Food Can Market

Food Can Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709869 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Food Can Market Size

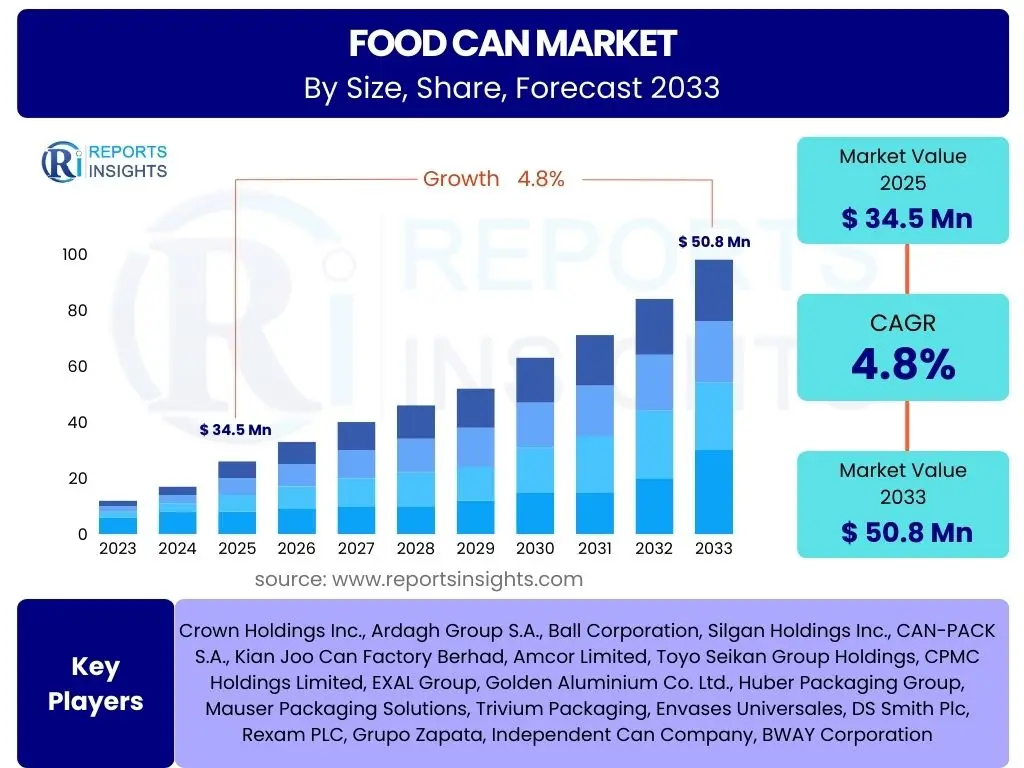

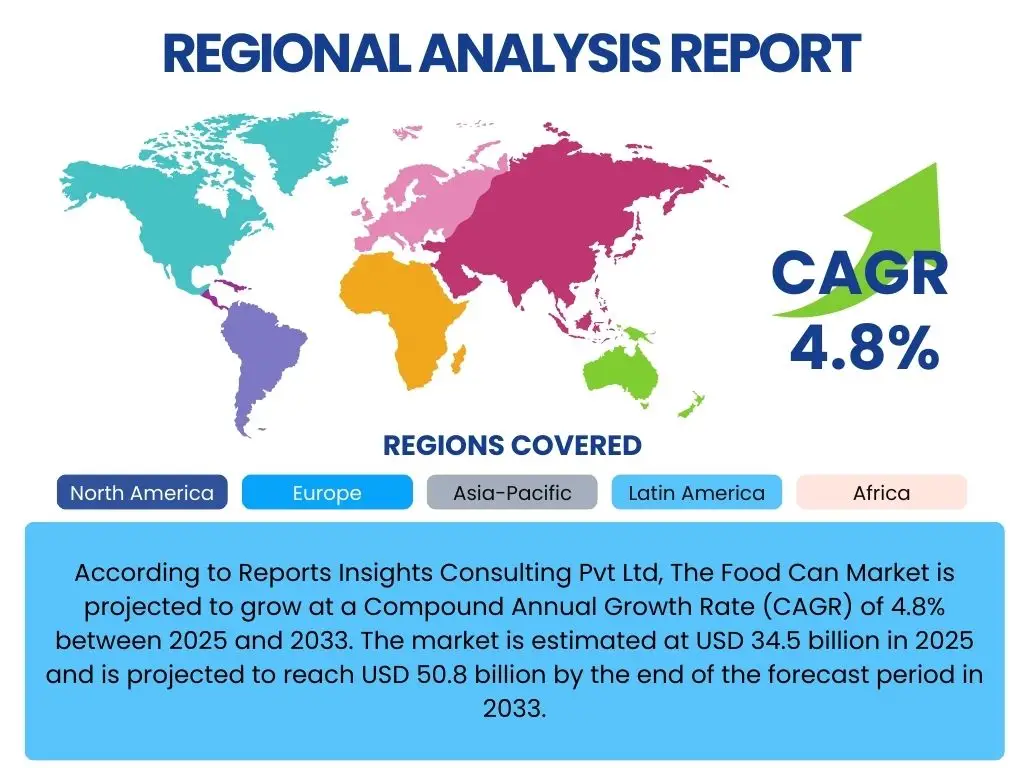

According to Reports Insights Consulting Pvt Ltd, The Food Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 34.5 billion in 2025 and is projected to reach USD 50.8 billion by the end of the forecast period in 2033.

Key Food Can Market Trends & Insights

User inquiries frequently revolve around the evolving landscape of food packaging, particularly the innovations and shifts within the food can sector. Key themes emerging from these discussions include the escalating demand for sustainable packaging solutions, advancements in material science to enhance can performance, and the influence of changing consumer lifestyles on product design and convenience. Furthermore, there is significant interest in how manufacturers are adapting to global supply chain challenges and regulatory pressures, while simultaneously exploring new market opportunities through product diversification and technological integration.

The market is experiencing a notable pivot towards eco-friendly materials and manufacturing processes, driven by both consumer preference and corporate responsibility initiatives. Innovations in lightweighting and the development of alternative coatings are paramount to reducing environmental impact and improving product safety. Additionally, the proliferation of ready-to-eat and on-the-go food options continues to bolster the demand for convenient, durable, and shelf-stable packaging formats that food cans inherently provide. These trends underscore a dynamic industry focused on balancing economic viability with environmental stewardship and evolving consumer needs.

- Increased demand for sustainable and recyclable metal packaging solutions.

- Growth in adoption of lightweighting technologies to reduce material usage and transportation costs.

- Development of advanced internal coatings to enhance food safety and extend shelf life, moving away from BPA.

- Rising popularity of convenient, ready-to-eat, and portion-controlled canned food products.

- Expansion of functional and smart packaging features, including enhanced traceability.

- Shift towards premium and aesthetically appealing can designs to attract discerning consumers.

- Emphasis on supply chain resilience and localized production to mitigate geopolitical and logistical risks.

AI Impact Analysis on Food Can

Common user questions regarding AI's impact on the food can industry center on how artificial intelligence can optimize manufacturing processes, enhance supply chain efficiency, and improve product quality and safety. There is a strong curiosity about the practical applications of AI in areas such as predictive maintenance for production lines, automation of quality control, and demand forecasting to reduce waste and inventory costs. Users are also keen to understand the potential for AI to drive innovation in can design and material selection, and how it might enable greater customization and responsiveness to market shifts.

The integration of AI technologies is poised to revolutionize several aspects of food can production and distribution. By leveraging machine learning algorithms, manufacturers can achieve unprecedented levels of operational efficiency, leading to reduced energy consumption and improved resource utilization. AI's capacity for complex data analysis also offers significant benefits in terms of ensuring consistent product quality, detecting anomalies during manufacturing, and personalizing product offerings based on consumer behavior. This technological advancement represents a strategic imperative for companies aiming to maintain a competitive edge and meet the escalating demands for efficiency, sustainability, and innovation within the industry.

- Optimized Production Processes: AI-driven predictive maintenance reduces downtime and increases operational efficiency in can manufacturing plants.

- Enhanced Quality Control: AI-powered vision systems for automated defect detection in cans, ensuring higher product quality and safety standards.

- Supply Chain Efficiency: AI algorithms for demand forecasting and inventory management, minimizing waste and optimizing logistics for raw materials and finished products.

- Material Innovation: AI-assisted design and simulation for developing new lightweight materials and advanced coatings, improving can performance and sustainability.

- Personalization and Customization: AI-driven insights into consumer preferences enabling manufacturers to produce customized can sizes, shapes, and designs more efficiently.

- Energy Management: AI systems optimizing energy consumption in manufacturing facilities, contributing to sustainability goals.

Key Takeaways Food Can Market Size & Forecast

User queries regarding the food can market's future predominantly focus on understanding the core factors driving its growth and the segments that present the most promising opportunities. There's a particular interest in the balance between traditional uses of food cans and emerging applications, as well as the impact of sustainability trends on overall market trajectory. Users seek clear, actionable insights into how these dynamics translate into market value and growth rates over the forecast period, aiming to identify strategic investment areas and potential challenges.

The market for food cans is characterized by stable growth, underpinned by its essential role in food preservation and distribution. The forecast indicates a steady expansion, driven by both demographic shifts, such as global population growth and urbanization, and evolving consumer preferences for convenient, safe, and long-lasting food storage solutions. While material innovations and environmental concerns are reshaping the industry, the inherent advantages of food cans—durability, recyclability, and barrier protection—ensure their continued relevance and market expansion. The key takeaway emphasizes sustained growth, albeit with an increasing focus on sustainable practices and technological integration to meet future demands.

- Consistent Growth Trajectory: The market is projected for steady expansion, reaching USD 50.8 billion by 2033 from USD 34.5 billion in 2025, demonstrating resilience and essential utility.

- Sustainability as a Core Driver: Increasing consumer and regulatory pressure for eco-friendly packaging solutions significantly boosts demand for highly recyclable metal cans.

- Innovation in Materials and Coatings: Continuous advancements in lightweighting and non-BPA internal coatings are crucial for market competitiveness and product safety.

- Convenience and Shelf-Life: Food cans remain indispensable for preserving food products, catering to the growing demand for convenient and long-lasting food options, especially in urbanizing regions.

- Regional Market Variations: Growth rates and adoption trends will vary significantly across regions, with emerging economies demonstrating faster expansion due to increased industrialization and shifting consumption patterns.

Food Can Market Drivers Analysis

The food can market is fundamentally driven by the enduring need for efficient and safe food preservation globally. Population growth and urbanization, particularly in emerging economies, are significant accelerators, as they translate into increased demand for packaged and shelf-stable food products. This demographic shift necessitates packaging solutions that can withstand extended supply chains and diverse climatic conditions while ensuring food safety and nutritional integrity. The inherent barrier properties of metal cans make them an ideal choice for meeting these foundational requirements, fostering continuous demand across various food categories.

Beyond basic preservation, evolving consumer lifestyles play a crucial role. The rising prevalence of single-person households, busy work schedules, and a preference for convenience foods further fuels the market. Canned foods offer unparalleled ease of storage, preparation, and portion control, aligning perfectly with modern dietary habits. Additionally, the growing awareness and preference for sustainable packaging materials contribute significantly to market expansion, with metal cans being celebrated for their high recyclability rates and circular economy potential. Manufacturers are actively responding to these drivers by innovating in can design, material science, and production efficiency to solidify the food can's position in the global food supply chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Population Growth and Urbanization | +1.2% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Increasing Demand for Convenient & Ready-to-Eat Foods | +0.9% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| High Recyclability and Sustainability of Metal Cans | +0.8% | Europe, North America, Japan | Mid to Long-term (2025-2033) |

| Enhanced Food Preservation and Shelf Life Capabilities | +0.7% | Global | Long-term (2025-2033) |

| Technological Advancements in Can Manufacturing | +0.6% | Global | Short to Mid-term (2025-2029) |

| Rise in Disposable Income in Developing Nations | +0.5% | China, India, Southeast Asia | Long-term (2025-2033) |

| Growth of Organized Retail and E-commerce for Packaged Foods | +0.4% | Global | Mid-term (2025-2030) |

Food Can Market Restraints Analysis

Despite its robust market position, the food can industry faces several significant restraints that could temper its growth trajectory. One primary concern revolves around the increasing consumer preference for fresh or minimally processed foods, which often translates to a reduced reliance on canned goods. This shift is particularly evident in developed markets where health and wellness trends emphasize natural, unpackaged produce, posing a challenge to the traditional appeal of canned products. Furthermore, persistent misconceptions about the nutritional value of canned foods, despite scientific evidence to the contrary, continue to influence purchasing decisions and create a perception barrier.

Another critical restraint is the intense competition from alternative packaging materials. Flexible packaging, glass, and plastic containers offer diverse advantages such as lighter weight, visual appeal, and resealability, which resonate with specific consumer needs and product types. While metal cans boast superior barrier properties and recyclability, these competitors often provide cost-effective or aesthetically preferred options for certain applications. Additionally, fluctuating raw material prices, particularly for steel and aluminum, directly impact manufacturing costs and, consequently, the final product pricing, which can influence consumer affordability and market competitiveness. The regulatory landscape, including evolving standards for food contact materials and environmental impact, also presents a complex environment that requires continuous adaptation and investment from manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Consumer Preference for Fresh & Minimally Processed Foods | -0.8% | North America, Europe | Long-term (2025-2033) |

| Competition from Alternative Packaging Materials (Flexible, Glass, Plastic) | -0.7% | Global | Long-term (2025-2033) |

| Fluctuating Raw Material Prices (Steel, Aluminum) | -0.6% | Global | Short to Mid-term (2025-2029) |

| Perception Issues and Misconceptions about Canned Food Quality | -0.5% | Developed Markets | Long-term (2025-2033) |

| Stringent Regulations on Food Contact Materials (e.g., BPA-free coatings) | -0.4% | Europe, North America | Mid-term (2025-2030) |

| High Initial Capital Investment for Manufacturing Facilities | -0.3% | Developing Markets | Long-term (2025-2033) |

Food Can Market Opportunities Analysis

The food can market is ripe with opportunities, primarily driven by the ongoing global emphasis on sustainability and the circular economy. As consumers and regulators increasingly prioritize environmentally responsible packaging, the inherent recyclability of metal cans positions them favorably against many plastic alternatives. This creates a significant avenue for market expansion, especially as manufacturers invest in advanced recycling technologies and promote the environmental benefits of their products. Furthermore, the burgeoning demand for sustainable, plant-based, and organic food products often requires robust, sterile packaging solutions, presenting a perfect fit for the protective qualities of food cans.

Technological innovation also unlocks substantial growth prospects. The development of advanced, non-BPA internal coatings not only addresses health concerns but also allows for a wider range of food products to be safely packaged in cans, including acidic and sensitive items. Lightweighting initiatives continue to reduce material usage and transport costs, enhancing the economic and environmental appeal of food cans. Moreover, the expansion into emerging markets, particularly in Asia Pacific and Africa, where food security and shelf-stable options are paramount, offers considerable untapped potential. These regions are experiencing rapid urbanization and a rise in disposable incomes, translating into greater demand for packaged foods and the dependable containment that food cans provide.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable & Recyclable Packaging Solutions | +1.1% | Global, particularly Europe and North America | Long-term (2025-2033) |

| Expansion into Emerging Markets with Rising Disposable Incomes | +1.0% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Development of Advanced Non-BPA Coatings and Lightweight Materials | +0.9% | Global | Mid to Long-term (2025-2033) |

| Increasing Consumer Preference for Plant-Based and Organic Canned Foods | +0.8% | North America, Europe | Mid-term (2025-2030) |

| Innovation in Can Aesthetics and Functionality (e.g., easy-open, resealable) | +0.7% | Global | Short to Mid-term (2025-2029) |

| Partnerships and Collaborations with Food Manufacturers for Custom Solutions | +0.6% | Global | Mid-term (2025-2030) |

| Strategic Investments in Automation and Smart Manufacturing | +0.5% | Global | Short to Mid-term (2025-2029) |

Food Can Market Challenges Impact Analysis

The food can market faces a range of challenges that require strategic navigation to maintain growth and profitability. One significant hurdle is the escalating cost of raw materials, particularly aluminum and steel. These price volatilities, often influenced by global economic conditions, trade policies, and energy costs, directly impact manufacturing expenses and can erode profit margins if not effectively managed. Manufacturers must constantly seek efficiencies in production and explore hedging strategies to mitigate these financial risks, adding complexity to operational planning.

Another substantial challenge stems from evolving consumer perceptions and preferences. While food cans offer numerous benefits, a segment of the population associates them with less fresh or highly processed foods, which can hinder market penetration, especially in health-conscious demographics. Addressing this requires robust marketing efforts focused on educating consumers about the nutritional benefits, safety, and sustainability of canned goods. Furthermore, the industry faces continuous pressure to innovate in areas like BPA-free coatings and lighter designs, which, while creating opportunities, also demand significant R&D investment and compliance with increasingly stringent environmental and health regulations across diverse geographical markets. Intense competition from alternative packaging formats also pressures the market, requiring constant differentiation and value proposition enhancement.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices (Aluminum, Steel) | -0.9% | Global | Short to Mid-term (2025-2029) |

| Intense Competition from Alternative Packaging Materials | -0.8% | Global | Long-term (2025-2033) |

| Negative Consumer Perceptions Regarding Canned Food vs. Fresh | -0.7% | Developed Markets | Long-term (2025-2033) |

| Stringent and Evolving Regulatory Standards for Food Contact Materials | -0.6% | Europe, North America, Japan | Mid-term (2025-2030) |

| High Energy Consumption in Manufacturing Processes | -0.5% | Global | Long-term (2025-2033) |

| Managing Global Supply Chain Disruptions and Geopolitical Risks | -0.4% | Global | Short-term (2025-2027) |

| Need for Continuous Investment in R&D for Innovation and Sustainability | -0.3% | Global | Long-term (2025-2033) |

Food Can Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global food can industry, covering historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, segmented by various parameters such as material, product type, application, and region. It further delves into the competitive landscape, profiling key industry players and their strategic initiatives, alongside an analysis of the impact of emerging technologies like AI on market evolution. The report offers critical insights for stakeholders seeking to understand market trends and make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 34.5 Billion |

| Market Forecast in 2033 | USD 50.8 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Crown Holdings Inc., Ardagh Group S.A., Ball Corporation, Silgan Holdings Inc., CAN-PACK S.A., Kian Joo Can Factory Berhad, Amcor Limited, Toyo Seikan Group Holdings, CPMC Holdings Limited, EXAL Group, Golden Aluminium Co. Ltd., Huber Packaging Group, Mauser Packaging Solutions, Trivium Packaging, Envases Universales, DS Smith Plc, Rexam PLC, Grupo Zapata, Independent Can Company, BWAY Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The food can market is extensively segmented to provide a detailed understanding of its diverse components and dynamics. These segmentations are critical for identifying key growth areas, understanding competitive landscapes, and tailoring strategic approaches for various applications and regional markets. The primary categorizations include material type, which differentiates between steel and aluminum cans based on their respective properties and cost-effectiveness, and product type, distinguishing between two-piece and three-piece can constructions due to their manufacturing processes and end-use suitability. Further segmentation by application highlights specific food categories such as fruits and vegetables, meat and seafood, and ready-to-eat meals, reflecting varied preservation needs and consumer demands.

An additional layer of analysis involves segmenting by end-use sector, categorizing demand from commercial entities like food manufacturers and the residential sector. This comprehensive segmentation framework allows for a granular analysis of market trends, enabling stakeholders to pinpoint niche opportunities and address specific challenges across the value chain. Understanding these distinct market segments is essential for developing targeted marketing strategies, optimizing production capabilities, and innovating in response to evolving consumer preferences and industry standards, thereby supporting sustained market expansion and competitive advantage.

- By Material:

- Steel: Widely used for its strength and cost-effectiveness, particularly for products requiring high-pressure processing.

- Aluminum: Valued for its lightweight properties, excellent recyclability, and suitability for various food and beverage items.

- By Product Type:

- 2-Piece Cans: Preferred for their seamless body, lighter weight, and efficient manufacturing, commonly used for beverages and some food items.

- 3-Piece Cans: Versatile and robust, suitable for a wide range of food products, offering flexibility in size and shape.

- By Application:

- Fruits & Vegetables: A traditional and major segment, leveraging cans for seasonal preservation and extended shelf life.

- Meat & Seafood: Essential for preserving protein-rich products, ensuring safety and extended storage.

- Pet Food: A significant and growing application, providing durable and convenient packaging for animal nutrition.

- Soups & Sauces: Cans offer ideal barrier protection and convenience for these viscous food items.

- Ready-to-Eat Meals: Catering to modern lifestyles, providing quick and convenient meal solutions.

- Beverages (Non-alcoholic food cans): Including fruit juices, concentrates, and non-carbonated drinks.

- Other Food Products: Encompasses diverse items like dairy products, bakery ingredients, and specialty foods.

- By End-use Sector:

- Commercial: Includes food manufacturers, restaurants, and institutional food service providers.

- Residential: Direct consumer purchases for household use.

Regional Highlights

- North America: A mature market characterized by high consumption of canned goods, a strong focus on sustainability initiatives, and continuous innovation in can design and materials. The United States and Canada lead in adopting advanced packaging technologies and have a well-established recycling infrastructure.

- Europe: Driven by stringent environmental regulations and high consumer awareness regarding sustainability. Countries like Germany, the UK, and France are at the forefront of lightweighting and the adoption of BPA-free coatings, alongside a stable demand for traditional canned food products.

- Asia Pacific (APAC): Represents the fastest-growing region, fueled by rapid urbanization, increasing disposable incomes, and changing dietary habits. China and India are major contributors, experiencing significant growth in packaged food consumption, with demand rising for both basic and premium canned goods. Southeast Asian countries also show substantial potential.

- Latin America: Exhibiting steady growth, primarily influenced by economic development, an expanding middle class, and the increasing penetration of organized retail. Brazil and Mexico are key markets, with a growing demand for convenient and shelf-stable food options.

- Middle East and Africa (MEA): Emerging as a promising market due to population growth, improved economic conditions, and rising food security concerns. The region increasingly relies on imported and locally produced canned foods for extended shelf life and accessibility, driving investment in food processing and packaging infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Can Market.- Crown Holdings Inc.

- Ardagh Group S.A.

- Ball Corporation

- Silgan Holdings Inc.

- CAN-PACK S.A.

- Kian Joo Can Factory Berhad

- Amcor Limited

- Toyo Seikan Group Holdings

- CPMC Holdings Limited

- EXAL Group

- Golden Aluminium Co. Ltd.

- Huber Packaging Group

- Mauser Packaging Solutions

- Trivium Packaging

- Envases Universales

- DS Smith Plc

- Rexam PLC

- Grupo Zapata

- Independent Can Company

- BWAY Corporation

Frequently Asked Questions

Analyze common user questions about the Food Can market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Food Can Market?

The Food Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated value of USD 50.8 billion by 2033.

What are the primary drivers for the Food Can Market?

Key drivers include global population growth and urbanization, increasing demand for convenient and ready-to-eat foods, the high recyclability and sustainability of metal cans, and their effective food preservation capabilities. Technological advancements also play a significant role.

How do sustainability concerns impact the Food Can Market?

Sustainability is a major opportunity and driver for the Food Can Market. The high recyclability of metal cans aligns with growing consumer and regulatory demand for eco-friendly packaging, fostering innovation in lightweighting and material use.

What challenges does the Food Can Market face?

Challenges include volatility in raw material prices (aluminum, steel), intense competition from alternative packaging materials like plastic and glass, negative consumer perceptions regarding canned versus fresh foods, and stringent regulatory standards for food contact materials.

How is AI expected to influence the Food Can industry?

AI is anticipated to significantly impact the food can industry by optimizing production processes through predictive maintenance, enhancing quality control with automated defect detection, improving supply chain efficiency via demand forecasting, and assisting in the development of new materials and designs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted