sheer volume and velocity of data generated in cloud environments, leading to potential issues with data ingestion, storage costs, and alert fatigue for security teams. Effectively managing, correlating, and analyzing petabytes of security logs from diverse cloud services, applications, and endpoints without overwhelming analysts remains a complex technical and operational hurdle.

Another critical challenge involves the integration complexities with diverse cloud services and existing legacy security infrastructure. Enterprises often operate in multi-cloud environments and still rely on a mix of on-premise and traditional security tools. Achieving seamless interoperability and comprehensive visibility across this heterogeneous landscape requires sophisticated integration capabilities, robust APIs, and consistent data normalization, which can be difficult to implement and maintain.

Furthermore, the evolving threat landscape and the rapid pace of cloud innovation present a continuous challenge for Cloud Native SIEM providers. Attackers constantly develop new techniques, and cloud service providers frequently update their services and introduce new features. SIEM solutions must continuously adapt their detection logic, threat intelligence, and data collection mechanisms to keep pace, ensuring that they remain effective against emerging threats and compatible with the latest cloud offerings, demanding significant R&D investment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Volume Management & Ingestion Costs | -2.0% | Global, particularly for large enterprises | Short-term to Long-term (2025-2033) |

| Interoperability & Integration with Diverse Cloud & Legacy Systems | -1.8% | Global, especially hybrid and multi-cloud adopters | Short-term to Mid-term (2025-2029) |

| Evolving Threat Landscape & Rapid Cloud Innovation Pace | -1.5% | Global, all industries | Long-term (2025-2033) |

| Alert Fatigue & High False Positive Rates Without Advanced AI | -1.0% | Global, particularly for SOC teams | Short-term to Mid-term (2025-2028) |

| Achieving Comprehensive Visibility Across Multi-Cloud Environments | -0.7% | Global, enterprises with complex cloud footprints | Mid-term (2026-2030) |

Cloud Native SIEM Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Cloud Native SIEM market, offering detailed insights into its current size, growth trajectory, key trends, and future projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, along with a detailed segmentation analysis by components, deployment models, organization sizes, and industry verticals. The report also highlights the regional landscape and profiles leading market players, aiming to equip stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 19.5 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Splunk, IBM, Microsoft, Exabeam, Securonix, LogRhythm, Sumo Logic, Elastic, CrowdStrike, SentinelOne, Arctic Wolf, Palo Alto Networks, Datadog, Google Cloud (Chronicle), AWS, Fortinet, Trend Micro, Rapid7, CyberArk, Zscaler |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cloud Native SIEM market is comprehensively segmented to provide granular insights into its various dimensions, reflecting the diverse needs and adoption patterns across the global landscape. This segmentation allows for a detailed understanding of which components are driving revenue, preferred deployment models, how different organization sizes are adopting these solutions, and the specific requirements of various industry verticals. Each segment highlights unique market dynamics, competitive landscapes, and growth opportunities.

Analysis by component differentiates between the core SIEM solutions, encompassing log management, security analytics, threat intelligence, and SOAR functionalities, and the range of services, including managed and professional services, which are crucial for deployment and ongoing support. The deployment model segmentation – public, private, and hybrid cloud – illustrates the varied preferences based on security policies, compliance needs, and existing infrastructure. Furthermore, segmenting by organization size (large enterprises versus SMEs) reveals distinct procurement behaviors and solution requirements, while the industry vertical breakdown offers insights into sector-specific use cases and regulatory influences.

- By Component

- Solution

- Log Management

- Security Analytics

- Threat Intelligence

- Security Orchestration, Automation, and Response (SOAR)

- Services

- Managed Services

- Professional Services (Consulting, Integration, Support)

- Solution

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Industry Vertical

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Retail & E-commerce

- IT & Telecommunications

- Government & Defense

- Manufacturing

- Energy & Utilities

- Others

Regional Highlights

- North America: Expected to dominate the Cloud Native SIEM market due to the early adoption of cloud technologies, a high concentration of cybersecurity vendors, robust IT infrastructure, and stringent regulatory compliance mandates. High cyberattack sophistication and significant R&D investments further fuel market growth in this region.

- Europe: Demonstrates strong growth, largely driven by the stringent General Data Protection Regulation (GDPR) and other data privacy laws, which necessitate advanced security and logging capabilities. Increased cloud adoption across various industries and a strong focus on digital sovereignty are also key factors.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by rapid digital transformation initiatives, increasing cloud infrastructure investments, and a burgeoning threat landscape. Countries like China, India, Japan, and Australia are experiencing significant adoption driven by economic growth and expanding digital ecosystems.

- Latin America: Showing nascent but accelerating growth, spurred by increasing internet penetration, digital service adoption, and a growing awareness of cybersecurity risks among businesses. Economic development and regional governmental efforts to enhance cybersecurity infrastructure contribute to market expansion.

- Middle East & Africa (MEA): Witnessing considerable investment in digital infrastructure and smart city projects, leading to an increased demand for advanced security solutions. Government initiatives in cybersecurity and a rising focus on data protection in key economies are driving the Cloud Native SIEM market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cloud Native SIEM Market.- Splunk

- IBM

- Microsoft

- Exabeam

- Securonix

- LogRhythm

- Sumo Logic

- Elastic

- CrowdStrike

- SentinelOne

- Arctic Wolf

- Palo Alto Networks

- Datadog

- Google Cloud (Chronicle)

- AWS

- Fortinet

- Trend Micro

- Rapid7

- CyberArk

- Zscaler

Frequently Asked Questions

What is Cloud Native SIEM?

Cloud Native SIEM (Security Information and Event Management) is a security solution built specifically for cloud environments. It collects, normalizes, and analyzes security data from various cloud services, applications, and infrastructure to detect, investigate, and respond to threats in real-time. Unlike traditional SIEMs, it leverages cloud elasticity, scalability, and integration capabilities.

Why are organizations shifting from traditional SIEM to Cloud Native SIEM?

Organizations are transitioning due to the inherent limitations of traditional SIEMs in dynamic cloud environments. Cloud Native SIEM offers superior scalability, agility, and cost-effectiveness by leveraging cloud infrastructure. It provides comprehensive visibility across multi-cloud setups, enhanced threat detection through AI/ML, and better integration with other cloud-native tools, addressing the complexities of modern digital footprints more effectively.

How does AI impact Cloud Native SIEM?

AI significantly enhances Cloud Native SIEM by improving threat detection accuracy, reducing false positives, and automating incident response. It enables advanced behavioral analytics, identifies subtle anomalies across vast datasets, and facilitates predictive security, thereby boosting the efficiency and effectiveness of security operations and allowing human analysts to focus on high-priority tasks.

What are the key benefits of implementing Cloud Native SIEM?

Key benefits include enhanced scalability and elasticity to handle growing data volumes, reduced infrastructure costs, improved agility and faster deployment, comprehensive visibility across cloud and hybrid environments, advanced threat detection capabilities powered by AI/ML, and streamlined compliance reporting. It also facilitates quicker incident response and fosters better collaboration among security teams.

What are the primary challenges in adopting Cloud Native SIEM?

Primary challenges involve managing the massive volume of cloud data, ensuring seamless integration with diverse cloud services and existing legacy systems, addressing data residency and compliance concerns across regions, and overcoming the shortage of skilled cybersecurity professionals. Additionally, organizations face the challenge of navigating potential initial migration costs and vendor lock-in concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted