Antifouling Agent Market

Antifouling Agent Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702913 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Antifouling Agent Market Size

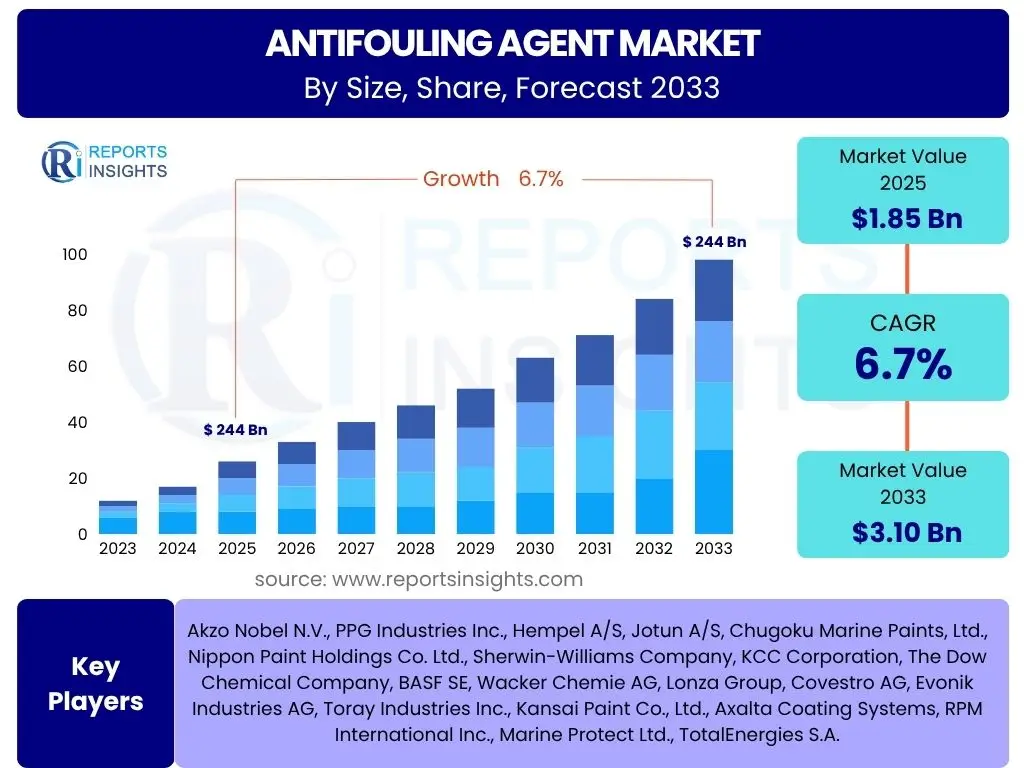

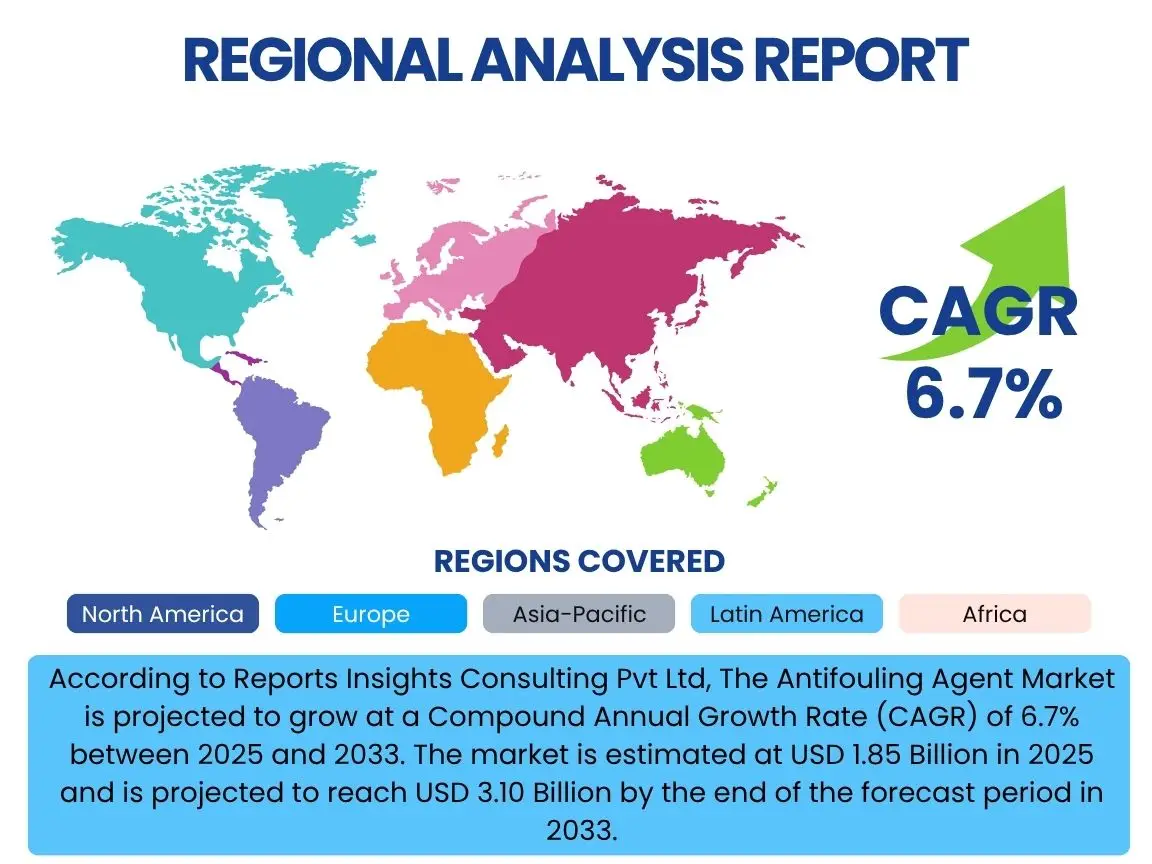

According to Reports Insights Consulting Pvt Ltd, The Antifouling Agent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.10 Billion by the end of the forecast period in 2033.

Key Antifouling Agent Market Trends & Insights

The Antifouling Agent Market is observing significant shifts driven by evolving environmental regulations and technological advancements. User inquiries frequently highlight the transition towards more sustainable and eco-friendly solutions, moving away from traditional biocide-based systems due to their adverse ecological impacts. There is also a keen interest in the development of novel coating technologies that offer enhanced performance and longer lifespans, thereby reducing maintenance costs and dry-docking frequency for marine vessels and structures. Furthermore, the expansion of the global shipping industry and increasing investments in offshore infrastructure are foundational drivers shaping market dynamics.

Another prevalent area of interest concerns the integration of smart technologies and advanced materials, such as nanotechnology and self-polishing copolymers, which are designed to improve the efficacy and durability of antifouling coatings. Users are also keen on understanding the regional disparities in market growth, influenced by differing regulatory landscapes and the concentration of marine activities. The shift towards non-toxic or low-toxicity solutions, driven by stricter international maritime organization (IMO) guidelines, is a dominant theme, pushing research and development efforts toward innovative, environmentally compliant alternatives that maintain high performance standards.

- Growing demand for eco-friendly and biocide-free antifouling solutions.

- Increased adoption of advanced coating technologies like foul-release and nanocoatings.

- Expansion of the global shipping fleet and maritime trade.

- Rising investment in offshore oil & gas, renewable energy, and aquaculture infrastructure.

- Stricter environmental regulations governing marine coatings.

AI Impact Analysis on Antifouling Agent

User questions regarding the impact of Artificial Intelligence (AI) on the Antifouling Agent market primarily center on how AI can enhance efficiency, reduce costs, and accelerate the development of new solutions. There is considerable interest in AI's role in optimizing the application process of antifouling coatings, predicting their lifespan, and identifying optimal maintenance schedules. Users anticipate AI could lead to more precise formulation of coatings, leveraging vast datasets on marine environments, fouling organisms, and material performance to develop highly customized and effective solutions that are less reliant on trial-and-error methods. This shift is expected to revolutionize research and development by shortening innovation cycles.

Furthermore, concerns and expectations revolve around AI's ability to monitor coating integrity in real-time using drones or autonomous underwater vehicles (AUVs) equipped with AI-driven vision systems. This capability could enable predictive maintenance, ensuring coatings are reapplied only when necessary, thus minimizing waste and maximizing efficiency. The integration of AI in supply chain management for antifouling agents, from raw material sourcing to distribution, is also a topic of interest, with users anticipating improved logistics and reduced operational complexities. While the direct implementation is nascent, the potential for AI to optimize every stage of the antifouling lifecycle, from design to disposal, is a key area of user inquiry and future expectation.

- AI-driven optimization of antifouling coating formulation and material discovery.

- Predictive maintenance schedules for marine vessels based on AI analysis of coating performance.

- Automated inspection of hull coatings using AI-powered robotics and image processing.

- Enhanced supply chain management and logistics for antifouling agent distribution.

- AI-enabled data analysis for understanding fouling patterns and environmental conditions.

Key Takeaways Antifouling Agent Market Size & Forecast

Common user questions about the Antifouling Agent market size and forecast reveal a focus on understanding the primary drivers of growth, the influence of regulatory changes, and the long-term sustainability of the market. Insights suggest that while traditional maritime activities remain a core demand source, emerging applications in offshore renewable energy and aquaculture are poised to contribute significantly to market expansion. Users are particularly interested in how technological innovations, especially in biocide-free alternatives, will shape market dynamics and valuation over the forecast period, and whether these advancements can effectively balance performance with environmental compliance.

Another crucial takeaway frequently sought by users is the regional distribution of market growth, with an emphasis on identifying high-growth geographies driven by industrialization and increasing maritime trade volumes. The market is characterized by a steady growth trajectory, underpinned by the indispensable need for vessel and infrastructure protection against biofouling. The forecast indicates a transition toward more sophisticated and environmentally responsible solutions, which will likely command premium pricing and drive overall market value upward, reflecting a shift from volume-driven sales to value-added propositions. This implies a market increasingly focused on innovation, sustainability, and high-performance solutions rather than solely on cost-effectiveness.

- Sustained growth driven by global maritime trade and offshore industries.

- Significant market shift towards environmentally compliant and biocide-free solutions.

- Technological advancements are key to enhancing product performance and market value.

- Asia Pacific is projected to remain a dominant and high-growth region.

- Regulatory frameworks worldwide play a critical role in shaping market demand and product development.

Antifouling Agent Market Drivers Analysis

The Antifouling Agent market is fundamentally driven by the continuous expansion of global maritime activities and the imperative to protect marine assets from biofouling. The growth in international shipping, including commercial freight, passenger vessels, and naval fleets, directly translates into increased demand for effective antifouling solutions to maintain vessel speed, fuel efficiency, and structural integrity. Furthermore, the burgeoning aquaculture industry, reliant on submerged structures like nets and cages, necessitates robust antifouling measures to ensure productivity and prevent disease transmission. These sectors collectively underpin a consistent demand for protective coatings, driving market expansion and innovation.

Beyond the direct growth in maritime and aquaculture sectors, stringent environmental regulations imposed by international bodies such as the IMO and various national authorities are compelling a significant shift in the market. The ban or restriction on harmful biocides like tributyltin (TBT) has spurred intense research and development into novel, eco-friendly alternatives. This regulatory push, while presenting challenges, simultaneously acts as a powerful driver for innovation, promoting the adoption of advanced, compliant technologies that are more sustainable. The increasing awareness of the economic and environmental costs associated with biofouling, including increased fuel consumption and the spread of invasive species, further propels the demand for high-performance antifouling agents across the globe.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Global Maritime Trade & Shipping Industry | +1.5% | Global, particularly Asia Pacific, Europe | Long-term (2025-2033) |

| Stringent Environmental Regulations on Biocides | +1.2% | Europe, North America, Global (IMO) | Mid-to-Long-term (2025-2030) |

| Expansion of Aquaculture Sector | +0.8% | Asia Pacific, Europe, Latin America | Long-term (2025-2033) |

| Increasing Demand for Fuel Efficiency in Vessels | +1.0% | Global | Long-term (2025-2033) |

| Development of Offshore Energy Infrastructure (Oil & Gas, Wind) | +0.7% | Europe, North America, Asia Pacific | Mid-to-Long-term (2025-2033) |

Antifouling Agent Market Restraints Analysis

The Antifouling Agent market faces several inherent restraints that could temper its growth trajectory. One significant challenge is the high research and development (R&D) costs associated with discovering and commercializing new, effective, and environmentally benign antifouling chemistries. The development process is lengthy, complex, and requires extensive testing to ensure performance and compliance with evolving global regulations, often leading to substantial financial outlays before a product reaches the market. This can deter smaller players and limit the pace of innovation, concentrating market power among a few large entities capable of sustaining such investments.

Another major restraint is the performance limitations and shorter lifespan of some advanced biocide-free or low-biocide coatings compared to traditional, highly effective, but environmentally harmful solutions. While the industry is moving towards sustainable options, achieving comparable long-term protection against diverse fouling organisms across varied marine environments remains a technical hurdle. Furthermore, the relatively higher cost of these newer, more sophisticated coatings can be a deterrent for end-users, especially in cost-sensitive segments of the market or during periods of economic slowdown in the shipbuilding and marine industries. Economic downturns, geopolitical tensions, and fluctuations in raw material prices can also disrupt the supply chain and manufacturing processes, further impacting market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D Costs & Long Product Development Cycles | -0.9% | Global | Long-term (2025-2033) |

| Performance Limitations of Eco-Friendly Alternatives | -0.7% | Global | Mid-term (2025-2029) |

| Higher Cost of Advanced Biocide-Free Coatings | -0.6% | Developing Regions, Price-sensitive Segments | Mid-term (2025-2029) |

| Economic Volatility in Shipbuilding and Shipping Industries | -0.5% | Global | Short-to-Mid-term (2025-2027) |

| Lack of Universal Antifouling Solution for All Environments | -0.4% | Global | Long-term (2025-2033) |

Antifouling Agent Market Opportunities Analysis

Significant opportunities are emerging in the Antifouling Agent market, primarily driven by the ongoing shift towards sustainability and the demand for advanced material solutions. The development of next-generation biocide-free technologies, such as foul-release coatings based on silicone or fluoropolymer chemistries, and bio-inspired surfaces that mimic natural antifouling mechanisms, presents a substantial growth avenue. These innovations not only address environmental concerns but also offer the potential for superior long-term performance and reduced maintenance requirements. Companies investing heavily in green chemistry and nanotechnology are poised to capture a larger share of the evolving market, catering to increasingly stringent global regulatory standards and eco-conscious end-users.

Furthermore, the expansion into new application areas beyond traditional shipping and offshore oil and gas structures offers considerable growth potential. The burgeoning offshore renewable energy sector, including wind farms and tidal energy installations, requires robust antifouling solutions for submerged components to ensure operational efficiency and extend asset lifespan. Similarly, the growing global aquaculture industry, with its reliance on submerged nets and pens, represents a vital, underserved segment seeking effective and non-toxic antifouling protection. The integration of smart coating technologies, which can monitor fouling levels and self-repair, also presents a lucrative niche for market players. These diverse applications and technological advancements create a fertile ground for innovation and market diversification, driving the overall growth trajectory of the antifouling agent market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Commercialization of Biocide-Free Coatings | +1.8% | Global | Long-term (2025-2033) |

| Expansion into Offshore Renewable Energy Sector | +1.5% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Increased Demand from Sustainable Aquaculture Practices | +1.0% | Asia Pacific, Europe, Latin America | Mid-to-Long-term (2025-2033) |

| Technological Advancements in Nano-coatings & Smart Coatings | +0.9% | Global | Long-term (2025-2033) |

| Retrofit Market for Existing Vessels & Structures | +0.7% | Global | Mid-term (2025-2029) |

Antifouling Agent Market Challenges Impact Analysis

The Antifouling Agent market is confronted by a range of challenges that necessitate strategic responses from industry players. One of the most significant hurdles is navigating the complex and ever-evolving global regulatory landscape concerning marine coatings. Environmental agencies worldwide are continuously revising permissible biocide levels and introducing new restrictions, demanding constant reformulation and re-certification of products. This regulatory stringency not only increases compliance costs but also creates uncertainty for product development and market entry, often delaying the commercialization of new solutions that meet performance and environmental benchmarks simultaneously.

Another critical challenge lies in developing universally effective and long-lasting antifouling solutions that perform optimally across diverse marine environments, including varying water temperatures, salinity levels, and types of fouling organisms. What works effectively in one region or for a specific vessel type may not be as efficacious elsewhere, leading to fragmented market demand and the need for specialized product portfolios. Furthermore, ensuring the cost-effectiveness and scalability of novel, high-performance technologies, particularly biocide-free options, remains a key concern. Balancing superior performance, environmental compliance, and competitive pricing is crucial for widespread market adoption. The potential for intellectual property infringement and the need for robust patent protection also present ongoing challenges in a technologically advancing market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating Complex & Evolving Environmental Regulations | -1.0% | Global | Long-term (2025-2033) |

| Achieving Cost-Effectiveness for Advanced Technologies | -0.8% | Global, especially developing markets | Mid-term (2025-2029) |

| Developing Universal Solutions for Diverse Fouling Organisms | -0.7% | Global | Long-term (2025-2033) |

| Ensuring Long-Term Performance of Eco-Friendly Coatings | -0.6% | Global | Mid-term (2025-2029) |

| Supply Chain Disruptions & Raw Material Price Volatility | -0.5% | Global | Short-to-Mid-term (2025-2027) |

Antifouling Agent Market - Updated Report Scope

This report provides an extensive analysis of the global Antifouling Agent market, covering historical performance from 2019 to 2023, current market dynamics for 2024, and forward-looking projections up to 2033. It details market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope encompasses detailed segmentation by type, application, and end-use, offering insights into emerging trends and the competitive landscape. The report also highlights the impact of regulatory frameworks and technological innovations, including AI, on market evolution, providing a holistic view for stakeholders seeking to understand and capitalize on the market's potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.10 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Akzo Nobel N.V., PPG Industries Inc., Hempel A/S, Jotun A/S, Chugoku Marine Paints, Ltd., Nippon Paint Holdings Co. Ltd., Sherwin-Williams Company, KCC Corporation, The Dow Chemical Company, BASF SE, Wacker Chemie AG, Lonza Group, Covestro AG, Evonik Industries AG, Toray Industries Inc., Kansai Paint Co., Ltd., Axalta Coating Systems, RPM International Inc., Marine Protect Ltd., TotalEnergies S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Antifouling Agent market is meticulously segmented to provide a granular view of its diverse components, allowing for targeted analysis of market dynamics across different product types, applications, and end-user industries. This comprehensive segmentation helps in identifying key growth pockets, understanding technological preferences, and assessing demand patterns in various sectors. The primary segmentation distinguishes between biocidal and biocide-free coatings, reflecting the industry's significant shift towards environmentally compliant solutions. Further divisions highlight critical application areas, such as marine vessels (including commercial, naval, and recreational), offshore structures, and the rapidly expanding aquaculture sector.

Each segment holds unique characteristics and growth drivers. For instance, the biocidal segment, while facing increasing regulatory pressure, continues to be a dominant force due to its proven efficacy and cost-effectiveness for certain applications. Conversely, the biocide-free segment, comprising foul-release and hard coatings, is experiencing accelerated growth fueled by environmental mandates and technological advancements promising comparable performance without ecological harm. Analyzing these segments individually provides critical insights into market maturity, competitive intensity, and future investment opportunities across the global antifouling landscape. The end-use segmentation further delineates demand from commercial shipping, recreational boating, defense, and broader industrial applications, each with distinct requirements and adoption rates.

- By Type:

- Biocidal Coatings

- Copper-based

- Organotin-based (historically, now largely restricted)

- Others (Zinc pyrithione, Diuron, etc.)

- Biocide-free Coatings

- Foul Release Coatings (Silicone, Fluoropolymer-based)

- Hard Coatings (Ceramic, Epoxy, UV-cured)

- Other Physical Barriers (Fibers, textured surfaces)

- Biocidal Coatings

- By Application:

- Ships

- Commercial Vessels (Tankers, Cargo Ships, Container Ships)

- Naval Vessels

- Recreational Boats

- Offshore Structures

- Oil & Gas Rigs

- Wind Turbines (Submerged parts)

- Pipelines

- Aquaculture

- Fish Cages

- Nets

- Other Equipment

- Others (Buoys, Docks, Submerged Sensors, Power Plant Intakes)

- Ships

- By End-use:

- Commercial

- Recreational

- Defense

- Industrial

Regional Highlights

- Asia Pacific (APAC): Dominates the Antifouling Agent market due to its robust shipbuilding industry, extensive maritime trade routes, and significant presence of aquaculture activities, particularly in countries like China, South Korea, Japan, and Southeast Asian nations. Rapid industrialization and increasing port activities further drive demand.

- Europe: A mature market characterized by stringent environmental regulations and a strong focus on sustainable and high-performance solutions. Countries like Germany, Norway, the Netherlands, and the UK are at the forefront of adopting advanced biocide-free technologies and investing in offshore renewable energy infrastructure.

- North America: Exhibits steady growth, driven by a significant recreational boating sector, a strong naval presence, and increasing investments in offshore energy. Environmental regulations, especially in coastal states, are pushing the adoption of eco-friendly antifouling solutions.

- Latin America: An emerging market with growing shipbuilding activities and a developing aquaculture industry, especially in countries like Brazil and Chile. While currently smaller, the region presents opportunities for market expansion as its maritime and fishing sectors grow.

- Middle East and Africa (MEA): Growth is primarily fueled by the region's strategic importance in global oil and gas shipping, port development, and naval defense. Investments in maritime infrastructure and a focus on maintaining efficient crude oil transportation contribute to market demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Antifouling Agent Market.- Akzo Nobel N.V.

- PPG Industries Inc.

- Hempel A/S

- Jotun A/S

- Chugoku Marine Paints, Ltd.

- Nippon Paint Holdings Co. Ltd.

- Sherwin-Williams Company

- KCC Corporation

- The Dow Chemical Company

- BASF SE

- Wacker Chemie AG

- Lonza Group

- Covestro AG

- Evonik Industries AG

- Toray Industries Inc.

- Kansai Paint Co., Ltd.

- Axalta Coating Systems

- RPM International Inc.

- Marine Protect Ltd.

- TotalEnergies S.A.

Frequently Asked Questions

Analyze common user questions about the Antifouling Agent market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are antifouling agents and why are they important?

Antifouling agents are specialized coatings or chemicals applied to submerged surfaces of marine vessels and structures to prevent the accumulation of marine organisms (biofouling) such as barnacles, algae, and mussels. They are crucial for maintaining hull integrity, optimizing vessel speed and fuel efficiency, and preventing the spread of invasive species.

What are the main types of antifouling agents?

The main types include biocidal coatings, which release active substances to deter fouling (e.g., copper-based), and biocide-free coatings, which prevent attachment through physical properties (e.g., foul-release coatings like silicone-based, or hard, low-friction coatings). There are also emerging technologies like biomimetic and nanotechnology-based solutions.

What are the key environmental concerns associated with antifouling agents?

Historically, environmental concerns revolved around the toxicity of traditional biocides, particularly organotin compounds (like TBT), which were harmful to non-target marine life. Current concerns focus on managing the environmental impact of copper and developing fully non-toxic, eco-friendly alternatives that meet stringent regulations while maintaining performance.

How do regulations impact the Antifouling Agent market?

Regulations, primarily from the International Maritime Organization (IMO) and national environmental agencies, significantly impact the market by restricting or banning harmful biocides, pushing for more environmentally compliant solutions, and driving innovation towards sustainable and high-performance products. Compliance is a major factor influencing product development and market adoption.

What are the future trends in the Antifouling Agent market?

Future trends include a strong shift towards advanced biocide-free coatings, increased research into bio-inspired and nano-coatings, the integration of smart monitoring technologies and AI for optimized application and maintenance, and expansion into new applications like offshore renewable energy and sustainable aquaculture. The market will continue to prioritize efficacy combined with environmental responsibility.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted