Casted Alumunium Wheel Market

Casted Alumunium Wheel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708437 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

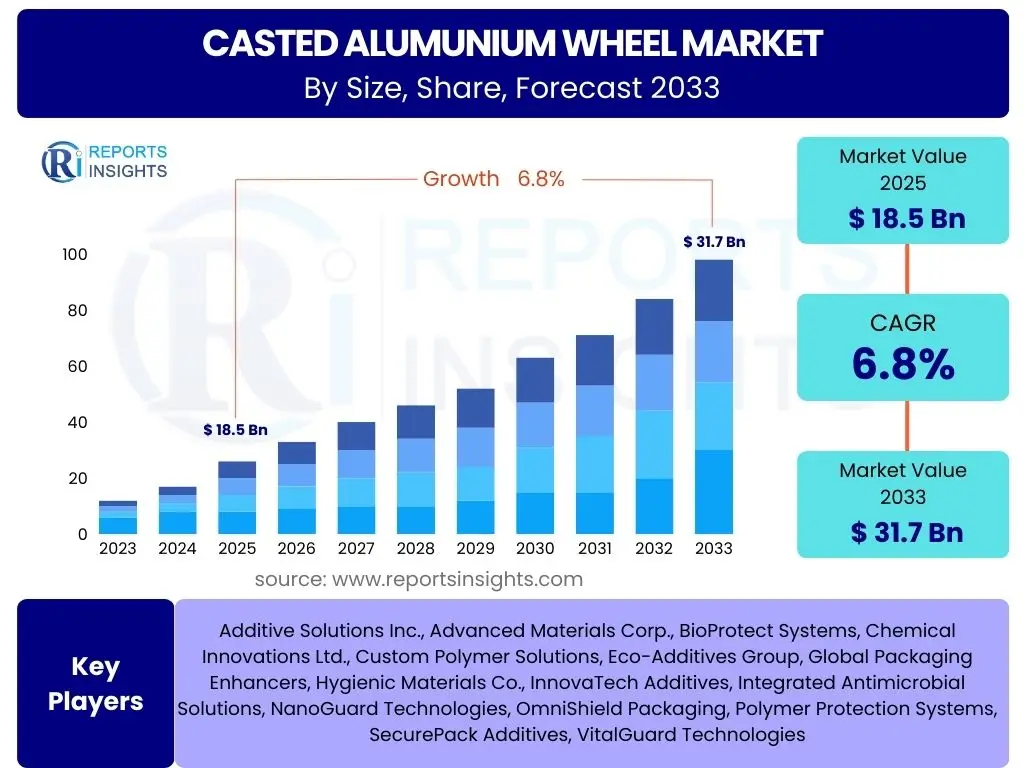

Casted Aluminum Wheel Market Size

According to Reports Insights Consulting Pvt Ltd, The Casted Aluminum Wheel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 18.5 billion in 2025 and is projected to reach USD 31.7 billion by the end of the forecast period in 2033.

Key Casted Aluminum Wheel Market Trends & Insights

The Casted Aluminum Wheel market is experiencing significant transformation driven by evolving automotive industry demands and technological advancements. Key user questions frequently revolve around the impact of electric vehicle (EV) proliferation, the pursuit of lightweighting solutions for fuel efficiency and range extension, and the increasing consumer preference for aesthetic customization. Furthermore, inquiries often focus on the adoption of advanced manufacturing processes, such as advanced low-pressure die casting and semi-solid casting, which enhance product quality and performance.

Market insights suggest a strong correlation between rising disposable incomes, particularly in emerging economies, and the growing demand for premium vehicle aesthetics and performance. This trend is fueling the market for larger diameter and more intricately designed aluminum wheels. Additionally, sustainability concerns are prompting innovations in material recycling and energy-efficient production methods, shaping the long-term trajectory of the industry. The aftermarket segment also exhibits robust growth, driven by vehicle customization trends and replacement cycles.

- Increasing demand for lightweight wheels to enhance fuel efficiency and EV range.

- Growing aesthetic customization trends in both OEM and aftermarket segments.

- Proliferation of electric vehicles driving demand for specific wheel designs and performance characteristics.

- Advancements in casting technologies improving strength, durability, and design flexibility.

- Rising focus on sustainable manufacturing practices and recycled aluminum content.

- Shift towards larger diameter wheels, particularly in SUV and luxury vehicle segments.

- Integration of smart manufacturing and automation in production processes.

AI Impact Analysis on Casted Aluminum Wheel

User inquiries concerning the impact of Artificial Intelligence (AI) on the Casted Aluminum Wheel sector primarily focus on its potential to revolutionize design, optimize manufacturing processes, and enhance supply chain efficiency. There is significant interest in how AI can facilitate predictive maintenance for casting machinery, thereby reducing downtime and operational costs. Users also frequently ask about AI's role in quality control, particularly in detecting minute defects that human inspection might miss, and its ability to refine material compositions for improved wheel performance and durability.

The adoption of AI is anticipated to lead to more sophisticated product development cycles, allowing for rapid iteration and simulation of new wheel designs that balance aesthetics, aerodynamics, and structural integrity. Furthermore, AI-driven analytics can optimize energy consumption during the casting process and manage raw material inventories more effectively, addressing both cost efficiency and sustainability goals. While the initial investment and the need for specialized data scientists present challenges, the long-term benefits in terms of enhanced productivity, reduced waste, and superior product quality are expected to drive significant AI integration across the industry.

- AI-driven generative design for optimized wheel structures and aerodynamics.

- Predictive maintenance for casting machinery, reducing downtime and improving operational efficiency.

- Enhanced quality control through AI-powered visual inspection systems detecting micro-defects.

- Optimization of casting parameters and material compositions for superior performance and reduced waste.

- Improved supply chain management and inventory forecasting through advanced analytics.

- Automation of repetitive tasks and process monitoring in manufacturing facilities.

Key Takeaways Casted Aluminum Wheel Market Size & Forecast

Key user questions regarding the market's future predominantly revolve around the primary growth accelerators, the influence of macro-economic factors, and the longevity of current demand trends. Users seek to understand what specific segments offer the most promising investment opportunities and which regions are poised for exponential growth. There is a strong emphasis on identifying sustainable competitive advantages and potential disruptive technologies that could reshape the market landscape over the forecast period.

The market is characterized by robust growth, primarily fueled by the automotive sector's continuous evolution towards lightweight materials, increased vehicle production, and a strong global demand for aesthetically pleasing and performance-oriented components. While traditional internal combustion engine (ICE) vehicles remain a significant demand source, the burgeoning electric vehicle market is rapidly emerging as a critical growth engine. Companies focusing on innovation in design, material science, and manufacturing efficiency are expected to capture a larger market share, leveraging advanced technologies to meet diverse consumer and OEM requirements.

- The market is on a strong growth trajectory, driven by automotive industry expansion and lightweighting trends.

- Electric Vehicle (EV) segment represents a significant growth catalyst for advanced aluminum wheel designs.

- Technological innovation in casting processes and material science is crucial for competitive advantage.

- Asia Pacific is projected to remain the dominant and fastest-growing region due to escalating vehicle production and consumer demand.

- Aftermarket and premium vehicle segments offer substantial revenue generation opportunities.

- Sustainability initiatives, including recycled content and energy-efficient production, are becoming increasingly important for market positioning.

Casted Aluminum Wheel Market Drivers Analysis

The Casted Aluminum Wheel market is propelled by a confluence of factors stemming from the automotive industry's strategic imperatives and evolving consumer preferences. A primary driver is the pervasive industry trend towards lightweighting, where aluminum wheels significantly contribute to reducing overall vehicle weight. This weight reduction directly translates to improved fuel efficiency for internal combustion engine vehicles and extended range for electric vehicles, aligning with stringent environmental regulations and consumer demand for eco-friendlier transportation solutions. Furthermore, the inherent design flexibility of cast aluminum allows manufacturers to create intricate and visually appealing wheel designs, catering to the growing consumer desire for vehicle customization and premium aesthetics, which are critical differentiators in competitive automotive markets.

Another substantial driver is the expansion of global vehicle production, particularly in emerging economies where rising disposable incomes are fueling a surge in vehicle ownership. As vehicle sales increase, so does the demand for both OEM (Original Equipment Manufacturer) wheels and aftermarket replacements and upgrades. The robust growth of the luxury and SUV segments also plays a pivotal role, as these vehicles often feature larger, more sophisticated, and higher-value aluminum wheels as standard or optional equipment. Technological advancements in casting processes, such as low-pressure die casting, have made the production of high-quality, complex aluminum wheels more efficient and cost-effective, further stimulating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Vehicles | +1.5% | Global, particularly North America, Europe, China | Long-term (2025-2033) |

| Growing Vehicle Production and Sales | +1.2% | Asia Pacific (China, India), Latin America | Mid to Long-term (2025-2033) |

| Rising Consumer Preference for Premium Aesthetics & Customization | +0.9% | Global, particularly developed economies | Mid to Long-term (2025-2033) |

| Technological Advancements in Casting Processes | +0.7% | Global, particularly industrialized nations | Mid-term (2025-2030) |

Casted Aluminum Wheel Market Restraints Analysis

Despite robust growth prospects, the Casted Aluminum Wheel market faces several notable restraints that could temper its expansion. One significant challenge is the volatility of raw material prices, primarily aluminum. Fluctuations in global aluminum commodity markets can directly impact production costs, squeezing profit margins for manufacturers and potentially leading to higher end-product prices, which might affect consumer demand. This unpredictability in material costs necessitates sophisticated hedging strategies and efficient supply chain management, adding complexity to operations. Furthermore, the energy-intensive nature of aluminum casting processes contributes to higher production costs, especially in regions with elevated energy prices, posing a competitive disadvantage against alternative materials or manufacturing methods.

Another crucial restraint is the intense competition from alternative wheel materials, such as steel and, increasingly, carbon fiber. While aluminum offers an excellent balance of weight, strength, and cost, steel wheels remain a more economical option, particularly for entry-level vehicles and commercial applications where cost-effectiveness often outweighs the benefits of lighter weight. Carbon fiber wheels, though significantly more expensive, offer superior lightweighting and performance for high-end luxury and performance vehicles, potentially capping aluminum's market penetration in the ultra-premium segment. Additionally, stringent environmental regulations pertaining to manufacturing emissions and waste disposal introduce compliance costs and operational complexities, particularly in developed markets, which can act as a barrier to market entry and expansion for some players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material (Aluminum) Prices | -0.8% | Global | Short to Mid-term (2025-2028) |

| High Energy Consumption in Manufacturing Process | -0.6% | Europe, North America | Mid to Long-term (2025-2033) |

| Competition from Alternative Wheel Materials (Steel, Carbon Fiber) | -0.5% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations | -0.4% | Europe, North America, East Asia | Mid to Long-term (2025-2033) |

Casted Aluminum Wheel Market Opportunities Analysis

The Casted Aluminum Wheel market is poised to capitalize on several significant opportunities driven by evolving automotive trends and technological advancements. The accelerated global shift towards electric vehicles (EVs) presents a substantial avenue for growth. EVs inherently benefit more from lightweight components to maximize battery range, making aluminum wheels a preferred choice. This segment requires specialized wheel designs that not only reduce weight but also often incorporate aerodynamic features to minimize drag, creating new design and engineering challenges that innovative manufacturers can leverage. The expanding luxury and premium vehicle segments, alongside the burgeoning SUV and crossover market, also represent considerable opportunities, as these vehicles frequently utilize larger, more stylized, and higher-value aluminum wheels as standard equipment, reflecting consumer demand for enhanced aesthetics and performance.

Furthermore, the aftermarket segment continues to offer robust growth potential. Vehicle owners increasingly seek to personalize their vehicles, driving demand for custom and upgraded aluminum wheels that offer both aesthetic enhancements and performance improvements. This trend is particularly strong among younger demographics and automotive enthusiasts. Technological advancements in casting, such as hybrid casting processes and the use of recycled aluminum, present opportunities for cost reduction, improved material properties, and enhanced sustainability, appealing to both environmentally conscious consumers and regulations. Expanding into emerging markets, particularly in Southeast Asia, Africa, and Latin America, where vehicle ownership is on the rise, also provides new avenues for market penetration, albeit with considerations for localized product offerings and distribution strategies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Production | +1.8% | Global, particularly China, Europe, North America | Long-term (2025-2033) |

| Expanding Luxury and SUV/Crossover Segments | +1.3% | Global | Mid to Long-term (2025-2033) |

| Increasing Aftermarket Demand for Customization | +1.0% | North America, Europe, parts of Asia Pacific | Mid to Long-term (2025-2033) |

| Development of Advanced & Sustainable Casting Technologies | +0.8% | Global | Mid to Long-term (2025-2033) |

Casted Aluminum Wheel Market Challenges Impact Analysis

The Casted Aluminum Wheel market faces several significant challenges that necessitate strategic navigation from manufacturers. One primary challenge involves maintaining cost competitiveness amidst fluctuating raw material prices and the high capital expenditure required for advanced casting equipment. The entry of new players, particularly from regions with lower manufacturing costs, intensifies price pressure on established market participants, demanding continuous innovation in production efficiency and supply chain optimization. Moreover, the increasing complexity of wheel designs, driven by aesthetic trends and aerodynamic requirements for electric vehicles, adds to manufacturing complexity and requires specialized expertise and advanced machinery, impacting production timelines and costs.

Another critical challenge lies in adhering to increasingly stringent safety and performance standards imposed by regulatory bodies and automotive OEMs. Wheels are critical safety components, and any failure can have severe consequences, leading to rigorous testing and certification processes. This demands significant investment in R&D and quality assurance, particularly as vehicles become heavier and more powerful, and as autonomous driving technologies emerge. Furthermore, managing the environmental footprint of production, from raw material sourcing to energy consumption and waste management, presents a continuous challenge, requiring ongoing investment in sustainable practices to meet regulatory requirements and corporate social responsibility goals.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition and Cost Management | -0.9% | Global | Mid to Long-term (2025-2033) |

| Adherence to Strict Safety and Performance Standards | -0.7% | Global, particularly developed markets | Long-term (2025-2033) |

| Complexity of Design and Manufacturing Processes | -0.5% | Global | Mid to Long-term (2025-2033) |

| Environmental Compliance and Sustainability Demands | -0.4% | Europe, North America, East Asia | Long-term (2025-2033) |

Casted Aluminum Wheel Market - Updated Report Scope

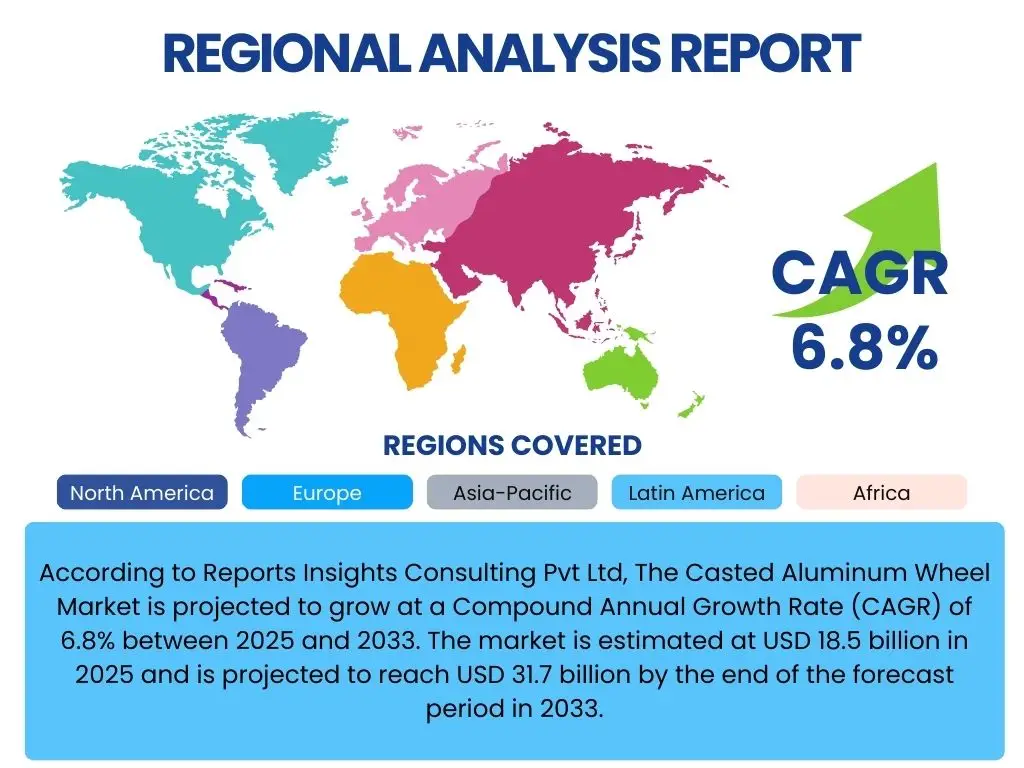

This comprehensive report delves into the intricate dynamics of the global Casted Aluminum Wheel Market, providing an in-depth analysis of market size, growth projections, and key influencing factors from 2019 to 2033. It offers a detailed examination of market segmentation by vehicle type, technology, size, and end-use, complemented by a thorough regional analysis spanning North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The report integrates an AI impact assessment, highlights emerging trends, and identifies critical drivers, restraints, opportunities, and challenges that shape the industry landscape. Profiles of leading market players are included to provide competitive insights, equipping stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 31.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Maxion Wheels, Superior Industries International, Ronal Group, Enkei Corporation, Topy Industries, BBS GmbH, Borbet GmbH, Advanti Racing, CM Wheels, Uniwheel Group, Citic Dicastal Co. Ltd., Foshan Nanhai Zhongnan Aluminum Wheel Co. Ltd., Wanfeng Auto Wheel, Zhejiang Jinfei Kaida Wheel Co. Ltd., Alcoa Corporation, OZ S.p.A., Method Race Wheels, Rays Engineering, American Racing, Konig Wheels |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Casted Aluminum Wheel market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of market performance across different product categories, application areas, and end-user types, offering valuable insights into consumer behavior and industry-specific demands. Each segment contributes uniquely to the overall market landscape, influenced by varying technological adoption rates, economic conditions, and regulatory environments. Understanding these individual segments is critical for stakeholders to identify niche opportunities, tailor product strategies, and optimize market penetration in specific areas.

The primary segmentation categories include vehicle type, technology utilized in casting, wheel size, and end-use application. Vehicle type differentiation helps in understanding demand patterns from passenger cars versus commercial vehicles, each with distinct requirements for durability, weight, and design. Technology segmentation highlights the prevalence and evolution of various casting methods, indicating the adoption of advanced manufacturing techniques for improved performance and cost-efficiency. Wheel size is a key indicator of market trends related to vehicle segments (e.g., small cars vs. SUVs) and consumer preferences. Finally, the distinction between OEM and aftermarket provides insights into initial equipment supply versus consumer-driven replacement and customization markets, both of which exhibit distinct growth drivers and competitive landscapes.

- By Vehicle Type: Passenger Cars, Commercial Vehicles

- By Technology: Low-Pressure Die Casting, Gravity Casting, High-Pressure Die Casting, Counter Pressure Casting

- By Size: Up to 15 inch, 15 to 18 inch, 19 to 22 inch, Above 22 inch

- By End-Use: Original Equipment Manufacturer (OEM), Aftermarket

Regional Highlights

- North America: Characterized by a robust automotive industry, high consumer disposable income, and a strong demand for performance-oriented and aesthetically appealing wheels. The region is a significant adopter of larger diameter wheels for SUVs and luxury vehicles. Stringent fuel efficiency standards also drive the demand for lightweight aluminum wheels.

- Europe: A mature market with a high emphasis on advanced manufacturing, stringent environmental regulations, and a strong preference for premium and high-performance vehicles. The region is a hub for innovation in casting technologies and sustainable production, with a growing electric vehicle market further boosting demand for specialized aluminum wheels.

- Asia Pacific (APAC): The largest and fastest-growing market for Casted Aluminum Wheels, primarily driven by expanding vehicle production in China, India, Japan, and South Korea. Rapid urbanization, rising disposable incomes, and increasing middle-class populations contribute to a burgeoning demand for both OEM and aftermarket wheels. The region is also a major manufacturing base, benefiting from economies of scale.

- Latin America: An emerging market demonstrating steady growth, fueled by increasing vehicle sales and infrastructure development. Economic stabilization and rising consumer spending power in countries like Brazil and Mexico are driving demand, though often with a preference for more cost-effective solutions and a growing aftermarket segment.

- Middle East & Africa (MEA): Exhibiting nascent but promising growth, primarily driven by automotive market expansion in the Gulf Cooperation Council (GCC) countries and parts of Africa. Investments in infrastructure and a rising standard of living contribute to increased vehicle ownership, with a developing demand for both standard and performance-enhancing aluminum wheels.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Casted Aluminum Wheel Market.- Maxion Wheels

- Superior Industries International

- Ronal Group

- Enkei Corporation

- Topy Industries

- BBS GmbH

- Borbet GmbH

- Advanti Racing

- CM Wheels

- Uniwheel Group

- Citic Dicastal Co. Ltd.

- Foshan Nanhai Zhongnan Aluminum Wheel Co. Ltd.

- Wanfeng Auto Wheel

- Zhejiang Jinfei Kaida Wheel Co. Ltd.

- Alcoa Corporation

- OZ S.p.A.

- Method Race Wheels

- Rays Engineering

- American Racing

- Konig Wheels

Frequently Asked Questions

Analyze common user questions about the Casted Aluminum Wheel market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Casted Aluminum Wheel Market?

The Casted Aluminum Wheel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 31.7 billion by 2033 from USD 18.5 billion in 2025.

What are the primary drivers for the Casted Aluminum Wheel Market?

Key drivers include the increasing demand for lightweight vehicles to improve fuel efficiency and EV range, growing global vehicle production, rising consumer preference for premium aesthetics and customization, and continuous technological advancements in casting processes.

How is the electric vehicle (EV) sector impacting the market?

The EV sector is a significant growth opportunity, as electric vehicles benefit greatly from lightweight aluminum wheels to extend battery range and improve performance, leading to specialized design and manufacturing demands.

Which region holds the largest share in the Casted Aluminum Wheel Market?

The Asia Pacific (APAC) region is currently the largest and fastest-growing market, driven by high vehicle production volumes, rapid urbanization, and increasing disposable incomes in countries like China and India.

What are the main challenges faced by Casted Aluminum Wheel manufacturers?

Key challenges include intense price competition, volatility in raw material costs, the high energy consumption of manufacturing processes, and strict adherence to increasingly stringent safety, performance, and environmental regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted