Organophosphoru flame retardant Market

Organophosphoru flame retardant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705739 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

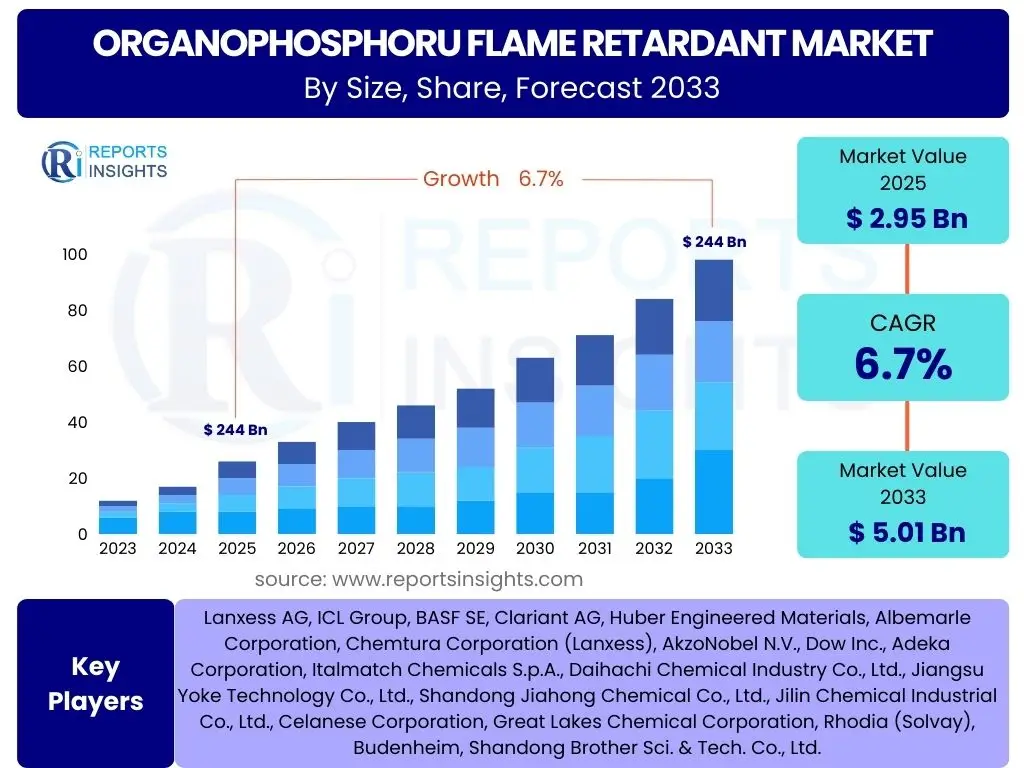

Organophosphoru flame retardant Market Size

According to Reports Insights Consulting Pvt Ltd, The Organophosphoru flame retardant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 2.95 Billion in 2025 and is projected to reach USD 5.01 Billion by the end of the forecast period in 2033.

Key Organophosphoru flame retardant Market Trends & Insights

The organophosphorus flame retardant market is undergoing significant transformation driven by evolving regulatory landscapes, technological advancements, and a heightened global emphasis on fire safety. User inquiries frequently center on the emergence of novel, environmentally friendly formulations, the increasing adoption of these flame retardants in diverse industrial applications, and the strategic shifts manufacturers are undertaking to meet stringent performance and sustainability standards. There is a strong interest in understanding how the market is adapting to demands for halogen-free solutions and exploring the potential of bio-based alternatives.

Key trends also reflect a push for multi-functional materials that not only impart flame retardancy but also offer enhanced mechanical properties or improved processability. The integration of smart materials and advanced composites in sectors like electric vehicles and consumer electronics is creating new opportunities for specialized organophosphorus compounds. Furthermore, ongoing research into intumescent systems, which form a protective char layer upon heating, represents a significant area of innovation, promising safer and more efficient fire protection solutions.

- Shift towards halogen-free organophosphorus flame retardants due to environmental and health concerns.

- Increasing adoption in high-performance applications such as electric vehicle battery components and aerospace materials.

- Development of bio-based and sustainable organophosphorus flame retardant solutions.

- Growth in demand from the electrical and electronics sector for enhanced fire safety in devices.

- Advancements in intumescent flame retardant technologies for improved char formation and fire barrier properties.

- Focus on multi-functional additives that offer flame retardancy alongside other desired material properties.

AI Impact Analysis on Organophosphoru flame retardant

Common user questions regarding AI's influence on the organophosphorus flame retardant sector revolve around its potential to revolutionize research and development, optimize manufacturing processes, and provide predictive insights into market dynamics. Users are particularly keen to understand how artificial intelligence can accelerate the discovery of novel compounds with superior performance and lower environmental impact. There is also significant curiosity about AI's role in streamlining production, enhancing quality control, and reducing operational costs within the chemical industry.

The application of AI extends to predictive modeling for material properties, allowing formulators to anticipate the performance of new flame retardant compositions without extensive physical testing. This capability not only reduces time-to-market but also minimizes resource consumption. Moreover, AI-driven analytics can optimize supply chain management, predict demand fluctuations, and identify potential disruptions, thereby enhancing the overall efficiency and resilience of the organophosphorus flame retardant market. The integration of AI tools is expected to foster a new era of precision in chemical engineering and market strategy.

- Accelerated discovery and design of novel organophosphorus flame retardant compounds through AI-driven molecular modeling.

- Optimization of formulation processes and application techniques using machine learning algorithms.

- Enhanced quality control and performance prediction of flame retardant materials via data analytics.

- Predictive maintenance and operational efficiency improvements in manufacturing facilities.

- Supply chain optimization and demand forecasting for raw materials and finished products.

Key Takeaways Organophosphoru flame retardant Market Size & Forecast

User queries frequently target the most critical insights derived from the organophosphorus flame retardant market size and forecast, focusing on the primary growth catalysts, significant market challenges, and the regional landscapes poised for substantial expansion. The market's robust growth trajectory is largely attributed to stringent global fire safety regulations and the escalating demand for fire-resistant materials across diverse industries. There is a clear emphasis on innovation geared towards sustainable and halogen-free solutions, reflecting a broader industry shift towards environmental responsibility.

A key takeaway is the burgeoning opportunity within rapidly expanding sectors such as electric vehicles and consumer electronics, where the need for enhanced thermal stability and fire suppression is paramount. While raw material price volatility and perceived toxicity concerns present ongoing challenges, the market is continually adapting through the development of advanced formulations and strategic collaborations. Asia Pacific remains the dominant consumption region, driven by its robust manufacturing base and infrastructure development, signifying its continued importance in the global market outlook.

- The market is poised for significant growth, primarily fueled by global fire safety regulations and expanding industrial applications.

- Innovation in sustainable and halogen-free organophosphorus flame retardants is a central theme driving product development.

- Asia Pacific is projected to remain the largest and fastest-growing regional market due to industrialization and infrastructure development.

- Opportunities in emerging applications like electric vehicles, renewable energy infrastructure, and smart electronics are substantial.

- Navigating raw material supply chain complexities and managing perceptions around environmental safety are key ongoing challenges for market participants.

Organophosphoru flame retardant Market Drivers Analysis

The organophosphorus flame retardant market is propelled by a confluence of regulatory pressures, sustained industrial growth, and continuous innovation in material science. Stringent fire safety regulations mandated by governmental bodies worldwide are the foremost driver, compelling manufacturers across various sectors to incorporate effective flame retardant solutions into their products. These regulations are particularly impactful in industries such as construction, electrical and electronics, and automotive, where product safety is paramount and often legally enforced.

Furthermore, the expansion of critical end-use industries significantly contributes to market growth. The burgeoning global construction sector, coupled with increasing investments in infrastructure projects, demands flame-retardant materials for insulation, wiring, and structural components. Similarly, the rapid growth in the electronics and electrical sector, driven by technological advancements and rising consumer demand for smart devices, necessitates high-performance flame retardants to prevent fire hazards in electronic circuitry and casings. The automotive industry, especially with the surge in electric vehicle (EV) production, is another key driver, requiring specialized flame retardants for battery components and interior materials to enhance vehicle safety.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Global Fire Safety Regulations | +2.5% | Global | 2025-2033 |

| Growth in Construction and Infrastructure Development | +1.8% | Asia Pacific, Middle East | 2025-2030 |

| Rising Demand from Electrical & Electronics Sector | +2.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Automotive Industry, particularly EVs | +1.5% | Europe, Asia Pacific, North America | 2027-2033 |

| Increasing Focus on Halogen-Free Flame Retardants | +1.2% | Global | 2025-2033 |

Organophosphoru flame retardant Market Restraints Analysis

Despite significant growth drivers, the organophosphorus flame retardant market faces several notable restraints that could temper its expansion. Environmental and health concerns surrounding certain flame retardant chemicals represent a primary impediment. Regulatory bodies and consumer groups are increasingly scrutinizing the potential long-term impacts of these compounds, leading to stricter environmental guidelines and, in some cases, advocating for their phased reduction or elimination. This perception of toxicity, even for less harmful variants, can deter adoption and spur the search for alternative solutions, impacting market sentiment and demand.

Another significant restraint is the inherent volatility in raw material prices. The production of organophosphorus flame retardants relies on various chemical intermediates, whose costs can fluctuate significantly due to geopolitical factors, supply chain disruptions, and global economic conditions. Such price instability directly affects manufacturing costs, potentially eroding profit margins for producers and leading to higher end-product prices, which can reduce competitiveness. Furthermore, the market faces strong competition from alternative flame retardant technologies, including inorganic flame retardants, nitrogen-based compounds, and intumescent systems, which may offer different performance profiles or perceived environmental benefits, thus challenging the market share of organophosphorus variants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns & Toxicity Perceptions | -1.0% | Europe, North America | 2025-2033 |

| Volatility in Raw Material Prices | -0.8% | Global | 2025-2030 |

| Competition from Alternative Flame Retardant Technologies | -0.7% | Global | 2025-2033 |

| High Research and Development Costs | -0.5% | Global | 2025-2033 |

Organophosphoru flame retardant Market Opportunities Analysis

The organophosphorus flame retardant market presents several promising opportunities for growth and innovation. A significant avenue lies in the burgeoning electric vehicle (EV) sector, where the inherent risk of thermal runaway in batteries creates an urgent demand for advanced fire safety solutions. Organophosphorus compounds, due to their efficacy and potential for intumescent properties, are well-positioned to meet the stringent safety requirements for EV battery packs, charging infrastructure, and interior components. This expanding application area represents a substantial, high-value market segment for specialized flame retardant formulations.

Moreover, the increasing global emphasis on sustainability is driving opportunities for the development of bio-based and more environmentally benign organophosphorus flame retardants. Researchers and manufacturers are actively exploring renewable feedstocks and greener synthetic pathways to produce flame retardants that align with circular economy principles and reduce ecological footprints. This focus on sustainable chemistry can unlock new markets, particularly in regions with strong environmental policies. Additionally, the broader adoption of smart home devices, robotics, and advanced manufacturing processes continues to expand the scope of application for organophosphorus flame retardants, as these technologies often require compact, high-performance fire protection solutions for their sophisticated electronic components and integrated systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand in Electric Vehicles (EVs) | +1.5% | Global | 2027-2033 |

| Development of Bio-based and Sustainable Flame Retardants | +1.0% | Europe, North America | 2028-2033 |

| Expansion into Aerospace and Defense Applications | +0.8% | North America, Europe | 2025-2033 |

| Growth in Smart Home Devices and Consumer Electronics | +0.7% | Asia Pacific, North America | 2026-2032 |

| Innovations in Nanotechnology-based Flame Retardant Synergists | +0.6% | Global | 2028-2033 |

Organophosphoru flame retardant Market Challenges Impact Analysis

The organophosphorus flame retardant market faces several critical challenges that require strategic navigation for sustained growth. One significant hurdle is the complex and evolving regulatory landscape. Different regions and countries impose varying standards and restrictions on the use of certain chemical compounds, including flame retardants, often based on ongoing toxicological assessments and environmental impact studies. Compliance with these diverse and sometimes conflicting regulations necessitates significant investment in research, testing, and product reformulation, adding complexity and cost to manufacturers' operations.

Another major challenge pertains to the end-of-life management of products containing flame retardants, specifically disposal and recycling. As concerns about the persistence and bioaccumulation of certain chemicals grow, there is increasing pressure to develop easily recyclable materials or flame retardants that can be safely recovered and reused. This presents a technical challenge for material scientists and a logistical challenge for waste management systems. Furthermore, manufacturers are constantly striving to achieve an optimal balance between flame retardant performance and cost-effectiveness. High-performance formulations can be expensive, limiting their adoption in price-sensitive applications, while cheaper alternatives may not meet stringent fire safety standards. This ongoing trade-off demands continuous innovation to deliver solutions that are both effective and economically viable for a broad range of applications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating Complex and Evolving Regulatory Landscape | -0.9% | Europe, North America, Asia Pacific | 2025-2033 |

| Disposal and Recycling Challenges for Treated Materials | -0.6% | Global | 2025-2033 |

| Achieving Balance Between Performance and Cost-Effectiveness | -0.5% | Global | 2025-2030 |

| Supply Chain Disruptions and Raw Material Scarcity | -0.4% | Global | 2025-2027 |

Organophosphoru flame retardant Market - Updated Report Scope

This section details the fundamental parameters and comprehensive coverage of the market research report, offering a transparent overview of the analytical scope and key data points included. It outlines the historical and forecast periods, clarifies the base year for analysis, and specifies the market valuation figures at the beginning and end of the forecast horizon. Furthermore, it enumerates the core market attributes, including the projected growth rate, the number of pages in the full report, and a detailed list of key trends, segmented categories, and leading companies whose profiles are included. This structure ensures clarity regarding the depth and breadth of the market insights provided.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 Billion |

| Market Forecast in 2033 | USD 5.01 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lanxess AG, ICL Group, BASF SE, Clariant AG, Huber Engineered Materials, Albemarle Corporation, Chemtura Corporation (Lanxess), AkzoNobel N.V., Dow Inc., Adeka Corporation, Italmatch Chemicals S.p.A., Daihachi Chemical Industry Co., Ltd., Jiangsu Yoke Technology Co., Ltd., Shandong Jiahong Chemical Co., Ltd., Jilin Chemical Industrial Co., Ltd., Celanese Corporation, Great Lakes Chemical Corporation, Rhodia (Solvay), Budenheim, Shandong Brother Sci. & Tech. Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The organophosphorus flame retardant market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across various categories. This segmentation typically includes classification by type of organophosphorus compound, the specific application areas where these flame retardants are utilized, and the primary end-use industries that drive demand. Further refinement often involves segmentation by the physical form in which these retardants are supplied, such as liquid, powder, or granules, reflecting their suitability for different manufacturing processes and material matrices.

Analyzing these segments helps identify key growth pockets, assess market saturation, and pinpoint emerging opportunities. For instance, the shift from halogenated to non-halogenated types highlights an industry-wide drive towards sustainability, while the breakdown by application reveals the most impactful areas of consumption, such as in plastics for electronics or textiles for furniture. Understanding these interdependencies across segments is crucial for strategic planning and product development, enabling stakeholders to align their offerings with specific market needs and regulatory requirements. This multi-faceted segmentation provides a robust framework for market analysis and forecasting.

- By Type:

- Halogenated Organophosphorus Flame Retardants

- Non-Halogenated Organophosphorus Flame Retardants

- Phosphate Esters (e.g., Triphenyl Phosphate, Tricresyl Phosphate)

- Phosphonates

- Phosphinates

- Polymeric Organophosphorus Flame Retardants

- By Application:

- Plastics

- Polyolefins (PP, PE)

- Polyvinyl Chloride (PVC)

- Engineering Plastics (PC, ABS, PBT, Nylon)

- Polystyrene (PS, HIPS, EPS)

- Polyurethane (PU)

- Textiles

- Coatings

- Adhesives & Sealants

- Rubber

- Foams (Flexible and Rigid Polyurethane Foams)

- Plastics

- By End-Use Industry:

- Building & Construction

- Electrical & Electronics

- Automotive & Transportation

- Textiles & Furniture

- Wires & Cables

- Aerospace & Defense

- Paints & Coatings

- By Form:

- Liquid

- Powder

- Granules

Regional Highlights

The global organophosphorus flame retardant market exhibits significant regional disparities in terms of consumption patterns, regulatory frameworks, and growth opportunities. These regional nuances are shaped by varying industrial development levels, specific fire safety standards, and local environmental policies. Understanding these differences is crucial for market participants to tailor their strategies effectively and capitalize on regional strengths.

Asia Pacific dominates the market, driven by rapid industrialization, burgeoning construction activities, and the expansive growth of the electrical and electronics manufacturing sectors in countries like China, India, Japan, and South Korea. This region also sees increasing adoption of stringent fire safety codes, further propelling demand. Europe represents a mature market characterized by a strong emphasis on environmental regulations, leading to a high demand for halogen-free and eco-friendly organophosphorus solutions, particularly in the automotive and electrical industries. North America, another significant market, prioritizes high-performance materials in its aerospace, automotive, and building sectors, underpinned by robust fire safety legislation. Latin America and the Middle East & Africa are emerging markets, with growing infrastructure development and increasing awareness of fire safety standards gradually boosting demand for flame retardants in these regions.

- Asia Pacific: Commands the largest market share and is projected to exhibit the highest growth rate due to rapid industrialization, extensive construction projects, and a booming electronics manufacturing base in countries such as China, India, and ASEAN nations.

- Europe: A mature market characterized by stringent environmental regulations, driving the demand for halogen-free and more sustainable organophosphorus flame retardants, particularly in automotive and electronics applications.

- North America: Exhibits strong demand from the automotive, aerospace, and building & construction sectors, supported by comprehensive fire safety codes and a focus on high-performance materials.

- Latin America: An emerging market experiencing gradual growth, influenced by increasing foreign investments in manufacturing and growing awareness of fire safety standards in infrastructure and consumer goods.

- Middle East and Africa (MEA): A developing region with growing demand fueled by significant investments in infrastructure, commercial, and residential construction projects, alongside rising industrialization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Organophosphoru flame retardant Market.- Lanxess AG

- ICL Group

- BASF SE

- Clariant AG

- Huber Engineered Materials

- Albemarle Corporation

- Adeka Corporation

- Italmatch Chemicals S.p.A.

- Daihachi Chemical Industry Co., Ltd.

- Jiangsu Yoke Technology Co., Ltd.

- Shandong Jiahong Chemical Co., Ltd.

- Jilin Chemical Industrial Co., Ltd.

- Celanese Corporation

- Valtris Specialty Chemicals

- Sanko Chemical Industry Co., Ltd.

- PCC Rokita SA

- Chemische Fabrik Budenheim KG

- Shandong Brother Sci. & Tech. Co., Ltd.

- Nippon Chemical Industrial Co., Ltd.

- Kyowa Chemical Industry Co., Ltd.

Frequently Asked Questions

What are organophosphorus flame retardants used for?

Organophosphorus flame retardants are primarily used to enhance the fire safety of materials across various industries by inhibiting or slowing down combustion. Their applications span plastics, textiles, coatings, adhesives, and foams, serving critical sectors such as building and construction, electrical and electronics, automotive, and furniture.

Are organophosphorus flame retardants safe?

The safety of organophosphorus flame retardants is a complex and evolving area of research. While they are generally considered safer alternatives to some halogenated counterparts, their specific safety profile depends on the compound's chemical structure, application, and exposure levels. Manufacturers are increasingly focusing on developing non-toxic, environmentally benign, and sustainable formulations to address health and environmental concerns.

How are regulations impacting the organophosphorus flame retardant market?

Regulations significantly impact the organophosphorus flame retardant market by imposing stricter fire safety standards and simultaneously increasing scrutiny on chemical safety and environmental profiles. This drives innovation towards halogen-free and more sustainable solutions, while also influencing regional market dynamics based on specific compliance requirements, particularly in Europe and North America.

What are the key trends in organophosphorus flame retardant innovation?

Key innovations focus on the development of halogen-free compounds, bio-based and sustainable formulations, and advanced intumescent systems that create a protective char layer. There is also a trend towards multi-functional flame retardants that offer additional material benefits and enhanced performance in high-tech applications like electric vehicle batteries and advanced electronics.

Which regions are major consumers of organophosphorus flame retardants?

Asia Pacific is the largest and fastest-growing consumer of organophosphorus flame retardants, driven by extensive industrialization, robust construction, and booming electronics manufacturing sectors. Europe and North America also represent significant mature markets, primarily due to stringent fire safety regulations and high demand from their automotive and specialized industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted