Carbon Black Market

Carbon Black Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704019 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

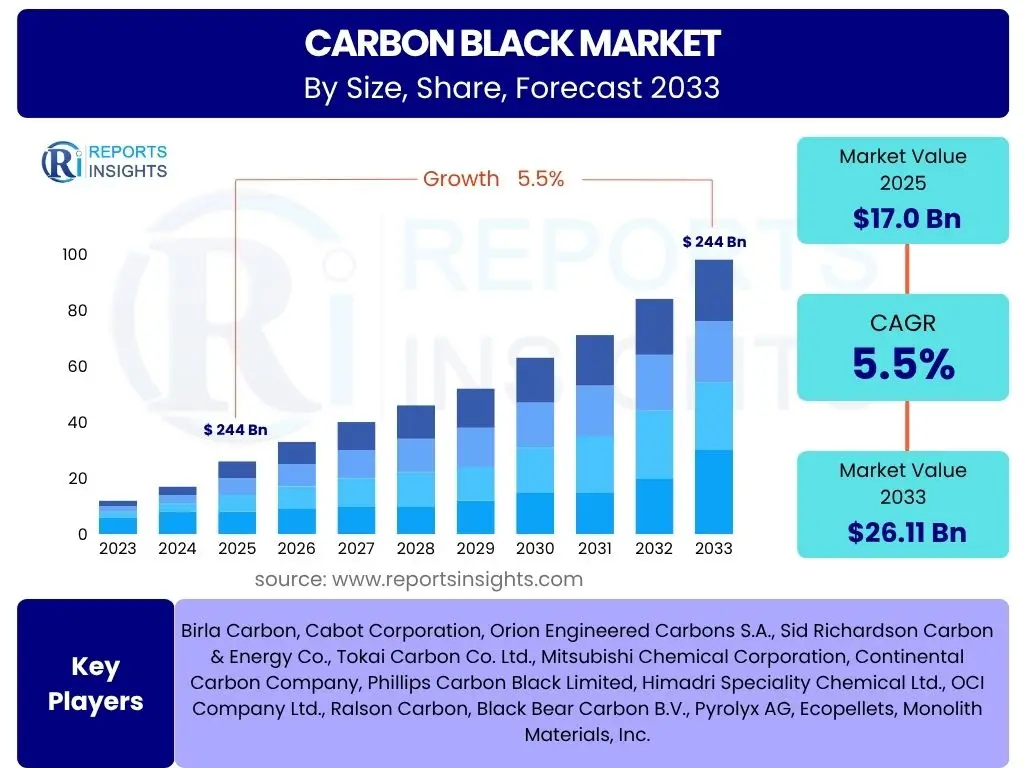

Carbon Black Market Size

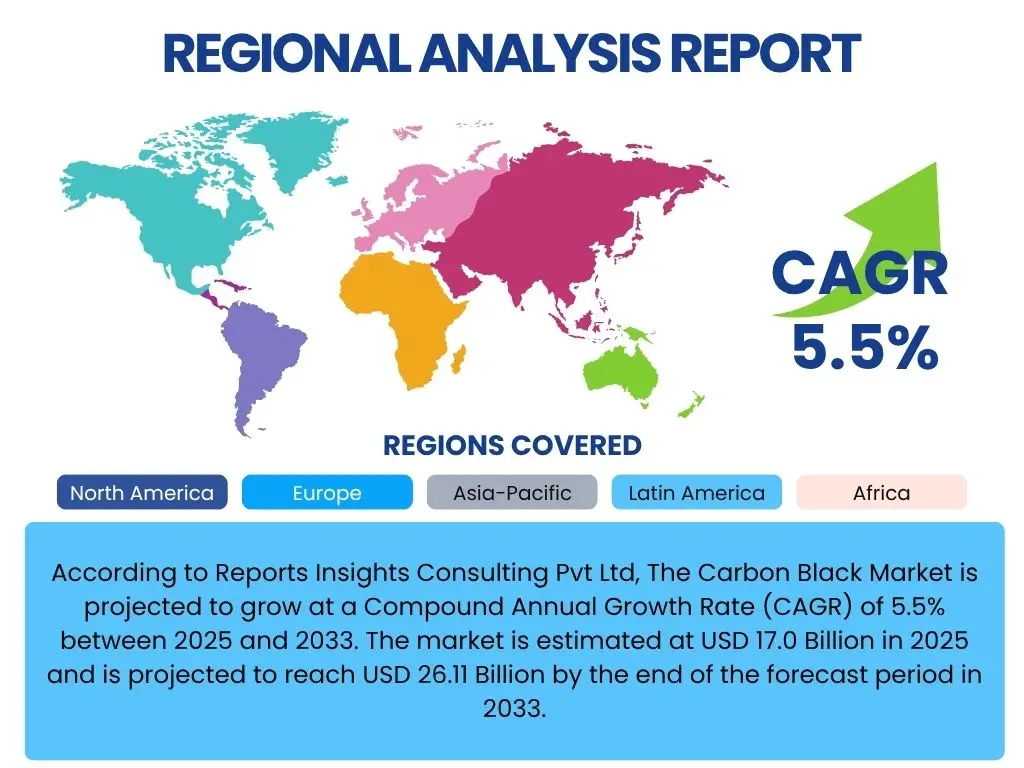

According to Reports Insights Consulting Pvt Ltd, The Carbon Black Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 17.0 Billion in 2025 and is projected to reach USD 26.11 Billion by the end of the forecast period in 2033.

Key Carbon Black Market Trends & Insights

Analysis of user inquiries concerning carbon black market trends reveals a strong interest in sustainable manufacturing practices, the impact of electric vehicle adoption, and the diversification of applications beyond traditional rubber products. Users frequently seek information on how environmental regulations influence market dynamics and the emergence of novel production methods. There is also significant curiosity regarding the shift towards specialty carbon black grades and their increasing importance in advanced materials. The market's evolution is closely tied to global industrial growth and technological advancements, prompting a demand for insights into future demand patterns and competitive landscapes.

Furthermore, common questions revolve around the geopolitical implications for raw material sourcing, particularly crude oil derivatives, and the strategic responses of leading manufacturers to these challenges. The push for circular economy principles, especially in the tire industry, is a recurring theme, with users keen to understand the viability and market penetration of recovered carbon black (rCB). Innovation in carbon black functionalities, such as enhanced conductivity or UV protection, also garners considerable attention, indicating a market moving towards higher-value applications.

- Increasing demand for specialty carbon black in high-performance applications like coatings, plastics, and conductive materials.

- Growing adoption of sustainable and recovered carbon black (rCB) due to environmental regulations and circular economy initiatives.

- Significant growth driven by the electric vehicle (EV) sector, particularly for high-performance tires and battery components.

- Technological advancements in carbon black production processes aimed at reducing energy consumption and environmental footprint.

- Regional shifts in manufacturing capabilities, with a pronounced focus on Asia Pacific for both production and consumption.

- Development of carbon black variants with enhanced properties for specific industrial applications, expanding market versatility.

AI Impact Analysis on Carbon Black

Common user questions regarding AI's impact on the carbon black industry primarily focus on process optimization, supply chain efficiency, and the potential for accelerated research and development. Users are keen to understand how artificial intelligence can enhance production yields, improve quality consistency, and mitigate operational risks within manufacturing plants. There is also significant interest in AI's role in predictive maintenance, aiming to reduce downtime and extend the lifespan of machinery used in carbon black production, directly influencing cost efficiencies and operational reliability.

Moreover, inquiries often touch upon AI's capabilities in demand forecasting and supply chain management, enabling better inventory control and more agile responses to market fluctuations in raw materials and end-product demand. The application of AI in material science, particularly for designing novel carbon black formulations with enhanced properties or discovering new applications, is another area of user concern. This includes exploring how AI-driven simulations and data analytics can lead to breakthroughs in product innovation and contribute to the development of more sustainable and high-performance carbon black solutions.

- AI-driven optimization of manufacturing processes leading to improved yield, energy efficiency, and reduced waste.

- Enhanced quality control through AI-powered anomaly detection and real-time process adjustments.

- Predictive maintenance of machinery and equipment, minimizing downtime and optimizing operational costs.

- Advanced supply chain management and logistics optimization using AI for demand forecasting and inventory control.

- Accelerated research and development of new carbon black grades and applications through AI-driven material discovery and simulation.

Key Takeaways Carbon Black Market Size & Forecast

Analysis of user questions regarding the key takeaways from the carbon black market size and forecast consistently highlights the market's robust growth trajectory, driven primarily by the automotive and industrial rubber sectors. Users frequently seek to understand the underlying factors contributing to this growth, emphasizing the critical role of tire manufacturing and the expanding demand for non-tire rubber products. The increasing global vehicle fleet and industrialization in emerging economies are recognized as fundamental drivers, underscoring the market's resilience despite economic fluctuations.

Furthermore, insights are sought on the accelerating shift towards specialty applications and the growing importance of sustainable solutions like recovered carbon black, indicating a market keen on diversification and environmental responsibility. The regional dynamics, particularly the dominance of the Asia Pacific region in both production and consumption, also form a significant area of interest for stakeholders. These trends collectively suggest a market that is not only expanding in volume but also evolving in its product offerings and geographical focus, presenting both opportunities and challenges for industry participants.

- The global carbon black market is poised for steady growth, primarily fueled by the expanding automotive and industrial rubber sectors.

- Asia Pacific remains the largest and fastest-growing regional market, driven by rapid industrialization and manufacturing expansion.

- Increasing focus on sustainable and recovered carbon black (rCB) is transforming the industry landscape, driven by regulatory pressures and consumer demand.

- Specialty carbon black grades are experiencing significant uptake due to their diverse applications in high-performance plastics, coatings, and inks.

- Volatility in raw material prices and stringent environmental regulations pose ongoing challenges but also spur innovation in production methods.

Carbon Black Market Drivers Analysis

The global carbon black market is significantly propelled by the consistent expansion of the automotive industry, which relies heavily on carbon black for tire manufacturing. As global vehicle production and sales continue to rise, particularly in developing economies, the demand for carbon black for both original equipment and replacement tires experiences a direct positive impact. This driver is further amplified by the increasing adoption of electric vehicles, which often require specialized tire formulations incorporating advanced carbon black grades for improved performance and durability.

Beyond the automotive sector, the escalating demand from various industrial rubber products, plastics, and specialty applications plays a crucial role. Carbon black is indispensable in conveyor belts, hoses, seals, and various molded rubber goods due to its reinforcing properties and ability to enhance durability. Moreover, its use in plastics for UV stabilization, pigmentation, and conductivity, along with its application in coatings, inks, and toners, diversifies the market's revenue streams and ensures sustained growth across multiple end-use industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of the Automotive Industry and Tire Production | +1.8% | Global, particularly Asia Pacific (China, India), North America | Short to Medium-Term (2025-2030) |

| Increasing Demand from Industrial Rubber Products | +1.2% | North America, Europe, Asia Pacific | Medium-Term (2025-2031) |

| Rising Adoption in Plastics, Coatings, and Inks | +1.0% | Europe, North America, Asia Pacific | Medium to Long-Term (2026-2033) |

| Expansion of Electric Vehicle (EV) Market | +0.8% | Global, particularly China, Europe, USA | Long-Term (2027-2033) |

| Technological Advancements in Specialty Carbon Black | +0.7% | Global, led by developed economies | Medium to Long-Term (2026-2033) |

Carbon Black Market Restraints Analysis

The carbon black market faces significant restraints, primarily stemming from the volatility of crude oil prices, which serve as the predominant feedstock for its production. Fluctuations in petroleum prices directly impact manufacturing costs, leading to unpredictable pricing for end-products and affecting profit margins for manufacturers. This unpredictability necessitates complex hedging strategies and can deter investment in new production capacities, particularly for smaller market players. The reliance on fossil fuels also exposes the industry to geopolitical risks and supply chain disruptions.

Moreover, stringent environmental regulations globally pose a considerable challenge, particularly concerning emissions during the manufacturing process and the disposal of waste products. Governments and environmental agencies are increasingly imposing stricter limits on pollutants, necessitating substantial investments in advanced pollution control technologies. This increases operational costs and can sometimes lead to production capacity limitations or even closures for facilities unable to comply, pushing manufacturers towards more sustainable but potentially more expensive production methods or alternative materials.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil Prices (Feedstock) | -1.5% | Global, particularly Middle East, Asia Pacific importers | Short to Medium-Term (2025-2030) |

| Stringent Environmental Regulations and Emissions Standards | -1.3% | Europe, North America, China | Medium to Long-Term (2026-2033) |

| Availability of Substitute Materials (e.g., Silica in Tires) | -0.9% | Global, particularly developed markets | Medium to Long-Term (2026-2033) |

| Health and Safety Concerns Related to Carbon Black Exposure | -0.7% | Global, especially workplaces in manufacturing | Ongoing |

| High Capital Investment and Energy Consumption in Production | -0.5% | Global | Long-Term (2027-2033) |

Carbon Black Market Opportunities Analysis

Significant opportunities in the carbon black market emerge from the burgeoning demand for specialty carbon black grades, particularly in sectors requiring high-performance materials. These include advanced conductive applications in electronics and batteries, specialized pigments for high-end coatings and plastics, and UV stabilizers for durable outdoor products. The unique properties of specialty carbon black, such as specific particle size, surface area, and structure, enable its use in niche but rapidly growing markets, offering higher profit margins compared to commodity grades. Investment in research and development for customized solutions can unlock new application areas and foster market diversification.

Furthermore, the increasing global emphasis on sustainability and circular economy principles presents a substantial opportunity for recovered carbon black (rCB) derived from end-of-life tires. As industries seek to reduce their environmental footprint and comply with evolving regulations, the adoption of rCB as a sustainable alternative to virgin carbon black is gaining traction. This trend is supported by technological advancements in pyrolysis and other recovery processes, making rCB more economically viable and performance-competitive. Expanding into emerging economies, where industrialization and infrastructure development are accelerating, also offers vast untapped potential for market penetration and growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Specialty Carbon Black Applications | +1.5% | North America, Europe, Asia Pacific (South Korea, Japan) | Medium to Long-Term (2026-2033) |

| Development and Adoption of Recovered Carbon Black (rCB) | +1.2% | Global, particularly Europe, North America, China | Medium to Long-Term (2026-2033) |

| Expansion into Emerging Economies and New Industrial Applications | +1.0% | Asia Pacific (Southeast Asia), Latin America, Africa | Long-Term (2027-2033) |

| Technological Innovation in Carbon Black Manufacturing | +0.8% | Global | Long-Term (2027-2033) |

| Increased Use in Conductive Polymers and Battery Components | +0.7% | Global, especially China, USA, Europe | Long-Term (2027-2033) |

Carbon Black Market Challenges Impact Analysis

The carbon black market faces persistent challenges, notably the significant environmental footprint associated with its conventional production methods, which involve high energy consumption and emissions. The furnace black process, while efficient for mass production, contributes to greenhouse gas emissions and particulate matter, drawing scrutiny from environmental agencies and public opinion. Addressing these concerns necessitates substantial investments in cleaner technologies and sustainable practices, which can increase production costs and potentially impact market competitiveness, especially for manufacturers in regions with less stringent regulations.

Moreover, the competition from alternative materials, such as precipitated silica in tire manufacturing, presents a continuous challenge. While carbon black remains dominant, advancements in silica technology offer comparable or superior performance in certain applications, pushing manufacturers to innovate or risk market share erosion. Supply chain disruptions, often triggered by geopolitical events, trade disputes, or natural disasters, also pose a considerable challenge, affecting raw material availability and logistics, leading to production delays and increased operational complexities across the global supply network.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption and Environmental Footprint of Production | -1.0% | Global | Ongoing |

| Competition from Alternative Reinforcing Fillers (e.g., Silica) | -0.8% | Global, particularly automotive sector | Medium to Long-Term (2026-2033) |

| Supply Chain Disruptions and Geopolitical Instability | -0.7% | Global | Short to Medium-Term (2025-2030) |

| Waste Management and Disposal of Carbon Black By-products | -0.6% | Global, especially manufacturing hubs | Ongoing |

| Market Saturation in Traditional Applications in Developed Regions | -0.4% | North America, Europe | Long-Term (2027-2033) |

Carbon Black Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the carbon black industry, covering historical market performance, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. Emphasis is placed on segmentation by type, grade, application, and end-use industry, alongside a thorough regional analysis to provide a holistic view of the global market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.0 Billion |

| Market Forecast in 2033 | USD 26.11 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Birla Carbon, Cabot Corporation, Orion Engineered Carbons S.A., Sid Richardson Carbon & Energy Co., Tokai Carbon Co. Ltd., Mitsubishi Chemical Corporation, Continental Carbon Company, Phillips Carbon Black Limited, Himadri Speciality Chemical Ltd., OCI Company Ltd., Ralson Carbon, Black Bear Carbon B.V., Pyrolyx AG, Ecopellets, Monolith Materials, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The carbon black market is comprehensively segmented across various dimensions to provide a granular understanding of its diverse applications and product types. This detailed segmentation allows for a precise analysis of demand patterns, technological advancements, and market dynamics within specific industry verticals and product categories. The versatility of carbon black necessitates this multi-faceted approach to accurately capture its widespread industrial utility.

Understanding these segments is crucial for stakeholders to identify growth pockets, tailor product offerings, and devise effective market entry strategies. For instance, the distinction between standard and specialty grades highlights the shift towards high-value applications, while end-use industry segmentation illuminates the primary demand drivers and emerging consumption trends across different sectors globally. This structured breakdown enables a clearer view of market potential and competitive positioning.

- By Type:

- Furnace Black: The most common type, widely used for rubber reinforcement.

- Channel Black: Produced using older methods, with diminishing market share.

- Thermal Black: Characterized by large particle size, used for low-stress reinforcement.

- Acetylene Black: Known for high electrical conductivity, primarily for batteries and cables.

- Lamp Black: Traditionally used for pigments and inks.

- Others: Including newer bio-based and recovered carbon black types.

- By Grade:

- Standard Grade: Primarily used for general-purpose rubber products and tires.

- Specialty Grade: Tailored for specific properties such as conductivity, UV protection, and color in plastics, coatings, and inks.

- By Application:

- Tires: The largest application segment, for reinforcing rubber in various tire types.

- Industrial Rubber Products: Used in belts, hoses, seals, and other molded rubber goods.

- Plastics: As a pigment, UV stabilizer, and conductive filler.

- Coatings: For pigmentation, UV absorption, and conductivity in paints and varnishes.

- Inks and Toners: Providing deep black color and specific rheological properties.

- Textile Fibers: For coloration and UV resistance in synthetic fibers.

- Others: Including metallurgy, refractories, and carbon brushes.

- By End-Use Industry:

- Automotive: Encompassing tires, automotive belts, and other rubber components.

- Building & Construction: For roofing materials, sealants, and composites.

- Packaging: In plastic films and containers for coloration and barrier properties.

- Electronics: For conductive polymers and components.

- Consumer Goods: In footwear, appliances, and various household items.

- Others: Including healthcare, agriculture, and defense.

Regional Highlights

The global carbon black market exhibits significant regional disparities in terms of production capacity, consumption patterns, and regulatory landscapes. Each major region contributes uniquely to the market's dynamics, influenced by local industrial growth, automotive production trends, environmental policies, and raw material availability. Understanding these regional nuances is critical for stakeholders to identify key growth markets and adapt their strategies accordingly.

- North America: Characterized by a mature automotive industry and increasing demand for specialty carbon black in high-performance materials and conductive applications. Stringent environmental regulations drive innovation towards cleaner production and the adoption of recovered carbon black.

- Europe: A region with a strong focus on sustainability and circular economy initiatives, leading to increased investment in recovered carbon black technologies. The automotive sector, particularly the electric vehicle segment, continues to be a major demand driver, alongside growing specialty chemical applications.

- Asia Pacific (APAC): Dominates the global carbon black market in both production and consumption, primarily driven by robust industrialization, rapid growth in the automotive sector, and expanding manufacturing bases in countries like China and India. The region also sees significant investment in new production capacities and technological upgrades.

- Latin America: Experiences steady growth, fueled by increasing automotive production and infrastructure development, particularly in Brazil and Mexico. The market here is largely driven by demand for tires and industrial rubber products, with emerging opportunities in specialty applications.

- Middle East and Africa (MEA): Shows emerging potential due to ongoing industrialization, infrastructure projects, and a developing automotive sector. The region's proximity to raw material sources (crude oil) offers competitive advantages, albeit with varying levels of environmental compliance and regulatory oversight.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Carbon Black Market.- Birla Carbon

- Cabot Corporation

- Orion Engineered Carbons S.A.

- Sid Richardson Carbon & Energy Co.

- Tokai Carbon Co. Ltd.

- Mitsubishi Chemical Corporation

- Continental Carbon Company

- Phillips Carbon Black Limited

- Himadri Speciality Chemical Ltd.

- OCI Company Ltd.

- Ralson Carbon

- Black Bear Carbon B.V.

- Pyrolyx AG

- Ecopellets

- Monolith Materials, Inc.

- Jiangxi Black Cat Carbon Black Inc., Ltd.

- Shandong Huadong Rubber Materials Co., Ltd.

- Longxing Chemical Group Co., Ltd.

- JFE Chemical Corporation

- Nippon Carbon Co., Ltd.

Frequently Asked Questions

What is carbon black primarily used for?

Carbon black is predominantly used as a reinforcing filler in tires and other rubber products, enhancing their strength, durability, and wear resistance. It also serves as a pigment, UV stabilizer, and conductive agent in various applications including plastics, coatings, inks, and toners, providing deep black color and functional properties.

What are the key factors driving the growth of the carbon black market?

The primary drivers include the consistent growth of the global automotive industry and associated tire production, the increasing demand for industrial rubber products across various sectors, and the expanding applications of specialty carbon black in plastics, coatings, and conductive materials. Additionally, the rising adoption of electric vehicles is creating new demand for specialized tire formulations.

What are the main challenges facing the carbon black industry?

The key challenges involve the volatility of crude oil prices, which directly impacts production costs, and stringent environmental regulations concerning emissions and waste disposal during manufacturing. Competition from alternative materials like silica in tire applications and potential supply chain disruptions also pose significant hurdles for the market.

How is sustainability impacting the carbon black market?

Sustainability is a major trend, driving the development and adoption of recovered carbon black (rCB) derived from end-of-life tires. This shift is prompted by increasing environmental awareness, regulatory pressures, and the industry's commitment to circular economy principles, aiming to reduce reliance on virgin fossil-fuel-based carbon black and minimize waste.

Which region dominates the global carbon black market?

The Asia Pacific (APAC) region currently dominates the global carbon black market in terms of both production and consumption. This is primarily attributed to rapid industrialization, robust growth in the automotive sector, and significant manufacturing expansion in countries such as China and India, making it the largest and fastest-growing market.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted