Carbon Black Feed Stock Market

Carbon Black Feed Stock Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702676 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

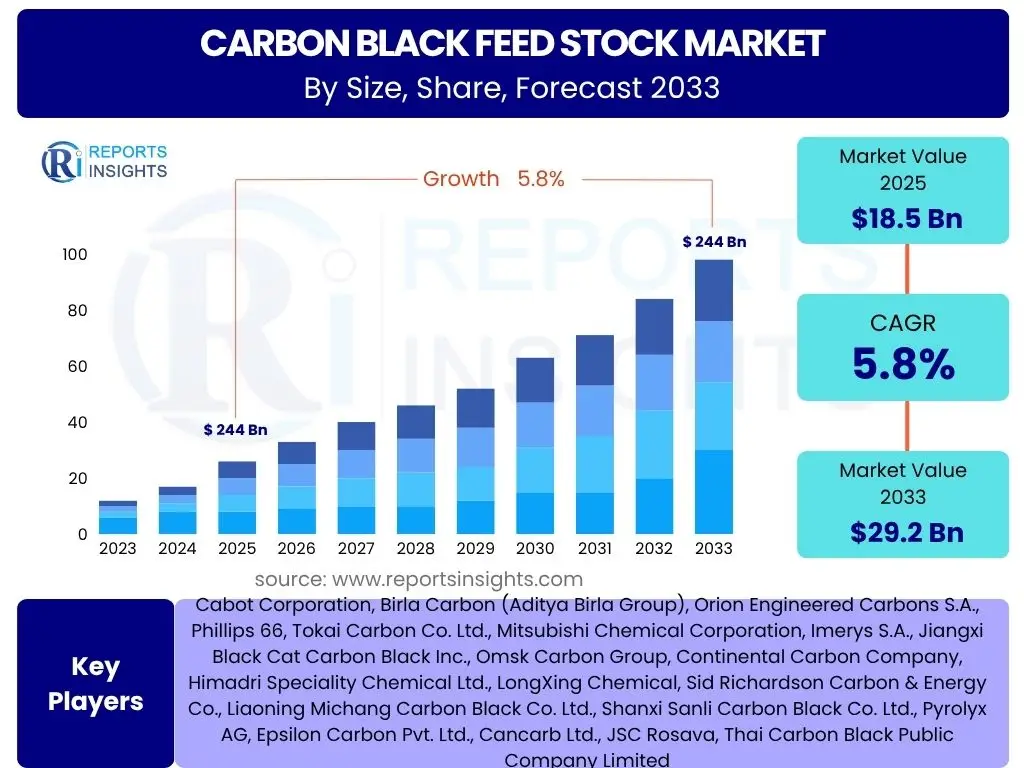

Carbon Black Feed Stock Market Size

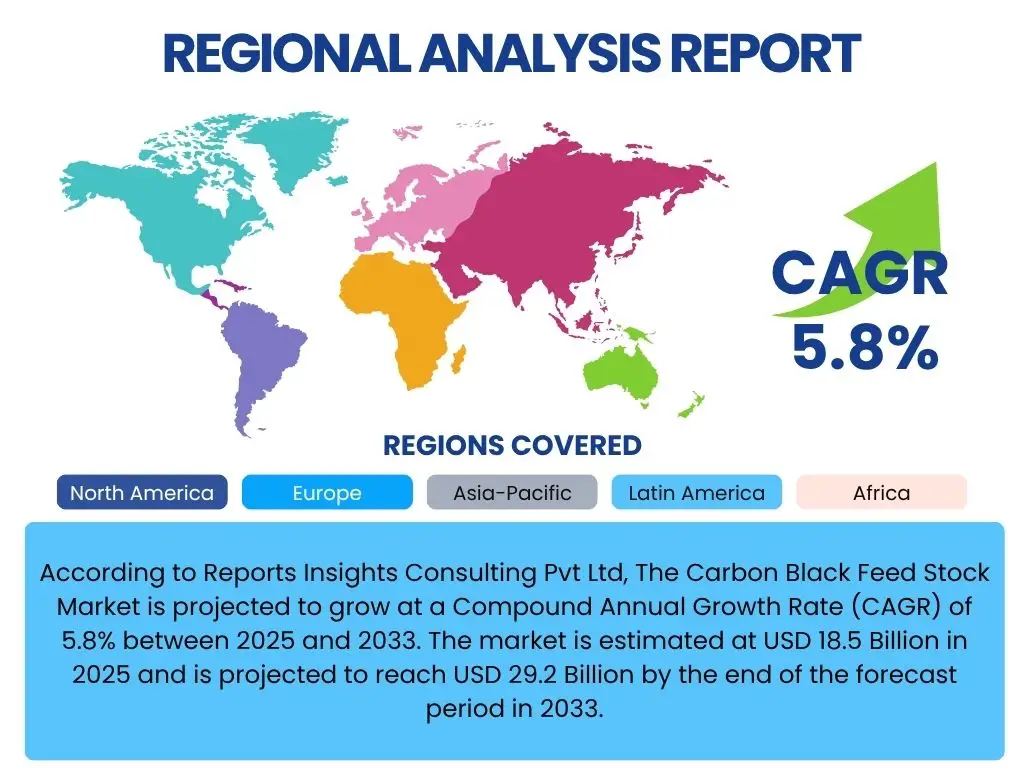

According to Reports Insights Consulting Pvt Ltd, The Carbon Black Feed Stock Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 29.2 Billion by the end of the forecast period in 2033.

Key Carbon Black Feed Stock Market Trends & Insights

The Carbon Black Feed Stock market is undergoing significant transformation driven by evolving industrial demands and increasing sustainability imperatives. A prominent trend is the growing emphasis on circular economy principles, leading to intensified research and development into alternative and recycled feedstocks. This shift aims to reduce reliance on traditional fossil fuel-derived materials and mitigate environmental impact, aligning with global efforts towards decarbonization and resource efficiency. Innovations in pyrolysis technology, particularly for end-of-life tires, are creating new avenues for feedstock supply, offering both environmental benefits and diversified sourcing options for carbon black producers.

Another critical insight centers on the dynamic interplay between raw material availability and geopolitical stability. Fluctuations in crude oil prices and supply chain disruptions have underscored the necessity for diversified feedstock portfolios, prompting market participants to explore non-traditional sources such as coal tar pitch and bio-based derivatives more vigorously. Furthermore, the burgeoning electric vehicle (EV) industry is driving demand for specialized carbon black grades used in high-performance tires and battery applications, influencing the types of feedstocks required and pushing innovation in carbon black properties. This demand for advanced materials necessitates feedstocks that can support superior product performance, leading to a focus on feedstock purity and composition.

Technological advancements in carbon black manufacturing processes are also shaping the market. Enhanced reactor designs and process optimization techniques are improving yield and quality, making feedstock utilization more efficient. Digitalization and automation are being integrated into production facilities to enhance operational efficiency, reduce waste, and improve consistency in feedstock processing. These technological shifts are not only improving the economics of carbon black production but also enabling manufacturers to adapt to changing feedstock characteristics, thus enhancing overall market resilience and adaptability to emerging industry standards and performance requirements.

- Increasing adoption of circular economy principles and recycled feedstocks.

- Rising demand for high-performance carbon black in electric vehicle tires and battery applications.

- Diversification of feedstock sources to mitigate geopolitical risks and price volatility.

- Technological advancements in pyrolysis and carbon black manufacturing processes.

- Focus on sustainability and reduced environmental footprint in feedstock sourcing.

AI Impact Analysis on Carbon Black Feed Stock

The integration of Artificial Intelligence (AI) and machine learning (ML) technologies is poised to significantly optimize various facets of the Carbon Black Feed Stock value chain. Common user questions revolve around how AI can enhance efficiency, improve quality, and provide predictive capabilities in a traditionally resource-intensive industry. AI algorithms can analyze vast datasets from feedstock sourcing, quality control, and production processes, identifying patterns and anomalies that human analysis might miss. This allows for more precise grading and selection of feedstocks, ensuring optimal input materials for carbon black production and reducing variations in the final product. Predictive analytics, powered by AI, can forecast feedstock availability and price fluctuations, enabling more strategic procurement decisions and mitigating supply chain risks effectively.

Furthermore, AI plays a crucial role in optimizing the carbon black manufacturing process itself. By continuously monitoring operational parameters such as temperature, pressure, and flow rates within reactors, AI systems can dynamically adjust conditions to maximize yield, improve product consistency, and minimize energy consumption. This level of real-time optimization leads to significant operational cost savings and a reduction in waste. Quality control is another area where AI offers substantial benefits; machine vision and predictive models can detect impurities or deviations in feedstock composition before they impact production, preventing costly batch failures and ensuring that the final carbon black meets stringent industry specifications. This proactive approach to quality assurance translates into higher product reliability and customer satisfaction.

Beyond production, AI is also influencing market dynamics by enhancing demand forecasting and logistics. By analyzing historical sales data, macroeconomic indicators, and even social media sentiment, AI models can provide more accurate predictions of future carbon black demand across various end-user industries. This improved foresight allows producers to optimize production schedules and inventory levels, reducing holding costs and ensuring timely delivery. In logistics, AI can optimize transportation routes and schedules for feedstock delivery and finished product distribution, leading to reduced fuel consumption, lower emissions, and improved delivery times. Overall, AI's impact on the carbon black feedstock market is characterized by enhanced efficiency, superior quality control, and data-driven decision-making across the entire supply chain, fostering greater resilience and competitiveness.

- AI-driven optimization of feedstock selection and grading for improved quality.

- Predictive analytics for feedstock price and supply chain risk management.

- Real-time process optimization in carbon black manufacturing for enhanced efficiency and yield.

- Advanced quality control and impurity detection using machine vision and AI models.

- Improved demand forecasting and logistics optimization for timely product delivery.

Key Takeaways Carbon Black Feed Stock Market Size & Forecast

The Carbon Black Feed Stock market is poised for robust expansion, driven primarily by sustained demand from key end-use industries and an increasing focus on feedstock innovation. Common user inquiries often center on the long-term growth trajectory and the underlying factors contributing to market resilience. The forecasted CAGR of 5.8% between 2025 and 2033, leading to a market value of USD 29.2 Billion, underscores a healthy growth outlook. This growth is intrinsically linked to the expanding automotive sector, particularly the tire industry, which remains the largest consumer of carbon black. As global vehicle production and replacement tire demand continue to rise, the need for reliable and high-quality feedstocks will similarly escalate, reinforcing the market's foundational stability.

A significant takeaway is the dual emphasis on both traditional market drivers and emerging sustainability trends. While the consumption of carbon black in conventional applications like industrial rubber products and plastics continues to provide a strong base, the market is increasingly influenced by environmental considerations. This includes the push for low-sulfur content feedstocks and the exploration of bio-based or recycled alternatives, which are viewed not just as regulatory responses but as critical opportunities for market differentiation and long-term viability. The integration of advanced technologies in feedstock processing and carbon black production further bolsters this positive forecast, enabling producers to meet evolving performance requirements and environmental standards more effectively.

Moreover, the market's geographical diversification and the growth in developing economies present substantial opportunities. Regions experiencing rapid industrialization and infrastructure development, particularly in Asia Pacific, are expected to contribute significantly to market expansion. The strategic focus on expanding production capacities and optimizing supply chains to cater to these growing regional demands is a critical factor supporting the upward trajectory of the market size and forecast. The market is not only growing in volume but also evolving in complexity, requiring adaptable and innovative feedstock solutions to meet the diverse needs of a global industrial landscape.

- Significant growth projected, reaching USD 29.2 Billion by 2033, primarily driven by automotive and industrial sectors.

- Dual focus on traditional demand and emerging sustainable feedstock solutions is shaping market evolution.

- Technological advancements in processing enhance feedstock utilization and product quality.

- Geographical expansion, particularly in Asia Pacific, is a key contributor to overall market growth.

- Market resilience is supported by diverse end-use applications and continuous product innovation.

Carbon Black Feed Stock Market Drivers Analysis

The Carbon Black Feed Stock market is significantly propelled by robust demand from its primary end-use industries, particularly the global tire manufacturing sector. As the automotive industry continues to grow, encompassing both new vehicle production and the vast replacement tire market, the consumption of carbon black, and by extension its feedstocks, escalates proportionally. Carbon black is an essential reinforcing filler in tires, imparting strength, durability, and resilience, making its demand directly correlated with vehicle sales and usage. Furthermore, the increasing complexity and performance demands of modern tires, including those for electric vehicles, necessitate higher quality and more specialized carbon black grades, which in turn drives demand for premium feedstocks.

Beyond tires, the expansion of industrial rubber products, plastics, and specialty applications also acts as a crucial driver. Carbon black is widely used in conveyor belts, hoses, seals, and various molded rubber goods, where its reinforcing properties are indispensable. In the plastics industry, it serves as a pigment, UV stabilizer, and conductive agent for a wide array of products ranging from automotive components to packaging materials. The continuous innovation in these sectors, coupled with global industrialization and infrastructure development, ensures a steady and increasing demand for carbon black feedstocks. Emerging applications, such as conductive carbon black for batteries and advanced materials for construction, are further diversifying the demand landscape.

Finally, the growing emphasis on higher performance and durability in manufactured goods globally contributes to the demand for carbon black feedstocks. Consumers and industries increasingly seek products that are more robust, long-lasting, and capable of performing under challenging conditions. Carbon black's unique properties, derived from its feedstock, are critical to achieving these performance benchmarks in various materials. This persistent drive for material excellence across multiple industries ensures that the fundamental need for high-quality carbon black feedstocks will continue to be a significant market driver, fostering investment in both conventional and advanced feedstock sourcing and processing technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Tire Industry | +1.5% | Global, particularly Asia Pacific, North America | Long-term |

| Expansion of Industrial Rubber Products & Plastics | +1.2% | Asia Pacific, Europe, North America | Medium to Long-term |

| Increasing Use in Specialty & Performance Applications | +0.8% | North America, Europe, China | Medium to Long-term |

| Economic Growth and Industrialization in Emerging Economies | +1.0% | Asia Pacific, Latin America, Africa | Long-term |

| Technological Advancements in Carbon Black Production | +0.5% | Global | Medium-term |

Carbon Black Feed Stock Market Restraints Analysis

The Carbon Black Feed Stock market faces significant restraints, primarily stemming from the volatility of crude oil prices, as a substantial portion of feedstocks like FCC slurry and ethylene cracking tar are petroleum-derived. Fluctuations in crude oil markets directly impact the cost of these raw materials, leading to unpredictable production costs for carbon black manufacturers. This price instability makes long-term planning challenging and can compress profit margins, especially for companies without diversified feedstock portfolios or robust hedging strategies. Such volatility can also deter investments in new production capacities, impacting the overall supply stability of carbon black feedstocks.

Stringent environmental regulations worldwide pose another substantial restraint. The production of carbon black and the use of its feedstocks are associated with emissions and waste generation, leading to increasing pressure from environmental agencies. Regulations targeting sulfur content, particulate matter emissions, and carbon dioxide footprints are compelling manufacturers to invest in costly abatement technologies and to seek cleaner, more sustainable feedstock alternatives. Compliance with these regulations not only adds to operational expenses but can also limit the availability of certain feedstocks that do not meet environmental standards, thereby narrowing the supply base and potentially increasing feedstock prices due to limited options.

Furthermore, the emergence of alternative materials and the increasing focus on circular economy initiatives present a growing challenge to traditional carbon black feedstock consumption. While the demand for carbon black remains strong, research into alternative reinforcing fillers and pigments (e.g., silica in tires) and the development of recycled carbon black (rCB) from end-of-life tires could potentially reduce the reliance on virgin feedstocks over the long term. Although rCB offers a sustainable solution, its quality and consistency need to match that of virgin carbon black to achieve widespread adoption, a factor that still presents a restraint in terms of immediate, large-scale displacement of conventional feedstocks. These factors collectively require the industry to adapt and innovate to maintain competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil Prices | -1.0% | Global | Short to Medium-term |

| Stringent Environmental Regulations | -0.8% | Europe, North America, China | Medium to Long-term |

| Development of Alternative Materials & rCB | -0.7% | Global | Long-term |

| Supply Chain Disruptions & Geopolitical Instability | -0.5% | Global | Short-term |

| High Capital Investment for New Production Facilities | -0.3% | Global | Long-term |

Carbon Black Feed Stock Market Opportunities Analysis

The Carbon Black Feed Stock market is presented with significant opportunities driven by the global shift towards sustainability and the circular economy. A major avenue for growth lies in the increasing adoption and technological advancement of bio-based and recycled feedstocks. As industries seek to reduce their carbon footprint and improve resource efficiency, the demand for feedstocks derived from renewable resources or waste streams, such as pyrolysis oil from end-of-life tires, is rising. This trend creates new market segments and value propositions for manufacturers capable of producing high-quality carbon black from these sustainable sources. Investment in R&D for efficient processing of these alternative feedstocks represents a substantial opportunity for future market leadership and compliance with evolving environmental standards.

Another compelling opportunity emerges from the rapid expansion of the electric vehicle (EV) sector. EVs place new and stringent demands on tire performance, requiring carbon black grades that enhance durability, reduce rolling resistance, and improve battery life. This drives the need for specialized carbon black, which in turn necessitates specific feedstock formulations and processing techniques. Furthermore, conductive carbon black, crucial for lithium-ion battery cathodes, is seeing a surge in demand directly linked to EV battery production. This niche but high-growth application opens up lucrative avenues for feedstock suppliers who can provide materials optimized for these advanced electrical and automotive applications, requiring precise control over feedstock quality and composition.

Lastly, the industrialization and economic growth in emerging economies, particularly in Asia Pacific, Latin America, and Africa, continue to present immense opportunities. These regions are experiencing significant growth in their automotive, construction, and manufacturing sectors, leading to a corresponding increase in demand for carbon black and its feedstocks. As these economies mature, there is also a rising emphasis on higher quality products and performance materials, creating a market for advanced carbon black grades. Localizing feedstock sourcing and production in these high-growth regions can provide a competitive advantage, reduce logistics costs, and capitalize on the expanding industrial base. These demographic and economic shifts offer long-term growth potential for the carbon black feedstock market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable & Recycled Feedstocks | +1.3% | Global | Long-term |

| Rising Demand from Electric Vehicle (EV) Sector | +1.0% | North America, Europe, China | Medium to Long-term |

| Growth in Emerging Economies & Industrialization | +0.9% | Asia Pacific, Latin America, Africa | Long-term |

| Technological Innovation in Specialty Carbon Black | +0.6% | Global | Medium-term |

| Digitalization & Supply Chain Optimization | +0.4% | Global | Short to Medium-term |

Carbon Black Feed Stock Market Challenges Impact Analysis

The Carbon Black Feed Stock market confronts several significant challenges, primarily centered on raw material supply chain complexity and geopolitical instability. As many traditional feedstocks like FCC slurry are by-products of the oil refining industry, their availability can be influenced by global refining capacities, crude oil supply, and geopolitical events. Disruptions such as conflicts, trade disputes, or natural disasters can severely impact the supply of these essential raw materials, leading to price spikes and production bottlenecks for carbon black manufacturers. Managing a diversified and resilient supply chain across different regions becomes a critical challenge, requiring robust risk management strategies and strategic partnerships to ensure consistent feedstock availability.

Another major challenge lies in the stringent regulatory environment and the increasing pressure for decarbonization. Carbon black production is an energy-intensive process, and the use of certain feedstocks can result in significant greenhouse gas emissions and other pollutants. Governments and environmental organizations worldwide are imposing stricter limits on emissions, demanding cleaner production processes and sustainable sourcing practices. This necessitates substantial capital investment in new technologies, emission control systems, and research into environmentally benign feedstocks. The high cost of compliance and the need to adapt to rapidly evolving environmental standards can pose a significant financial burden, particularly for smaller market players, and may influence production strategies and regional competitiveness.

Furthermore, the consistency and quality variability of certain feedstocks present ongoing operational challenges. While petroleum-derived feedstocks generally offer good consistency, the growing interest in alternative and recycled feedstocks introduces greater variability in composition and impurity levels. Ensuring that these diverse feedstocks can consistently produce high-quality carbon black that meets the demanding specifications of industries like tire manufacturing requires sophisticated process control and purification technologies. Overcoming these quality consistency issues for novel feedstocks is crucial for their wider adoption and for the carbon black industry to fully capitalize on sustainable sourcing opportunities, requiring continuous innovation in both feedstock pre-treatment and carbon black reactor technology.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Supply Chain Volatility & Geopolitical Risks | -0.9% | Global | Short to Medium-term |

| Stringent Environmental & Emissions Regulations | -0.8% | Europe, North America, China | Medium to Long-term |

| Quality Consistency of Alternative/Recycled Feedstocks | -0.6% | Global | Medium-term |

| High Energy Consumption & Operating Costs | -0.5% | Global | Short to Medium-term |

| Competition from Alternative Reinforcing Agents | -0.4% | Global | Long-term |

Carbon Black Feed Stock Market - Updated Report Scope

This report provides an in-depth analysis of the Carbon Black Feed Stock market, encompassing its current landscape, historical performance, and future projections. It delivers comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry. The scope covers detailed segmentation by feedstock type, application, and end-use industry, alongside a thorough regional analysis. The report also highlights the competitive landscape, profiling key players and their strategic initiatives, and assesses the impact of emerging technologies such as Artificial Intelligence on market dynamics. The objective is to equip stakeholders with actionable intelligence for strategic decision-making and market positioning within the global carbon black feedstock ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 29.2 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cabot Corporation, Birla Carbon (Aditya Birla Group), Orion Engineered Carbons S.A., Phillips 66, Tokai Carbon Co. Ltd., Mitsubishi Chemical Corporation, Imerys S.A., Jiangxi Black Cat Carbon Black Inc., Omsk Carbon Group, Continental Carbon Company, Himadri Speciality Chemical Ltd., LongXing Chemical, Sid Richardson Carbon & Energy Co., Liaoning Michang Carbon Black Co. Ltd., Shanxi Sanli Carbon Black Co. Ltd., Pyrolyx AG, Epsilon Carbon Pvt. Ltd., Cancarb Ltd., JSC Rosava, Thai Carbon Black Public Company Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Carbon Black Feed Stock market is comprehensively segmented to provide a detailed understanding of its diverse components and drivers. These segmentations allow for a granular analysis of market dynamics, identifying specific growth areas, competitive landscapes, and evolving consumer preferences across various applications and geographies. Understanding these segments is crucial for stakeholders to develop targeted strategies, optimize resource allocation, and capitalize on emerging opportunities within the complex carbon black value chain.

The primary segmentation divides the market based on the type of feedstock, acknowledging the different sources and chemical compositions that yield various carbon black grades suitable for distinct applications. Further segmentation by application highlights the primary industries consuming carbon black, from its dominant use in tires to its roles in industrial rubber, plastics, and more specialized fields. Lastly, the end-use industry segmentation provides insight into the broader sectors that drive demand for products containing carbon black, such as automotive, construction, and electronics. This multi-layered segmentation ensures a holistic view of the market structure and its underlying demand drivers.

- By Type:

- FCC Slurry (Fluid Catalytic Cracking Slurry Oil)

- Coal Tar Pitch

- Ethylene Tar

- Naphtha Tar

- Bio-based Feedstock

- Recycled Feedstock (Pyrolysis Oil)

- Others (e.g., Waste Tire Oil)

- By Application:

- Tires (Passenger Car Tires, Truck & Bus Tires, Off-road Tires)

- Industrial Rubber Products (Belts, Hoses, Gaskets, Seals)

- Plastics (Pipes, Films, Compounding, Masterbatches)

- Inks and Coatings (Printing Inks, Paints, Toners)

- Batteries (Lithium-ion Batteries, Lead-acid Batteries)

- Others (Pigments, Electrodes, Adhesives)

- By End-Use Industry:

- Automotive

- Industrial (Manufacturing, Heavy Machinery)

- Construction

- Electrical & Electronics

- Consumer Goods

Regional Highlights

- North America: Characterized by a mature automotive industry and increasing focus on specialty carbon black grades for high-performance applications. Stringent environmental regulations drive innovation in cleaner production processes and demand for sustainable feedstocks. Significant research and development activities in advanced materials and EV battery technologies contribute to growth.

- Europe: A hub for advanced manufacturing and automotive innovation, Europe demonstrates strong demand for carbon black feed stock. The region is at the forefront of implementing circular economy principles, leading to higher adoption rates of recycled and bio-based feedstocks. Strict environmental policies influence production practices and feedstock choices, pushing for lower emissions and sustainable sourcing.

- Asia Pacific (APAC): The largest and fastest-growing market, driven by rapid industrialization, burgeoning automotive production (especially in China, India, Japan, and South Korea), and expanding manufacturing bases. High demand for tires and industrial rubber products fuels the market. Significant investments in infrastructure development and electronics manufacturing further contribute to market expansion.

- Latin America: Exhibits steady growth, primarily influenced by the automotive sector and construction activities in countries like Brazil and Mexico. The region's market is sensitive to economic stability and raw material import costs, making local feedstock sourcing and diversified supply chains increasingly important.

- Middle East and Africa (MEA): Poised for growth due to developing industrial sectors, infrastructure projects, and increasing vehicle parc. The region's market is influenced by the availability of petroleum resources, which can serve as a direct source for feedstocks. Investments in manufacturing capabilities are gradually increasing demand for carbon black feed stock.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Carbon Black Feed Stock Market.- Cabot Corporation

- Birla Carbon (Aditya Birla Group)

- Orion Engineered Carbons S.A.

- Phillips 66

- Tokai Carbon Co. Ltd.

- Mitsubishi Chemical Corporation

- Imerys S.A.

- Jiangxi Black Cat Carbon Black Inc.

- Omsk Carbon Group

- Continental Carbon Company

- Himadri Speciality Chemical Ltd.

- LongXing Chemical

- Sid Richardson Carbon & Energy Co.

- Liaoning Michang Carbon Black Co. Ltd.

- Shanxi Sanli Carbon Black Co. Ltd.

- Pyrolyx AG

- Epsilon Carbon Pvt. Ltd.

- Cancarb Ltd.

- JSC Rosava

- Thai Carbon Black Public Company Limited

Frequently Asked Questions

Analyze common user questions about the Carbon Black Feed Stock market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is carbon black feed stock?

Carbon black feedstock refers to the petroleum-derived or alternative raw materials used in the furnace black process to produce carbon black. Common types include FCC slurry oil, coal tar pitch, ethylene tar, and increasingly, bio-based or recycled oils derived from waste tires.

What are the primary applications of carbon black produced from these feedstocks?

The primary applications of carbon black are as a reinforcing filler in tires and other industrial rubber products, a pigment and UV stabilizer in plastics, and an additive in inks, coatings, and increasingly, in battery electrodes for electric vehicles.

What are the main drivers for the growth of the Carbon Black Feed Stock market?

Key drivers include the expanding global automotive industry (especially tire demand), growth in industrial rubber and plastics sectors, increasing demand for specialty carbon black grades in new applications like EVs and conductive materials, and overall industrialization in emerging economies.

What challenges does the Carbon Black Feed Stock market face?

Major challenges include the volatility of crude oil prices impacting feedstock costs, stringent environmental regulations on emissions, supply chain disruptions, and the need to ensure consistent quality from alternative or recycled feedstocks.

How is sustainability impacting the Carbon Black Feed Stock market?

Sustainability is driving significant innovation, leading to increased research and adoption of bio-based and recycled feedstocks (e.g., from pyrolysis of end-of-life tires). It also pushes for cleaner production processes and reduced environmental footprint across the value chain to meet global environmental standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted