Bio Acetic Acid Market

Bio Acetic Acid Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706007 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

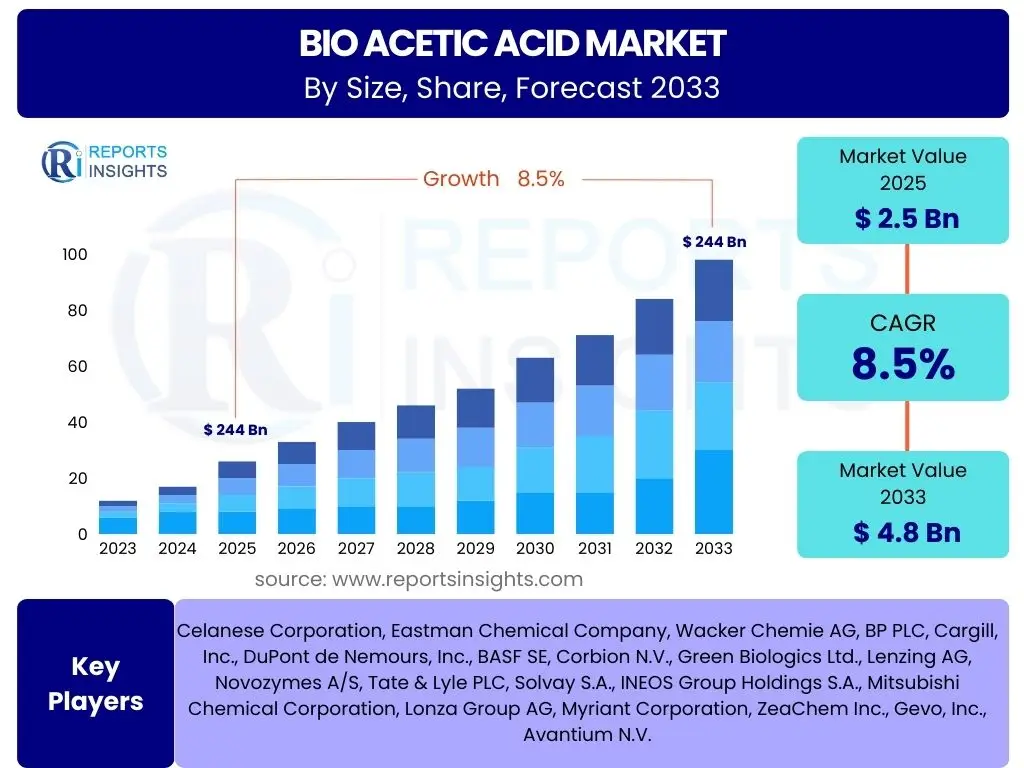

Bio Acetic Acid Market Size

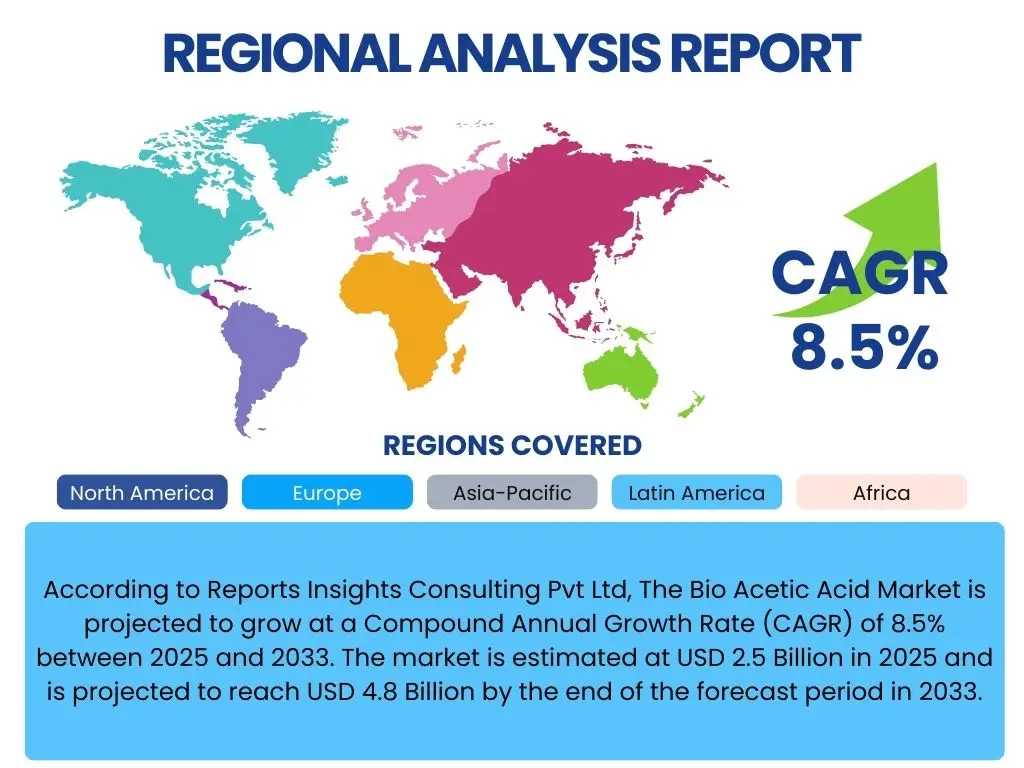

According to Reports Insights Consulting Pvt Ltd, The Bio Acetic Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.8 Billion by the end of the forecast period in 2033.

Key Bio Acetic Acid Market Trends & Insights

The Bio Acetic Acid market is characterized by a significant shift towards sustainable chemical manufacturing, driven by escalating environmental concerns and stringent regulatory frameworks. A prominent trend involves the adoption of advanced biotechnological processes, particularly microbial fermentation, which enhances production efficiency and reduces the carbon footprint compared to conventional synthesis methods. This push for green chemistry is propelling demand across various industries, including food and beverages, pharmaceuticals, and textile manufacturing, where bio-based alternatives are increasingly preferred for their eco-friendly profiles.

Furthermore, the market is witnessing innovation in feedstock utilization, moving beyond traditional sugar-based sources to include lignocellulosic biomass and industrial waste streams, which contributes to circular economy principles and reduces reliance on food crops. This diversification of raw materials, coupled with process optimization, is making bio acetic acid a more economically viable and environmentally attractive option. The expansion into novel applications, such as the production of biodegradable plastics and bio-based solvents, further underscores the dynamic evolution and growth potential within this sector.

- Growing preference for sustainable and bio-based chemicals.

- Advancements in fermentation technologies and feedstock diversification.

- Increasing adoption in food and beverage, pharmaceutical, and textile industries.

- Development of new applications in bioplastics and bio-solvents.

- Focus on circular economy principles and waste valorization.

AI Impact Analysis on Bio Acetic Acid

Artificial Intelligence (AI) is poised to revolutionize the Bio Acetic Acid market by significantly enhancing efficiency, optimizing production processes, and accelerating research and development. AI algorithms can analyze vast datasets from bioreactors to predict optimal fermentation conditions, including temperature, pH, and nutrient levels, thereby maximizing yield and purity while minimizing energy consumption. This predictive capability allows for real-time process adjustments, reducing human error and improving overall operational consistency and economic viability for bio-based production facilities.

In research and development, AI is instrumental in discovering and engineering new, highly efficient microbial strains for acetic acid production. Machine learning models can quickly sift through genetic data, identify promising metabolic pathways, and simulate the performance of novel microorganisms, dramatically shortening the time required for strain optimization. Furthermore, AI can optimize supply chain logistics for raw materials, predict market demand fluctuations, and manage inventory more effectively, ensuring a steady and cost-efficient supply of bio acetic acid to end-users. This comprehensive impact across the value chain positions AI as a critical enabler for the future growth and sustainability of the bio acetic acid industry.

- Optimization of fermentation parameters for higher yields and purity.

- Accelerated discovery and engineering of efficient microbial strains.

- Predictive maintenance and fault detection in bioreactors.

- Enhanced supply chain management and logistics for raw materials.

- Improved quality control and consistency of final product.

Key Takeaways Bio Acetic Acid Market Size & Forecast

The Bio Acetic Acid market is on a robust growth trajectory, primarily fueled by the global imperative for sustainability and the increasing adoption of bio-based products across diverse industries. The forecast indicates significant expansion, driven by continuous innovation in production technologies that enhance efficiency and cost-effectiveness, making bio acetic acid a more competitive alternative to its petrochemical counterparts. This growth underscores a fundamental shift in industrial preferences towards renewable resources and environmentally friendly manufacturing processes, positioning bio acetic acid as a critical component in the transition to a bio-economy.

A key insight is the expanding application landscape, particularly in emerging sectors such as bioplastics and sustainable agriculture, which are opening new revenue streams and diversifying market demand. The market's resilience is further supported by favorable government policies and consumer awareness programs promoting green chemistry. For stakeholders, investing in advanced fermentation techniques, exploring diverse feedstock options, and fostering strategic partnerships will be crucial to capitalize on the sustained demand and secure a strong position in this evolving market.

- Strong market growth driven by sustainability trends and demand for bio-based products.

- Technological advancements are enhancing production efficiency and competitiveness.

- Expanding applications in bioplastics and agriculture are key growth drivers.

- Favorable regulatory landscape and increasing consumer awareness support market expansion.

- Strategic investments in R&D and diversified feedstock are vital for market leaders.

Bio Acetic Acid Market Drivers Analysis

The increasing global emphasis on sustainability and environmental protection stands as a primary driver for the Bio Acetic Acid market. Industries are under growing pressure from regulatory bodies and consumers to reduce their carbon footprint and transition away from fossil fuel-derived chemicals. Bio acetic acid, produced from renewable biomass, offers a compelling solution by significantly lowering greenhouse gas emissions and reducing reliance on finite resources, aligning perfectly with corporate sustainability goals and national environmental targets.

Technological advancements in biotechnology, particularly in microbial fermentation and biorefinery processes, have dramatically improved the efficiency and economic viability of bio acetic acid production. These innovations have led to higher yields, reduced processing times, and lower production costs, making bio acetic acid more competitive against synthetic acetic acid. The continuous research and development in strain engineering and process optimization further contribute to making bio-based production more attractive and scalable for industrial applications.

Furthermore, the escalating demand from key end-use industries, such as food and beverages, pharmaceuticals, and chemicals, is a significant market driver. In the food sector, bio acetic acid is preferred for its natural origin in various applications like preservation and flavor enhancement. The pharmaceutical industry values its high purity and sustainable sourcing. As these sectors continue to grow and prioritize green alternatives, the demand for bio acetic acid is expected to rise proportionately, solidifying its market position.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Sustainable Chemicals | +2.5% | Global, especially Europe, North America | 2025-2033 |

| Advancements in Biotechnological Production | +1.8% | Global, led by North America, APAC | 2025-2033 |

| Growth in End-Use Industries (Food, Pharma, Bioplastics) | +2.0% | Asia Pacific, North America, Europe | 2025-2033 |

| Favorable Government Policies & Regulations | +1.2% | Europe, North America, China | 2025-2030 |

Bio Acetic Acid Market Restraints Analysis

Despite its promising growth, the Bio Acetic Acid market faces significant restraints, primarily stemming from its higher production costs compared to conventional, fossil-derived acetic acid. The capital expenditure required for setting up biorefineries can be substantial, and the cost of fermentable raw materials, such as sugar or corn, can fluctuate based on agricultural yields and market dynamics. These economic disadvantages often make it challenging for bio acetic acid to compete purely on price with established synthetic routes, especially in price-sensitive bulk chemical markets.

Another key restraint is the technical complexity and scalability challenges associated with biological production processes. Optimizing fermentation for high yields and purity on an industrial scale requires precise control over microbial activity, nutrient balance, and environmental conditions. Any deviation can lead to reduced efficiency or contamination, impacting overall production costs and product quality. Scaling up laboratory-proven methods to commercial production often presents unforeseen engineering hurdles and demands significant investment in R&D and process validation.

Furthermore, the availability and consistent supply of suitable biomass feedstock can be a constraint. While various feedstocks can be used, their availability can be seasonal or geographically limited, potentially leading to supply chain disruptions and price volatility. Competition for feedstock with other bio-based industries, such as biofuels, also adds pressure. Additionally, the existing infrastructure heavily favors petrochemical production, requiring substantial investment and time to build out a parallel bio-based infrastructure, which further acts as a market impediment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs Compared to Synthetic | -1.5% | Global | 2025-2033 |

| Technical Challenges in Scaling Up Production | -1.0% | Global, especially emerging markets | 2025-2030 |

| Raw Material Price Volatility and Availability | -0.8% | Global, depending on agricultural cycles | 2025-2033 |

| Competition from Established Petrochemical Processes | -0.7% | Global | 2025-2033 |

Bio Acetic Acid Market Opportunities Analysis

The burgeoning bioplastics market presents a significant opportunity for bio acetic acid. As global efforts intensify to reduce plastic waste and seek sustainable alternatives, bio acetic acid can serve as a key building block for certain biodegradable polymers and bioplastics. Its role as a monomer or intermediate in the production of bio-based materials offers a high-growth application area, aligning with consumer and regulatory demands for environmentally friendly packaging and products. This expansion into the bioplastics sector can significantly boost market volume and value.

Moreover, the development of advanced fermentation technologies and novel microbial strains offers continuous opportunities for cost reduction and efficiency improvement. Research into more robust and productive microorganisms, combined with breakthroughs in bioreactor design and process control, can lower production costs and expand the range of usable feedstocks. This ongoing innovation will enhance the competitiveness of bio acetic acid against traditional methods and unlock new capabilities, making the bio-based route more attractive for large-scale industrial adoption.

Emerging economies and increasing investments in green chemistry initiatives worldwide provide substantial growth opportunities. Countries in Asia Pacific and Latin America are rapidly industrializing and also increasingly focusing on sustainable development, creating a fertile ground for bio-based chemical markets. Government incentives, subsidies for bio-refineries, and mandates for sustainable procurement can accelerate the market penetration of bio acetic acid. Furthermore, the rising consumer awareness and demand for products with a reduced environmental footprint compel manufacturers to incorporate bio-based ingredients, thereby expanding the market scope.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Bioplastics & Biodegradable Polymers | +2.0% | Global, especially Europe, APAC | 2027-2033 |

| Technological Breakthroughs in Fermentation Efficiency | +1.5% | North America, Europe, APAC | 2025-2033 |

| Growing Green Chemistry Initiatives & Investments | +1.2% | Global, with strong focus in Europe, China | 2025-2030 |

| Diversification of Feedstock to Non-Food Sources | +1.0% | Global | 2026-2033 |

Bio Acetic Acid Market Challenges Impact Analysis

The primary challenge for the Bio Acetic Acid market is achieving cost competitiveness with synthetic acetic acid. Traditional methods of acetic acid production, largely petrochemical-based, benefit from well-established infrastructure, mature technologies, and economies of scale, leading to significantly lower production costs. Bio acetic acid, conversely, often incurs higher feedstock costs, greater capital expenditure for specialized biorefineries, and more complex purification processes, making it difficult to compete on price, particularly in bulk chemical applications. This cost disparity can hinder widespread adoption, especially in price-sensitive markets.

Another significant challenge is ensuring consistent product quality and purity, which is critical for various industrial applications like pharmaceuticals and food. Biological processes are inherently more complex and susceptible to variability due to factors such as microbial health, feedstock consistency, and environmental conditions. Maintaining stringent quality control standards and achieving high purity levels consistently on an industrial scale requires advanced analytical techniques and robust process management, adding to operational complexity and costs. Deviations in quality can impact customer acceptance and market reputation.

Regulatory hurdles and the time-consuming approval processes for new bio-based products also pose a challenge. While regulations often favor sustainable products, the specific requirements for commercializing novel bio-based chemicals can be complex and vary significantly across different regions. Navigating these regulatory landscapes, demonstrating product safety, and obtaining necessary certifications can be a lengthy and expensive endeavor, potentially delaying market entry and limiting global market reach for new bio acetic acid products or applications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cost Competitiveness with Synthetic Acetic Acid | -1.8% | Global | 2025-2033 |

| Ensuring Consistent Product Quality & Purity | -1.1% | Global | 2025-2033 |

| Regulatory Complexities & Approval Processes | -0.9% | Europe, North America, China | 2025-2030 |

| Limited Industrial Scale Production Experience | -0.6% | Global, particularly emerging markets | 2025-2028 |

Bio Acetic Acid Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Bio Acetic Acid market, covering historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges affecting the industry. It further segments the market by application, production method, and raw material, offering granular insights into various market segments. The report also highlights regional market performance and profiles key companies operating in the competitive landscape, providing a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.8 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Celanese Corporation, Eastman Chemical Company, Wacker Chemie AG, BP PLC, Cargill, Inc., DuPont de Nemours, Inc., BASF SE, Corbion N.V., Green Biologics Ltd., Lenzing AG, Novozymes A/S, Tate & Lyle PLC, Solvay S.A., INEOS Group Holdings S.A., Mitsubishi Chemical Corporation, Lonza Group AG, Myriant Corporation, ZeaChem Inc., Gevo, Inc., Avantium N.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bio Acetic Acid market is comprehensively segmented to provide granular insights into its diverse applications, production methodologies, and raw material sources. This segmentation allows for a detailed understanding of market dynamics within specific niches and identifies key growth areas. The application segments range across critical industries, reflecting the broad utility of bio acetic acid in promoting sustainability, while the production method and raw material segments highlight the technological evolution and resource diversification shaping the industry.

Understanding these segments is crucial for stakeholders to identify lucrative opportunities, tailor product development, and formulate targeted market strategies. The varied end-uses underscore the versatility of bio acetic acid as a sustainable chemical intermediate, while the different production routes and feedstock options indicate the ongoing innovation aimed at improving efficiency and reducing environmental impact. This multi-faceted segmentation provides a foundational framework for analyzing market trends and forecasting future demand across the value chain.

- By Application: Food & Beverages, Pharmaceuticals, Chemicals (e.g., vinyl acetate monomer, acetic anhydride), Textiles, Plastics & Polymers (e.g., cellulose acetate, PLA), Agriculture, Others.

- By Production Method: Fermentation (e.g., traditional microbial, advanced microbial), Biorefinery Processes (e.g., syngas fermentation).

- By Raw Material: Biomass (e.g., Corn Starch, Sugarcane Molasses, Lignocellulosic Biomass), Glycerol, Syngas, Others.

Regional Highlights

- North America: This region demonstrates strong growth propelled by significant investments in biotechnology research and development, stringent environmental regulations promoting bio-based chemicals, and increasing consumer awareness regarding sustainable products. The United States and Canada are at the forefront, with robust R&D infrastructure and a high adoption rate of green chemistry principles in industries like food, pharmaceuticals, and emerging bioplastics.

- Europe: Europe is a leading market driven by ambitious sustainability goals, supportive government policies such as the European Green Deal, and a strong emphasis on the circular economy. Countries like Germany, the Netherlands, and France are heavily investing in biorefineries and sustainable chemical production, fostering a conducive environment for bio acetic acid adoption across various industrial sectors.

- Asia Pacific (APAC): The APAC region is poised for substantial growth due to rapid industrialization, expanding manufacturing sectors, and increasing environmental consciousness, particularly in China, India, and Japan. The burgeoning demand for food and beverage additives, pharmaceuticals, and textiles, coupled with government initiatives to reduce pollution, is fueling the adoption of bio acetic acid, despite a higher price point compared to synthetic alternatives.

- Latin America: This region presents significant opportunities due to the abundant availability of agricultural feedstock, such as sugarcane and corn. Countries like Brazil are well-positioned to become major producers of bio-based chemicals, including bio acetic acid, leveraging their vast biomass resources and growing focus on sustainable industrial development.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is expected to witness gradual growth, driven by diversification efforts from traditional oil-based industries towards sustainable chemicals and increasing investments in industrial infrastructure. The rising awareness of environmental benefits and the development of new industrial hubs are anticipated to contribute to market expansion in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bio Acetic Acid Market.- Celanese Corporation

- Eastman Chemical Company

- Wacker Chemie AG

- BP PLC

- Cargill, Inc.

- DuPont de Nemours, Inc.

- BASF SE

- Corbion N.V.

- Green Biologics Ltd.

- Lenzing AG

- Novozymes A/S

- Tate & Lyle PLC

- Solvay S.A.

- INEOS Group Holdings S.A.

- Mitsubishi Chemical Corporation

- Lonza Group AG

- Myriant Corporation

- ZeaChem Inc.

- Gevo, Inc.

- Avantium N.V.

Frequently Asked Questions

What is bio acetic acid?

Bio acetic acid is a naturally derived form of acetic acid produced through the fermentation of renewable biomass feedstocks, such as corn, sugarcane, or lignocellulosic materials. Unlike synthetic acetic acid, which is typically derived from petrochemicals, bio acetic acid offers a more sustainable and environmentally friendly alternative with a reduced carbon footprint.

What are the primary applications of bio acetic acid?

Bio acetic acid finds widespread applications across various industries. Its primary uses include being a key ingredient in the food and beverage industry for preservation, flavoring, and acidity regulation; a crucial component in pharmaceuticals; an essential intermediate in the production of various chemicals like vinyl acetate monomer and acetic anhydride; a solvent in textiles; and a building block for bioplastics and polymers.

How is bio acetic acid produced?

Bio acetic acid is primarily produced through a biotechnological process, most commonly microbial fermentation. Microorganisms, such as acetogenic bacteria, convert sugars or other carbon sources from biomass into acetic acid under controlled anaerobic conditions. Emerging methods also include biorefinery processes utilizing syngas or glycerol as feedstocks, contributing to diverse production routes.

What are the environmental benefits of bio acetic acid?

The key environmental benefits of bio acetic acid include its production from renewable resources, which reduces reliance on fossil fuels. It significantly lowers greenhouse gas emissions compared to synthetic acetic acid, contributes to a circular economy by potentially utilizing waste biomass, and aligns with sustainability goals by promoting green chemistry practices and biodegradable product development.

What are the key drivers for the bio acetic acid market?

The main drivers for the bio acetic acid market are the increasing global demand for sustainable and eco-friendly chemicals, stringent environmental regulations pushing industries towards greener alternatives, and continuous advancements in biotechnological production processes that enhance efficiency and reduce costs. Growing applications in emerging sectors like bioplastics also significantly contribute to market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted