Automotive Steel Market

Automotive Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710094 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Steel Market Size

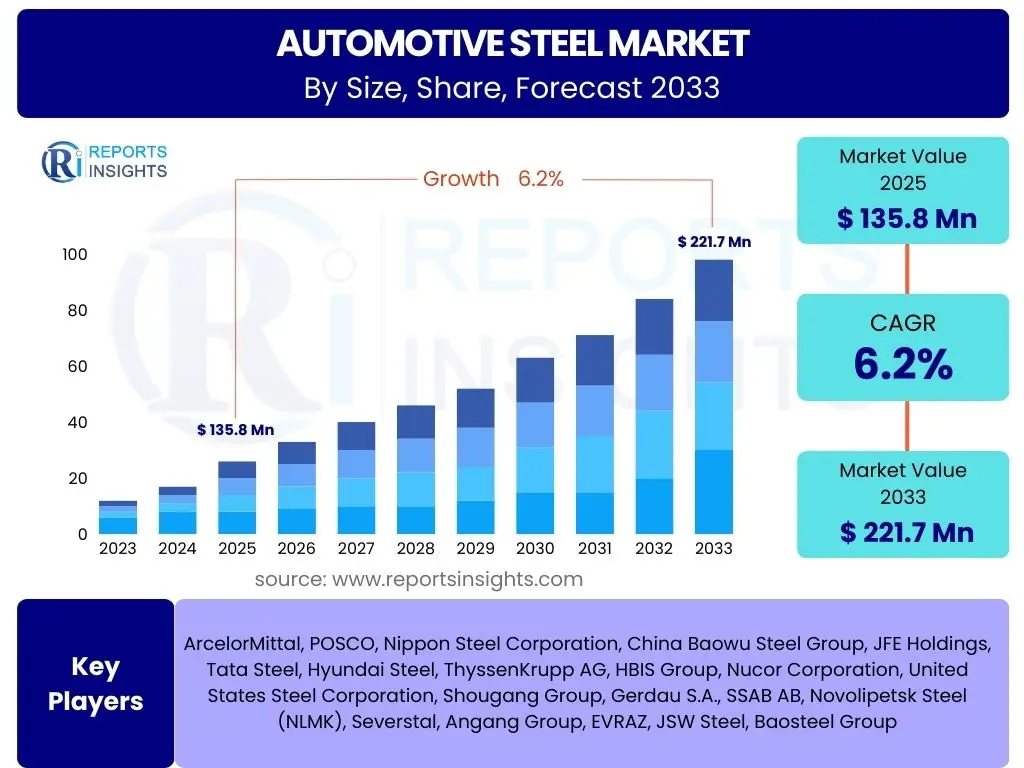

According to Reports Insights Consulting Pvt Ltd, The Automotive Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 135.8 Billion in 2025 and is projected to reach USD 221.7 Billion by the end of the forecast period in 2033.

Key Automotive Steel Market Trends & Insights

User inquiries frequently highlight the evolving landscape of vehicle manufacturing, with a strong emphasis on sustainability, performance, and efficiency. Common questions revolve around the types of steel used in new vehicle architectures, the impact of electric vehicle (EV) growth on material choices, and the industry's response to environmental regulations. There is also significant interest in how advanced manufacturing techniques and material innovations are shaping the future of automotive steel, particularly concerning lightweighting and enhanced safety features. These trends collectively underscore a market moving towards more sophisticated, environmentally conscious, and performance-driven steel solutions.

- Increased adoption of Advanced High-Strength Steels (AHSS) for lightweighting and enhanced safety.

- Growing demand for automotive steel in Electric Vehicle (EV) battery casings and structural components.

- Emphasis on sustainable production methods and recycled content in steel manufacturing.

- Development of innovative steel grades with improved crash performance and corrosion resistance.

- Integration of digital manufacturing and Industry 4.0 technologies in steel production processes.

AI Impact Analysis on Automotive Steel

Common user questions regarding AI's impact on the automotive steel sector primarily focus on its potential to revolutionize production efficiency, material design, and supply chain management. Users are keen to understand how artificial intelligence and machine learning algorithms can optimize steel manufacturing processes, predict material performance, and enhance quality control. There is also interest in AI's role in predictive maintenance for equipment, improving operational uptime, and streamlining complex logistics within the steel supply chain for automotive applications. The overarching theme is the expectation that AI will drive significant advancements in both the operational and innovative aspects of automotive steel production and utilization.

- AI-driven optimization of steel production processes, leading to improved energy efficiency and reduced waste.

- Machine learning algorithms for predictive maintenance of manufacturing equipment, enhancing operational reliability.

- AI-assisted material design for developing new, high-performance steel grades with specific properties.

- Enhanced quality control and defect detection in steel manufacturing through computer vision and AI.

- Optimized supply chain logistics and inventory management using AI-powered forecasting and planning tools.

Key Takeaways Automotive Steel Market Size & Forecast

Analysis of common user questions reveals a strong interest in understanding the core growth drivers and future trajectory of the automotive steel market. Users frequently inquire about the primary factors contributing to market expansion, such as the increasing demand for advanced vehicle technologies and global vehicle production trends. There's also a significant focus on how material innovation, particularly in lightweighting and electrification, will influence market size and value. The overall sentiment points towards a market characterized by continuous evolution, driven by technological advancements and shifting consumer preferences, demanding more specialized and high-performance steel solutions.

- The market is poised for significant growth, driven by increasing global vehicle production and the evolution of automotive technologies.

- Advanced High-Strength Steels (AHSS) will be a critical growth segment due to their lightweighting and safety benefits.

- Electric Vehicle (EV) expansion represents a substantial opportunity for specialized steel applications in battery structures and chassis.

- Sustainability initiatives and circular economy principles are increasingly influencing material selection and market dynamics.

- Geographic shifts in automotive manufacturing, particularly towards Asia Pacific, will significantly impact regional market shares.

Automotive Steel Market Drivers Analysis

The global automotive steel market is significantly propelled by the increasing demand for lightweight and fuel-efficient vehicles. As governments worldwide implement stricter emission standards, automakers are compelled to incorporate advanced materials that reduce vehicle weight without compromising safety or structural integrity. This imperative directly fuels the adoption of Advanced High-Strength Steels (AHSS), which offer superior strength-to-weight ratios compared to conventional steel grades. The continuous innovation in AHSS technologies allows for thinner gauges and more complex designs, supporting both environmental compliance and enhanced vehicle performance.

Another major driver is the robust growth in global vehicle production, particularly in emerging economies and the expanding electric vehicle (EV) segment. While alternative materials such as aluminum and composites are gaining traction, steel remains the dominant material due to its cost-effectiveness, recyclability, and well-established manufacturing infrastructure. The burgeoning EV market, in particular, requires specialized steel for battery enclosures, motor components, and structural frames that can withstand higher stresses and offer better crash protection. This sustained demand from both conventional and electric vehicle segments underpins the market's positive trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for lightweight and fuel-efficient vehicles | +1.5% | Global, particularly Europe & North America | 2025-2033 |

| Growth in global automotive production, including Electric Vehicles (EVs) | +1.2% | Asia Pacific, North America, Europe | 2025-2033 |

| Stricter emission and safety regulations | +0.8% | Europe, China, North America | 2025-2030 |

| Technological advancements in Advanced High-Strength Steels (AHSS) | +0.7% | Global | 2025-2033 |

| Cost-effectiveness and recyclability of steel over alternative materials | +0.5% | Global | 2025-2033 |

Automotive Steel Market Restraints Analysis

One of the primary restraints in the automotive steel market is the persistent volatility in raw material prices, particularly iron ore, coking coal, and scrap steel. Fluctuations in these commodity prices directly impact the production costs for steel manufacturers, leading to unpredictable pricing for automotive customers. This uncertainty can complicate budgeting and long-term planning for automakers, potentially forcing them to absorb higher costs or seek alternative materials if steel prices become excessively unstable. Such volatility makes it challenging for the entire supply chain to maintain consistent profit margins and competitiveness.

Another significant restraint is the increasing competition from alternative lightweight materials. Materials such as aluminum, carbon fiber composites, and plastics are continuously improving in terms of performance and cost-effectiveness. While steel remains dominant, automakers are increasingly exploring multi-material designs to meet aggressive lightweighting targets, especially in electric vehicles where battery weight is a critical factor. This trend poses a threat to steel's market share, particularly in high-end vehicle segments or specific components where the weight-saving benefits of alternatives outweigh their higher material costs. The ongoing research and development into these competing materials could further erode steel's prevalence in future vehicle designs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices (iron ore, coking coal) | -1.0% | Global | 2025-2033 |

| Intensifying competition from alternative lightweight materials (aluminum, composites) | -0.9% | North America, Europe, Asia Pacific | 2025-2033 |

| High energy consumption and environmental concerns in steel production | -0.6% | Global | 2025-2030 |

| Trade protectionism and tariffs on steel imports | -0.4% | North America, Europe, China | Short-to-Mid-term |

| Capital-intensive nature of upgrading steel production facilities | -0.3% | Global | Mid-to-Long-term |

Automotive Steel Market Opportunities Analysis

The development and widespread adoption of Advanced High-Strength Steels (AHSS) and Ultra High-Strength Steels (UHSS) represent a significant opportunity for the automotive steel market. These advanced grades offer superior strength-to-weight ratios, enabling automakers to design lighter vehicles without compromising safety or structural integrity. As vehicle manufacturers strive to meet stringent emission targets and enhance fuel efficiency, the demand for AHSS/UHSS is expected to surge. Continued innovation in metallurgical processes will lead to new generations of these steels, expanding their application across various vehicle components and cementing steel's role in future automotive designs.

Another compelling opportunity lies in the burgeoning electric vehicle (EV) market. While EVs present challenges in terms of battery weight, they also create new demands for specialized steel components. Steel is crucial for battery enclosures, motor laminations, and structural elements designed to protect occupants during collisions, especially with the added mass of battery packs. Furthermore, the push for a circular economy and increased sustainability offers steel producers an advantage due to steel's inherent recyclability. Developing sustainable production methods and utilizing recycled content can enhance steel's appeal, aligning with evolving consumer preferences and regulatory pressures for environmentally friendly manufacturing. These factors collectively present a robust pathway for market expansion and value creation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Further development and adoption of Advanced High-Strength Steels (AHSS) | +1.8% | Global | 2025-2033 |

| Growing demand from Electric Vehicle (EV) manufacturing for specialized steel | +1.5% | Asia Pacific, Europe, North America | 2025-2033 |

| Emphasis on sustainability and circular economy in material selection | +0.9% | Europe, North America | 2025-2030 |

| Emerging markets for automotive production in Southeast Asia and Africa | +0.6% | Asia Pacific, Africa | Mid-to-Long-term |

| Technological advancements in steel forming and joining techniques | +0.4% | Global | 2025-2030 |

Automotive Steel Market Challenges Impact Analysis

The automotive steel market faces significant challenges from increasingly stringent environmental regulations and the ongoing pressure to decarbonize industrial processes. Steel production is energy-intensive and traditionally associated with high carbon emissions, which puts considerable pressure on manufacturers to adopt cleaner technologies and practices. Meeting these environmental targets often requires substantial capital investment in new equipment, carbon capture technologies, or shifts to green hydrogen-based steelmaking, which can be costly and impact overall competitiveness. Failure to adapt to these regulatory demands could lead to increased operational costs, fines, or even limitations on market access in certain regions.

Another major challenge is the complexity of global supply chains and the potential for disruptions. Geopolitical tensions, trade disputes, natural disasters, and pandemics have all demonstrated the fragility of global supply networks for raw materials and finished steel products. Any interruption can lead to material shortages, production delays for automakers, and significant price spikes. Managing these risks requires robust supply chain diversification, enhanced inventory management, and closer collaboration between steel producers and automotive manufacturers. Furthermore, the rapid pace of technological change in the automotive sector, particularly the shift towards new vehicle architectures and propulsion systems, demands constant innovation from steel producers to ensure their products remain relevant and competitive.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations and decarbonization pressures | -0.8% | Europe, North America, China | 2025-2033 |

| Supply chain disruptions and geopolitical instability | -0.7% | Global | Short-to-Mid-term |

| High capital expenditure required for technological upgrades and R&D | -0.5% | Global | 2025-2033 |

| Talent shortages in advanced metallurgy and manufacturing | -0.3% | Developed economies | 2025-2030 |

| Rapid pace of technological change in automotive industry | -0.2% | Global | 2025-2030 |

Automotive Steel Market - Updated Report Scope

This comprehensive market insights report provides an in-depth analysis of the Automotive Steel Market, covering historical performance, current trends, and future projections from 2025 to 2033. It examines key market drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report segments the market by product type, application, and vehicle type across major global regions, providing stakeholders with critical data for strategic decision-making. Furthermore, it includes a detailed competitive analysis of leading market players, highlighting their strategies and market positions, alongside an assessment of the impact of emerging technologies like AI on the sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 135.8 Billion |

| Market Forecast in 2033 | USD 221.7 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, POSCO, Nippon Steel Corporation, China Baowu Steel Group, JFE Holdings, Tata Steel, Hyundai Steel, ThyssenKrupp AG, HBIS Group, Nucor Corporation, United States Steel Corporation, Shougang Group, Gerdau S.A., SSAB AB, Novolipetsk Steel (NLMK), Severstal, Angang Group, EVRAZ, JSW Steel, Baosteel Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive steel market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of material types, their specific applications within vehicles, and their adoption across different vehicle categories. The market is primarily divided by type, including various grades of steel with distinct properties; by application, detailing where these steels are utilized in vehicle construction; and by vehicle type, reflecting the different demands and volumes across passenger cars, commercial vehicles, and the rapidly expanding electric vehicle sector. Each segment plays a crucial role in shaping the overall market landscape and future growth trajectories.

- By Type: Advanced High-Strength Steel (AHSS), Carbon Steel, Alloy Steel, Stainless Steel, Tool Steel

- By Application: Body-in-White, Powertrain, Chassis, Suspension, Electricals, Others

- By Vehicle Type: Passenger Cars, Commercial Vehicles, Electric Vehicles (EVs)

Regional Highlights

- Asia Pacific: Dominates the market due to high vehicle production volumes, rapid industrialization, and significant growth in countries like China, India, and Japan. The region is a major hub for both traditional and electric vehicle manufacturing.

- Europe: Characterized by stringent emission regulations and a strong emphasis on lightweighting and advanced safety features, driving the adoption of AHSS. Germany, France, and Italy are key contributors with robust automotive industries.

- North America: Exhibits strong demand for automotive steel, particularly for light trucks and SUVs. The region is actively investing in EV production and advanced manufacturing techniques.

- Latin America: Expected to show steady growth driven by increasing vehicle sales and expanding manufacturing capabilities, especially in Brazil and Mexico.

- Middle East and Africa (MEA): Emerging as a potential growth region with rising disposable incomes and developing automotive manufacturing bases, though currently a smaller market share.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Steel Market.- ArcelorMittal

- POSCO

- Nippon Steel Corporation

- China Baowu Steel Group

- JFE Holdings

- Tata Steel

- Hyundai Steel

- ThyssenKrupp AG

- HBIS Group

- Nucor Corporation

- United States Steel Corporation

- Shougang Group

- Gerdau S.A.

- SSAB AB

- Novolipetsk Steel (NLMK)

- Severstal

- Angang Group

- EVRAZ

- JSW Steel

- Baosteel Group

Frequently Asked Questions

What is the projected growth rate for the Automotive Steel Market?

The Automotive Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033, driven by advancements in vehicle technologies and global production.

What are the primary drivers of the Automotive Steel Market?

Key drivers include the increasing demand for lightweight and fuel-efficient vehicles, stringent emission and safety regulations, and the expanding global automotive production, especially in the Electric Vehicle (EV) segment.

How is AI impacting the Automotive Steel industry?

AI is significantly impacting the industry by optimizing production processes, enabling AI-assisted material design for new steel grades, improving quality control, and enhancing supply chain efficiency through predictive analytics.

Which steel types are gaining prominence in the automotive sector?

Advanced High-Strength Steels (AHSS) and Ultra High-Strength Steels (UHSS) are increasingly prominent due to their superior strength-to-weight ratio, crucial for lightweighting and enhanced vehicle safety.

What role does sustainability play in the Automotive Steel Market?

Sustainability is a critical factor, driving demand for greener steel production methods, increased use of recycled content, and the development of materials that contribute to the circular economy within the automotive industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted