Ballast Water Treatment System Market

Ballast Water Treatment System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709200 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

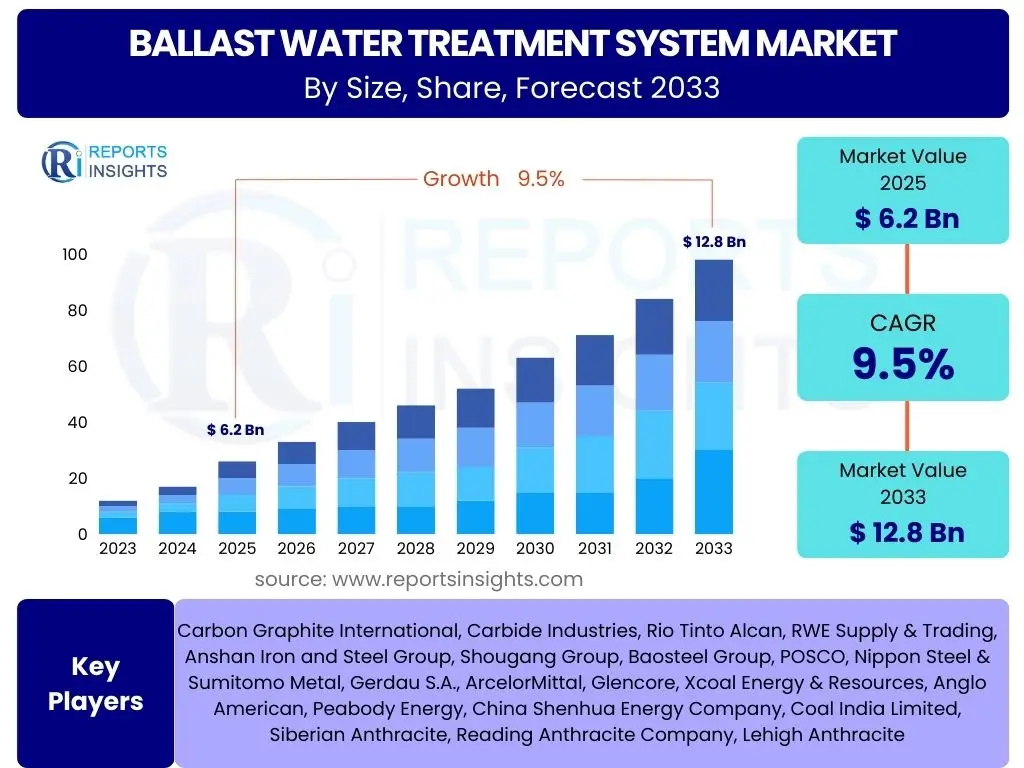

Ballast Water Treatment System Market Size

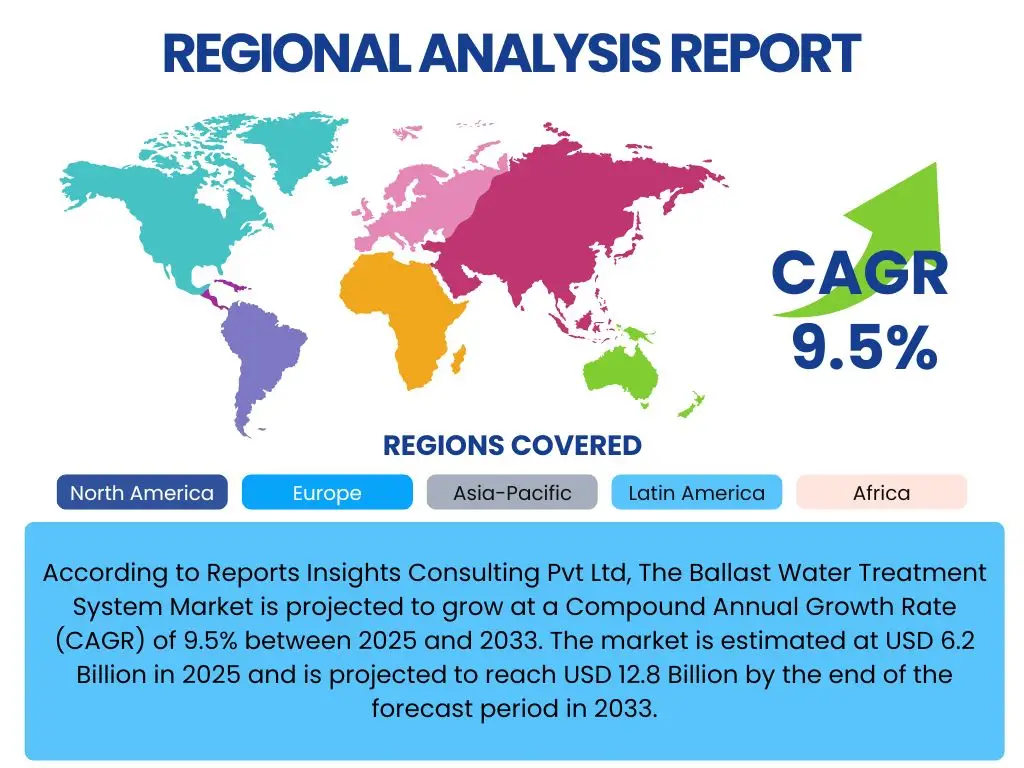

According to Reports Insights Consulting Pvt Ltd, The Ballast Water Treatment System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 12.8 Billion by the end of the forecast period in 2033.

Key Ballast Water Treatment System Market Trends & Insights

The Ballast Water Treatment System (BWTS) market is undergoing significant transformation, primarily driven by stringent global environmental regulations aimed at preventing the spread of invasive aquatic species. Users frequently inquire about the latest technological advancements, the impact of regulatory updates from organizations like the IMO and USCG, and the increasing demand for compact and energy-efficient systems. There is also considerable interest in the integration of digital solutions for enhanced system monitoring and maintenance, reflecting a broader industry shift towards operational optimization and cost reduction while ensuring compliance.

Current insights suggest a strong market inclination towards proven and reliable treatment technologies such as UV-based and electro-chlorination systems due to their effectiveness and established operational track records. Furthermore, the retrofit market continues to be a major revenue stream as older vessels adapt to new compliance standards. The push for modular and hybrid systems that can adapt to varying water conditions and vessel types is also a prominent trend, addressing the diverse operational requirements of the global shipping fleet and simplifying installation processes.

- Stringent global environmental regulations (IMO D-2, USCG) driving mandatory adoption.

- Increased demand for compact, modular, and energy-efficient treatment systems suitable for diverse vessel types.

- Growing preference for established technologies such as UV and electro-chlorination due to reliability and efficacy.

- Rising integration of digital technologies for remote monitoring, data analytics, and predictive maintenance.

- Significant activity in the retrofit market as older vessels comply with international standards.

- Development of hybrid systems combining multiple treatment methods for enhanced performance and adaptability.

- Focus on systems with lower operational expenditure and simplified maintenance requirements.

AI Impact Analysis on Ballast Water Treatment System

User questions related to the impact of Artificial Intelligence (AI) on Ballast Water Treatment Systems often revolve around how AI can enhance efficiency, reduce operational costs, and improve regulatory compliance. There is a clear interest in AI's potential to provide predictive analytics for maintenance, optimize treatment processes in real-time based on water conditions, and streamline data reporting for regulatory bodies. Concerns are also raised regarding the initial investment in AI infrastructure, data security, and the need for skilled personnel to manage and interpret AI-driven insights within the maritime sector.

AI's influence is anticipated to revolutionize BWTS operations by moving beyond basic automation towards intelligent, adaptive management. This includes the deployment of machine learning algorithms to analyze vast datasets pertaining to water quality, system performance, and vessel routes, enabling systems to make autonomous adjustments for optimal treatment. Such capabilities will not only ensure consistent compliance under varying environmental conditions but also contribute significantly to reducing energy consumption and prolonging the lifespan of BWTS components. The future of BWTS heavily leans on AI for smarter, more reliable, and cost-effective operations, transforming how ships manage ballast water globally.

- Predictive Maintenance: AI algorithms analyze sensor data to predict equipment failures, enabling proactive maintenance and reducing costly downtime.

- Optimized Operation: Real-time data analysis of water conditions (salinity, turbidity, temperature) allows AI to adjust treatment parameters for maximum efficiency and compliance.

- Enhanced Regulatory Compliance: AI-driven reporting systems automate data collection and submission, ensuring accurate and timely adherence to international and local regulations.

- Energy Efficiency: AI optimizes power consumption of BWTS components by fine-tuning operation based on specific treatment needs, leading to reduced operational costs.

- Fault Detection and Diagnostics: Rapid identification of system malfunctions through AI minimizes manual intervention and speeds up troubleshooting processes.

- Crew Training and Decision Support: AI-powered interfaces can provide intuitive operational guidance and training for crew members, improving overall system management.

Key Takeaways Ballast Water Treatment System Market Size & Forecast

User inquiries into the key takeaways from the Ballast Water Treatment System market size and forecast consistently highlight the critical role of environmental mandates in shaping market growth. The most significant insight is that regulatory compliance, particularly the IMO D-2 standard and USCG requirements, remains the primary catalyst for market expansion. This ongoing regulatory pressure ensures a sustained demand for BWTS solutions across the global shipping fleet, emphasizing retrofits for existing vessels and integrated systems for newbuilds. Furthermore, the market exhibits robust growth potential, driven by technological advancements aimed at improving system efficiency, reducing operational complexities, and lowering lifecycle costs.

Another crucial takeaway is the increasing fragmentation of the market, with various technologies competing for market share, each with its own advantages and limitations depending on vessel type and operational profile. Stakeholders are keen to understand which technologies are gaining traction and why, often seeking insights into cost-effectiveness, environmental impact, and ease of integration. The forecast underscores a future where BWTS adoption is near universal, but the competitive landscape will be defined by innovation in system design, automation, and after-sales support, moving towards smarter, more adaptable, and energy-efficient solutions to meet the evolving demands of the maritime industry.

- The Ballast Water Treatment System market demonstrates significant and sustained growth, primarily propelled by the mandatory implementation of international and national regulations.

- Technological innovation is central to market development, focusing on solutions that offer improved efficiency, reduced footprint, lower energy consumption, and enhanced automation.

- The retrofit segment continues to be a dominant driver of sales, ensuring existing global fleets conform to strict environmental standards.

- Compliance remains a top priority for shipowners and operators, driving investment in reliable and approved BWTS technologies to avoid penalties and ensure uninterrupted trade.

- The market is characterized by intense competition and a diverse range of technological approaches, necessitating continuous R&D and strategic partnerships for market leadership.

Ballast Water Treatment System Market Drivers Analysis

The primary driver for the Ballast Water Treatment System market is the increasingly stringent global regulatory framework. The International Maritime Organization's (IMO) Ballast Water Management Convention, particularly the D-2 standard, along with the United States Coast Guard (USCG) regulations, mandates that all vessels engaged in international trade install approved BWTS to prevent the introduction of invasive aquatic species. This global legislative push ensures a continuous and non-discretionary demand for treatment solutions, compelling shipowners to invest in compliance. The phasing-in schedule for these regulations has already created a substantial backlog of vessels requiring retrofits, which will continue to fuel market expansion over the forecast period.

Beyond regulatory compliance, the growing awareness of marine environmental protection and biodiversity conservation plays a significant role. Stakeholders across the maritime industry, including port authorities, environmental organizations, and the general public, are increasingly demanding environmentally responsible shipping practices. This heightened ecological consciousness encourages earlier adoption and investment in advanced BWTS solutions, even beyond the minimum regulatory requirements. Furthermore, technological advancements in treatment methods, such as improved UV lamp efficiency, more effective electro-chlorination processes, and the development of compact systems, are making BWTS more viable, efficient, and attractive for a wider range of vessel types and sizes.

The global increase in maritime trade and shipping traffic also contributes to the market's growth. As more goods are transported across oceans, the volume of ballast water discharged by ships rises, amplifying the potential for species transfer. This escalating activity necessitates widespread BWTS adoption to mitigate environmental risks effectively. Additionally, the economic implications of non-compliance, including heavy fines, detention of vessels, and reputational damage, serve as powerful incentives for shipowners to invest in robust and reliable ballast water management solutions, reinforcing the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter IMO and USCG Regulations | +3.5% | Global, particularly Europe, North America, Asia Pacific | 2025-2033 (Ongoing) |

| Increasing Global Seaborne Trade | +2.0% | Asia Pacific, Europe, Emerging Economies | 2025-2033 (Long-term) |

| Growing Environmental Awareness | +1.5% | Global, developed nations leading | 2025-2033 (Medium-term) |

| Technological Advancements in BWTS | +1.0% | Global, especially R&D hubs in Europe, Asia | 2025-2033 (Continuous) |

| Risk of Invasive Species and Ecosystem Damage | +1.5% | Global, coastal states and biodiversity hotspots | 2025-2033 (Pervasive) |

Ballast Water Treatment System Market Restraints Analysis

Despite robust growth, the Ballast Water Treatment System market faces several significant restraints that could impede its full potential. A primary challenge is the high upfront capital expenditure associated with the procurement and installation of BWTS. For many shipowners, especially those managing older or smaller vessels, the cost of acquiring and integrating these complex systems can be substantial, often requiring significant financial planning and potentially impacting profitability. This financial burden is further exacerbated by the varying costs across different technologies and suppliers, leading to complex decision-making processes for compliance.

Another considerable restraint is the operational complexity and ongoing maintenance costs. BWTS require regular maintenance, power consumption, and often specialized training for crew members. The need for spare parts, chemical reagents (for some systems), and regular system checks adds to the operational expenditure (OPEX) over the lifetime of the vessel. Furthermore, older vessels may face severe space constraints, making the physical installation of large BWTS components challenging and sometimes requiring extensive vessel modifications, which adds further costs and extends dry-dock periods. The integration of BWTS into existing ship infrastructure is not always straightforward, presenting engineering hurdles and installation delays.

Moreover, the fragmentation of regulatory interpretations and enforcement across different port states can create confusion and uncertainty for ship operators. While IMO and USCG provide overarching guidelines, regional and local variations in enforcement or additional requirements can complicate compliance efforts. This lack of complete harmonization sometimes leads to operational inefficiencies and potential delays for vessels navigating diverse international routes. These factors collectively contribute to a challenging environment for market participants, requiring continuous innovation and support to overcome these inherent hurdles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) | -2.0% | Global, affects small & medium enterprises | 2025-2033 (Ongoing) |

| Operational & Maintenance Costs (OPEX) | -1.5% | Global, impacts long-term profitability | 2025-2033 (Throughout lifespan) |

| Space Constraints on Existing Vessels | -1.0% | Global, particularly older fleet | 2025-2030 (Retrofit phase) |

| Complexities of System Integration | -0.8% | Global, varies by vessel type | 2025-2033 (Installation phase) |

| Varying Regulatory Interpretations/Enforcement | -0.5% | Global, impacts operational flexibility | 2025-2033 (Continuous) |

Ballast Water Treatment System Market Opportunities Analysis

The Ballast Water Treatment System market is rich with opportunities, primarily driven by the ongoing need for vessels to achieve and maintain compliance with global regulations. A significant opportunity lies in the extensive retrofit market, as a large proportion of the global shipping fleet still requires the installation of compliant BWTS. This segment provides a continuous demand for equipment manufacturers, engineering services, and installation providers. As the deadlines for compliance approach for various vessel categories, the urgency for retrofitting will intensify, creating a sustained revenue stream. Furthermore, the market for newbuild vessels will consistently integrate BWTS as standard equipment, ensuring a stable baseline demand for new installations and advanced, integrated solutions.

Another key opportunity emerges from the continuous innovation in BWTS technology. There is a strong demand for more compact, energy-efficient, and easily maintainable systems that can operate effectively across diverse water conditions (fresh, brackish, and marine). The development of modular and hybrid systems that offer greater flexibility and performance is particularly attractive to shipowners. These technological advancements can address the historical challenges of space limitations and high operational costs, thereby expanding the market to vessel types that previously found BWTS installation problematic or economically unfeasible. Such innovations also foster competitive differentiation and allow companies to capture niche market segments.

Beyond hardware, the digitalization of the maritime industry presents a significant opportunity for BWTS providers. The integration of smart monitoring, data analytics, and remote diagnostic capabilities into BWTS offers enhanced operational efficiency, predictive maintenance, and streamlined regulatory reporting. This shift towards smart shipping solutions can transform BWTS from a standalone compliance requirement into an integrated component of a vessel's overall operational intelligence. Additionally, the growing demand for after-sales services, including maintenance, spare parts, crew training, and certification support, creates substantial recurring revenue opportunities, building long-term relationships with clients and ensuring the sustained performance and compliance of installed systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Retrofit Market for Existing Vessels | +2.5% | Global, all major shipping regions | 2025-2030 (Primary Focus) |

| Technological Innovation (Compact, Efficient Systems) | +2.0% | Global, especially R&D-intensive regions | 2025-2033 (Continuous) |

| Digitalization and Smart Monitoring Solutions | +1.8% | Global, tech-forward shipowners | 2025-2033 (Emerging) |

| After-sales Services and Support | +1.2% | Global, long-term revenue stream | 2025-2033 (Sustained) |

| Expansion into Specialized Vessel Segments | +1.0% | Coastal shipping, offshore vessels, fishing fleets | 2028-2033 (Future Growth) |

Ballast Water Treatment System Market Challenges Impact Analysis

The Ballast Water Treatment System market, while robust, faces several critical challenges that demand strategic attention from industry participants. A significant hurdle is the complexity and dynamic nature of global regulatory compliance. While international regulations exist, their interpretation and enforcement can vary across different flag states and port states. This often leads to confusion for shipowners regarding specific requirements, approved systems, and reporting protocols, potentially resulting in delays, fines, or operational disruptions. The ongoing evolution of these regulations, including potential amendments or new standards, also creates uncertainty and necessitates continuous adaptation from manufacturers and operators.

Another substantial challenge revolves around the operational reliability and performance of BWTS under diverse and often extreme environmental conditions. Ballast water characteristics, such as salinity, temperature, turbidity, and organism load, vary significantly across different regions, impacting the effectiveness of certain treatment technologies. Ensuring consistent compliance and optimal performance in all operating environments can be technically demanding. Issues such as filter clogging in high-sediment waters or reduced UV efficacy in turbid conditions can lead to system failures or non-compliance, undermining confidence in the installed systems. This necessitates robust testing and certification processes, which themselves add to development costs and market entry barriers.

Furthermore, the availability of skilled personnel for the operation, maintenance, and troubleshooting of BWTS poses a considerable challenge. As these systems become more sophisticated, specialized training for ship crews is essential. A shortage of adequately trained staff can lead to improper operation, increased maintenance costs, and potential non-compliance. The global nature of shipping means that training and support infrastructure must be widespread and accessible, which is a complex logistical undertaking. Addressing these challenges effectively will be crucial for sustained market growth and for ensuring the long-term success of ballast water management initiatives worldwide.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Complexity and Harmonization | -1.5% | Global, impacts international trade | 2025-2033 (Ongoing) |

| Operational Performance in Diverse Water Conditions | -1.2% | Global, affects system efficacy | 2025-2033 (Continuous) |

| Availability of Skilled Crew & Technical Support | -1.0% | Global, affects operational reliability | 2025-2033 (Long-term) |

| System Reliability and Durability | -0.8% | Global, impacts investment returns | 2025-2033 (Throughout lifespan) |

| Cybersecurity Risks for Digital Systems | -0.5% | Global, growing concern for smart ships | 2028-2033 (Emerging) |

Ballast Water Treatment System Market - Updated Report Scope

This report provides a comprehensive analysis of the Ballast Water Treatment System market, offering detailed insights into market dynamics, segmentation, and regional landscapes. It encompasses an in-depth evaluation of market drivers, restraints, opportunities, and challenges influencing industry growth from 2025 to 2033. The scope includes a thorough review of technological advancements, competitive benchmarking, and the impact of regulatory frameworks on market evolution, delivering a holistic perspective for stakeholders. The report is designed to assist businesses in making informed strategic decisions by understanding current trends and future projections within this critical maritime sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 12.8 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alfa Laval, Wartsila, Evoqua Water Technologies, DESMI A/S, Headway Technology Co., Ltd., OceanSaver AS, Optimarin AS, Panasia Co., Ltd., Samsung Heavy Industries Co., Ltd., Hyde Marine Inc., Hitachi, Ltd., Ecochlor, Inc., Techcross Inc., SunRui Marine Environment Engineering Co., Ltd., Qingdao Sunrui Co., Ltd., Damen Shipyards Group, Fuji Electric Co., Ltd., Mitsui E&S Shipbuilding Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ballast Water Treatment System market is meticulously segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed understanding of market dynamics influenced by various technological approaches, different vessel types, and distinct end-use industries. The comprehensive breakdown helps stakeholders identify specific growth areas, competitive landscapes within sub-segments, and the varying adoption rates across different market dimensions. Such detailed analysis is crucial for strategic planning, product development, and targeted market penetration, enabling businesses to tailor their offerings to precise customer needs and regulatory requirements.

Understanding the interplay between these segments is vital for predicting future market shifts. For instance, the retrofit segment's growth is largely driven by compliance deadlines for existing vessels, whereas the newbuild segment focuses on integrating advanced, more efficient systems from the outset. Similarly, the choice of technology often correlates with vessel size, operational routes, and budget constraints, highlighting the nuanced decision-making process within the industry. This multi-faceted segmentation ensures that the report captures the full complexity and potential of the global BWTS market, offering actionable intelligence across all key dimensions.

- By Technology:

- UV (Ultraviolet) Treatment: Widely adopted for its chemical-free process and effectiveness, particularly in clear water.

- Electro-chlorination (EC): Utilizes electrolysis to generate active substances, effective across varying water conditions.

- Chemical Injection: Employs active substances to kill organisms, requiring neutralization before discharge.

- De-oxygenation: Removes oxygen from ballast water, creating an anoxic environment unsuitable for aquatic life.

- Others: Includes cavitation, plasma, and heat treatment methods under development or niche applications.

- By Component:

- Filters: Essential for removing larger organisms and sediments before primary treatment.

- UV Lamps/Reactors: Core component of UV-based systems for disinfection.

- Electrolytic Units: Key for electro-chlorination systems, generating active substances.

- Neutralization Units: Required for chemical injection and electro-chlorination systems to remove residual active substances.

- Control Systems: Automation and monitoring systems crucial for optimal operation and compliance.

- Others: Pumps, sensors, valves, and other ancillary equipment.

- By Application:

- Newbuild Vessels: Installation of BWTS during the construction phase of new ships.

- Retrofit Vessels: Installation of BWTS on existing ships to meet compliance deadlines.

- By Vessel Type:

- Container Ships: Large vessels transporting standardized cargo units.

- Tankers: Ships designed to carry liquids in bulk (oil, chemicals, LNG).

- Bulk Carriers: Vessels that carry unpackaged dry cargo (grains, ores).

- General Cargo Ships: Versatile ships carrying various types of cargo.

- Offshore Vessels: Support vessels for offshore oil and gas industry.

- Passenger Ships: Cruise ships, ferries, and other vessels carrying passengers.

- Others: Includes fishing vessels, naval ships, and specialized craft.

- By End-use:

- Commercial Shipping: Covers the vast majority of international trade vessels.

- Defense: Naval vessels and other military ships requiring compliance.

- Cruise Ships: Large passenger vessels with specific operational requirements.

- Offshore Oil & Gas: Platforms, support vessels, and other units in the energy sector.

- Others: Government vessels, research ships, and various smaller fleets.

Regional Highlights

- Asia Pacific: This region stands as the largest market for BWTS, primarily driven by its dominance in global shipbuilding and a massive fleet of vessels requiring compliance. Countries like China, South Korea, and Japan are at the forefront of newbuild installations and technological innovation. The significant volume of maritime trade originating from and transiting through APAC also amplifies the demand for effective ballast water management. The increasing enforcement of environmental regulations across key coastal nations further solidifies the region's market leadership.

- Europe: Europe represents a mature market characterized by stringent environmental regulations and a strong emphasis on technological advancements and research & development. European shipowners were among the earliest adopters of BWTS, and the region continues to lead in developing advanced, energy-efficient, and modular systems. Countries such as Germany, Norway, and Sweden, with their strong maritime heritage and commitment to sustainability, play a crucial role in driving market innovation and ensuring compliance across their extensive fleets.

- North America: The North American market is significantly influenced by the strict regulations set forth by the United States Coast Guard (USCG), which often impose more demanding standards than the IMO's D-2 requirements. This creates a distinct demand for USCG-approved systems, fostering a specialized market segment. The region's focus on protecting its diverse coastal ecosystems and critical waterways ensures sustained investment in BWTS, particularly for vessels operating in or entering U.S. waters, contributing to a robust demand for compliant technologies and services.

- Latin America: This region is an emerging market for BWTS, characterized by increasing awareness of environmental protection and a growing push for regulatory compliance. While adoption rates might be slower than in more developed regions, the expanding maritime trade and the need to protect sensitive marine environments are gradually driving demand. Investment in port infrastructure and the modernization of local fleets are expected to accelerate BWTS adoption over the forecast period, presenting long-term growth opportunities for market players.

- Middle East and Africa (MEA): The MEA region is experiencing growth in the BWTS market, fueled by expanding shipping activities, particularly in the oil and gas sector, and a gradual tightening of maritime environmental regulations. Strategic locations along major shipping lanes and significant port developments contribute to the increasing need for ballast water management. While infrastructure challenges and varying levels of regulatory enforcement exist, the long-term outlook for BWTS adoption remains positive as countries in the region enhance their environmental stewardship and integrate into global maritime standards.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ballast Water Treatment System Market.- Alfa Laval

- Wartsila

- Evoqua Water Technologies

- DESMI A/S

- Headway Technology Co., Ltd.

- OceanSaver AS

- Optimarin AS

- Panasia Co., Ltd.

- Samsung Heavy Industries Co., Ltd.

- Hyde Marine Inc.

- Hitachi, Ltd.

- Ecochlor, Inc.

- Techcross Inc.

- SunRui Marine Environment Engineering Co., Ltd.

- Qingdao Sunrui Co., Ltd.

- Damen Shipyards Group

- Fuji Electric Co., Ltd.

- Mitsui E&S Shipbuilding Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Ballast Water Treatment System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Ballast Water Treatment System (BWTS)?

A Ballast Water Treatment System is a technology installed on ships to remove or neutralize biological organisms from ballast water before it is discharged, preventing the introduction of invasive aquatic species into new environments.

Why are Ballast Water Treatment Systems necessary?

BWTS are crucial for protecting marine ecosystems and biodiversity by preventing the transfer of harmful aquatic organisms and pathogens via ship's ballast water, which can devastate local species and economies.

What are the primary technologies used in BWTS?

The main technologies include Ultraviolet (UV) irradiation, Electro-chlorination (EC), and various chemical injection methods, often combined with mechanical filtration for effective treatment across diverse water conditions.

What are the key regulations driving the BWTS market?

The market is primarily driven by the International Maritime Organization (IMO)'s Ballast Water Management (BWM) Convention (D-2 standard) and the United States Coast Guard (USCG) regulations, both mandating the installation of approved BWTS on most international vessels.

What is the estimated market size and growth rate for BWTS?

The Ballast Water Treatment System market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 12.8 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 9.5% during the forecast period.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted