Autonomou Trailer Terminal Tractor Market

Autonomou Trailer Terminal Tractor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707371 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

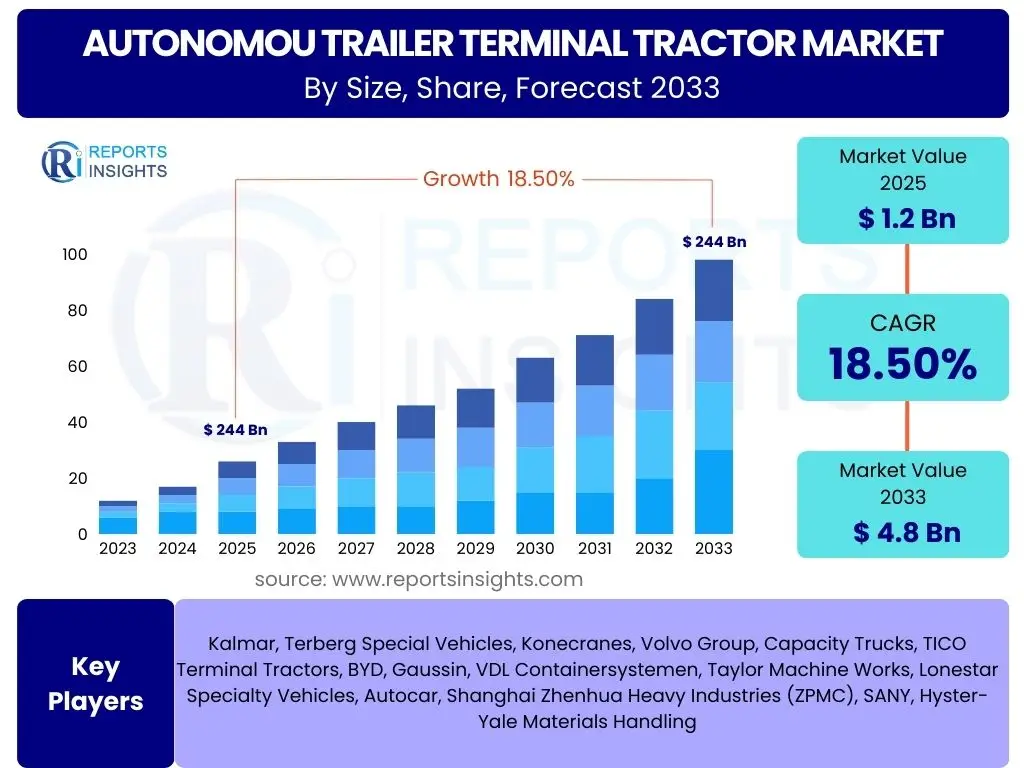

Autonomou Trailer Terminal Tractor Market Size

According to Reports Insights Consulting Pvt Ltd, The Autonomou Trailer Terminal Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 4.8 Billion by the end of the forecast period in 2033.

Key Autonomou Trailer Terminal Tractor Market Trends & Insights

The Autonomou Trailer Terminal Tractor market is currently experiencing significant transformative trends driven by the imperative for enhanced operational efficiency and safety within logistics and supply chain sectors. Automation is at the forefront, with advancements in sensor technology, real-time data analytics, and sophisticated navigation systems enabling these vehicles to operate with minimal human intervention. This shift is not only about reducing labor costs but also about optimizing throughput and mitigating human error in highly dynamic environments such as port terminals, warehouses, and distribution centers.

Another prominent trend is the increasing focus on electrification. As global sustainability initiatives gain momentum and stricter emission regulations are enforced, the adoption of electric autonomous terminal tractors is accelerating. These vehicles offer reduced operational noise, lower maintenance requirements, and zero tailpipe emissions, aligning with corporate environmental responsibilities and contributing to cleaner operational sites. The integration of advanced battery technologies and rapid charging infrastructure is further supporting this transition, making electric models a more viable and attractive option for long-term fleet investments.

Furthermore, the market is witnessing a convergence of technologies, including Artificial intelligence, Internet of Things (IoT), and 5G connectivity. This integration facilitates robust vehicle-to-infrastructure (V2I) and vehicle-to-vehicle (V2V) communication, enabling highly coordinated movements, predictive maintenance, and real-time operational adjustments. Such technological synergy enhances the overall intelligence and responsiveness of autonomous fleets, leading to more efficient resource utilization and optimized logistics flows. These trends collectively underscore a market moving towards fully integrated, sustainable, and intelligent terminal operations.

- Increasing adoption of fully autonomous and semi-autonomous capabilities.

- Rising demand for electric and hybrid autonomous terminal tractors due to environmental concerns and operational cost savings.

- Integration of advanced sensor technologies, including LiDAR, radar, and cameras, for improved perception and safety.

- Growth in cloud-based platforms and real-time data analytics for fleet management and predictive maintenance.

- Expansion of connectivity solutions, such as 5G and V2X communication, for enhanced vehicle coordination.

- Emphasis on modular and scalable autonomous solutions to meet diverse operational needs.

AI Impact Analysis on Autonomou Trailer Terminal Tractor

Artificial intelligence is profoundly reshaping the Autonomou Trailer Terminal Tractor market by enhancing decision-making capabilities, optimizing operational workflows, and improving overall safety standards. Users frequently inquire about how AI enables these vehicles to navigate complex environments, handle dynamic scenarios, and predict maintenance needs. AI algorithms facilitate advanced perception through sensory data fusion, allowing tractors to accurately identify trailers, obstacles, and personnel, even in challenging weather conditions or low visibility. This intelligence is crucial for autonomous operation, enabling precise positioning and seamless trailer coupling and uncoupling, thereby reducing idle times and boosting productivity.

Moreover, AI plays a pivotal role in optimizing route planning and traffic management within terminal environments. By continuously analyzing real-time data on traffic congestion, trailer availability, and destination priorities, AI systems can dynamically adjust routes to minimize travel time and maximize efficiency. This predictive capability extends to resource allocation, ensuring that the right autonomous tractor is deployed for the right task at the optimal time. The intelligent allocation of tasks and dynamic scheduling capabilities are key areas of interest for operators seeking to maximize asset utilization and operational throughput.

Beyond operational efficiency, AI significantly contributes to predictive maintenance and enhanced safety. AI-driven analytics can monitor vehicle performance, identify anomalies, and predict potential equipment failures before they occur, allowing for proactive maintenance and minimizing costly downtime. In terms of safety, AI algorithms continuously learn from operational data to refine obstacle avoidance, emergency braking, and path planning, reducing the likelihood of accidents. User concerns often revolve around the reliability and robustness of AI systems in real-world, unpredictable scenarios, emphasizing the need for rigorous testing and continuous algorithm improvement to build trust in these advanced capabilities.

- Enhanced perception and navigation through sensor fusion and machine learning algorithms.

- Optimized route planning and traffic management within complex terminal environments.

- Predictive maintenance capabilities, reducing downtime and operational costs.

- Improved safety through advanced anomaly detection and autonomous emergency braking.

- Real-time decision-making for dynamic task allocation and resource optimization.

- Facilitates human-machine collaboration through intuitive interfaces and adaptive behaviors.

Key Takeaways Autonomou Trailer Terminal Tractor Market Size & Forecast

The Autonomou Trailer Terminal Tractor market is poised for substantial expansion, driven by the escalating demand for automated and efficient logistics solutions across global industries. A primary takeaway from the market size and forecast analysis is the robust Compound Annual Growth Rate (CAGR) projected through 2033, indicating a significant industry shift towards smart, interconnected material handling systems. This growth trajectory is fundamentally underpinned by the pressing need for enhanced operational throughput, reduced labor dependency, and improved safety protocols in high-volume environments such as ports, warehouses, and manufacturing facilities. The forecast underscores the increasing recognition among industry stakeholders of the long-term cost benefits and productivity gains offered by autonomous solutions.

Another crucial insight is the accelerating adoption of electric variants within the autonomous terminal tractor segment. Environmental regulations, corporate sustainability goals, and the inherent operational advantages of electric vehicles, such as lower noise levels and reduced maintenance, are significantly influencing purchasing decisions. This shift indicates a broader industry commitment to sustainable practices and a move away from traditional fossil fuel-powered equipment. The market's future growth will be heavily influenced by advancements in battery technology and the expansion of charging infrastructure, making electric autonomous tractors an even more compelling investment.

Furthermore, the market's evolution is characterized by continuous technological innovation, particularly in the realm of Artificial Intelligence, advanced sensor arrays, and connectivity. These advancements are not merely incremental but are foundational to enabling higher levels of autonomy, improving the accuracy of tasks, and facilitating seamless integration into existing logistics ecosystems. The forecast suggests that continuous investment in research and development will be paramount for market players to maintain competitive advantage and meet the evolving demands for sophisticated autonomous capabilities. Overall, the market is set to become a cornerstone of modern, highly efficient, and environmentally conscious logistics operations globally.

- Significant growth anticipated, driven by automation and efficiency demands.

- Electrification is a key growth accelerator, aligning with sustainability goals.

- Technological advancements, particularly in AI and IoT, are critical enablers.

- Increased focus on safety and reduced operational costs are primary motivators for adoption.

- Market expansion driven by applications in ports, logistics hubs, and manufacturing sites.

Autonomou Trailer Terminal Tractor Market Drivers Analysis

The Autonomou Trailer Terminal Tractor market is propelled by a confluence of powerful drivers that are fundamentally transforming logistics and supply chain operations. A primary driver is the pervasive challenge of labor shortages within the trucking and logistics industries. As the availability of skilled human operators for terminal tractors dwindles, businesses are increasingly turning to autonomous solutions to maintain and enhance operational continuity and efficiency. These autonomous systems offer a reliable alternative, ensuring consistent performance regardless of labor availability, which is particularly critical in 24/7 operational environments such as major ports and distribution centers.

Secondly, the escalating demand for operational efficiency and rapid turnaround times across various industries significantly boosts the adoption of autonomous terminal tractors. Traditional manual operations often face limitations in speed, consistency, and precision, leading to bottlenecks and delays. Autonomous tractors, with their ability to perform repetitive tasks with high accuracy and speed, drastically reduce loading and unloading times, optimize trailer movements, and enhance overall throughput. This efficiency gain translates directly into cost savings and improved service levels, making them an attractive investment for logistics providers and industrial operators aiming to streamline their processes and gain a competitive edge.

Furthermore, stringent environmental regulations and the growing corporate emphasis on sustainability are powerful catalysts for market growth. Governments and international bodies are imposing stricter emission standards, pushing industries to adopt greener technologies. Autonomous electric terminal tractors offer a compelling solution, providing zero direct emissions, reduced noise pollution, and lower energy consumption compared to their diesel counterparts. This not only helps companies comply with regulations but also aligns with their broader environmental, social, and governance (ESG) objectives, enhancing their public image and operational sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Labor Shortages and Rising Labor Costs | +4.2% | North America, Europe, APAC | Short to Mid-term (2025-2029) |

| Increased Demand for Operational Efficiency and Throughput | +3.8% | Global | Mid to Long-term (2027-2033) |

| Stringent Environmental Regulations and Sustainability Goals | +3.5% | Europe, North America, China | Short to Mid-term (2025-2030) |

| Technological Advancements in AI, Sensors, and Connectivity | +3.0% | Global | Long-term (2028-2033) |

| Growth in E-commerce and Logistics Hubs | +2.5% | Global | Mid to Long-term (2026-2033) |

Autonomou Trailer Terminal Tractor Market Restraints Analysis

Despite the strong growth drivers, the Autonomou Trailer Terminal Tractor market faces several significant restraints that could impede its full potential. A primary challenge is the substantial upfront capital investment required for adopting these advanced systems. The cost of autonomous tractors, coupled with the necessary infrastructure upgrades for charging, communication networks, and fleet management software, can be prohibitive for many businesses, particularly small and medium-sized enterprises. This high initial outlay poses a significant barrier to entry and can deter potential adopters, especially in regions with limited access to capital or where existing infrastructure is not readily adaptable.

Another key restraint involves the complexities associated with regulatory frameworks and the slow pace of standardization. As autonomous technologies are still evolving, many countries lack comprehensive and unified regulations governing their deployment and operation on public or semi-public roads. Issues such as liability in case of accidents, certification processes for autonomous systems, and interoperability standards across different manufacturers remain largely undefined or vary significantly by region. This regulatory uncertainty creates hesitation among potential users and manufacturers, slowing down widespread adoption and hindering market expansion, particularly across international borders.

Furthermore, concerns regarding safety and cybersecurity pose critical impediments to market growth. While autonomous systems are designed to enhance safety, public perception and trust remain a challenge. Any incident, however minor, involving an autonomous vehicle can severely impact confidence in the technology. Additionally, the increasing reliance on digital connectivity and complex software makes these systems vulnerable to cybersecurity threats, including hacking and data breaches. Ensuring robust cybersecurity measures and demonstrating irrefutable safety records are essential to overcome these concerns, but achieving this requires continuous investment and adherence to stringent security protocols, adding to the operational complexities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment | -3.5% | Global, particularly emerging economies | Short to Mid-term (2025-2030) |

| Regulatory and Legal Uncertainties | -2.8% | Global, varies by region | Short to Mid-term (2025-2031) |

| Safety Concerns and Public Perception | -2.2% | Global | Mid-term (2026-2032) |

| Integration Complexity with Existing Infrastructure | -1.9% | Global, especially older facilities | Short to Mid-term (2025-2029) |

| Cybersecurity Risks | -1.5% | Global | Mid to Long-term (2027-2033) |

Autonomou Trailer Terminal Tractor Market Opportunities Analysis

Significant opportunities exist within the Autonomou Trailer Terminal Tractor market, driven by expanding application areas and continuous technological evolution. One major opportunity lies in the untapped potential for widespread adoption across various industrial sectors beyond traditional logistics and port operations. While ports and large distribution centers have been early adopters, there is immense scope for autonomous terminal tractors in large-scale manufacturing plants, airports, rail yards, and container freight stations. These environments often face similar challenges regarding labor intensity, efficiency bottlenecks, and safety concerns, making them ideal candidates for autonomous solutions. The customization of autonomous systems to suit specific industry requirements can unlock substantial new revenue streams and market penetration.

Another compelling opportunity stems from the ongoing advancements in Artificial intelligence, machine learning, and sensor technologies. As these technologies mature, they enable higher levels of autonomy, improved decision-making capabilities, and enhanced performance in dynamic and unstructured environments. Future autonomous terminal tractors will likely feature more sophisticated predictive analytics for maintenance, real-time adaptive routing, and enhanced interoperability with other automated systems within a smart logistics ecosystem. Investing in research and development to integrate cutting-edge AI and IoT solutions will allow market players to offer highly differentiated and value-added products, catering to the evolving demands for increasingly intelligent and self-optimizing operations.

Furthermore, the development of robust charging infrastructure and battery technologies presents a lucrative opportunity, particularly for electric autonomous terminal tractors. As the demand for sustainable and electric vehicles rises, companies that can provide comprehensive solutions, including efficient charging stations, battery-as-a-service models, and intelligent energy management systems, will gain a significant competitive advantage. Partnerships with energy providers and infrastructure developers can facilitate faster deployment and wider acceptance of electric autonomous fleets. The strategic focus on developing holistic electric autonomous solutions, from the vehicle itself to the supporting energy ecosystem, will be crucial for capitalizing on the long-term growth potential in this environmentally conscious segment of the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas (e.g., Manufacturing, Airports) | +3.2% | Global | Mid to Long-term (2027-2033) |

| Advancements in AI, Machine Learning, and IoT Integration | +2.9% | Global | Long-term (2028-2033) |

| Development of Robust Charging Infrastructure for Electric Variants | +2.5% | Europe, North America, China | Mid to Long-term (2026-2033) |

| Partnerships and Collaborations within the Ecosystem | +2.0% | Global | Mid-term (2026-2031) |

| Increasing Focus on Remote Operations and Telematics | +1.8% | Global | Short to Mid-term (2025-2029) |

Autonomou Trailer Terminal Tractor Market Challenges Impact Analysis

The Autonomou Trailer Terminal Tractor market, while promising, faces several operational and developmental challenges that demand strategic solutions. One significant challenge is the complexity of integrating autonomous systems into existing, often legacy, infrastructure and operational workflows. Many port terminals, warehouses, and distribution centers were not originally designed for autonomous vehicle operations, requiring substantial modifications to layouts, communication systems, and safety protocols. This integration can be costly, time-consuming, and disruptive, often necessitating a phased approach that can slow down adoption rates. Ensuring seamless interoperability between autonomous tractors and other material handling equipment, as well as human operators, adds another layer of complexity.

Another critical challenge revolves around the development and maintenance of public trust and acceptance of autonomous heavy machinery. Despite the potential for enhanced safety, any perceived risk or actual incident can severely impact adoption. Addressing concerns related to system reliability, potential job displacement, and the ethical implications of autonomous decision-making requires transparent communication, rigorous testing, and clear demonstrations of safety and efficiency. Overcoming resistance from labor unions and ensuring proper training for existing workforces to adapt to new roles within an automated environment are also crucial for successful deployment and long-term acceptance.

Furthermore, the talent gap in specialized skills presents a formidable barrier. The design, deployment, maintenance, and operation of autonomous trailer terminal tractors require a highly specialized workforce proficient in robotics, AI, software engineering, cybersecurity, and advanced mechanics. There is a current shortage of professionals with these integrated skill sets, making it challenging for companies to recruit and retain the necessary talent. This deficit can impact the pace of innovation, quality of deployment, and ongoing support for autonomous fleets, thereby constraining market growth. Addressing this challenge necessitates strategic investments in education, training programs, and collaborative efforts between industry and academia to cultivate the required expertise.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Legacy Systems and Infrastructure | -2.0% | Global | Short to Mid-term (2025-2030) |

| Public Trust and Acceptance Issues | -1.8% | Global | Mid-term (2026-2032) |

| Shortage of Skilled Workforce for Development & Maintenance | -1.5% | Global | Short to Mid-term (2025-2029) |

| Cybersecurity Threats and Data Privacy Concerns | -1.2% | Global | Mid to Long-term (2027-2033) |

| High Research & Development Costs | -1.0% | Global | Long-term (2028-2033) |

Autonomou Trailer Terminal Tractor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Autonomou Trailer Terminal Tractor Market, offering critical insights into its current state, historical performance, and future growth trajectories. The scope encompasses a detailed examination of market size and forecast from 2025 to 2033, utilizing a robust methodology that considers various macroeconomic and industry-specific factors. It explores key market trends, identifying the technological shifts, operational imperatives, and regulatory landscapes that are shaping the industry's evolution. The report also provides a thorough assessment of the impact of Artificial Intelligence on market dynamics, highlighting its role in enhancing autonomy, efficiency, and safety.

Furthermore, the report offers a granular analysis of market drivers, restraints, opportunities, and challenges, providing a holistic view of the forces influencing market expansion and potential impediments. It includes detailed segmentation analysis across various parameters such as component, propulsion, autonomy level, and application, enabling stakeholders to understand the most lucrative and high-growth segments. Regional highlights are meticulously covered, dissecting market performance and potential across North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, offering localized insights into adoption rates and market potential.

A crucial component of this report is the profiling of top key players operating in the Autonomou Trailer Terminal Tractor market. This section provides an overview of their strategic initiatives, product offerings, and competitive positioning, offering valuable intelligence for market entrants and established companies alike. The report is designed to serve as a strategic tool for investors, manufacturers, logistics providers, and technology developers seeking to make informed decisions and capitalize on the emerging opportunities within this dynamic and rapidly evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 4.8 Billion |

| Growth Rate | 18.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kalmar, Terberg Special Vehicles, Konecranes, Volvo Group, Capacity Trucks, TICO Terminal Tractors, BYD, Gaussin, VDL Containersystemen, Taylor Machine Works, Lonestar Specialty Vehicles, Autocar, Shanghai Zhenhua Heavy Industries (ZPMC), SANY, Hyster-Yale Materials Handling |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Autonomou Trailer Terminal Tractor market is meticulously segmented to provide a granular understanding of its diverse components and applications, enabling stakeholders to pinpoint areas of high growth and strategic investment. The segmentation by component typically includes hardware, software, and services. Hardware encompasses the physical components such as advanced sensors (LiDAR, radar, cameras), GPS modules, actuators, and control units that enable autonomous operation. Software comprises the intelligent algorithms for navigation, fleet management systems, and operating software that orchestrate vehicle movements and integrate with larger logistical networks. Services involve the crucial post-sale support, including maintenance, training, and system integration, which are vital for the successful deployment and sustained operation of autonomous fleets.

Further segmentation by propulsion type distinguishes between electric, hybrid, and diesel autonomous terminal tractors. The electric segment is gaining significant traction due to increasing environmental awareness, stringent emission regulations, and the operational benefits of electric powertrains such as reduced noise and lower maintenance costs. Hybrid models offer a transitional solution, combining the benefits of electric power with the extended range of diesel, while diesel variants, though facing environmental pressures, still maintain a presence due to their robust performance in certain heavy-duty applications. This propulsion-based analysis highlights the industry's shift towards more sustainable and efficient energy sources.

Segmentation by autonomy level categorizes tractors into semi-autonomous and fully autonomous systems. Semi-autonomous tractors feature advanced driver-assistance systems (ADAS) that assist human operators, while fully autonomous vehicles operate entirely without human intervention, leveraging sophisticated AI and sensor fusion. The market is also segmented by application, including their use in ports and terminals, warehouses and distribution centers, manufacturing facilities, airports, and rail yards. Each application area presents unique operational demands and regulatory landscapes, influencing the specific requirements and adoption rates of autonomous terminal tractors. This multi-faceted segmentation provides a comprehensive framework for understanding market dynamics and identifying niche opportunities.

- By Component: Hardware, Software, Services

- By Propulsion: Electric, Hybrid, Diesel

- By Autonomy Level: Semi-Autonomous, Fully Autonomous

- By Application: Ports and Terminals, Warehouses and Distribution Centers, Manufacturing Facilities, Airports, Rail Yards

Regional Highlights

- North America: This region is a leading adopter of autonomous terminal tractors, driven by severe labor shortages, a strong focus on supply chain optimization, and significant investments in smart port and logistics infrastructure. The presence of major e-commerce players and large distribution networks further fuels demand, with a growing emphasis on fully electric and highly automated solutions.

- Europe: Europe exhibits strong growth, largely influenced by stringent environmental regulations pushing for electric and zero-emission vehicles, along with a high degree of automation in its advanced logistics and manufacturing sectors. Countries like Germany, Netherlands, and Scandinavia are at the forefront of implementing autonomous solutions in ports and industrial facilities, often supported by government initiatives for sustainable transport.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, propelled by rapid industrialization, burgeoning e-commerce, and massive investments in new port infrastructure and logistics hubs, particularly in China, India, and Southeast Asia. The region benefits from technological advancements and a willingness to adopt innovative solutions to improve efficiency and manage increasing trade volumes, though cost remains a consideration.

- Latin America: This region is an emerging market for autonomous terminal tractors, with growth primarily driven by the modernization of port facilities and the expansion of logistics operations in key economic zones. While adoption is slower due to economic factors and infrastructure limitations, there is a growing recognition of the need for automation to enhance competitiveness and efficiency.

- Middle East and Africa (MEA): The MEA region is witnessing increasing interest and adoption, particularly in the Gulf Cooperation Council (GCC) countries, due to massive infrastructure projects, smart city initiatives, and efforts to diversify economies beyond oil. Investments in state-of-the-art ports and logistics parks are creating fertile ground for autonomous vehicle deployment, often with a focus on integrating renewable energy solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Autonomou Trailer Terminal Tractor Market.- Kalmar (Cargotec Corporation)

- Terberg Special Vehicles

- Konecranes

- Volvo Group

- Capacity Trucks (REV Group)

- TICO Terminal Tractors

- BYD Company Ltd.

- Gaussin SA

- VDL Containersystemen B.V.

- Taylor Machine Works, Inc.

- Lonestar Specialty Vehicles

- Autocar, LLC

- Shanghai Zhenhua Heavy Industries (ZPMC)

- SANY Group

- Hyster-Yale Materials Handling, Inc.

Frequently Asked Questions

What is the projected growth rate for the Autonomou Trailer Terminal Tractor Market?

The Autonomou Trailer Terminal Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, driven by increasing automation and efficiency demands in logistics.

What are the primary drivers of growth in this market?

Key growth drivers include labor shortages, the escalating demand for operational efficiency and throughput in logistics, stringent environmental regulations promoting electrification, and continuous technological advancements in AI and sensor systems.

How does AI impact the development of autonomous trailer terminal tractors?

AI significantly enhances autonomous trailer terminal tractors by improving navigation, enabling advanced perception, optimizing route planning, facilitating predictive maintenance, and enhancing overall safety through intelligent decision-making and anomaly detection.

What are the main challenges facing the adoption of autonomous terminal tractors?

Major challenges include high upfront capital investment, complex integration with existing legacy infrastructure, regulatory uncertainties, public trust and acceptance issues regarding autonomous technologies, and a shortage of skilled personnel for development and maintenance.

Which regions are expected to be key markets for autonomous trailer terminal tractors?

North America and Europe are leading the market due to robust infrastructure and automation focus, while Asia Pacific is projected to be the fastest-growing region driven by rapid industrialization and significant investments in logistics hubs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted