Carbon Fibre Market

Carbon Fibre Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702190 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

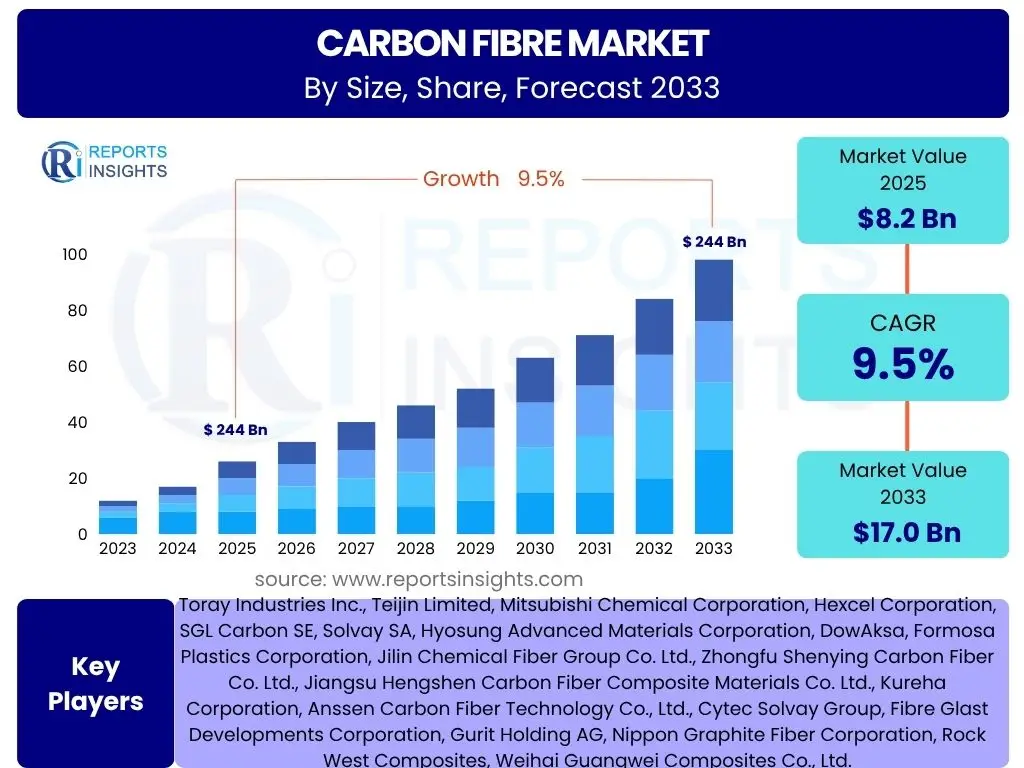

Carbon Fibre Market Size

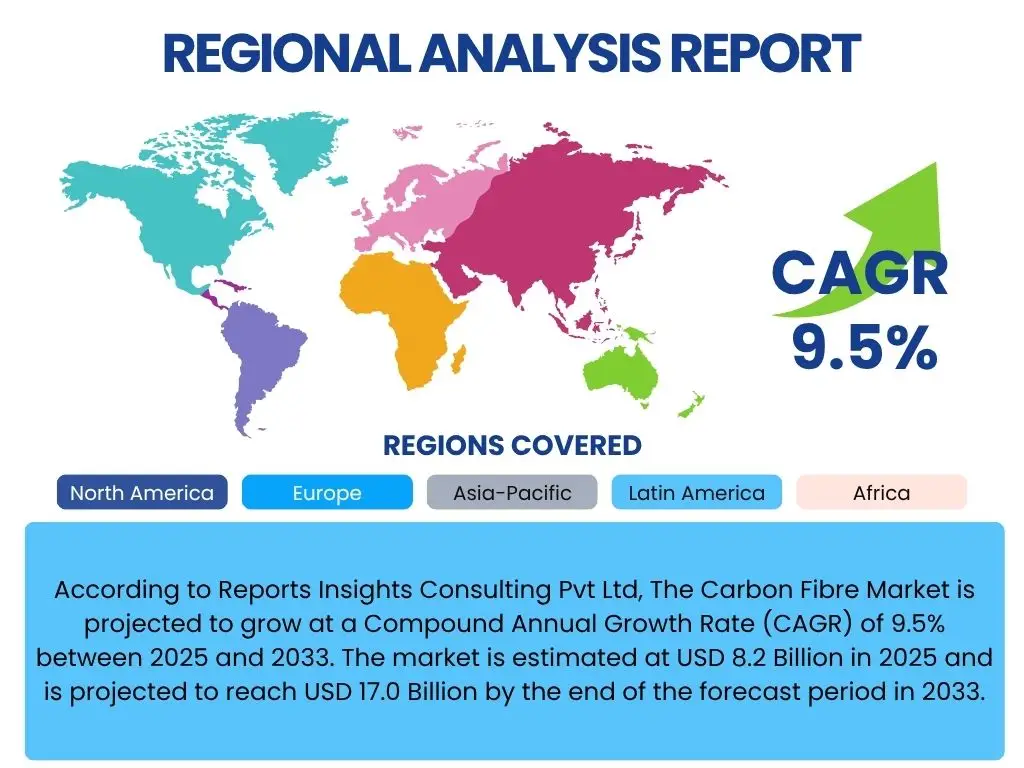

According to Reports Insights Consulting Pvt Ltd, The Carbon Fibre Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 8.2 Billion in 2025 and is projected to reach USD 17.0 Billion by the end of the forecast period in 2033.

Key Carbon Fibre Market Trends & Insights

The Carbon Fibre market is experiencing significant evolution, driven by a growing imperative for lightweighting and enhanced performance across diverse industries. Key user inquiries often revolve around the adoption rates in new sectors, advancements in material science, and the integration of sustainable practices. The market is witnessing a profound shift towards greater utilization in electric vehicles and renewable energy, reflecting global environmental objectives and technological progress. Furthermore, there is an increasing focus on improving the cost-effectiveness of carbon fiber production and exploring innovative manufacturing techniques to broaden its applicability.

Innovations in precursor materials, alongside the development of more efficient and automated manufacturing processes, are pivotal trends reducing production costs and increasing scalability. This includes advancements in areas like automated fiber placement and additive manufacturing, which facilitate complex part geometries and reduce material waste. The push for sustainability is also profoundly impacting the market, leading to increased research into recyclable carbon fiber and bio-based precursors. These combined trends indicate a market poised for expansion into new, high-volume applications while striving for greater economic and environmental viability.

- Increasing demand for lightweight materials in automotive, particularly for Electric Vehicles (EVs), to extend battery range and improve performance.

- Growing adoption in the aerospace and defense sectors for fuel efficiency and structural integrity, including next-generation aircraft and unmanned aerial vehicles (UAVs).

- Expansion of carbon fibre usage in renewable energy, specifically in larger, more efficient wind turbine blades.

- Advancements in manufacturing technologies, such as automated fiber placement (AFP) and additive manufacturing (3D printing), reducing production time and cost.

- Rising focus on sustainable carbon fibre solutions, including recycling technologies and the development of bio-based or alternative precursor materials.

- Development of lower-cost and higher-performance carbon fibres tailored for industrial and mass-market applications.

AI Impact Analysis on Carbon Fibre

User queries regarding the impact of Artificial intelligence (AI) on Carbon Fibre manufacturing and application frequently explore how AI can optimize processes, reduce costs, and accelerate innovation. AI's influence is increasingly critical in material science for predictive modeling of carbon fibre properties, enabling researchers to design new composite materials with tailored characteristics more efficiently. Its application in manufacturing extends to real-time process monitoring, anomaly detection, and predictive maintenance, significantly enhancing production efficiency and reducing waste. This intelligent automation helps to address the inherent complexities and precision requirements of carbon fibre fabrication.

Furthermore, AI is instrumental in quality control, utilizing machine vision and deep learning algorithms to detect subtle defects that human inspection might miss, thereby ensuring the integrity and reliability of carbon fibre components. In design and simulation, AI-powered tools allow for rapid iteration and optimization of composite structures, leading to lighter, stronger, and more cost-effective products. The integration of AI across the carbon fibre value chain promises to unlock new levels of efficiency, innovation, and scalability, ultimately making carbon fibre more accessible and competitive for a broader range of applications.

- AI-driven material design and optimization for tailored carbon fibre properties and performance.

- Process automation and real-time control in manufacturing, leading to enhanced efficiency and reduced cycle times.

- Predictive maintenance and anomaly detection in production lines, minimizing downtime and optimizing resource utilization.

- Enhanced quality control through AI-powered vision systems for precise defect detection and classification.

- Simulation and digital twin technologies for rapid prototyping and performance validation of carbon fibre composites.

- Optimization of supply chain logistics and demand forecasting for carbon fibre precursors and finished products.

Key Takeaways Carbon Fibre Market Size & Forecast

Analysis of common user questions concerning the Carbon Fibre market size and forecast consistently reveals a strong interest in the overall growth trajectory, the primary drivers of this expansion, and the sustainability of demand. The overarching insight is that the carbon fibre market is set for robust growth, largely fueled by its indispensable role in lightweighting and performance enhancement across high-growth industries. This upward trend is not merely cyclical but reflects a fundamental shift towards more efficient and advanced materials in critical sectors such as aerospace, automotive, and renewable energy.

The market's resilience and projected expansion underscore the strategic importance of carbon fibre in addressing global challenges like energy efficiency and emissions reduction. While cost remains a consideration, ongoing technological advancements and increasing production scales are gradually mitigating this barrier, opening doors to new applications. The forecast indicates a future where carbon fibre becomes even more pervasive, driven by innovation, diverse industrial demand, and a growing emphasis on high-performance, lightweight solutions.

- The Carbon Fibre market is projected for significant and sustained growth, nearly doubling in value from 2025 to 2033.

- Strong demand from key end-use industries, particularly aerospace & defense, automotive (especially EVs), and wind energy, remains the primary growth catalyst.

- Ongoing technological advancements in manufacturing processes and precursor materials are crucial for improving cost-effectiveness and expanding market reach.

- The imperative for lightweighting to improve fuel efficiency and reduce emissions continues to drive carbon fibre adoption globally.

- Increasing investment in research and development for sustainable and recyclable carbon fibre solutions indicates a long-term commitment to environmental responsibility.

Carbon Fibre Market Drivers Analysis

The Carbon Fibre market is propelled by a confluence of powerful drivers, primarily centered around the global demand for lightweight, high-strength materials across various industries. The imperative for fuel efficiency in transportation and the quest for extended range in electric vehicles are significant forces. Carbon fibre's superior strength-to-weight ratio makes it an ideal material for reducing vehicle weight, leading to lower energy consumption and improved performance. This fundamental advantage positions carbon fibre as a critical component in the evolution of modern mobility and aerospace engineering.

Beyond transportation, the expansion of the renewable energy sector, particularly wind power, represents another substantial driver. Larger and more efficient wind turbine blades require materials that can withstand immense structural loads while remaining lightweight enough to optimize energy capture. Carbon fibre composites meet these demanding specifications, enabling the development of next-generation turbines. Furthermore, advancements in manufacturing technologies and the gradual reduction in production costs are making carbon fibre more accessible and economically viable for a broader array of applications, stimulating demand in new industrial and consumer sectors.

The increasing global focus on sustainability and carbon footprint reduction also indirectly drives the market. By enabling lighter vehicles and more efficient energy generation, carbon fibre contributes to lower emissions and resource consumption over the lifecycle of products. This aligns with corporate sustainability goals and government regulations, further embedding carbon fibre into future industrial strategies. Continued research and development in carbon fibre recycling and bio-based precursors are also enhancing its environmental appeal, creating a virtuous cycle of innovation and adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Materials | +1.8% | Global, North America, Europe, APAC | Short-term to Long-term |

| Growth in Aerospace and Defense Sector | +1.5% | North America, Europe, Asia Pacific | Medium-term to Long-term |

| Rising Automotive and Electric Vehicle Production | +1.7% | Asia Pacific, Europe, North America | Short-term to Medium-term |

| Expansion of Wind Energy Sector | +1.2% | Europe, Asia Pacific, North America | Medium-term to Long-term |

| Technological Advancements in Manufacturing | +1.0% | Global | Short-term to Medium-term |

Carbon Fibre Market Restraints Analysis

Despite its numerous advantages, the Carbon Fibre market faces several significant restraints that could impede its growth trajectory. The primary impediment is the high manufacturing cost associated with carbon fibre production. The energy-intensive processes, expensive precursor materials like polyacrylonitrile (PAN), and complex conversion steps contribute significantly to the final product cost. This elevated cost limits its widespread adoption in certain cost-sensitive applications and industries, where alternative materials, even if heavier, offer a more economically viable solution.

Another critical restraint is the complexity and slow pace of the production process itself. Manufacturing high-quality carbon fibre requires precise control over numerous parameters, making scaling up production challenging and often time-consuming. This can lead to supply chain bottlenecks, especially during periods of surging demand, and can affect the consistency of supply for high-volume applications. Furthermore, the limited availability and fluctuating prices of high-quality precursor materials, predominantly PAN, create supply chain vulnerabilities and cost instability for manufacturers.

Lastly, the challenge of recycling carbon fibre composites remains a substantial hurdle. Traditional thermoset carbon fibre composites are difficult and costly to recycle effectively, leading to landfill waste and environmental concerns. While mechanical and chemical recycling methods are being developed, they are not yet widely adopted or economically competitive on a large scale. This lack of robust recycling infrastructure and high recycling costs deter some environmentally conscious industries and contribute to the material's overall lifecycle cost, acting as a brake on its broader market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost | -1.1% | Global | Ongoing, Long-term |

| Complex Production Processes and Scalability Challenges | -0.8% | Global | Ongoing, Medium-term |

| Challenges in Recycling Carbon Fibre Composites | -0.7% | Global | Ongoing, Long-term |

| Competition from Alternative Materials | -0.5% | Global | Ongoing, Short-term |

Carbon Fibre Market Opportunities Analysis

The Carbon Fibre market is ripe with opportunities driven by innovation, market diversification, and the increasing global emphasis on sustainable material solutions. A significant opportunity lies in the development of lower-cost precursor materials. Current reliance on expensive PAN precursors contributes significantly to the final cost of carbon fibre. Research into alternative, more economical, and sustainably sourced precursors, such as lignin or pitch, could drastically reduce production costs, thereby expanding carbon fibre's applicability to a wider range of price-sensitive, high-volume markets.

Furthermore, the continuous evolution of advanced manufacturing techniques presents immense opportunities. Innovations such as automated fibre placement (AFP), filament winding, and emerging additive manufacturing (3D printing) for composites are enabling more efficient production, reduced material waste, and the creation of complex geometries. These advancements not only lower manufacturing costs but also open doors for carbon fibre in new applications where design flexibility and rapid prototyping are crucial, such as personalized medical devices or intricate industrial components.

Finally, the pursuit of sustainable carbon fibre solutions, including enhanced recycling technologies and the adoption of bio-based resins, offers a compelling avenue for market growth and improved environmental standing. As industries and consumers increasingly prioritize eco-friendly materials, developing commercially viable and efficient carbon fibre recycling processes will unlock significant value from end-of-life products and reduce the industry's environmental footprint. This shift towards a circular economy for carbon fibre could attract new investments and expand its appeal across sectors committed to sustainability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Low-Cost Precursor Materials | +1.3% | Global | Medium-term to Long-term |

| Expansion into New End-Use Applications | +1.0% | Global | Short-term to Long-term |

| Advancements in Recycling Technologies | +0.9% | Europe, North America, Asia Pacific | Medium-term to Long-term |

| Growing Demand for Sustainable and Green Composites | +0.7% | Global | Medium-term |

Carbon Fibre Market Challenges Impact Analysis

The Carbon Fibre market, while promising, grapples with several inherent challenges that demand strategic attention to ensure sustained growth and broader adoption. One primary challenge is the capital-intensive nature of establishing and expanding carbon fibre production facilities. The significant investment required for polymerization, carbonization, and surface treatment equipment, coupled with the high operating costs, poses a barrier to entry for new players and can limit the pace of capacity expansion by existing manufacturers. This financial hurdle can lead to supply constraints during periods of peak demand.

Another persistent challenge relates to the standardization of carbon fibre products and composite manufacturing processes. The wide variety of carbon fibre types, sizing agents, and resin systems, combined with diverse composite manufacturing techniques, can lead to inconsistencies in material properties and final product performance. This lack of universal standards can complicate material selection, design, and qualification processes for engineers and end-users, thereby increasing development costs and time-to-market for new applications. Achieving greater standardization is critical for fostering wider industrial adoption.

Furthermore, the environmental footprint associated with traditional carbon fibre production, particularly the energy consumption during the carbonization process and the generation of volatile organic compounds (VOCs), presents a significant challenge. As industries increasingly prioritize sustainability and carbon neutrality, manufacturers are under pressure to develop more environmentally friendly production methods. Addressing these environmental concerns through process optimization, energy efficiency initiatives, and the development of greener technologies is crucial for the long-term viability and public perception of the carbon fibre industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Production Facilities | -0.6% | Global | Ongoing, Long-term |

| Lack of Standardization Across Products and Processes | -0.4% | Global | Ongoing, Medium-term |

| Environmental Impact of Traditional Production Methods | -0.3% | Global | Ongoing, Long-term |

| Managing Supply Chain Volatility for Precursors | -0.2% | Global | Short-term to Medium-term |

Carbon Fibre Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Carbon Fibre market, offering detailed insights into market size, growth trends, drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of various market segments, including precursor types, modulus types, forms, and diverse end-use industries across key geographical regions. It integrates a detailed forecast model to project market dynamics from 2025 to 2033, providing strategic perspectives for stakeholders. Additionally, the report incorporates an AI impact analysis and key company profiles to deliver a holistic understanding of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.2 Billion |

| Market Forecast in 2033 | USD 17.0 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Toray Industries Inc., Teijin Limited, Mitsubishi Chemical Corporation, Hexcel Corporation, SGL Carbon SE, Solvay SA, Hyosung Advanced Materials Corporation, DowAksa, Formosa Plastics Corporation, Jilin Chemical Fiber Group Co. Ltd., Zhongfu Shenying Carbon Fiber Co. Ltd., Jiangsu Hengshen Carbon Fiber Composite Materials Co. Ltd., Kureha Corporation, Anssen Carbon Fiber Technology Co., Ltd., Cytec Solvay Group, Fibre Glast Developments Corporation, Gurit Holding AG, Nippon Graphite Fiber Corporation, Rock West Composites, Weihai Guangwei Composites Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Carbon Fibre market is comprehensively segmented to provide a granular understanding of its diverse applications and material characteristics. This segmentation allows for precise analysis of market dynamics, growth opportunities, and competitive landscapes within specific product categories and end-use sectors. By dissecting the market along various dimensions, stakeholders can identify niche markets, assess market saturation, and formulate targeted strategies, ensuring a more informed and effective approach to market engagement and product development.

Understanding these segments is crucial for manufacturers, suppliers, and investors alike, as it highlights the varied performance requirements and cost sensitivities across different applications. For instance, the demands of the aerospace industry for high-modulus, continuous tow carbon fibre differ significantly from the requirements for chopped carbon fibre in automotive or industrial applications. This detailed breakdown facilitates a nuanced appreciation of market trends and the strategic positioning of products within the vast carbon fibre ecosystem.

- By Precursor Type: This segment analyzes carbon fibre based on the raw material from which it is derived.

- PAN-based: Carbon fibre produced from polyacrylonitrile, representing the most common and widely used type due to its high strength and stiffness.

- Pitch-based: Carbon fibre derived from petroleum or coal pitch, often used for applications requiring high thermal conductivity or specific stiffness.

- Rayon-based: Historically significant but less common now, used for specific applications like ablative materials.

- Others: Including emerging precursor materials like lignin, which offer potential for lower cost and increased sustainability.

- By Modulus: Categorizes carbon fibre based on its stiffness or Young's modulus.

- Standard Modulus (SM): Offers good strength and stiffness, suitable for general industrial and consumer applications.

- Intermediate Modulus (IM): Provides a balance of strength and stiffness, commonly used in aerospace and high-performance sporting goods.

- High Modulus (HM): Characterized by exceptional stiffness, critical for applications requiring minimal deformation under stress, such as satellite structures and high-end aerospace components.

- By Form: This segment classifies carbon fibre by its physical configuration.

- Continuous Tow Carbon Fiber: Long, continuous filaments used in weaving, filament winding, and prepreg manufacturing for structural applications.

- Chopped Carbon Fiber: Short, discrete fibres used in molding compounds for parts requiring isotropic properties or for cost-effective reinforcement.

- Milled Carbon Fiber: Pulverized fibres, often used as additives in resins or coatings for improved surface properties or conductivity.

- Fabrics: Woven or non-woven structures made from carbon fibre tow, providing specific mechanical properties and ease of handling in composite manufacturing.

- Composites: Refers to the final products made by combining carbon fibre with a matrix material (resin), representing the largest segment in terms of end-use value.

- Others: Includes specific forms like felts, papers, or specialized preforms.

- By End-Use Industry: Examines the primary sectors utilizing carbon fibre.

- Aerospace & Defense: For aircraft structures, missiles, spacecraft, and unmanned aerial vehicles (UAVs) due to lightweight and high strength requirements.

- Automotive: For structural components, body panels, and chassis in luxury, high-performance, and increasingly electric vehicles to reduce weight and enhance fuel efficiency or range.

- Wind Energy: Primarily for manufacturing large, stiff, and lightweight blades for wind turbines.

- Sports & Leisure: In equipment such as bicycles, golf clubs, tennis rackets, fishing rods, and racing equipment for performance enhancement.

- Building & Construction: For structural reinforcement, seismic retrofitting, and lightweight architectural elements.

- Marine: In high-performance boats, yachts, and naval vessels for weight reduction and increased speed.

- Medical: For prosthetics, imaging equipment (e.g., X-ray tables), and surgical instruments due to its biocompatibility and radiolucency.

- Electrical & Electronics: For EMI shielding, thermal management, and structural components in consumer electronics and industrial electrical systems.

- Others: Including industrial machinery, pressure vessels, offshore platforms, and infrastructure repair.

Regional Highlights

- North America: This region is a major market for carbon fibre, driven by robust demand from the aerospace and defense sectors, a strong automotive industry embracing lightweighting, and significant investments in research and development. The United States, in particular, leads in advanced composite manufacturing and has a high adoption rate in high-performance applications.

- Europe: Europe represents a mature and technologically advanced market, with substantial demand stemming from the automotive (including luxury and sports cars), wind energy, and aerospace industries. Germany, France, and the UK are key contributors, focusing on innovative manufacturing processes and sustainable carbon fibre solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC is characterized by rapidly expanding automotive production (especially EVs), increasing wind energy installations, and growing industrialization. Countries like China, Japan, South Korea, and India are investing heavily in domestic carbon fibre production capabilities and increasing adoption across diverse applications, including consumer goods and infrastructure.

- Latin America: An emerging market with growing demand in the automotive and construction sectors. Brazil and Mexico are key countries in this region, driven by expanding manufacturing bases and infrastructure development.

- Middle East and Africa (MEA): This region is showing increasing interest in carbon fibre for infrastructure projects, aerospace MRO (maintenance, repair, and overhaul), and the developing automotive industry. Investments in diversification and industrialization are expected to drive gradual growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Carbon Fibre Market.- Toray Industries Inc.

- Teijin Limited

- Mitsubishi Chemical Corporation

- Hexcel Corporation

- SGL Carbon SE

- Solvay SA

- Hyosung Advanced Materials Corporation

- DowAksa

- Formosa Plastics Corporation

- Jilin Chemical Fiber Group Co. Ltd.

- Zhongfu Shenying Carbon Fiber Co. Ltd.

- Jiangsu Hengshen Carbon Fiber Composite Materials Co. Ltd.

- Kureha Corporation

- Anssen Carbon Fiber Technology Co., Ltd.

- Cytec Solvay Group

- Fibre Glast Developments Corporation

- Gurit Holding AG

- Nippon Graphite Fiber Corporation

- Rock West Composites

- Weihai Guangwei Composites Co., Ltd.

Frequently Asked Questions

What is carbon fibre primarily used for?

Carbon fibre is predominantly used in industries requiring lightweight, high-strength, and high-stiffness materials. Key applications include aerospace (aircraft parts), automotive (electric vehicles, sports cars), wind energy (turbine blades), sports equipment (bicycles, golf clubs), and infrastructure reinforcement.

How is carbon fibre manufactured?

Carbon fibre is typically manufactured through a multi-step process involving the conversion of precursor materials, most commonly polyacrylonitrile (PAN) or pitch, through stabilization, carbonization (heating to extremely high temperatures in an inert atmosphere), and surface treatment to create strong, thin filaments.

Is carbon fibre expensive, and what drives its cost?

Yes, carbon fibre is generally more expensive than traditional materials like steel or aluminum. Its high cost is primarily driven by the high cost of precursor materials, the energy-intensive manufacturing process, and the specialized equipment and expertise required for production and composite fabrication.

What are the main benefits of using carbon fibre?

The primary benefits of carbon fibre include its exceptionally high strength-to-weight ratio, excellent stiffness, corrosion resistance, fatigue resistance, and ability to withstand high temperatures. These properties make it ideal for applications where weight reduction and structural integrity are critical.

Can carbon fibre be recycled?

While challenging, carbon fibre can be recycled using mechanical or chemical processes. Mechanical recycling involves shredding and grinding, yielding short fibres, while chemical methods recover the fibres by dissolving the resin. Advancements are being made to make carbon fibre recycling more economically viable and environmentally friendly, enabling a circular economy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted