Aviation Electric Actuator System Market

Aviation Electric Actuator System Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706847 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

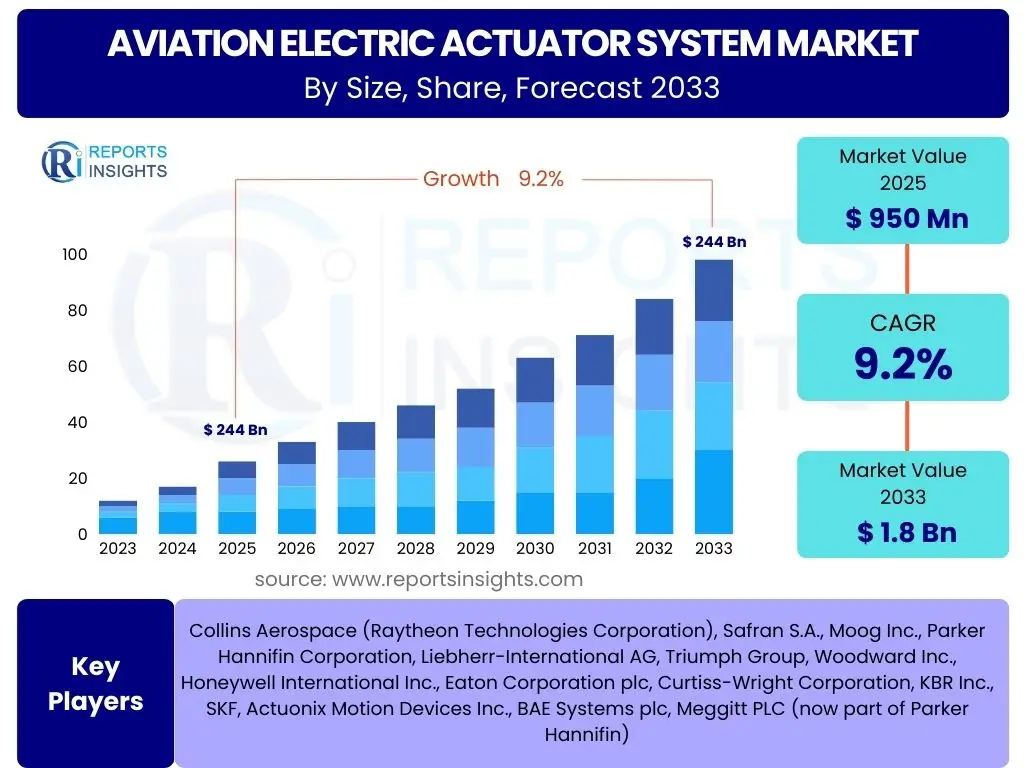

Aviation Electric Actuator System Market Size

According to Reports Insights Consulting Pvt Ltd, The Aviation Electric Actuator System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 950 Million in 2025 and is projected to reach USD 1.8 Billion by the end of the forecast period in 2033.

Key Aviation Electric Actuator System Market Trends & Insights

The aviation electric actuator system market is undergoing significant transformation, driven by a global shift towards more sustainable and efficient aircraft operations. Key trends indicate a robust demand for lightweight, high-power-density electric actuators, as well as a growing emphasis on smart systems capable of real-time monitoring and predictive maintenance. This evolution is heavily influenced by the increasing adoption of more electric aircraft (MEA) and the emerging urban air mobility (UAM) sector.

Furthermore, the market is witnessing a convergence of technologies, including advanced materials science, sophisticated control algorithms, and integrated sensor technologies. Manufacturers are continuously innovating to enhance reliability, reduce operational costs, and improve system performance across diverse aerospace applications. The push for electrification extends beyond traditional aircraft to encompass new platforms like eVTOLs, creating new design paradigms and performance requirements for actuation systems.

- Accelerated adoption of More Electric Aircraft (MEA) architectures.

- Increasing demand for lightweight and compact actuation solutions.

- Integration of smart features for condition monitoring and predictive maintenance.

- Growth in urban air mobility (UAM) and eVTOL aircraft development.

- Focus on enhanced power density and energy efficiency in actuator design.

- Development of fault-tolerant and highly reliable electric actuation systems.

AI Impact Analysis on Aviation Electric Actuator System

Artificial intelligence is poised to profoundly impact the aviation electric actuator system market by revolutionizing design, operation, and maintenance practices. Users frequently inquire about how AI can enhance performance, predict failures, and contribute to autonomous flight systems. AI algorithms can analyze vast datasets from actuator performance, environmental conditions, and flight parameters to optimize system efficiency and predict potential malfunctions with unprecedented accuracy, thereby reducing unscheduled downtime and improving overall safety.

In addition to predictive capabilities, AI is being explored for autonomous control and decision-making processes within complex flight control systems. This includes adaptive control logic that allows actuators to respond dynamically to changing flight conditions or system anomalies. Furthermore, AI-driven simulations and generative design tools are streamlining the development cycle of new actuator systems, enabling the creation of more robust and optimized designs that meet stringent aerospace requirements, ultimately leading to significant cost savings and faster innovation cycles.

- Enhanced predictive maintenance through AI-driven anomaly detection and prognostics.

- Optimization of actuator performance and energy consumption via machine learning algorithms.

- Development of adaptive control systems for improved responsiveness and stability.

- AI-assisted design and simulation for accelerated product development and validation.

- Real-time health monitoring and fault diagnosis, reducing operational risks.

- Potential for autonomous decision-making in future flight control applications.

Key Takeaways Aviation Electric Actuator System Market Size & Forecast

The Aviation Electric Actuator System Market is set for substantial growth, driven by technological advancements and the increasing electrification of the aerospace industry. Key inquiries highlight the market's consistent expansion, indicating a critical shift from traditional hydraulic and pneumatic systems towards more efficient electric alternatives. This growth is not merely incremental but represents a fundamental transformation in aircraft design and operation, emphasizing sustainability and enhanced performance.

Understanding the market size and forecast reveals several crucial insights for stakeholders. The projected revenue increase signifies robust investment opportunities and a high demand for innovative electric actuator solutions across commercial, military, and emerging aviation segments. Furthermore, the strong CAGR underscores the industry's commitment to modernizing aircraft fleets and adopting advanced technologies to meet future operational and environmental challenges. This trajectory positions electric actuators as a cornerstone technology for the next generation of aerospace vehicles.

- The market exhibits significant and consistent growth, reflecting a fundamental shift towards electric actuation in aviation.

- Technological advancements, particularly in MEA and UAM, are key drivers of market expansion.

- Investments in research and development are crucial for capitalizing on emerging opportunities.

- Reliability, power density, and efficiency remain paramount for new product development.

- The transition from traditional systems to electric alternatives is a long-term industry trend.

Aviation Electric Actuator System Market Drivers Analysis

The Aviation Electric Actuator System Market is primarily propelled by the ongoing shift towards more electric aircraft (MEA) architectures across both commercial and military aviation. This trend is driven by the desire to reduce fuel consumption, lower maintenance costs, and improve overall system efficiency by replacing traditional hydraulic and pneumatic systems with electric ones. The electrification also simplifies aircraft design, reduces weight, and enhances fault tolerance, contributing to improved safety and operational performance.

Additionally, the burgeoning urban air mobility (UAM) and eVTOL (electric vertical take-off and landing) aircraft sectors represent a significant new demand source for compact, high-performance electric actuators. These new aircraft types are inherently electric, requiring advanced electric actuation for flight control, landing gear, and other critical systems. The continuous innovation in electric motor and power electronics technology also contributes to making electric actuators more viable and attractive for a wider range of aircraft applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of More Electric Aircraft (MEA) concept | +2.5% | Global (North America, Europe, Asia Pacific) | Medium-Term (2025-2030) |

| Growing demand for fuel-efficient and environmentally friendly aircraft | +2.0% | Global | Long-Term (2025-2033) |

| Development and proliferation of Urban Air Mobility (UAM) and eVTOL aircraft | +1.8% | North America, Europe, Asia Pacific | Medium- to Long-Term (2027-2033) |

| Technological advancements in electric motor, power electronics, and control systems | +1.5% | Global | Ongoing (2025-2033) |

| Increase in global commercial aircraft fleet and MRO activities | +1.0% | Asia Pacific, North America, Europe | Medium-Term (2025-2030) |

Aviation Electric Actuator System Market Restraints Analysis

Despite significant growth prospects, the Aviation Electric Actuator System Market faces several restraints that could impede its expansion. One primary challenge is the high cost associated with the research, development, and certification of new electric actuation systems. The aerospace industry operates under extremely stringent safety and reliability standards, which necessitate extensive testing and validation, adding considerable time and expense to the product lifecycle, especially for novel electric systems replacing proven hydraulic ones.

Another significant restraint is the challenge of managing heat dissipation and power density in electric actuators, particularly for high-power applications on larger aircraft. While electric actuators offer weight savings due to the elimination of hydraulic lines, their inherent electrical components generate heat, which needs efficient management to prevent overheating and ensure reliable operation in varied environmental conditions. Furthermore, the integration complexities of new electric systems into existing aircraft designs or older platforms can be a barrier for fleet modernization efforts due to compatibility issues and required infrastructure overhauls.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High development, testing, and certification costs | -1.2% | Global | Long-Term (2025-2033) |

| Technical challenges related to power density, weight, and thermal management | -0.8% | Global | Medium-Term (2025-2030) |

| Stringent aviation regulations and long certification cycles | -0.7% | Global (esp. developed economies) | Long-Term (2025-2033) |

| Complexity of integrating new electric systems with legacy aircraft platforms | -0.5% | Global (esp. MRO sector) | Short- to Medium-Term (2025-2028) |

Aviation Electric Actuator System Market Opportunities Analysis

The Aviation Electric Actuator System Market is presented with numerous opportunities driven by evolving aerospace technologies and market demands. A significant avenue lies in the continued development of all-electric and hybrid-electric aircraft, which will inherently rely on advanced electric actuation systems for all functions, from primary flight controls to utility systems. This segment, though nascent, promises substantial long-term growth as electrification efforts intensify across the industry, moving beyond the "more electric" concept to fully electric designs.

Another key opportunity exists in the expansion into new aerospace applications, including military unmanned aerial vehicles (UAVs) and advanced defense platforms that increasingly utilize precise and reliable electric actuation. Furthermore, the aftermarket and MRO (Maintenance, Repair, and Overhaul) sector presents a steady stream of business for upgrading and maintaining existing electric actuator systems as more aircraft adopt this technology. Innovations in modular design and standardization could also unlock broader market adoption and reduce costs, creating opportunities for more diverse manufacturers to enter the supply chain with specialized components or integrated solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of all-electric and hybrid-electric propulsion aircraft | +1.5% | Global (North America, Europe) | Long-Term (2028-2033) |

| Emergence of new applications in military UAVs and advanced defense platforms | +1.0% | North America, Europe, Asia Pacific | Medium-Term (2026-2031) |

| Expansion of aftermarket services and MRO for electric actuator systems | +0.8% | Global | Ongoing (2025-2033) |

| Development of modular and standardized electric actuator solutions | +0.7% | Global | Medium- to Long-Term (2027-2033) |

Aviation Electric Actuator System Market Challenges Impact Analysis

The Aviation Electric Actuator System Market faces several critical challenges that demand innovative solutions from manufacturers and integrators. A significant hurdle is ensuring extreme reliability and redundancy for flight-critical systems. Electric actuators must meet or exceed the reliability standards of hydraulic systems, which have decades of proven performance. This requires sophisticated design, robust materials, and rigorous testing to guarantee performance under various operational stresses, including extreme temperatures, vibrations, and electromagnetic interference.

Another pressing challenge involves thermal management, especially in high-power applications where compact designs are essential. The heat generated by electric motors and power electronics can degrade performance and reduce lifespan if not efficiently dissipated. Furthermore, as aviation systems become increasingly interconnected and reliant on advanced electronics, cybersecurity threats to electric actuators and their control systems are emerging as a significant concern, requiring robust protective measures. Finally, the harmonization of standards across different aircraft manufacturers and international regulatory bodies presents a complex challenge for widespread adoption and interoperability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring ultra-high reliability and redundancy for safety-critical applications | -1.0% | Global | Long-Term (2025-2033) |

| Effective thermal management in high-power and compact designs | -0.8% | Global | Ongoing (2025-2033) |

| Addressing cybersecurity risks for integrated electric actuator systems | -0.7% | Global | Medium- to Long-Term (2026-2033) |

| Lack of standardized interfaces and protocols across diverse aircraft platforms | -0.5% | Global | Medium-Term (2025-2030) |

Aviation Electric Actuator System Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Aviation Electric Actuator System Market, covering market size estimations, growth forecasts, and detailed segmentation. It examines the key drivers, restraints, opportunities, and challenges influencing market dynamics, along with a comprehensive assessment of the competitive landscape. The report also highlights the impact of emerging technologies such as Artificial Intelligence and the evolving paradigm of More Electric Aircraft (MEA) on the industry's trajectory. It aims to offer strategic insights for stakeholders to navigate the market effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950 Million |

| Market Forecast in 2033 | USD 1.8 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Collins Aerospace (Raytheon Technologies Corporation), Safran S.A., Moog Inc., Parker Hannifin Corporation, Liebherr-International AG, Triumph Group, Woodward Inc., Honeywell International Inc., Eaton Corporation plc, Curtiss-Wright Corporation, KBR Inc., SKF, Actuonix Motion Devices Inc., BAE Systems plc, Meggitt PLC (now part of Parker Hannifin) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aviation Electric Actuator System Market is comprehensively segmented to provide a granular view of its diverse components and applications. This segmentation allows for a detailed analysis of market dynamics across different actuator types, their specific applications within aircraft systems, the various aircraft platforms they serve, and the end-users driving demand. Understanding these segments is crucial for identifying niche opportunities and developing targeted strategies in this evolving market.

Each segment contributes uniquely to the overall market growth, reflecting specific technological requirements and operational priorities. For instance, the shift towards electro-mechanical actuators (EMAs) is prominent within the 'Actuator Type' segment due to their efficiency and precision, while 'Flight Control Surfaces' remain a critical application area requiring the highest levels of reliability. The rise of new aircraft types like eVTOLs introduces entirely new demands, further diversifying the market landscape across various sub-segments, which include specific components vital to system functionality, from motors to complex control units.

- By Actuator Type:

- Linear

- Rotary

- Electro-Hydraulic (Hybrid)

- Electro-Mechanical

- By Application:

- Flight Control Surfaces (Ailerons, Elevators, Rudders, Spoilers)

- Landing Gear Systems (Actuation, Steering, Braking)

- Engine Control (Thrust Reversers, Fuel Valves, Inlet Guide Vanes)

- Utility Systems (Cargo Doors, Environmental Control Systems, Cabin Pressure)

- Thrust Vectoring

- Others (e.g., Seat Actuation, Weapon Bay Doors)

- By Aircraft Type:

- Commercial Aviation

- Narrow-Body Aircraft

- Wide-Body Aircraft

- Regional Jets

- Military Aviation

- Fighter Aircraft

- Transport Aircraft

- Trainer Aircraft

- Military Helicopters

- General Aviation

- Business Jets

- Unmanned Aerial Vehicles (UAVs)/Drones

- Electric Vertical Take-Off and Landing (eVTOL) Aircraft

- Commercial Aviation

- By End-User:

- Original Equipment Manufacturers (OEMs)

- Maintenance, Repair, and Overhaul (MRO) Providers

- Aftermarket

- By Component:

- Motors (Brushless DC Motors, Stepper Motors)

- Gearboxes

- Sensors (Position, Force, Temperature, Pressure)

- Controllers/ECUs (Electronic Control Units)

- Power Electronics (Inverters, Converters)

- Ball Screws

- Lead Screws

- Actuator Housings and Mechanical Parts

Regional Highlights

- North America: This region is a dominant force in the Aviation Electric Actuator System Market, driven by significant defense spending, a large commercial aerospace industry, and extensive research and development activities in advanced aviation technologies. The presence of major aircraft manufacturers and electric actuator system suppliers, coupled with early adoption of MEA concepts and investment in UAM, positions North America as a leading market. Regulatory support for new aircraft designs and strong investment in R&D further bolster its market position.

- Europe: Europe represents another key market, characterized by a robust aerospace manufacturing base and a strong emphasis on sustainable aviation initiatives. Countries like France, Germany, and the UK are at the forefront of developing next-generation aircraft and electric propulsion systems, directly driving the demand for advanced electric actuators. The region's focus on reducing carbon emissions and enhancing aircraft efficiency aligns well with the benefits offered by electric actuation technology, fostering continuous innovation and adoption.

- Asia Pacific (APAC): The Asia Pacific region is projected to exhibit the highest growth rate, fueled by the rapid expansion of air travel, increasing demand for new commercial aircraft, and growing defense budgets in countries like China, India, and Japan. The burgeoning middle class and urbanization trends are leading to significant investments in aviation infrastructure and fleet modernization. This dynamic growth creates substantial opportunities for electric actuator suppliers to enter and expand their presence within this region.

- Latin America: While smaller than the major markets, Latin America shows steady growth in its aviation sector, driven by increasing air connectivity and the modernization of existing aircraft fleets. Investment in new aircraft deliveries and ongoing MRO activities provide opportunities for the adoption of more efficient electric actuator systems. The region's market is expected to grow steadily, albeit at a slower pace compared to the major aerospace hubs.

- Middle East and Africa (MEA): The MEA region is witnessing growth spurred by strategic investments in airport infrastructure, expansion of national airlines, and increasing military spending. Countries in the Middle East, particularly, are investing heavily in new aircraft to support growing tourism and business travel. This development, combined with a focus on defense modernization, contributes to the demand for advanced electric actuation systems, offering long-term growth prospects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aviation Electric Actuator System Market.- Collins Aerospace (Raytheon Technologies Corporation)

- Safran S.A.

- Moog Inc.

- Parker Hannifin Corporation

- Liebherr-International AG

- Triumph Group

- Woodward Inc.

- Honeywell International Inc.

- Eaton Corporation plc

- Curtiss-Wright Corporation

- KBR Inc.

- SKF

- Actuonix Motion Devices Inc.

- BAE Systems plc

- Meggitt PLC (now part of Parker Hannifin)

Frequently Asked Questions

What is an Aviation Electric Actuator System?

An Aviation Electric Actuator System is a device that converts electrical energy into mechanical motion, used to control various aircraft functions such as flight surfaces, landing gear, engine components, and utility systems, replacing traditional hydraulic or pneumatic systems.

Why are electric actuators preferred over hydraulic systems in modern aircraft?

Electric actuators are increasingly preferred due to their advantages in fuel efficiency, reduced weight, lower maintenance costs, simplified design, enhanced reliability, and superior precision and controllability compared to hydraulic systems.

What are the key applications of electric actuators in aircraft?

Key applications include primary flight controls (ailerons, elevators, rudders), landing gear extension/retraction, engine thrust reversers, flap and slat actuation, brake-by-wire systems, and various utility and cabin systems.

How does the 'More Electric Aircraft' concept relate to electric actuator systems?

The 'More Electric Aircraft' (MEA) concept focuses on replacing hydraulic, pneumatic, and mechanical systems with electrically powered alternatives. Electric actuator systems are central to MEA, enabling a reduction in overall aircraft weight, complexity, and fuel consumption.

What is the future outlook for the Aviation Electric Actuator System Market?

The market is poised for significant growth, driven by ongoing aircraft electrification, the emergence of Urban Air Mobility (UAM) and eVTOL aircraft, and continuous advancements in actuator technology, leading to more efficient, reliable, and intelligent systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted