Automotive Connected Car Platform Market

Automotive Connected Car Platform Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708632 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Connected Car Platform Market Size

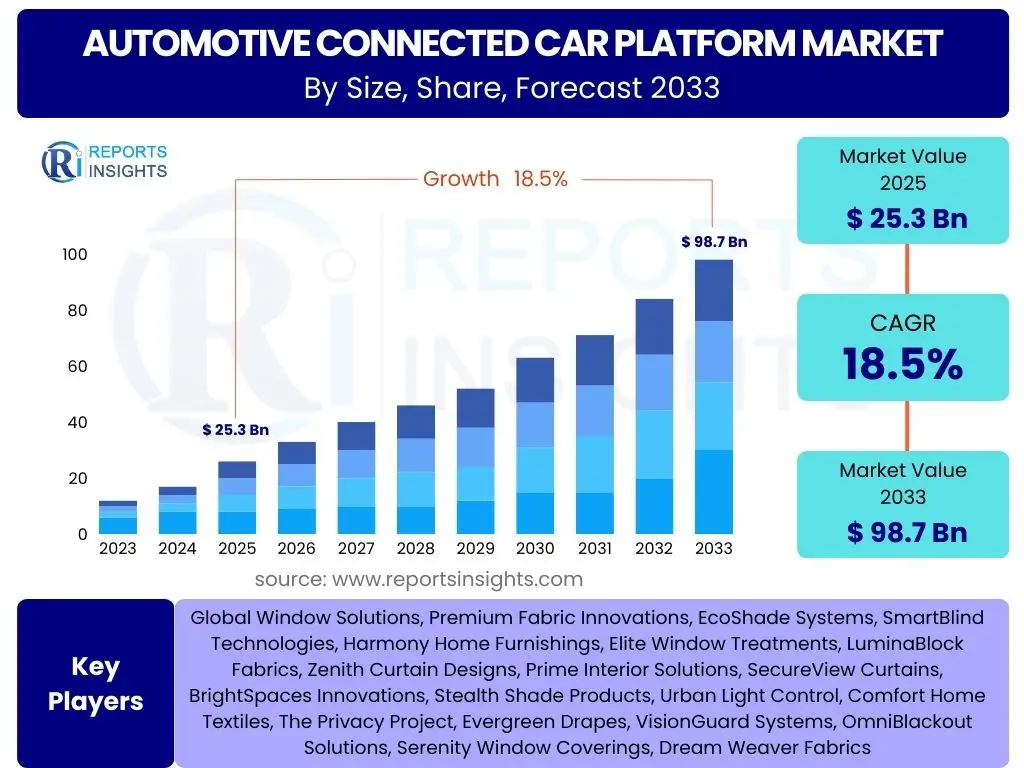

According to Reports Insights Consulting Pvt Ltd, The Automotive Connected Car Platform Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 25.3 billion in 2025 and is projected to reach USD 98.7 billion by the end of the forecast period in 2033. This substantial growth is driven by increasing integration of advanced connectivity solutions in vehicles, rising consumer demand for in-car digital experiences, and stringent safety and security regulations mandating connected features.

The market expansion is further bolstered by continuous advancements in telematics, infotainment systems, and vehicle-to-everything (V2X) communication technologies. As automotive manufacturers increasingly pivot towards software-defined vehicles, connected car platforms become central to offering a rich ecosystem of services, from remote diagnostics and predictive maintenance to over-the-air updates and personalized user experiences. The robust CAGR reflects the critical role these platforms play in the future of mobility, transforming vehicles from mere modes of transport into intelligent, networked devices.

Key Automotive Connected Car Platform Market Trends & Insights

Common user inquiries about market trends for automotive connected car platforms frequently center on the evolution of connectivity standards, the proliferation of new in-car services, and the shift towards subscription-based models. Users are keen to understand how 5G and V2X technologies are reshaping the landscape, the growing importance of seamless integration with smart city infrastructure, and the increasing focus on personalized and proactive user experiences. There is also significant interest in how cybersecurity concerns are being addressed amidst the expansion of connected features.

- Enhanced 5G and V2X Communication: The rollout of 5G networks and advancements in V2X communication are enabling ultra-low latency, high-bandwidth data exchange, crucial for real-time traffic information, cooperative driving, and autonomous vehicle operations.

- Software-Defined Vehicles (SDVs): A paradigm shift towards SDVs, where vehicle functionality is primarily managed by software, is accelerating the adoption of connected platforms for feature upgrades, customization, and new service deployment via over-the-air (OTA) updates.

- Subscription-Based Services: Automotive OEMs are increasingly offering connected features and services through subscription models, creating recurring revenue streams and enhancing customer loyalty with continuous value propositions such as premium navigation, advanced driver assistance features, and personalized infotainment.

- Integrated Digital Cockpit Experiences: The fusion of advanced infotainment, digital clusters, and enhanced human-machine interfaces (HMIs) creates a cohesive and immersive digital cockpit, offering occupants a seamless and intuitive interaction with vehicle functions and external services.

- Focus on Cybersecurity and Data Privacy: With the growing complexity and connectivity of vehicles, there is an escalating emphasis on robust cybersecurity measures and transparent data privacy protocols to protect vehicle systems from threats and ensure user trust.

AI Impact Analysis on Automotive Connected Car Platform

User questions regarding the impact of Artificial Intelligence (AI) on automotive connected car platforms often revolve around its role in enhancing personalization, improving safety, and enabling autonomous driving capabilities. Consumers and industry professionals seek to understand how AI is leveraged for predictive analytics, voice assistance, adaptive infotainment, and decision-making in complex driving scenarios. There is also a strong interest in the ethical implications of AI in vehicle systems and its potential to revolutionize the entire in-car experience.

AI's influence is profound, transforming connected cars into intelligent, self-learning environments. From optimizing energy consumption based on driving patterns to providing proactive maintenance alerts, AI algorithms are processing vast amounts of vehicular and environmental data to deliver smarter, safer, and more personalized mobility solutions. This integration extends beyond mere automation, delving into predictive behavior, natural language processing for intuitive human-vehicle interaction, and dynamic risk assessment, making AI an indispensable component for the next generation of automotive platforms.

- Personalized User Experience: AI algorithms analyze driving habits, preferences, and biometric data to tailor infotainment, climate control, seating positions, and navigation suggestions, creating a highly personalized cabin environment.

- Enhanced Autonomous Driving Capabilities: AI is central to advanced driver-assistance systems (ADAS) and autonomous driving, enabling real-time perception, decision-making, path planning, and obstacle avoidance through sophisticated sensor fusion and machine learning models.

- Predictive Maintenance and Diagnostics: AI-powered platforms monitor vehicle performance data to predict potential component failures, schedule proactive maintenance, and provide real-time diagnostic insights, significantly reducing downtime and operational costs.

- Advanced Voice Assistants and Natural Language Processing (NLP): AI-driven voice assistants offer intuitive, hands-free control over various vehicle functions, navigation, and connectivity services, improving convenience and reducing driver distraction through natural language understanding.

- Optimized Route Planning and Traffic Management: AI processes real-time traffic, weather, and road condition data to optimize routes, suggest alternative paths, and contribute to smart city traffic management systems, enhancing efficiency and reducing congestion.

Key Takeaways Automotive Connected Car Platform Market Size & Forecast

Common user questions regarding key takeaways from the Automotive Connected Car Platform market size and forecast often focus on the overarching growth trajectory, the primary drivers of this expansion, and the areas expected to witness the most significant transformation. Users are eager to understand the long-term viability of investment in this sector, the critical technologies underpinning future growth, and the strategic implications for both automotive manufacturers and technology providers. Insights into market saturation potential and emerging geographies for expansion are also frequently sought after.

The market is poised for significant and sustained growth, driven by an accelerating shift towards digitalization in the automotive industry and increasing consumer expectation for seamless, integrated digital experiences in their vehicles. The rapid evolution of connectivity standards, coupled with advanced software capabilities, positions connected car platforms as foundational technologies for future mobility services, including autonomous driving and shared mobility models. Strategic partnerships between traditional automotive players and tech innovators will be crucial for capitalizing on the diverse opportunities presented by this dynamic market.

- Exponential Market Expansion: The market is projected for robust growth, with a nearly fourfold increase in valuation by 2033, underscoring the indispensable role of connectivity in modern vehicles.

- Technology Convergence as a Catalyst: The integration of 5G, AI, and cloud computing is critical, enabling more sophisticated and responsive connected car services that cater to evolving consumer demands.

- Service-Centric Business Models: A significant shift towards subscription-based services and over-the-air updates will redefine revenue generation for OEMs and service providers, fostering continuous engagement with customers.

- Cybersecurity as a Core Requirement: As vehicles become more connected, robust cybersecurity frameworks are not merely features but fundamental necessities to ensure safety, data integrity, and consumer trust.

- Global and Regional Disparities: While growth is global, developed regions like North America and Europe are leading in adoption, with emerging markets in Asia Pacific rapidly catching up due to increasing disposable income and supportive government initiatives.

Automotive Connected Car Platform Market Drivers Analysis

The automotive connected car platform market is experiencing substantial growth propelled by several critical factors. A primary driver is the escalating consumer demand for advanced in-car infotainment and connectivity features, which have evolved from luxury additions to expected standards. Drivers also include increasingly stringent safety regulations and the global push for enhanced road safety, leading to the integration of telematics and emergency call systems. Moreover, the rapid expansion of 5G infrastructure and advancements in Internet of Things (IoT) technologies are providing the necessary backbone for more robust and reliable connected car services.

Automotive manufacturers are also playing a pivotal role by strategically embedding connected capabilities into their new vehicle architectures, recognizing the long-term value in data generation, over-the-air updates, and new revenue streams through subscription services. The growing urbanization and increasing traffic congestion in major metropolitan areas further fuel the demand for smart navigation, real-time traffic updates, and vehicle-to-infrastructure (V2I) communication, all facilitated by connected car platforms. This synergistic combination of consumer pull, regulatory push, technological advancements, and OEM strategies creates a powerful impetus for market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Consumer Demand for In-Car Connectivity & Infotainment | +5.2% | Global (North America, Europe, Asia Pacific) | Short- to Mid-term (2025-2030) |

| Strict Regulatory Mandates for Vehicle Safety & Telematics | +4.8% | Europe (eCall), North America (Safety Standards) | Mid-term (2025-2033) |

| Expansion of 5G Network Infrastructure and IoT Ecosystem | +4.5% | China, South Korea, US, European Union | Mid- to Long-term (2027-2033) |

| Automotive OEMs' Strategic Shift Towards Software-Defined Vehicles | +4.0% | Germany, Japan, US, South Korea | Mid- to Long-term (2027-2033) |

| Growing Adoption of Advanced Driver Assistance Systems (ADAS) & Autonomous Driving | +3.5% | Global (US, China, Germany) | Long-term (2028-2033) |

Automotive Connected Car Platform Market Restraints Analysis

Despite the robust growth, the automotive connected car platform market faces several significant restraints that could temper its expansion. One of the primary challenges is the high cost associated with developing, deploying, and maintaining connected car technologies. This includes the expense of advanced hardware, sophisticated software, and ongoing data connectivity, which can translate into higher vehicle prices or recurring subscription fees, potentially deterring price-sensitive consumers. Another critical restraint is the pervasive concern regarding data privacy and cybersecurity vulnerabilities, as connected vehicles collect and transmit vast amounts of sensitive personal and operational data, making them targets for cyberattacks.

Furthermore, the lack of standardized protocols and interoperability across different manufacturers and regions creates fragmentation within the market, hindering seamless integration and universal service offerings. Limited awareness and understanding among a segment of the consumer base regarding the benefits and functionalities of connected car platforms also act as a restraint, particularly in developing economies. Addressing these multifaceted challenges, from cost reduction and robust security frameworks to standardization and consumer education, will be crucial for sustained market growth and widespread adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Connected Car Technology & Recurring Subscription Fees | -3.8% | Global (Emerging Markets like India, Brazil) | Short- to Mid-term (2025-2030) |

| Cybersecurity Risks & Data Privacy Concerns | -3.5% | Global (Europe - GDPR, North America) | Ongoing (2025-2033) |

| Lack of Standardization & Interoperability Across Platforms | -3.0% | Global | Mid- to Long-term (2027-2033) |

| Limited Network Coverage & Infrastructure in Remote Areas | -2.5% | Rural regions in APAC, Africa, Latin America | Long-term (2028-2033) |

| Consumer Skepticism & Lack of Awareness in Certain Demographics | -2.0% | Older demographics, less technologically inclined users | Short- to Mid-term (2025-2030) |

Automotive Connected Car Platform Market Opportunities Analysis

The automotive connected car platform market presents numerous opportunities for innovation and growth. The burgeoning demand for autonomous driving capabilities is a significant opportunity, as connected platforms are fundamental to enabling vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, crucial for safe and efficient autonomous operations. The expansion of electric vehicles (EVs) also offers a unique avenue for growth, as connected platforms can provide crucial services such as real-time charging station availability, battery management, and route optimization for EV drivers, enhancing the overall EV ownership experience.

Furthermore, the potential for new data monetization strategies, leveraging the vast amounts of data generated by connected cars, represents a substantial opportunity for OEMs and third-party service providers. This data can be used to offer tailored insurance products, predictive maintenance, personalized advertising, and smart city planning solutions. The integration with smart home ecosystems and the broader Internet of Things (IoT) also opens doors for seamless digital lifestyles extending from the home to the vehicle, creating a highly integrated and convenient user experience. Strategic partnerships between automotive companies, tech giants, and telecommunications providers are key to unlocking these diverse opportunities and fostering an ecosystem of advanced mobility services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Autonomous Driving Systems and V2X Communication | +6.0% | US, China, Germany, Japan | Mid- to Long-term (2027-2033) |

| Growth of Electric Vehicles (EVs) and Associated Smart Services | +5.5% | Europe, China, North America | Mid- to Long-term (2027-2033) |

| Data Monetization & New Revenue Streams from Connected Services | +5.0% | Global | Mid-term (2025-2030) |

| Expansion into Shared Mobility and Fleet Management Solutions | +4.5% | Urban centers globally | Mid- to Long-term (2027-2033) |

| Seamless Integration with Smart Home and IoT Ecosystems | +4.0% | North America, Europe, Developed Asia Pacific | Long-term (2028-2033) |

Automotive Connected Car Platform Market Challenges Impact Analysis

The automotive connected car platform market, while promising, is confronted by several significant challenges that necessitate strategic solutions. One major hurdle is managing the immense volume of data generated by connected vehicles, encompassing data storage, processing, and real-time analytics, which requires robust cloud infrastructure and sophisticated AI algorithms. The complexity of integrating various hardware and software components from multiple vendors into a cohesive and secure platform also poses a substantial technical challenge, requiring extensive testing and validation.

Another critical challenge lies in ensuring regulatory compliance across diverse international jurisdictions, particularly concerning data privacy, cybersecurity standards, and telematics regulations. These varying legal landscapes can complicate global deployment and require significant investment in localized solutions. Furthermore, the rapid pace of technological change necessitates continuous innovation and investment to stay competitive, while addressing the need for skilled talent in areas such as cybersecurity, AI, and software development remains a persistent industry-wide challenge. Overcoming these complexities will be vital for sustained market leadership and broader adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing & Processing Massive Volumes of Data | -4.2% | Global | Ongoing (2025-2033) |

| Complexity of System Integration & Interoperability | -3.7% | Global | Ongoing (2025-2033) |

| Ensuring Regulatory Compliance Across Diverse Geographies | -3.5% | Europe, North America, China | Ongoing (2025-2033) |

| High Development & Maintenance Costs for Advanced Features | -3.0% | Global | Short- to Mid-term (2025-2030) |

| Shortage of Skilled Talent in AI, Cybersecurity, & Software Development | -2.8% | North America, Europe, Asia Pacific | Ongoing (2025-2033) |

Automotive Connected Car Platform Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Connected Car Platform Market, covering historical performance from 2019 to 2023 and offering detailed forecasts from 2025 to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages advanced analytical methodologies to provide stakeholders with actionable insights into market dynamics, competitive landscape, technological advancements, and strategic recommendations for market entry and expansion. The scope is designed to offer a holistic view of the market's current state and future trajectory, empowering informed decision-making for businesses operating within or looking to enter this dynamic sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.3 Billion |

| Market Forecast in 2033 | USD 98.7 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Connected Car Solutions Inc., AutoNet Innovations, Mobility Intelligence Systems, DriveLink Technologies, SmartCar Platform Co., Vehicular Connectivity Leaders, NextGen Auto AI, Digital Drive Solutions, Future Mobility Tech, Connective Auto Systems, Integrated Vehicle Services, Advanced Telematics Corp., SmartRoad Networks, CyberCar Platforms, Seamless Mobility Providers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Connected Car Platform market is meticulously segmented across various critical dimensions to provide a granular understanding of its structure and dynamics. These segmentations allow for a detailed analysis of market performance based on how connectivity is implemented, the underlying technological standards, the specific services offered, the types of vehicles incorporating these platforms, and the end-use applications. Such an in-depth breakdown is essential for identifying high-growth areas, understanding competitive landscapes within niches, and formulating targeted market strategies. Each segment reveals distinct trends, adoption rates, and technological preferences, reflecting the diverse requirements and capabilities across the automotive ecosystem.

The market's intricate segmentation highlights the multifaceted nature of connected car platforms. For instance, the "By Connectivity Type" segment differentiates between factory-installed embedded systems, smartphone-tethered solutions, and fully integrated platforms, each offering distinct advantages in terms of reliability, functionality, and cost. Similarly, the "By Service" segment illustrates the broad spectrum of applications, from entertainment and navigation to critical safety and maintenance functions, underscoring the platform's role as a versatile enabler of modern automotive features. Understanding these distinctions is crucial for stakeholders to pinpoint opportunities and tailor their offerings to specific market demands.

- By Connectivity Type:

- Embedded: Factory-installed hardware and software providing independent connectivity.

- Tethered: Leverages a smartphone's internet connection to provide in-car connectivity.

- Integrated: Combines aspects of embedded and tethered, often with integrated hardware that can also use external device connectivity.

- By Technology:

- 2G/3G: Older generation networks, primarily for basic telematics.

- 4G/LTE: Current dominant standard, supporting rich infotainment and data services.

- 5G: Emerging standard offering ultra-low latency and high bandwidth for advanced applications like autonomous driving and V2X.

- Satellite: Used for remote areas or specific applications requiring global coverage.

- By Service:

- Infotainment: Streaming media, app integration, in-car Wi-Fi, digital radio.

- Telematics: Emergency call (eCall), breakdown assistance, stolen vehicle recovery, remote vehicle access.

- Navigation: Real-time traffic, dynamic routing, point-of-interest search, connected parking.

- Remote Diagnostics: Predictive maintenance, vehicle health reports, software updates.

- Over-the-Air (OTA) Updates: Software and firmware updates, feature upgrades.

- Autonomous Driving Features: Sensor data processing, V2X communication for ADAS and self-driving.

- V2X Communication: Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), Vehicle-to-Network (V2N) for enhanced safety and traffic flow.

- By Vehicle Type:

- Passenger Vehicles: Sedans, SUVs, hatchbacks, luxury cars.

- Commercial Vehicles:

- Light Commercial Vehicles (LCVs): Vans, pickups for delivery and small businesses.

- Heavy Commercial Vehicles (HCVs): Trucks, buses for logistics and public transport.

- By End-Use:

- Original Equipment Manufacturers (OEMs): Integrated solutions directly from vehicle manufacturers.

- Aftermarket: Third-party solutions and devices installed post-purchase.

Regional Highlights

- North America: This region is a leading market for automotive connected car platforms, driven by high consumer adoption of advanced technologies, a strong presence of major automotive OEMs and technology providers, and robust investment in 5G infrastructure. Stringent safety regulations, coupled with increasing demand for premium in-car experiences and autonomous driving features, further fuel market growth. The U.S. and Canada are key contributors, with a focus on comprehensive telematics, infotainment, and navigation services.

- Europe: Europe represents a mature and highly regulated market, with growth propelled by initiatives such as the mandatory eCall system, which has significantly boosted the adoption of embedded telematics. The region is also at the forefront of V2X communication development and smart city integration. Countries like Germany, France, and the UK are witnessing strong adoption, supported by luxury vehicle manufacturers and a push towards sustainable and efficient mobility solutions, including integrated platforms for electric vehicles.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily due to the rapid expansion of the automotive industry in China, India, Japan, and South Korea. Rising disposable incomes, increasing urbanization, and a tech-savvy consumer base are driving demand for connected services. Government initiatives supporting smart transportation and infrastructure development, coupled with competitive pricing strategies by local OEMs, are key factors contributing to the region's dynamic growth, particularly in 5G-enabled services and mass-market vehicle connectivity.

- Latin America: This region is experiencing steady growth in the connected car market, albeit at a slower pace compared to developed regions. The adoption is primarily driven by an increasing focus on vehicle security, anti-theft systems, and fleet management solutions for commercial vehicles. Brazil and Mexico are leading the market, with rising penetration of smartphones also supporting tethered connectivity solutions. Economic development and improving digital infrastructure are crucial for accelerating market expansion.

- Middle East and Africa (MEA): The MEA market for connected car platforms is in its nascent stage but shows significant potential for future growth. Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and UAE, are investing heavily in smart city projects and advanced infrastructure, which will drive demand for connected mobility. Vehicle security, navigation, and entertainment services are the primary applications gaining traction, with a growing interest in leveraging connected technologies for smart traffic management and public transportation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Connected Car Platform Market.- Global Connected Car Solutions Inc.

- AutoNet Innovations

- Mobility Intelligence Systems

- DriveLink Technologies

- SmartCar Platform Co.

- Vehicular Connectivity Leaders

- NextGen Auto AI

- Digital Drive Solutions

- Future Mobility Tech

- Connective Auto Systems

- Integrated Vehicle Services

- Advanced Telematics Corp.

- SmartRoad Networks

- CyberCar Platforms

- Seamless Mobility Providers

- Urban Mobility Platforms

- Pioneering Automotive Software

- Intelligent Transportation Systems Corp.

- Global Infotainment Partners

- Connected Safety Dynamics

Frequently Asked Questions

Analyze common user questions about the Automotive Connected Car Platform market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Automotive Connected Car Platform?

An Automotive Connected Car Platform is a comprehensive system that integrates hardware, software, and communication technologies to enable vehicles to send and receive data, communicate with external networks, and provide various services such as infotainment, telematics, navigation, and remote diagnostics to drivers and passengers.

How is 5G impacting the Connected Car Platform Market?

5G connectivity is revolutionizing the connected car market by offering ultra-low latency, high bandwidth, and increased reliability. This enables advanced applications like real-time V2X communication, enhanced autonomous driving capabilities, seamless over-the-air (OTA) updates, and high-definition in-car streaming services, significantly improving vehicle safety, efficiency, and user experience.

What are the main types of services offered by Connected Car Platforms?

The main types of services include infotainment (e.g., streaming, app integration), telematics (e.g., emergency call, breakdown assistance, stolen vehicle tracking), navigation (e.g., real-time traffic, dynamic routing), remote diagnostics, over-the-air (OTA) updates for software and firmware, and advanced features for autonomous driving and V2X communication.

What are the biggest challenges facing the adoption of Connected Car Platforms?

Key challenges include managing cybersecurity risks and ensuring data privacy, the high cost of technology development and deployment, the complexity of integrating diverse systems from multiple vendors, and the lack of universal standardization across different platforms and regions. Limited network infrastructure in certain areas and consumer awareness also pose hurdles.

Which regions are leading the growth in the Connected Car Platform Market?

North America and Europe are currently leading in market adoption due to strong technological infrastructure, high consumer demand for advanced features, and supportive regulatory environments. However, the Asia Pacific region, particularly China and India, is projected to be the fastest-growing market, driven by rapid automotive industry expansion and increasing digitalization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted