Carbon Capture And Storage Market

Carbon Capture And Storage Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700537 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

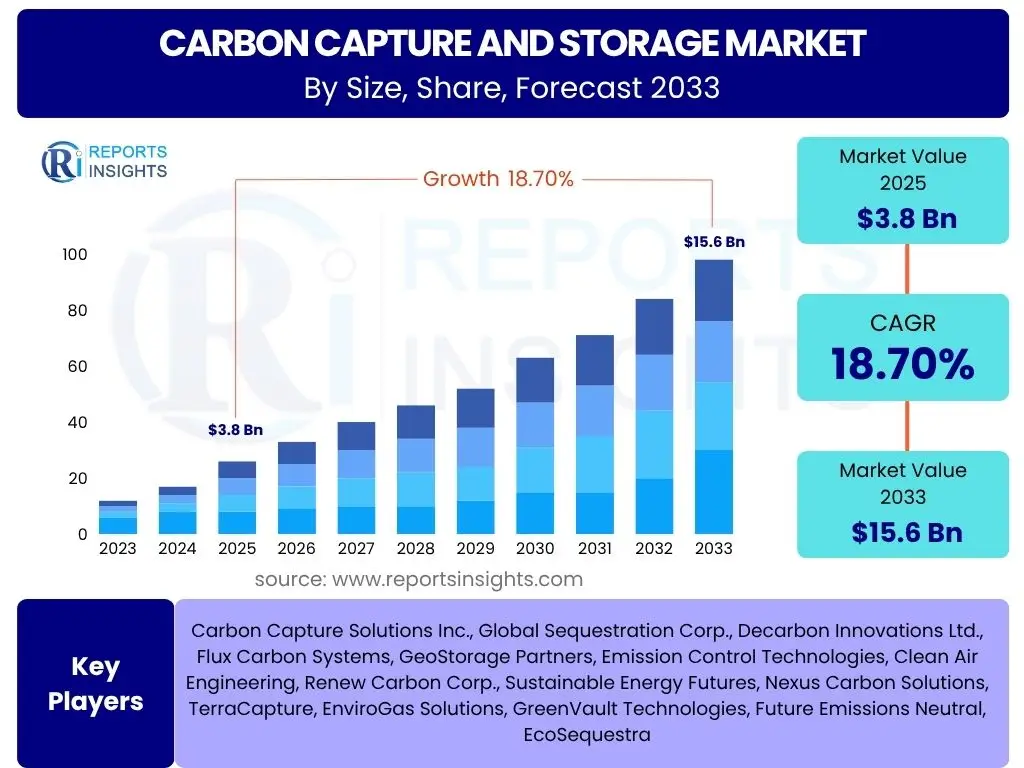

Carbon Capture And Storage Market Size

Carbon Capture And Storage Market is projected to grow at a Compound annual growth rate (CAGR) of 18.7% between 2025 and 2033, valued at USD 3.8 billion in 2025 and is projected to grow to USD 15.6 billion by 2033 the end of the forecast period.

Key Carbon Capture And Storage Market Trends & Insights

The Carbon Capture And Storage (CCS) market is experiencing dynamic growth driven by evolving global climate policies and increasing industrial commitments to decarbonization. Key trends shaping this market include the rapid scaling of CCS projects, significant advancements in capture technologies, and the growing emphasis on carbon utilization (CCU) for value creation. Furthermore, cross-sectoral collaborations are becoming more prevalent, fostering integrated solutions across various heavy industries. This evolution signifies a shift from nascent project development to a more mature and interconnected global CCS infrastructure.

- Rising governmental investments and policy support for decarbonization initiatives.

- Technological innovations enhancing capture efficiency and reducing operational costs.

- Increased focus on Direct Air Capture (DAC) as a complementary carbon removal solution.

- Expanding applications of Carbon Capture, Utilization, and Storage (CCUS) across diverse industries.

- Growing corporate commitments to Net Zero targets driving demand for CCS solutions.

- Development of large-scale industrial hubs for shared CO2 transport and storage infrastructure.

- Emergence of carbon credit markets incentivizing CCS deployment.

- Standardization of measurement, reporting, and verification (MRV) protocols for CO2 storage.

AI Impact Analysis on Carbon Capture And Storage

Artificial Intelligence (AI) is set to revolutionize the Carbon Capture and Storage (CCS) industry by optimizing complex processes, enhancing efficiency, and reducing operational expenditures across the entire value chain. AI-powered analytics can significantly improve the performance of capture technologies, predict equipment failures, and enable smarter decisions in CO2 transportation and geological storage. This integration of AI is not merely an incremental improvement but a transformative force, enabling more cost-effective and scalable CCS solutions essential for global decarbonization efforts.

- Optimization of CO2 capture processes through real-time data analysis and predictive modeling, leading to higher efficiency and lower energy consumption.

- Enhanced site selection and characterization for geological storage using AI algorithms to analyze vast geological datasets and identify optimal reservoirs.

- Predictive maintenance for CCS infrastructure, including pipelines and capture facilities, minimizing downtime and operational risks.

- Improved monitoring, verification, and reporting (MRV) of stored CO2 through AI-driven sensor networks and anomaly detection, ensuring long-term containment integrity.

- Development of smart control systems for autonomous operation of CCS plants, adapting to varying industrial loads and CO2 concentrations.

- Simulation and modeling of complex CO2 injection and plume migration scenarios, reducing uncertainties in storage capacity and safety.

- Accurate forecasting of carbon emissions and the effectiveness of capture strategies across industrial facilities, aiding in strategic planning.

- Streamlined supply chain and logistics for CO2 transport, optimizing routes and scheduling for improved cost-effectiveness.

Key Takeaways Carbon Capture And Storage Market Size & Forecast

- Robust market expansion projected at an 18.7% CAGR from 2025 to 2033, reaching USD 15.6 billion.

- Driven by stringent environmental regulations, corporate net-zero commitments, and carbon pricing.

- High capital expenditure and complex regulatory landscape pose primary restraints.

- Opportunities arise from Direct Air Capture (DAC) and Carbon Capture Utilization (CCU) advancements.

- Technological scalability and infrastructure development remain key challenges.

- North America and Europe lead in project deployment and policy support.

- AI integration is optimizing process efficiency and reducing operational costs across the CCS value chain.

- The market is shifting towards large-scale industrial clusters and cross-sectoral collaborations.

Carbon Capture And Storage Market Drivers Analysis

The Carbon Capture And Storage market is primarily propelled by an urgent global imperative to mitigate climate change, translated into a robust framework of environmental policies and economic incentives. Governments worldwide are increasingly enacting stricter emissions regulations, alongside implementing carbon pricing mechanisms, which significantly elevate the financial viability of CCS projects. Concurrently, major corporations are committing to ambitious decarbonization targets, viewing CCS as a critical pathway to achieve net-zero emissions, especially in hard-to-abate sectors. These factors collectively create a compelling demand-side push for CCS solutions, fostering technological advancements and stimulating investment across the value chain. This convergence of policy mandates, corporate responsibility, and economic drivers forms the bedrock of the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Global Environmental Regulations and Policies | +4.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Growing Corporate Decarbonization and Net-Zero Commitments | +3.8% | Global, especially OECD countries and multinational corporations | Mid to Long-term (2027-2033) |

| Implementation of Carbon Pricing and Emissions Trading Schemes | +3.2% | Europe, North America, parts of Asia (China, South Korea) | Short to Mid-term (2025-2030) |

| Advancements in Capture, Transport, and Storage Technologies | +2.9% | Global, driven by R&D in developed economies | Mid to Long-term (2028-2033) |

| Government Funding and Incentives for CCS Projects | +2.3% | North America (IRA, 45Q), Europe (Innovation Fund), Australia | Short to Mid-term (2025-2029) |

| Increasing Demand from Hard-to-Abate Industries (Cement, Steel, Chemicals) | +2.0% | Global, wherever heavy industry is prevalent | Mid to Long-term (2026-2033) |

Carbon Capture And Storage Market Restraints Analysis

Despite significant growth potential, the Carbon Capture And Storage market faces substantial restraints that could impede its widespread adoption and dampen its growth trajectory. The most prominent barrier remains the prohibitively high capital expenditure required for designing, constructing, and deploying CCS facilities, making it a challenging investment for many industries without robust financial incentives. This high initial cost is often coupled with operational complexities and significant energy penalties associated with the capture process itself. Furthermore, regulatory uncertainties in various regions, particularly regarding long-term liability for stored CO2 and the absence of harmonized frameworks, deter investment. Public perception issues, sometimes fueled by environmental concerns or skepticism about long-term storage safety, also contribute to resistance. These factors collectively create a challenging environment for accelerated CCS deployment, necessitating a concerted effort from policymakers and industry stakeholders to mitigate their impact.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Operating Costs | -4.0% | Global, affects all project scales and regions | Short to Mid-term (2025-2030) |

| Lack of Clear and Consistent Regulatory Frameworks | -3.5% | Many emerging markets, some European countries, inconsistent global standards | Short to Mid-term (2025-2029) |

| Public Perception and Social License to Operate Issues | -2.8% | Local communities near proposed storage sites, often developed countries | Ongoing throughout forecast period |

| Geological Storage Site Availability and Characterization Challenges | -2.2% | Regions with limited suitable geology or insufficient data (e.g., parts of Asia, Africa) | Mid to Long-term (2028-2033) |

| Energy Penalty Associated with CO2 Capture | -1.9% | Global, inherent technical challenge across all capture technologies | Ongoing throughout forecast period |

Carbon Capture And Storage Market Opportunities Analysis

The Carbon Capture And Storage market is rich with burgeoning opportunities poised to accelerate its deployment and expand its economic viability. A significant avenue for growth lies in the emergence of Direct Air Capture (DAC) technologies, which offer a pathway to address historical emissions and diffuse sources, complementing traditional point-source capture. Furthermore, the burgeoning field of Carbon Capture, Utilization, and Storage (CCUS) presents an attractive economic incentive, transforming CO2 from a waste product into a valuable feedstock for various industries, thereby offsetting capture costs. The development of large-scale CO2 transport and storage hubs, coupled with international collaborations, promises to unlock economies of scale and de-risk individual projects. As the global push for decarbonization intensifies across hard-to-abate sectors, the demand for integrated CCS solutions is set to surge, opening new markets and innovation pathways.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Carbon Capture, Utilization, and Storage (CCUS) Applications | +3.5% | Global, particularly in industries seeking circular economy solutions | Mid to Long-term (2027-2033) |

| Emergence and Scaling of Direct Air Capture (DAC) Technologies | +3.0% | North America, Europe, regions with strong R&D funding | Mid to Long-term (2028-2033) |

| Development of Large-Scale Industrial CCS Hubs and Clusters | +2.8% | North America (Gulf Coast), Europe (North Sea), Australia | Short to Mid-term (2025-2030) |

| Increased Investment in Research and Development for Cost Reduction | +2.5% | Global, especially academic and corporate research centers | Ongoing throughout forecast period |

| International Collaboration and Cross-Border CO2 Transport Initiatives | +2.0% | Europe (Northern Lights project), potential for Asian and North American links | Mid to Long-term (2029-2033) |

Carbon Capture And Storage Market Challenges Impact Analysis

The Carbon Capture And Storage market faces several inherent challenges that demand innovative solutions and concerted efforts from stakeholders to overcome. A primary concern is the significant technical complexity involved in scaling up capture technologies from pilot to commercial-scale deployment, particularly for diverse industrial flue gas compositions. This is compounded by the long project development cycles, often spanning a decade or more from conceptualization to operation, which introduces substantial financial and regulatory uncertainties. The necessity for extensive infrastructure development, including pipelines and storage facilities, requires massive upfront investment and coordinated planning across multiple sectors. Furthermore, achieving broad public acceptance, especially for CO2 transportation and geological storage, remains a persistent challenge, necessitating transparent communication and engagement strategies to build trust. Addressing these multifaceted challenges is crucial for unlocking the full potential of CCS as a vital climate mitigation tool.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability and Commercial Viability of Capture Technologies | -3.2% | Global, particularly for nascent technologies or diverse industrial applications | Short to Mid-term (2025-2030) |

| Long Project Development Cycles and Permitting Processes | -2.8% | Global, dependent on national and local regulatory efficiencies | Ongoing throughout forecast period |

| Development of Robust CO2 Transport and Storage Infrastructure | -2.5% | Regions lacking existing pipeline networks or comprehensive geological mapping | Mid to Long-term (2028-2033) |

| Achieving Social License and Public Acceptance for CCS Projects | -2.0% | Specific communities near proposed project sites, global media influence | Ongoing throughout forecast period |

| Inter-Sectoral Coordination and Value Chain Integration | -1.7% | Global, requiring collaboration between industrial emitters, transporters, and storage operators | Short to Mid-term (2025-2029) |

Carbon Capture And Storage Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Carbon Capture and Storage (CCS) market, offering critical insights into its current landscape, future projections, and the underlying dynamics shaping its evolution. The report details market size estimations, growth drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. It covers key market trends, the impact of AI, and a meticulous segmentation analysis to offer granular understanding across technologies, services, end-use industries, and geographical regions, equipping stakeholders with actionable intelligence for navigating this vital decarbonization sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 billion |

| Market Forecast in 2033 | USD 15.6 billion |

| Growth Rate | 18.7% CAGR from 2025 to 2033 |

| Number of Pages | 268 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Carbon Capture Solutions Inc., Global Sequestration Corp., Decarbon Innovations Ltd., Flux Carbon Systems, GeoStorage Partners, Emission Control Technologies, Clean Air Engineering, Renew Carbon Corp., Sustainable Energy Futures, Nexus Carbon Solutions, TerraCapture, EnviroGas Solutions, GreenVault Technologies, Future Emissions Neutral, EcoSequestra |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Carbon Capture and Storage (CCS) market is extensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This detailed breakdown allows for a precise analysis of technological preferences, service demands, industry-specific adoption patterns, and geological storage capabilities. Understanding these segmentations is crucial for stakeholders to identify niche opportunities, allocate resources effectively, and develop targeted strategies that align with specific market needs and technological readiness levels. The multi-dimensional segmentation ensures a comprehensive view of the market's structure and potential growth areas, enabling informed decision-making in a rapidly evolving decarbonization landscape.

- By Technology: This segment analyzes the various methods employed for capturing CO2 emissions from industrial sources and the atmosphere.

- Pre-Combustion Capture: Involves converting fossil fuels into a mixture of hydrogen and carbon dioxide before combustion, making CO2 easier to separate. This method is often applied in integrated gasification combined cycle (IGCC) power plants.

- Post-Combustion Capture: The most mature and widely applicable technology, separating CO2 from flue gases after fuel combustion. It is suitable for retrofitting existing power plants and industrial facilities.

- Oxy-Fuel Combustion Capture: Burns fuel in a mixture of oxygen and recycled flue gas instead of air, resulting in a flue gas that is mostly CO2 and water vapor, simplifying CO2 separation.

- Direct Air Capture (DAC): A more nascent but rapidly developing technology that removes CO2 directly from ambient air, offering a solution for diffuse emissions and historical carbon.

- By Service: This segment delineates the distinct stages involved in the CCS value chain, from emission source to permanent storage or utilization.

- Capture: Encompasses the technologies and processes used to separate CO2 from industrial flue gas streams or the atmosphere.

- Transportation: Involves the methods and infrastructure for moving captured CO2, primarily via pipelines, ships, or trucks, from the capture site to the storage or utilization facility.

- Storage: Refers to the long-term, secure geological sequestration of CO2, typically in deep saline aquifers, depleted oil and gas reservoirs, or unmineable coal seams.

- Utilization (CCU): Focuses on converting captured CO2 into commercially valuable products such as building materials, fuels, chemicals, or for enhanced oil recovery (EOR).

- By End-Use Industry: This segment examines the primary industrial sectors that are adopting or are anticipated to adopt CCS solutions to decarbonize their operations.

- Power Generation: Includes coal-fired and natural gas-fired power plants, which are significant point sources of CO2 emissions.

- Oil & Gas: Encompasses facilities involved in hydrocarbon processing, including refineries, gas processing plants, and also for enhanced oil recovery (EOR) operations.

- Cement: The cement industry is a major emitter due to both energy consumption and process emissions from calcination.

- Iron & Steel: Another hard-to-abate sector with substantial process emissions during steelmaking.

- Chemicals: Various chemical production processes generate significant CO2 emissions, particularly in ammonia and hydrogen production.

- Others: Includes other industrial sectors such as pulp and paper, waste-to-energy, glass manufacturing, and hydrogen production from fossil fuels.

- By Storage Type: This segment differentiates between the various geological formations utilized for the secure and permanent sequestration of CO2.

- Saline Aquifers: Deep rock formations saturated with saline water, offering vast potential for CO2 storage due to their extensive capacity.

- Depleted Oil & Gas Fields: Former hydrocarbon reservoirs that have proven containment characteristics and existing infrastructure for CO2 injection.

- Coal Seams: Unmineable coal seams can absorb CO2, potentially releasing methane that can be captured and utilized (ECBM).

- Basalt Formations: Volcanic rock formations that react with CO2 to form stable carbonate minerals, offering a permanent mineralization pathway.

- By Application: This segment categorizes the primary application areas where CCS technologies are deployed to mitigate emissions.

- Industrial Carbon Capture: Focuses on capturing CO2 from a wide range of industrial processes beyond power generation, such as cement, steel, chemicals, and fertilizers.

- Power Plant Carbon Capture: Specifically targets the capture of CO2 emissions from fossil fuel-fired power generation facilities.

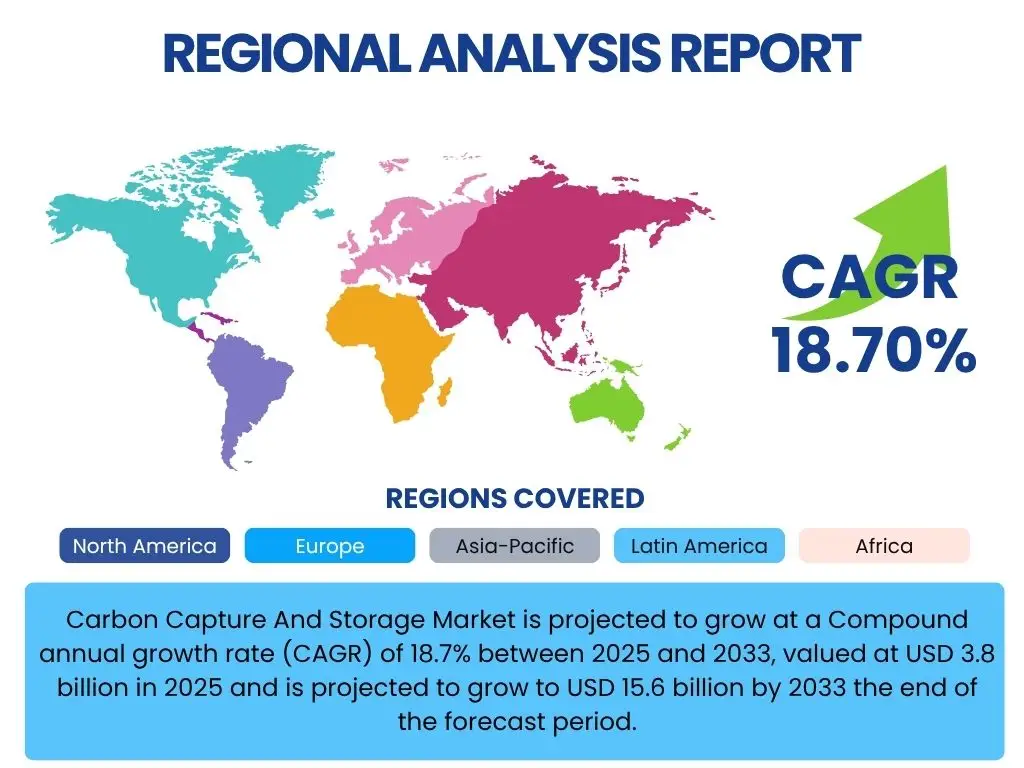

Regional Highlights

The global Carbon Capture and Storage (CCS) market exhibits distinct regional dynamics, influenced by varying policy landscapes, industrial concentrations, and geological endowments. Each region contributes uniquely to the market's growth, with certain areas emerging as pioneers due to strong governmental support and significant investment in large-scale projects. Understanding these regional highlights is crucial for identifying key growth epicenters and strategic investment opportunities in the global decarbonization effort.

- North America: This region stands as a significant leader in the Carbon Capture and Storage market, primarily driven by robust government incentives such as the 45Q tax credit in the United States, which provides substantial financial support for CCS projects. The region possesses extensive geological storage potential, particularly along the Gulf Coast, facilitating the development of large-scale CO2 transport and storage hubs. Canada also shows strong commitment with significant project pipelines and a focus on industrial decarbonization. The presence of a mature oil and gas industry further aids in leveraging existing infrastructure and expertise for CO2 sequestration, particularly for Enhanced Oil Recovery (EOR) and dedicated geological storage.

- Europe: Europe is a frontrunner in CCS deployment, propelled by ambitious climate targets set by the European Union and national governments, alongside carbon pricing mechanisms like the EU Emissions Trading System (ETS). Countries such as Norway, the Netherlands, and the United Kingdom are spearheading major CCS projects, including cross-border initiatives like the Northern Lights project, which aims to establish an open-source CO2 transport and storage infrastructure in the North Sea. The region's emphasis on industrial decarbonization across sectors like cement, steel, and chemicals is a key factor, with significant funding from programs like the EU Innovation Fund fostering technological development and large-scale demonstrations.

- Asia Pacific (APAC): The APAC region is poised for substantial growth in the CCS market, driven by its rapid industrialization and increasing awareness of environmental sustainability, particularly in countries like China, Japan, and Australia. China, as the world's largest emitter, is making significant strides in CCS research, development, and pilot projects, recognizing its necessity for meeting climate goals. Australia is leveraging its vast geological storage potential and expertise from its natural gas industry to develop large-scale CCS projects, especially in the context of hydrogen production with carbon capture. Japan and South Korea are also investing in CCUS technologies, focusing on hard-to-abate industries and exploring international CO2 storage solutions.

- Latin America: While still in nascent stages compared to other regions, Latin America holds considerable potential for CCS, largely due to its significant oil and gas reserves and the presence of heavy industries. Countries like Brazil and Mexico are exploring opportunities for CCUS, particularly for enhanced oil recovery (EOR) and reducing emissions from their industrial sectors. The region's development is expected to accelerate with increasing international collaboration and the establishment of supportive policy frameworks to unlock its geological storage capacity and industrial decarbonization needs.

- Middle East and Africa (MEA): The MEA region is emerging as a critical hub for CCS, primarily driven by oil and gas producing nations like Saudi Arabia and the United Arab Emirates. These countries are investing heavily in CCUS projects, often linked with enhanced oil recovery (EOR) and hydrogen production, to diversify their energy economies and reduce carbon footprints. The region possesses vast, well-characterized geological storage potential in its depleted oil and gas fields and saline aquifers. Africa, while having fewer operational projects, holds significant long-term potential for geological storage and is increasingly exploring CCS as part of its sustainable development agenda, particularly as industrialization progresses.

Top Key Players:

The market research report covers the analysis of key stake holders of the Carbon Capture And Storage Market. Some of the leading players profiled in the report include -- Carbon Capture Solutions Inc.

- Global Sequestration Corp.

- Decarbon Innovations Ltd.

- Flux Carbon Systems

- GeoStorage Partners

- Emission Control Technologies

- Clean Air Engineering

- Renew Carbon Corp.

- Sustainable Energy Futures

- Nexus Carbon Solutions

- TerraCapture

- EnviroGas Solutions

- GreenVault Technologies

- Future Emissions Neutral

- EcoSequestra

- CCS Alliance Group

- Climate Vault Innovations

- BlueCarbon Technologies

- Strategic Carbon Partners

- Evergreen Carbon Management

Frequently Asked Questions:

What is Carbon Capture and Storage (CCS)?

Carbon Capture and Storage (CCS) is a technology that captures carbon dioxide (CO2) emissions from large point sources, such as power plants and industrial facilities, and prevents it from entering the atmosphere. The captured CO2 is then transported, typically by pipeline, and stored permanently underground in geological formations like deep saline aquifers or depleted oil and gas fields, ensuring long-term containment.

How does Carbon Capture and Storage work?

CCS involves three main stages: First, capture, where CO2 is separated from other gases produced by industrial processes or directly from the air using various technologies like absorption or membrane separation. Second, transportation, where the captured CO2 is compressed and moved via pipelines, ships, or trucks to a suitable storage site. Third, storage, where the CO2 is injected deep underground into secure geological formations for permanent sequestration.

What are the primary benefits of Carbon Capture and Storage?

The primary benefits of CCS include significant greenhouse gas emissions reduction from heavy industries and power generation, critical for meeting global climate targets. It enables continued use of existing infrastructure while decarbonizing operations, supports the production of low-carbon hydrogen, and offers a pathway for achieving net-zero emissions, especially in hard-to-abate sectors where alternative decarbonization options are limited or more costly.

What are the main challenges facing the Carbon Capture and Storage market?

Key challenges in the CCS market include high upfront capital costs and operational expenses for capture technologies, which can hinder project viability. Regulatory uncertainties and a lack of consistent policy frameworks in many regions also create investment barriers. Furthermore, overcoming public perception issues regarding the safety and long-term integrity of CO2 storage, along with developing extensive CO2 transport infrastructure, remain significant hurdles to widespread adoption.

What is the projected growth rate for the Carbon Capture and Storage market?

The Carbon Capture and Storage market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. This robust growth trajectory is expected to increase the market size from an estimated USD 3.8 billion in 2025 to USD 15.6 billion by the end of the forecast period in 2033, driven by increasing climate action and industrial decarbonization efforts globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted