Clinical Data Management System Market

Clinical Data Management System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704530 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

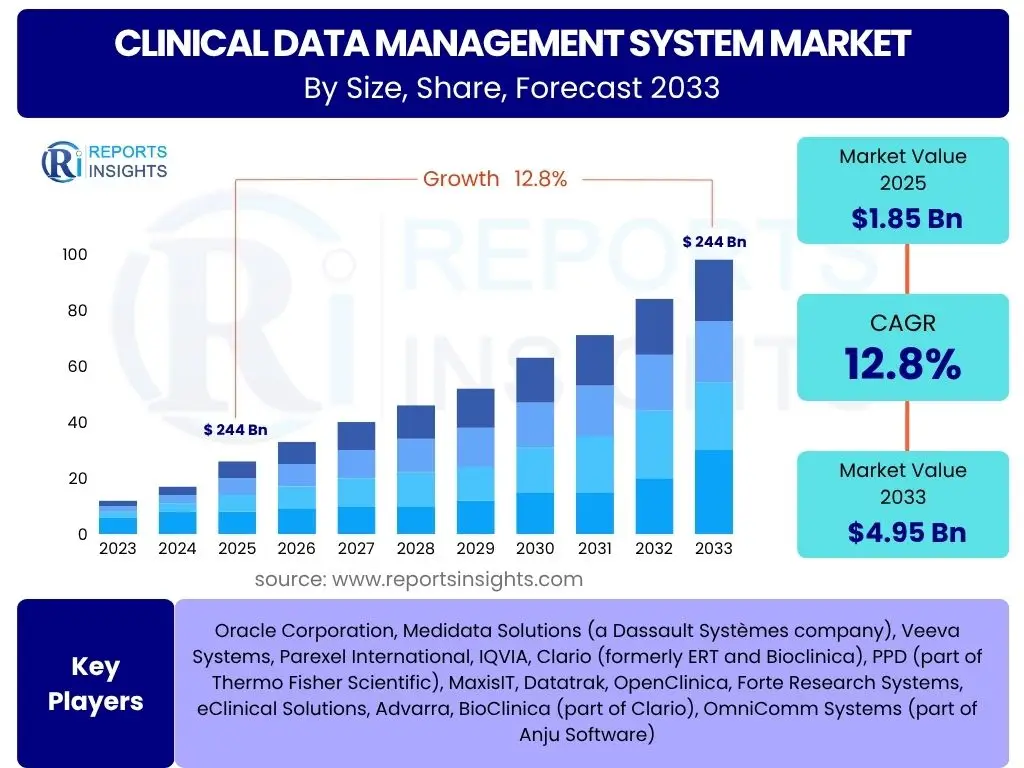

Clinical Data Management System Market Size

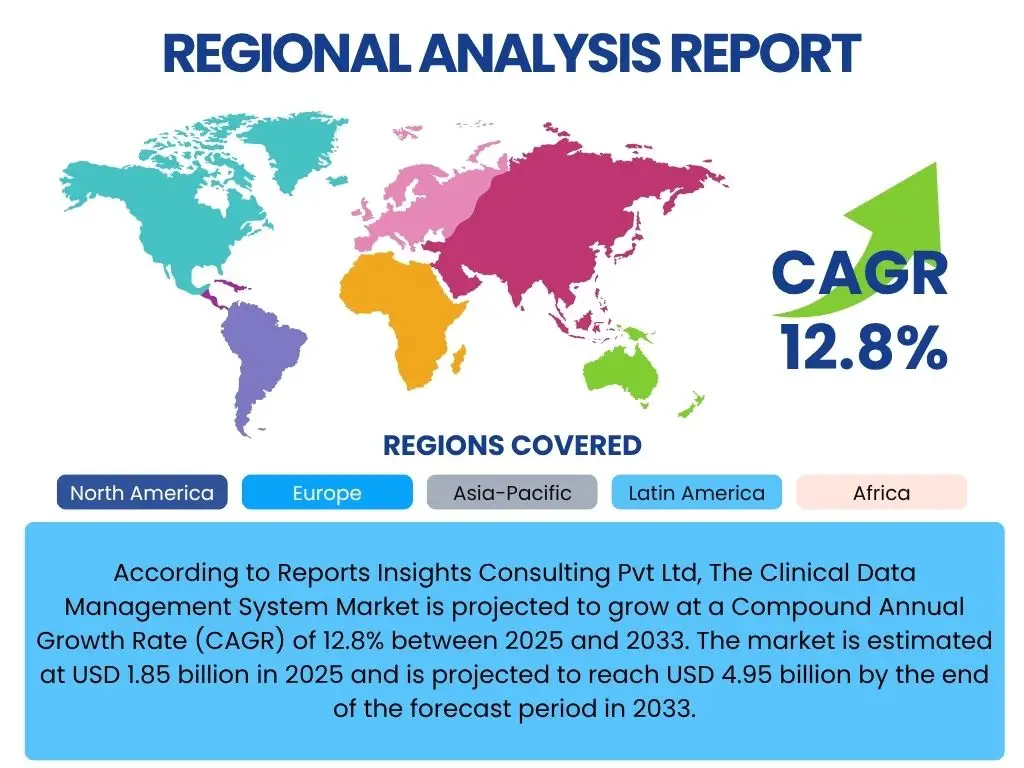

According to Reports Insights Consulting Pvt Ltd, The Clinical Data Management System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 4.95 billion by the end of the forecast period in 2033.

Key Clinical Data Management System Market Trends & Insights

The Clinical Data Management System (CDMS) market is currently experiencing a transformative phase, driven by the increasing complexity of clinical trials and the urgent need for efficient data handling. A significant trend observed is the accelerated adoption of cloud-based CDMS solutions, offering enhanced scalability, accessibility, and cost-effectiveness compared to traditional on-premise systems. This shift is particularly appealing to small and medium-sized pharmaceutical companies and Contract Research Organizations (CROs) seeking to streamline their operations without significant upfront infrastructure investments.

Another prominent insight is the growing emphasis on data integration and interoperability. Stakeholders are increasingly seeking CDMS platforms that can seamlessly integrate with other clinical trial systems, such as Electronic Health Records (EHR), Electronic Data Capture (EDC), and Enterprise Resource Planning (ERP) systems. This integration capability is crucial for creating a holistic view of patient data, reducing manual data entry errors, and improving overall data consistency and quality across the entire clinical research continuum. The focus on real-time data access and analytics is also reshaping expectations, pushing providers to offer more robust reporting and visualization tools.

- Shift towards cloud-based CDMS for enhanced flexibility and accessibility.

- Increased demand for integrated CDMS platforms capable of interoperability with diverse clinical systems.

- Emphasis on real-time data access and advanced analytical capabilities for improved decision-making.

- Adoption of decentralized clinical trial (DCT) models necessitating flexible and remote data capture solutions.

- Rising regulatory scrutiny and data privacy concerns driving demand for robust security features and compliance tools within CDMS.

- Automation of data validation and query management processes to reduce manual effort and accelerate timelines.

AI Impact Analysis on Clinical Data Management System

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to significantly revolutionize the Clinical Data Management System (CDMS) landscape. Common user questions often revolve around how AI can enhance data accuracy, automate tedious tasks, and provide deeper insights from vast datasets. AI algorithms can detect anomalies, identify data patterns, and predict potential errors with far greater efficiency than manual review, thereby improving the overall quality and integrity of clinical trial data. This capability is particularly valuable in accelerating the data cleaning and validation processes, which are traditionally time-consuming and labor-intensive.

Furthermore, AI holds immense potential in automating various aspects of data management, including query generation, coding, and discrepancy resolution. By automating these processes, CDMS platforms can reduce human error, minimize operational costs, and significantly shorten clinical trial timelines. Users also frequently inquire about AI's role in predictive analytics, such as forecasting patient recruitment rates or identifying high-risk sites. While the benefits are clear, concerns about data privacy, algorithm transparency, and the need for robust validation protocols for AI-driven insights remain critical considerations for widespread adoption and trust within the highly regulated clinical research environment.

- Automated data validation and anomaly detection, significantly improving data accuracy.

- Enhanced query management through AI-driven identification and resolution of discrepancies.

- Predictive analytics for trend identification, risk assessment, and proactive decision-making in trials.

- Streamlined medical coding and adverse event reporting using natural language processing (NLP).

- Potential for reduced manual workload and operational costs through intelligent automation.

- Challenges in data privacy, ethical considerations, and regulatory validation of AI algorithms.

Key Takeaways Clinical Data Management System Market Size & Forecast

The Clinical Data Management System (CDMS) market is set for robust expansion, primarily fueled by the global surge in clinical trials and the increasing complexity of pharmaceutical research. A key takeaway is the consistent double-digit Compound Annual Growth Rate (CAGR) projected through 2033, underscoring the indispensable role of advanced data management solutions in modern drug development. This growth trajectory is not merely volume-driven but reflects a deeper industry need for systems that can handle large datasets, ensure data integrity, and accelerate the regulatory submission process. The market's significant financial projection signals continued investment and innovation in this critical sector.

Another crucial insight is the accelerating shift towards technologically advanced CDMS platforms, particularly those leveraging cloud infrastructure and incorporating AI capabilities. This trend indicates that future market leadership will likely belong to providers offering highly scalable, secure, and intelligent solutions that move beyond basic data capture. The forecast also highlights the growing importance of data interoperability and real-time analytics, suggesting that integrated platforms will command a larger market share. The substantial market size forecast by 2033 reinforces the notion that CDMS is no longer a peripheral tool but a central pillar of efficient and compliant clinical research operations.

- Significant market expansion with a projected CAGR of 12.8% from 2025 to 2033.

- Market value expected to nearly triple from USD 1.85 billion in 2025 to USD 4.95 billion by 2033.

- Cloud-based and AI-integrated CDMS solutions are primary growth drivers.

- Increasing reliance on CDMS for managing complex, global clinical trials.

- Data integrity, regulatory compliance, and accelerated timelines are core value propositions.

Clinical Data Management System Market Drivers Analysis

The Clinical Data Management System (CDMS) market is propelled by a confluence of factors, foremost among them being the escalating volume and complexity of clinical trials globally. As pharmaceutical and biotechnology companies increasingly engage in multi-center, multi-country trials with larger patient cohorts and diverse data sources, the need for sophisticated, centralized data management becomes paramount. This complexity necessitates automated solutions to ensure data accuracy, reduce errors, and maintain regulatory compliance, thereby driving the adoption of advanced CDMS platforms.

Another significant driver is the growing demand for regulatory compliance and data integrity across the life sciences industry. Regulatory bodies worldwide, such as the FDA and EMA, impose stringent requirements for data quality, security, and traceability in clinical research. CDMS solutions inherently offer features like audit trails, version control, and data validation, which are critical for meeting these regulatory standards and mitigating risks during drug development. The increasing focus on real-world evidence (RWE) and decentralized clinical trials (DCTs) further amplifies the need for flexible and robust CDMS capabilities that can capture and manage data from diverse sources and settings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing volume and complexity of clinical trials | +3.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Stringent regulatory requirements and data integrity needs | +2.8% | Global, especially highly regulated markets | Medium-term (2025-2029) |

| Rising adoption of cloud-based solutions and SaaS models | +2.0% | North America, Europe, emerging APAC markets | Short-term to Medium-term (2025-2028) |

| Growth in pharmaceutical R&D expenditure and outsourcing to CROs | +1.5% | Global | Long-term (2025-2033) |

Clinical Data Management System Market Restraints Analysis

Despite the robust growth trajectory, the Clinical Data Management System (CDMS) market faces certain restraints that could temper its expansion. A primary concern for many organizations is the high initial implementation cost associated with advanced CDMS platforms. This includes not only the software licensing fees but also costs related to system customization, data migration from legacy systems, integration with existing IT infrastructure, and comprehensive staff training. For smaller biotechnology firms or academic research institutions with limited budgets, these upfront expenditures can be a significant deterrent, often leading them to opt for less sophisticated or manual data management methods.

Another notable restraint is the inherent complexity involved in CDMS software integration and data standardization. Clinical trials often involve diverse data sources, formats, and legacy systems, making seamless integration a formidable challenge. Ensuring data consistency and interoperability across different platforms requires significant technical expertise and resources. Furthermore, the resistance to change within organizations, particularly from clinical research professionals accustomed to traditional data management practices, can impede the smooth adoption and full utilization of new CDMS technologies. Concerns over data security and privacy breaches, particularly with cloud-based systems, also act as a significant restraint, compelling providers to invest heavily in robust cybersecurity measures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial implementation and maintenance costs | -1.2% | Global, particularly small and medium-sized enterprises | Long-term (2025-2033) |

| Data privacy and security concerns | -0.8% | Global, especially GDPR-compliant regions | Medium-term (2025-2029) |

| Lack of skilled professionals for advanced CDMS platforms | -0.6% | Emerging markets, some developed regions | Short-term to Medium-term (2025-2028) |

| Interoperability and integration challenges with existing systems | -0.5% | Global | Long-term (2025-2033) |

Clinical Data Management System Market Opportunities Analysis

The Clinical Data Management System (CDMS) market presents substantial growth opportunities driven by technological advancements and evolving clinical trial paradigms. The rapid proliferation of decentralized clinical trials (DCTs), which collect data from various remote sources including wearables, sensors, and patient-reported outcomes, creates an immense need for CDMS solutions capable of handling diverse data types and ensuring their integrity and security. CDMS providers can capitalize on this trend by developing flexible, patient-centric platforms that facilitate remote data capture and monitoring, expanding their addressable market significantly beyond traditional site-based trials.

Another significant opportunity lies in the integration of Artificial Intelligence (AI) and Machine Learning (ML) within CDMS platforms. These technologies can automate complex tasks such as data validation, query generation, and medical coding, dramatically improving efficiency and reducing manual effort. Furthermore, AI can unlock predictive analytics capabilities, offering insights into patient recruitment, trial risks, and potential adverse events, thereby enabling proactive decision-making. The increasing adoption of Real-World Evidence (RWE) for regulatory submissions and post-market surveillance also offers a lucrative avenue for CDMS providers to adapt their platforms to manage and analyze large volumes of RWE data, which often originates from disparate and unstructured sources like electronic health records and claims databases.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing adoption of Decentralized Clinical Trials (DCTs) | +2.0% | Global | Short-term to Long-term (2025-2033) |

| Integration of Artificial Intelligence (AI) and Machine Learning (ML) | +1.8% | Global, particularly developed economies | Medium-term to Long-term (2027-2033) |

| Increasing demand for Real-World Evidence (RWE) management | +1.5% | North America, Europe | Medium-term (2026-2030) |

| Expansion into emerging markets and untapped regions | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

Clinical Data Management System Market Challenges Impact Analysis

The Clinical Data Management System (CDMS) market faces several significant challenges that necessitate strategic navigation by market players. A primary challenge revolves around the increasingly stringent and complex global regulatory landscape. With diverse regulations such as GDPR in Europe, HIPAA in the U.S., and country-specific data privacy laws, CDMS providers must continuously update their platforms to ensure compliance across multiple jurisdictions. Non-compliance can lead to severe penalties, reputational damage, and delays in drug approvals, posing a considerable risk to both providers and end-users.

Another substantial challenge is maintaining robust data security and privacy in an era of escalating cyber threats and heightened concerns over sensitive patient information. As CDMS platforms increasingly move to the cloud and integrate with various external systems, the attack surface expands, demanding sophisticated encryption, access controls, and continuous monitoring. Organizations must also contend with the challenge of data standardization and interoperability across disparate systems and data sources, which can hinder seamless data flow and analysis. Lastly, the shortage of skilled professionals proficient in both clinical research and advanced data management technologies presents a bottleneck, affecting both the development of innovative CDMS solutions and their effective implementation by end-users.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating complex and evolving regulatory landscape | -1.0% | Global | Long-term (2025-2033) |

| Ensuring robust data security and patient privacy | -0.7% | Global | Long-term (2025-2033) |

| Achieving seamless interoperability and data standardization | -0.6% | Global | Medium-term (2025-2029) |

| Shortage of skilled workforce in clinical data management | -0.5% | Global | Short-term to Medium-term (2025-2028) |

Clinical Data Management System Market - Updated Report Scope

This report provides a comprehensive analysis of the Clinical Data Management System (CDMS) market, offering a detailed assessment of its current landscape, growth drivers, restraints, opportunities, and challenges. It encompasses an in-depth segmentation analysis by product, deployment model, end-use, and key regional markets. The study covers historical market performance from 2019 to 2023 and provides forecasts from 2025 to 2033, highlighting the impact of emerging technologies like AI and decentralized trial models. The report aims to furnish stakeholders with critical market insights to inform strategic business decisions, identify growth avenues, and understand competitive dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 billion |

| Market Forecast in 2033 | USD 4.95 billion |

| Growth Rate | 12.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Oracle Corporation, Medidata Solutions (a Dassault Systèmes company), Veeva Systems, Parexel International, IQVIA, Clario (formerly ERT and Bioclinica), PPD (part of Thermo Fisher Scientific), MaxisIT, Datatrak, OpenClinica, Forte Research Systems, eClinical Solutions, Advarra, BioClinica (part of Clario), OmniComm Systems (part of Anju Software) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Clinical Data Management System (CDMS) market is meticulously segmented to provide a granular view of its various facets, enabling a deeper understanding of market dynamics and growth opportunities. These segmentations are critical for identifying niche markets, tailoring product development strategies, and optimizing market entry approaches. The market is primarily bifurcated by product type, deployment model, end-use, component, application, and study design, each revealing distinct adoption patterns and growth drivers.

Under product type, the market differentiates between Web-based, Cloud-based, and Enterprise CDMS solutions, reflecting the evolving technological preferences and infrastructure capabilities of diverse users. The deployment model segment further categorizes solutions into on-premise and cloud-based options, with the latter increasingly dominating due to its flexibility and scalability. End-use segmentation highlights the primary consumers of CDMS, including pharmaceutical and biopharmaceutical companies, Contract Research Organizations (CROs), medical device companies, and academic & research institutions, each with specific requirements influencing their choice of CDMS.

- Product:

- Web-based CDMS

- Cloud-based CDMS

- Enterprise CDMS

- Deployment Mode:

- On-premise

- Cloud

- End Use:

- Pharmaceutical & Biopharmaceutical Companies

- Contract Research Organizations (CROs)

- Medical Device Companies

- Academic & Research Institutions

- Component:

- Software

- Services

- Application:

- Clinical Trials

- Regulatory Submissions

- Post-Market Surveillance

- Pharmacovigilance

- Study Design:

- Interventional

- Observational

- Expanded Access

Regional Highlights

- North America: This region is anticipated to maintain its dominance in the Clinical Data Management System market, primarily due to the presence of a well-established pharmaceutical and biotechnology industry, extensive research and development activities, and a high adoption rate of advanced clinical trial technologies. Stringent regulatory frameworks and significant investments in healthcare infrastructure also contribute to the region's leading market share. The United States, in particular, is a major hub for clinical trials and innovation in CDMS.

- Europe: Europe represents a substantial market for CDMS, driven by increasing clinical research initiatives, a strong focus on data quality and regulatory compliance (e.g., GDPR), and the growing trend of outsourcing clinical trials to CROs. Countries such as Germany, the UK, and France are key contributors, characterized by robust R&D spending and a proactive approach to adopting digital solutions in healthcare.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate in the CDMS market during the forecast period. This growth is fueled by the rising number of clinical trials being conducted in emerging economies like China, India, and South Korea, attracted by lower operational costs and large patient populations. Increasing healthcare expenditure, improving regulatory frameworks, and a growing presence of global pharmaceutical companies are key factors stimulating market expansion in this region.

- Latin America, Middle East, and Africa (MEA): These regions are emerging markets for CDMS, driven by improving healthcare infrastructure, increasing investment in clinical research, and the rising prevalence of chronic diseases necessitating drug development. While smaller in market share compared to North America and Europe, these regions offer significant untapped potential for CDMS providers seeking to expand their global footprint, particularly as clinical trial activities diversify geographically.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Clinical Data Management System Market.- Oracle Corporation

- Medidata Solutions (a Dassault Systèmes company)

- Veeva Systems

- Parexel International

- IQVIA

- Clario (formerly ERT and Bioclinica)

- PPD (part of Thermo Fisher Scientific)

- MaxisIT

- Datatrak

- OpenClinica

- Forte Research Systems

- eClinical Solutions

- Advarra

- BioClinica (part of Clario)

- OmniComm Systems (part of Anju Software)

- ArisGlobal

- TrialMaster (MedNet Solutions)

- PHASTAR

- Medrio

- Florence Healthcare

Frequently Asked Questions

What is the projected growth rate for the Clinical Data Management System (CDMS) market?

The Clinical Data Management System (CDMS) market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033.

What are the primary drivers for the CDMS market's growth?

Key drivers include the increasing volume and complexity of clinical trials, stringent regulatory requirements for data integrity, and the rising adoption of cloud-based CDMS solutions.

How is AI impacting the Clinical Data Management System market?

AI is significantly impacting CDMS by enabling automated data validation, enhancing query management, and providing predictive analytics for more efficient and accurate clinical data processing.

Which region is expected to lead the CDMS market?

North America is anticipated to maintain its leadership in the CDMS market due to a mature pharmaceutical industry, extensive R&D, and high technology adoption rates.

What are the main challenges faced by the CDMS market?

Major challenges include navigating complex and evolving global regulatory landscapes, ensuring robust data security and patient privacy, and addressing the shortage of skilled professionals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted