Brominated Flame Retardant Market

Brominated Flame Retardant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701082 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

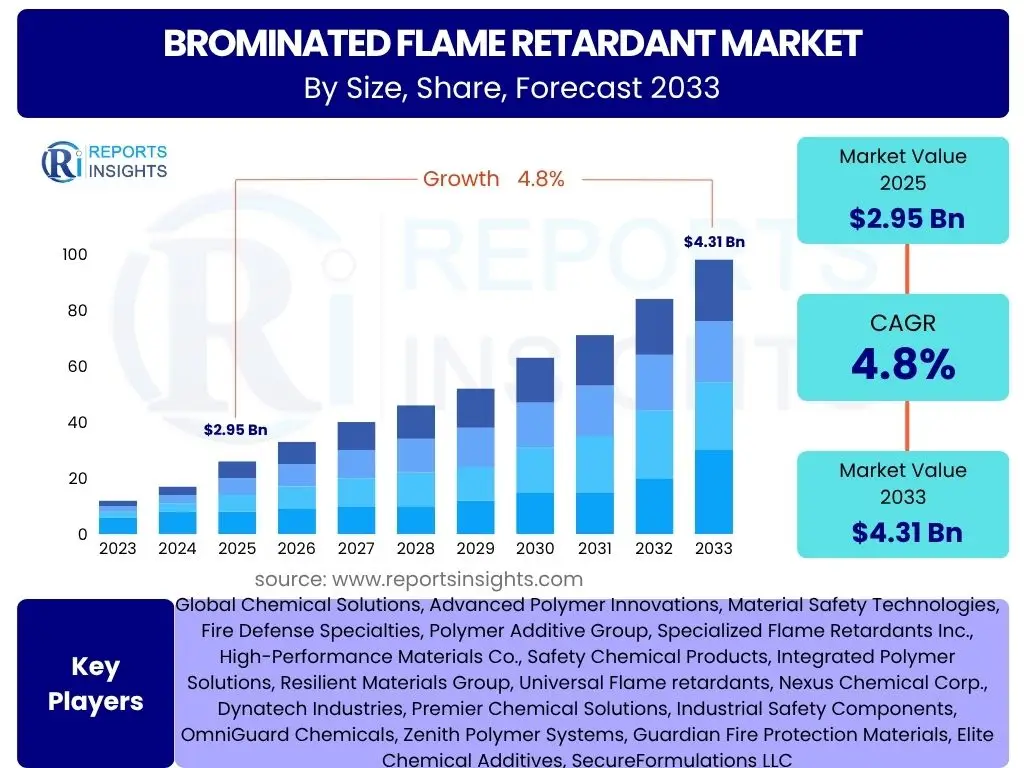

Brominated Flame Retardant Market Size

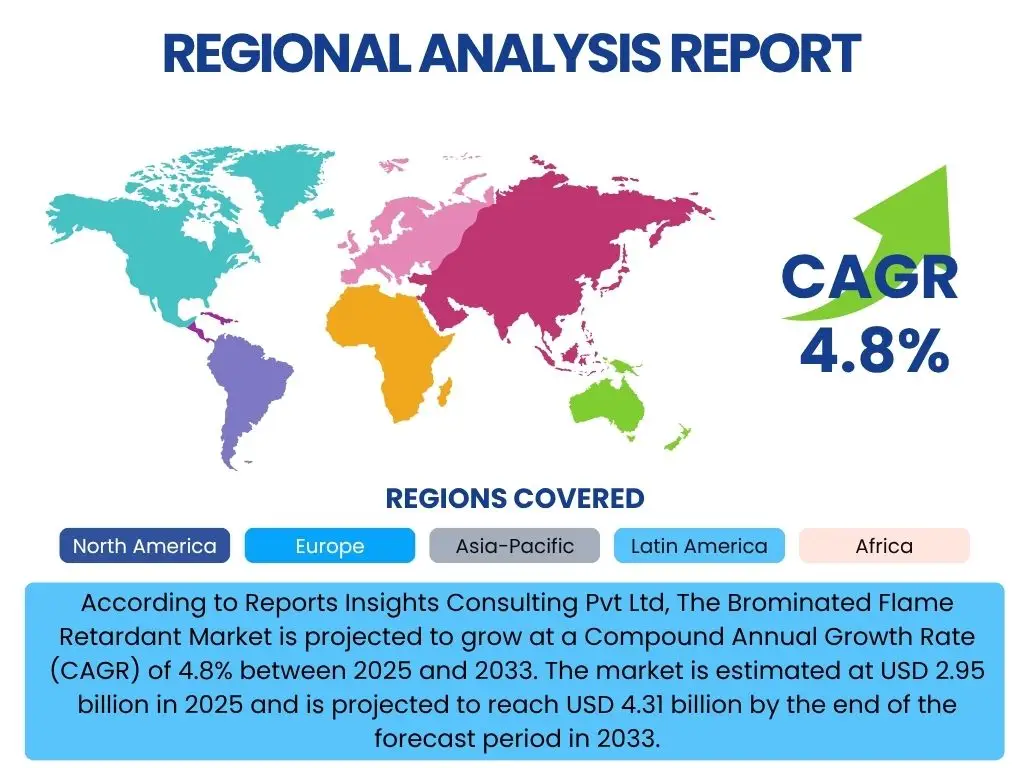

According to Reports Insights Consulting Pvt Ltd, The Brominated Flame Retardant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 2.95 billion in 2025 and is projected to reach USD 4.31 billion by the end of the forecast period in 2033.

Key Brominated Flame Retardant Market Trends & Insights

Common user inquiries regarding the Brominated Flame Retardant (BFR) market frequently revolve around the evolving regulatory landscape, the drive towards more sustainable and environmentally benign solutions, and shifts in end-use applications. There is a discernible trend towards the development of novel BFR chemistries that offer improved performance while adhering to increasingly stringent environmental and health standards. The integration of BFRs into high-performance materials for advanced electronics and electric vehicles also represents a significant area of interest, reflecting the market's adaptation to emerging technological demands. Furthermore, global supply chain dynamics and geopolitical factors are influencing sourcing strategies and production capacities for key BFR intermediates.

Another prominent trend is the increasing focus on circular economy principles within the flame retardant industry, prompting research into the recyclability of products containing BFRs and the development of strategies for safe end-of-life management. This includes the exploration of synergistic effects with other flame retardant types to reduce overall BFR content while maintaining efficacy. The market is also witnessing a regional divergence in regulatory approaches, with some regions implementing stricter bans or restrictions on certain BFRs, driving innovation towards compliant alternatives and global harmonization efforts. This regulatory complexity necessitates a nuanced understanding of market entry and product development strategies for manufacturers and suppliers.

- Shift towards low-bromine content and polymeric BFRs due to regulatory pressures and environmental concerns.

- Increased demand for BFRs in high-performance materials for consumer electronics, electric vehicles (EVs), and renewable energy infrastructure.

- Growing emphasis on circular economy principles, including BFR recycling and end-of-life management solutions.

- Development of synergistic flame retardant systems to optimize performance and reduce overall additive loading.

- Regional regulatory divergence driving localized product innovation and market strategies.

- Supply chain diversification and resilience building in response to global disruptions.

AI Impact Analysis on Brominated Flame Retardant

User queries regarding the impact of Artificial Intelligence (AI) on the Brominated Flame Retardant (BFR) market often center on its potential to revolutionize research and development, optimize manufacturing processes, and enhance supply chain efficiency. There is significant interest in how AI can accelerate the discovery of new, more environmentally friendly BFR formulations, predict material performance, and model the degradation pathways of existing BFRs. Furthermore, users are keen to understand AI's role in predictive maintenance for BFR production facilities, thereby reducing downtime and improving operational safety.

AI's analytical capabilities are also being explored for robust market forecasting and demand prediction, allowing BFR manufacturers to respond more agilely to fluctuations in raw material prices and end-user needs. By leveraging machine learning algorithms, companies can gain deeper insights into regulatory trends and consumer preferences, informing strategic decisions for product portfolio diversification and regional expansion. While the adoption of AI in the chemical industry is still nascent in some areas, its potential for optimizing complex chemical reactions and improving quality control in BFR synthesis is a key area of focus for industry stakeholders seeking competitive advantages and operational excellence.

- Accelerated discovery and development of novel BFR chemistries through AI-driven material design and predictive modeling.

- Optimization of BFR manufacturing processes, leading to improved yield, reduced energy consumption, and lower operational costs.

- Enhanced supply chain management, including predictive analytics for raw material sourcing, logistics, and inventory optimization.

- Predictive maintenance for BFR production equipment, minimizing downtime and increasing operational efficiency.

- Advanced data analysis for market forecasting, regulatory compliance monitoring, and identifying emerging application areas for BFRs.

Key Takeaways Brominated Flame Retardant Market Size & Forecast

Common inquiries concerning the key takeaways from the Brominated Flame Retardant (BFR) market size and forecast highlight a dual focus: understanding the underlying growth drivers despite regulatory pressures and identifying the most promising segments and regions for future investment. Users are particularly interested in the long-term viability of BFRs given the push for halogen-free alternatives, and the strategic adaptations being made by key market players. The resilience of demand from critical sectors like electronics and construction, coupled with evolving fire safety standards, underscores the continued relevance of BFRs, albeit with a clear trajectory towards more sustainable and compliant solutions.

The market forecast reveals a moderate but steady growth trajectory, primarily supported by increasing global demand for fire-safe materials in burgeoning industries and infrastructure projects. Despite ongoing scrutiny, the unique performance attributes of BFRs in specific applications, particularly where high fire resistance is paramount, continue to secure their market position. Strategic takeaways also include the imperative for innovation in product formulation to meet diverse regional requirements and the growing importance of lifecycle assessment in product development. The market is positioned for growth driven by technological advancements and the expansion of applications in developing economies, while mature markets navigate a more complex regulatory landscape.

- The BFR market exhibits steady growth, primarily fueled by stringent fire safety regulations and increasing demand from critical end-use industries.

- Innovation in BFR chemistry towards more environmentally friendly and high-performance solutions is crucial for market sustainability.

- Asia Pacific is projected to be the fastest-growing region, driven by rapid industrialization and infrastructure development.

- Electronics and construction sectors remain primary consumers, with emerging opportunities in electric vehicles and renewable energy.

- Regulatory shifts, particularly in Europe and North America, continue to influence product development and market dynamics, favoring low-bromine or polymeric solutions.

Brominated Flame Retardant Market Drivers Analysis

The Brominated Flame Retardant (BFR) market is significantly driven by an increasing emphasis on fire safety regulations across various industries globally. Governments and regulatory bodies worldwide are implementing stricter building codes, electronic product safety standards, and transportation safety guidelines to minimize fire hazards and protect lives and property. This heightened regulatory environment mandates the incorporation of flame retardants into a wide array of materials, from construction plastics to electronic components and textiles, thereby bolstering the demand for BFRs due to their proven efficacy and cost-effectiveness in achieving stringent fire resistance levels.

Furthermore, the rapid expansion of the electronics and electrical industry, particularly in emerging economies, serves as a pivotal market driver. With the proliferation of consumer electronics, telecommunications equipment, and IT infrastructure, there is an ever-growing need for materials that can withstand high temperatures and prevent the spread of fire in case of electrical malfunctions. BFRs are widely utilized in circuit boards, casings, and wires of electronic devices due to their superior flame retardancy characteristics, which are crucial for ensuring product safety and compliance with international standards. The burgeoning electric vehicle (EV) market also presents a new growth avenue, as BFRs are increasingly considered for battery components and interior materials where thermal runaway prevention is critical.

The construction sector's continuous growth, especially in developing regions, further contributes to the demand for BFRs. Flame retardants are incorporated into insulation materials, pipes, wires, and various building components to enhance fire safety in residential, commercial, and industrial structures. Urbanization trends and large-scale infrastructure projects worldwide necessitate the use of fire-resistant materials, thereby sustaining and expanding the market for BFRs. Despite ongoing debates about their environmental impact, the immediate effectiveness and established performance profile of BFRs continue to make them a preferred choice for many critical applications where fire safety cannot be compromised.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Fire Safety Regulations & Standards | +1.5% | Global, particularly North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Growth in Electronics & Electrical Appliances Sector | +1.2% | Asia Pacific (China, India), North America, Europe | Medium to Long Term (2026-2033) |

| Expansion of Construction Industry & Infrastructure Development | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term (2027-2033) |

| Rising Demand in Automotive (EV) Sector | +0.7% | North America, Europe, Asia Pacific (China) | Medium to Long Term (2028-2033) |

| Cost-Effectiveness & Performance Efficiency of BFRs | +0.5% | Global | Short to Medium Term (2025-2030) |

Brominated Flame Retardant Market Restraints Analysis

The Brominated Flame Retardant (BFR) market faces significant restraints primarily due to growing environmental and health concerns associated with their use. Regulatory bodies globally, particularly in Europe and North America, have introduced stringent regulations, including bans and restrictions on certain BFR types, owing to their persistence in the environment, bioaccumulation potential, and perceived toxicity. These regulations, such as the Restriction of Hazardous Substances (RoHS) Directive in Europe and various state-level bans in the United States, compel manufacturers to seek and adopt alternative flame retardants, thereby limiting the market's growth potential for traditional BFRs. The negative public perception and media scrutiny surrounding BFRs further exacerbate these challenges, influencing consumer preferences and corporate sustainability initiatives.

The increasing availability and adoption of non-halogenated flame retardants (NHFRs) present a substantial competitive restraint for the BFR market. As research and development in NHFRs advance, these alternatives offer comparable or even superior flame retardancy in certain applications, often with a more favorable environmental and health profile. Industries are increasingly transitioning to NHFRs to comply with regulations, meet corporate social responsibility goals, and cater to consumer demand for "green" products. While NHFRs may sometimes present higher costs or different processing characteristics, ongoing innovations are mitigating these drawbacks, making them increasingly viable substitutes for BFRs across various end-use sectors, including electronics and construction.

Furthermore, the complex and fragmented regulatory landscape across different regions and countries poses a significant challenge for BFR manufacturers and users. Navigating a patchwork of varying regulations requires substantial investment in compliance, testing, and product reformulation, adding to operational costs and market entry barriers. The lifecycle management of products containing BFRs, including recycling and disposal, also presents difficulties due to the environmental persistence of some compounds. These factors collectively contribute to a constrained market environment, pushing the industry towards a continuous evolution in chemistry and application to mitigate the impact of these formidable restraints and maintain market relevance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental & Health Regulations | -1.8% | Europe, North America, Japan | Short to Long Term (2025-2033) |

| Availability of Non-Halogenated Flame Retardant Alternatives | -1.5% | Global, particularly North America, Europe, Asia Pacific | Medium to Long Term (2026-2033) |

| Negative Public Perception & Media Scrutiny | -0.8% | Global, especially developed economies | Short to Medium Term (2025-2030) |

| High Cost of Compliance & Product Reformulation | -0.6% | Global | Short to Medium Term (2025-2029) |

| Complex Waste Management & Recycling Challenges | -0.4% | Europe, North America | Medium to Long Term (2027-2033) |

Brominated Flame Retardant Market Opportunities Analysis

Despite regulatory pressures, the Brominated Flame Retardant (BFR) market is poised for various opportunities driven by innovation and evolving application needs. A significant opportunity lies in the development of novel polymeric BFRs and encapsulated BFRs, which offer reduced leachability and lower environmental impact compared to traditional additive BFRs. These advanced formulations can meet stringent environmental regulations while maintaining superior flame retardancy performance, thereby expanding their applicability in sensitive sectors like medical devices and high-performance electronics. Research into synergistic blends of BFRs with other flame retardant types also presents an opportunity to optimize performance with lower overall BFR content, addressing sustainability concerns without compromising safety.

The rapid expansion of the electric vehicle (EV) market and the renewable energy sector (e.g., solar panels, wind turbines) presents a substantial growth avenue for BFRs. These industries require materials with exceptional fire safety properties, particularly for battery packs, charging infrastructure, and critical electrical components, where thermal runaway is a significant concern. BFRs, due to their high efficiency in preventing ignition and flame spread, are well-suited for these demanding applications. The increasing adoption of 5G technology and complex data centers also creates new demand for highly fire-resistant materials in advanced communication infrastructure, offering a niche but high-value segment for BFR manufacturers.

Furthermore, opportunities exist in emerging economies where industrialization and urbanization are accelerating, leading to increased construction activities and greater adoption of electronic devices. As fire safety standards in these regions gradually strengthen, the demand for effective flame retardants, including BFRs, is expected to rise. Manufacturers can capitalize on these markets by offering cost-effective and compliant BFR solutions tailored to local regulatory frameworks and industrial requirements. Additionally, the development of advanced recycling technologies and end-of-life solutions for BFR-containing products could transform environmental challenges into sustainable business models, creating a more circular economy for these critical materials and enhancing their long-term market acceptance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel & Polymeric BFRs | +1.3% | Global, particularly Europe, North America, Asia Pacific (R&D centers) | Medium to Long Term (2027-2033) |

| Rising Demand from Electric Vehicle (EV) & Renewable Energy Sectors | +1.0% | North America, Europe, Asia Pacific (China, South Korea) | Medium to Long Term (2028-2033) |

| Increasing Infrastructure & Electronics Demand in Emerging Economies | +0.8% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Short to Medium Term (2025-2030) |

| Innovation in Synergistic Flame Retardant Blends | +0.6% | Global R&D hotspots | Medium Term (2026-2031) |

| Advancements in BFR Recycling & End-of-Life Management | +0.4% | Europe, North America | Long Term (2030-2033) |

Brominated Flame Retardant Market Challenges Impact Analysis

The Brominated Flame Retardant (BFR) market confronts significant challenges primarily stemming from evolving regulatory landscapes and increasing public and environmental scrutiny. The persistent concern over the bioaccumulative nature and potential toxicity of certain BFRs continues to drive stricter regulations and outright bans in various regions, particularly impacting manufacturers' ability to maintain market access for traditional formulations. This regulatory fragmentation necessitates costly research and development into compliant alternatives, complex supply chain adjustments, and often leads to the discontinuation of established products. Companies must continually invest in reformulation and extensive testing to ensure their products meet diverse and frequently changing global standards, which adds substantial operational burden and delays market entry for new products.

Another prominent challenge is the strong competitive pressure from the rapidly developing non-halogenated flame retardant (NHFR) segment. As consumer preferences shift towards "green" and sustainable products, and as regulatory bodies increasingly favor halogen-free solutions, BFRs face an uphill battle in maintaining their market share. While NHFRs historically presented performance and cost trade-offs, ongoing innovations in this area are rapidly closing the gap, making them increasingly viable substitutes across a wider range of applications. This intense competition compels BFR manufacturers to innovate aggressively, focusing on new chemistries that address environmental concerns without sacrificing the inherent performance advantages of brominated compounds. However, the investment required for such innovation is substantial, and the market acceptance of new BFR formulations can be slow due to entrenched perceptions.

Furthermore, the complexity of managing the full lifecycle of BFR-containing products, from production to disposal and recycling, poses significant challenges. The difficulty in efficiently and safely separating BFRs from end-of-life products, coupled with concerns about their release into the environment during waste processing, complicates recycling initiatives and adds to the environmental burden. This challenge creates a negative feedback loop, reinforcing the push for alternatives and discouraging investment in BFR technologies. Supply chain disruptions, often driven by geopolitical events or raw material price volatility, further complicate the manufacturing and distribution of BFRs, impacting cost-effectiveness and timely delivery. Addressing these multifaceted challenges requires a concerted effort across the industry to innovate, collaborate on sustainable solutions, and engage effectively with regulators and the public to ensure the continued responsible use of BFRs where their unique properties remain indispensable for safety.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving & Restrictive Regulatory Landscape | -1.7% | Europe, North America, Japan | Short to Long Term (2025-2033) |

| Intensifying Competition from Non-Halogenated Alternatives | -1.4% | Global, particularly developed markets | Medium to Long Term (2026-2033) |

| Negative Consumer & Brand Perception | -0.9% | Global, especially Western markets | Short to Medium Term (2025-2030) |

| High R&D Costs for Compliant BFR Chemistries | -0.7% | Global | Medium Term (2026-2031) |

| Complexities in Lifecycle Management & Recycling | -0.5% | Europe, North America | Long Term (2029-2033) |

Brominated Flame Retardant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Brominated Flame Retardant (BFR) market, offering a detailed understanding of its current size, historical performance, and future growth projections. The report segments the market by product type, application, and end-use industry, providing a granular view of market dynamics across key regions. It also includes a thorough examination of market drivers, restraints, opportunities, and challenges, along with an impact analysis of Artificial Intelligence (AI) on the industry. The competitive landscape is meticulously analyzed, profiling key market players and their strategic initiatives, offering valuable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 billion |

| Market Forecast in 2033 | USD 4.31 billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chemical Solutions, Advanced Polymer Innovations, Material Safety Technologies, Fire Defense Specialties, Polymer Additive Group, Specialized Flame Retardants Inc., High-Performance Materials Co., Safety Chemical Products, Integrated Polymer Solutions, Resilient Materials Group, Universal Flame retardants, Nexus Chemical Corp., Dynatech Industries, Premier Chemical Solutions, Industrial Safety Components, OmniGuard Chemicals, Zenith Polymer Systems, Guardian Fire Protection Materials, Elite Chemical Additives, SecureFormulations LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Brominated Flame Retardant (BFR) market is extensively segmented by various dimensions including type, application, and end-use industry to provide a granular understanding of its diverse landscape. The segmentation by type typically includes major BFR compounds such as Tetrabromobisphenol A (TBBPA), Decabromodiphenyl Ethane (DBDPE), and Hexabromocyclododecane (HBCD), along with polymeric BFRs and other emerging brominated chemistries. Each type exhibits distinct properties and is preferred for specific applications based on regulatory compliance, cost-effectiveness, and performance requirements.

Application-wise, the market is primarily divided into plastics, textiles, electronics & electrical, coatings & adhesives, and construction materials. BFRs are integral to the plastics industry for various polymers used in consumer goods, automotive parts, and industrial equipment. In the electronics sector, they are crucial for circuit boards and casings to prevent fire propagation. The end-use industry segmentation further refines this, highlighting the specific industries that are the primary consumers of BFRs, such as building & construction, electronics & appliances, automotive & transportation, and textiles & furnishings. This layered segmentation reveals the complex interdependencies within the market and allows for targeted analysis of growth drivers and challenges in each sub-segment, reflecting the diverse utility of BFRs across modern industrial applications.

- By Type:

- Tetrabromobisphenol A (TBBPA)

- Decabromodiphenyl Ethane (DBDPE)

- Hexabromocyclododecane (HBCD)

- Brominated Polystyrene (BPS)

- Other Brominated Flame Retardants (e.g., Ethylenebistetrabromophthalimide)

- By Application:

- Plastics

- Textiles

- Electronics & Electrical

- Coatings & Adhesives

- Construction Materials

- Others (e.g., Wires & Cables, Foams)

- By End-Use Industry:

- Building & Construction

- Electronics & Appliances

- Automotive & Transportation

- Textiles & Furnishings

- Wires & Cables

- Paints & Coatings

- Others (e.g., Aerospace, Marine)

Regional Highlights

The global Brominated Flame Retardant (BFR) market exhibits significant regional variations in terms of consumption, regulatory landscape, and growth dynamics. Asia Pacific stands out as the leading and fastest-growing region, primarily driven by robust economic growth, rapid industrialization, and extensive infrastructure development, particularly in countries like China, India, and Southeast Asian nations. The burgeoning electronics manufacturing industry and the expanding construction sector in these economies fuel a substantial demand for BFRs to meet increasing fire safety standards. While regulatory frameworks are evolving, the current enforcement often allows for broader use of BFRs compared to Western counterparts, contributing to higher regional consumption.

North America and Europe represent mature markets for BFRs, characterized by stringent environmental regulations and a strong emphasis on product stewardship and sustainability. These regions have seen a gradual shift towards more regulated or alternative flame retardants due to bans on certain legacy BFRs, particularly in consumer products. However, demand for BFRs persists in highly specialized applications where their performance remains critical and suitable alternatives are scarce or cost-prohibitive, such as certain industrial electronics and aerospace components. Innovation in these regions often focuses on developing new BFR chemistries that comply with stricter environmental profiles, ensuring continued, albeit more targeted, market presence.

Latin America, the Middle East, and Africa (MEA) are emerging markets for BFRs, showing promising growth driven by increasing foreign investments, urbanization, and industrial expansion. As these regions experience economic development, there is a rising awareness of fire safety and a growing adoption of international building and product safety standards. This leads to an increased demand for flame-retardant materials across the construction, automotive, and electronics sectors. While the market size in these regions is currently smaller compared to Asia Pacific, the projected growth rates indicate significant potential for BFR manufacturers looking to diversify their market presence and tap into developing industrial bases.

- Asia Pacific: Dominant market share and highest growth rate due to booming electronics manufacturing, construction industry expansion, and increasing fire safety awareness in China, India, Japan, and South Korea.

- North America: Mature market with stable demand, driven by stringent fire safety regulations in construction, automotive, and electronics sectors in the United States and Canada, alongside a focus on developing more sustainable BFR solutions.

- Europe: Characterized by strict environmental regulations (e.g., RoHS, REACH), leading to a strategic shift towards compliant BFRs or non-halogenated alternatives; sustained demand in specialized industrial applications and regulated sectors across Germany, France, and the UK.

- Latin America: Emerging market with growing demand influenced by industrialization, infrastructure development, and increasing adoption of fire safety standards, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Growing market segment driven by construction booms, urbanization, and rising industrial output, with increasing awareness and implementation of fire safety measures in countries like UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Brominated Flame Retardant Market.- Global Chemical Solutions

- Advanced Polymer Innovations

- Material Safety Technologies

- Fire Defense Specialties

- Polymer Additive Group

- Specialized Flame Retardants Inc.

- High-Performance Materials Co.

- Safety Chemical Products

- Integrated Polymer Solutions

- Resilient Materials Group

- Universal Flame retardants

- Nexus Chemical Corp.

- Dynatech Industries

- Premier Chemical Solutions

- Industrial Safety Components

- OmniGuard Chemicals

- Zenith Polymer Systems

- Guardian Fire Protection Materials

- Elite Chemical Additives

- SecureFormulations LLC

Frequently Asked Questions

Analyze common user questions about the Brominated Flame Retardant market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Brominated Flame Retardants (BFRs) and why are they used?

Brominated Flame Retardants (BFRs) are a class of organic compounds containing bromine that are added to various materials to inhibit or slow the spread of fire. They work by interfering with the chemical reactions during combustion, forming a protective char layer, or releasing non-combustible gases. BFRs are primarily used to enhance fire safety in products like electronics, textiles, and building materials to comply with stringent fire safety regulations and prevent fire-related accidents.

Are Brominated Flame Retardants safe for human health and the environment?

The safety of Brominated Flame Retardants is a subject of ongoing debate and research. Some older BFRs, such as Polybrominated Diphenyl Ethers (PBDEs), have been linked to environmental persistence, bioaccumulation, and potential adverse health effects, leading to widespread restrictions and bans. However, newer generation BFRs, particularly polymeric forms, are designed to be more stable, less bioavailable, and have improved environmental profiles. Regulatory bodies continuously assess and regulate BFRs to minimize risks, pushing for safer alternatives and responsible use.

What are the main alternatives to Brominated Flame Retardants?

The primary alternatives to Brominated Flame Retardants are non-halogenated flame retardants (NHFRs). These include phosphorus-based compounds, nitrogen-based compounds, inorganic flame retardants (e.g., aluminum trihydrate, magnesium hydroxide), and intumescent systems. The choice of alternative depends on the specific application, material properties, desired flame retardancy level, cost, and regulatory requirements. Research and development in NHFRs are rapidly advancing, offering competitive performance for many applications.

Which industries are the largest consumers of Brominated Flame Retardants?

The electronics and electrical industry is a major consumer of Brominated Flame Retardants, particularly for circuit boards, connectors, and casings, where fire safety is paramount for consumer protection and product integrity. The building and construction sector also utilizes BFRs extensively in insulation materials, pipes, and wires. Other significant end-use industries include automotive (for interiors and components), textiles and furnishings, and various industrial applications where flame retardancy is critical.

What is the future outlook for the Brominated Flame Retardant market?

The Brominated Flame Retardant market is projected to experience moderate growth, driven by increasing global demand for fire-safe materials and evolving safety regulations. While certain legacy BFRs face phase-outs due to environmental concerns, the market is adapting through the development of newer, more compliant, and polymeric BFRs. Opportunities lie in emerging applications like electric vehicles and renewable energy, as well as in developing economies with growing industrialization. The market's future will be shaped by continued innovation, regulatory harmonization, and the ability of manufacturers to offer sustainable, high-performance solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted