Automotive Semiconductor for Parking Assist Market

Automotive Semiconductor for Parking Assist Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708204 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Semiconductor for Parking Assist Market Size

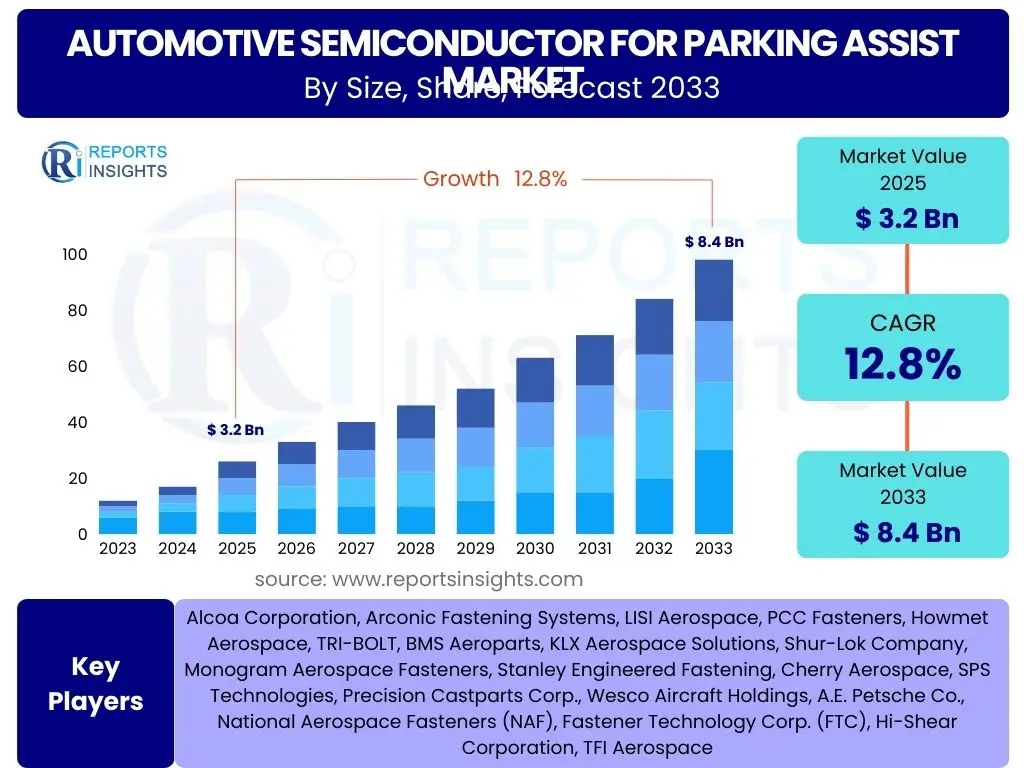

According to Reports Insights Consulting Pvt Ltd, The Automotive Semiconductor for Parking Assist Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 8.4 Billion by the end of the forecast period in 2033.

Key Automotive Semiconductor for Parking Assist Market Trends & Insights

Market inquiries frequently highlight the rapid evolution of Advanced Driver-Assistance Systems (ADAS) and the increasing complexity of vehicle electronics as pivotal trends. Users are particularly interested in how these advancements are translating into more sophisticated and autonomous parking features, alongside the underlying semiconductor technologies enabling such capabilities. The shift towards electrification and smart cities is also a recurring theme, driving demand for innovative, low-power, and high-performance semiconductor solutions tailored for seamless vehicle integration and enhanced safety.

Furthermore, there is significant interest in the convergence of various sensor modalities, such as ultrasonic, radar, and camera systems, into integrated parking assist solutions. This integration necessitates robust semiconductor components capable of processing large volumes of data in real-time to provide accurate environmental perception. Users are keen to understand the impact of miniaturization and increased computational power on the development of more compact and efficient parking assist modules, directly influencing vehicle design and consumer experience. The continuous push for enhanced safety standards and driver convenience remains a dominant driver, shaping innovation in this semiconductor segment.

- Integration of advanced sensor fusion for enhanced environmental perception.

- Rising adoption of fully autonomous parking systems.

- Miniaturization and higher integration density of semiconductor components.

- Growing demand for high-performance processors for real-time data analysis.

- Emphasis on cybersecurity features within parking assist semiconductor architectures.

AI Impact Analysis on Automotive Semiconductor for Parking Assist

Common user questions regarding AI's impact on automotive semiconductors for parking assist systems predominantly revolve around the enhancement of decision-making capabilities, object recognition accuracy, and the enablement of predictive parking functionalities. Users seek to understand how AI algorithms, particularly machine learning and deep learning, are being leveraged to interpret complex sensor data more effectively, leading to more reliable and intuitive parking experiences. There is also considerable interest in AI's role in personalizing parking assistance based on driver behavior and environmental conditions, moving beyond rule-based systems.

Moreover, the discussion often touches upon the need for specialized AI accelerators and neural processing units (NPUs) within automotive semiconductors to handle the intensive computational demands of AI models at the edge. Users are concerned with the efficiency, power consumption, and real-time performance of these AI-enabled chips, recognizing their critical role in the safety and responsiveness of parking assist systems. The potential for AI to facilitate vehicle-to-infrastructure (V2I) communication for smarter parking solutions and its contribution to the overall autonomous driving roadmap are also key areas of inquiry.

- Enhanced object detection and classification through machine learning algorithms.

- Enabling predictive parking path generation and obstacle avoidance.

- Facilitating sensor fusion by intelligently processing data from multiple sources.

- Optimization of parking maneuvers based on real-time environmental data.

- Development of dedicated AI accelerators within parking assist semiconductor units.

Key Takeaways Automotive Semiconductor for Parking Assist Market Size & Forecast

User inquiries concerning key takeaways from the Automotive Semiconductor for Parking Assist market size and forecast consistently point towards the robust growth trajectory driven by technological innovation and regulatory pressures. A primary insight is the significant role of ADAS proliferation, which mandates increasingly sophisticated semiconductor solutions for features like automatic parking, parking assist, and surround view. The market's expansion is not merely linear but is characterized by a rapid integration of advanced processing capabilities, signaling a clear shift towards more intelligent and autonomous vehicle functions.

Another crucial takeaway frequently emphasized is the burgeoning opportunity within emerging markets and the continued investment in research and development by industry players to meet evolving consumer expectations for safety and convenience. The forecast underscores the essential nature of high-performance, low-power semiconductors in enabling the next generation of parking assist systems, which are integral to the broader vision of connected and autonomous vehicles. The sustained demand across various vehicle segments, from passenger cars to commercial vehicles, further solidifies the market's promising outlook.

- The market exhibits substantial growth, driven by ADAS integration and autonomous driving trends.

- Technological advancements in sensor fusion and AI are critical for market expansion.

- Rising safety regulations and consumer demand for convenience are key accelerators.

- Significant investment in semiconductor R&D is crucial for future innovation.

- Asia Pacific is poised for high growth due to increased automotive production and technology adoption.

Automotive Semiconductor for Parking Assist Market Drivers Analysis

The market for automotive semiconductors in parking assist systems is primarily propelled by the escalating adoption of Advanced Driver-Assistance Systems (ADAS) in modern vehicles. As ADAS features become standard across various vehicle segments, the demand for robust and efficient semiconductor components that power ultrasonic sensors, cameras, radar, and associated electronic control units (ECUs) experiences a parallel surge. These semiconductors are foundational to features such as automatic parking, parking assist, and surround-view systems, directly contributing to enhanced vehicle safety and driver convenience. The continuous innovation in sensor technology, including miniaturization and improved accuracy, further fuels this demand.

Moreover, stringent global safety regulations, particularly in regions like Europe and North America, mandate the inclusion of advanced safety features in new vehicles, with parking assist systems frequently falling under these directives. This regulatory push compels automotive manufacturers to integrate sophisticated parking solutions, thereby increasing the consumption of specialized semiconductors. Concurrently, evolving consumer expectations for high-tech features and convenience in their vehicles drive the market. Drivers increasingly value automated parking capabilities, which simplify maneuvering in tight spaces and reduce the risk of collisions, directly influencing OEM decisions to incorporate these technologies, thereby boosting semiconductor demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of Advanced Driver-Assistance Systems (ADAS) | +3.5% | Global | Short to Mid-term (2025-2029) |

| Stringent global automotive safety regulations and mandates | +2.8% | Europe, North America, China | Mid-term (2027-2031) |

| Growing consumer demand for enhanced convenience and safety features | +2.3% | Global, particularly developed markets | Short to Mid-term (2025-2029) |

| Advancements in sensor technologies (ultrasonic, radar, camera) and sensor fusion | +2.0% | Global | Mid to Long-term (2028-2033) |

| Rising electrification and increasing complexity of in-vehicle electronics | +2.2% | Global | Mid to Long-term (2028-2033) |

Automotive Semiconductor for Parking Assist Market Restraints Analysis

The Automotive Semiconductor for Parking Assist Market faces several significant restraints that could impede its growth trajectory. One primary challenge is the high cost associated with integrating advanced semiconductor components and complex parking assist systems into vehicles. These sophisticated systems, incorporating multiple sensors, high-performance processors, and intricate software, can substantially increase the overall vehicle cost, potentially deterring price-sensitive consumers and manufacturers in emerging markets. The added expense often conflicts with the broader goal of making advanced safety features accessible across all vehicle segments, particularly in budget-conscious categories.

Furthermore, the automotive industry's susceptibility to global supply chain disruptions poses a considerable restraint. Semiconductor manufacturing is a highly complex process, reliant on a global network of specialized suppliers for raw materials, fabrication, and assembly. Geopolitical tensions, natural disasters, and unforeseen events can cause bottlenecks in the supply chain, leading to component shortages and production delays for parking assist systems. This volatility not only impacts manufacturing schedules but also inflates component costs, placing pressure on profit margins for both semiconductor suppliers and automotive OEMs. Moreover, the inherent complexity of integrating various hardware and software components from different vendors into a cohesive and reliable parking assist system presents significant engineering challenges, requiring extensive testing and validation, which adds to development costs and timelines.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost of advanced parking assist systems and components | -1.8% | Developing economies, Mass-market vehicle segments | Short to Mid-term (2025-2030) |

| Global supply chain volatility and semiconductor shortages | -2.5% | Global | Short-term (2025-2027) |

| Complexity of integrating diverse sensor technologies and software algorithms | -1.5% | Global | Mid-term (2027-2032) |

| Data privacy and cybersecurity concerns with connected vehicles | -1.0% | Europe (GDPR), North America | Long-term (2030-2033) |

| Lack of standardized protocols for communication and interoperability | -0.8% | Global | Mid to Long-term (2028-2033) |

Automotive Semiconductor for Parking Assist Market Opportunities Analysis

The Automotive Semiconductor for Parking Assist Market is ripe with significant opportunities, largely driven by the ongoing technological evolution towards fully autonomous vehicles. The development of advanced autonomous parking features, which require increasingly sophisticated sensor arrays and high-performance computing units, presents a substantial growth avenue for semiconductor manufacturers. As vehicles move beyond basic parking assist to fully automated parking systems capable of locating spots and maneuvering independently, the demand for specialized processors, memory solutions, and power management ICs will surge. This shift necessitates higher levels of integration and more robust processing capabilities to handle complex algorithms for environmental perception and path planning.

Moreover, the expansion into emerging automotive markets, particularly in Asia Pacific and Latin America, represents a fertile ground for market penetration. As these regions experience rapid urbanization and increased vehicle ownership, there is a growing demand for safety and convenience features, including parking assist systems, which were once considered premium. Semiconductor suppliers can capitalize on this trend by developing cost-effective yet high-performance solutions tailored to the specific needs and regulatory frameworks of these markets. Furthermore, the increasing connectivity of vehicles and the rise of vehicle-to-everything (V2X) communication open doors for integrated parking solutions that leverage external data, such as smart city infrastructure, to enhance parking efficiency and convenience. This includes innovative services like automated valet parking and predictive parking slot availability, driving demand for communication-centric semiconductor components and robust processing power for real-time data exchange.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and commercialization of autonomous parking systems | +3.0% | Global, particularly developed automotive markets | Mid to Long-term (2028-2033) |

| Expansion into untapped and emerging automotive markets (e.g., APAC, Latin America) | +2.5% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Integration with Vehicle-to-Everything (V2X) communication for smart parking solutions | +2.0% | Europe, North America, Japan, China | Long-term (2030-2033) |

| Advancements in solid-state LiDAR and next-generation radar technologies | +1.8% | Global | Mid to Long-term (2029-2033) |

| Strategic partnerships and collaborations for end-to-end parking solutions | +1.5% | Global | Short to Mid-term (2025-2029) |

Automotive Semiconductor for Parking Assist Market Challenges Impact Analysis

The Automotive Semiconductor for Parking Assist Market faces significant challenges, particularly concerning the establishment of industry-wide standards and regulatory frameworks. The absence of universal protocols for data communication, sensor fusion, and system interoperability among different manufacturers and technology providers creates fragmentation. This makes it difficult to achieve seamless integration of components from various suppliers and can impede the scalability and cost-effectiveness of parking assist solutions. Developing and adhering to common standards is critical for fostering innovation and ensuring broad market adoption, yet this remains a complex, ongoing process requiring consensus among diverse stakeholders globally.

Another substantial challenge is addressing data privacy and cybersecurity concerns within highly connected parking assist systems. As these systems collect and process extensive environmental data and potentially driver behavior information, ensuring the secure handling and protection of this sensitive data becomes paramount. The risk of cyber threats, including unauthorized access or malicious interference, could compromise vehicle safety and erode consumer trust. Consequently, manufacturers and semiconductor providers must invest heavily in robust cybersecurity measures and adhere to evolving data protection regulations like GDPR. Furthermore, the development of highly reliable and redundant systems is crucial, as any failure in a parking assist system could have significant safety implications, demanding stringent testing and validation processes that add to development complexity and cost. Gaining widespread consumer trust and acceptance for increasingly autonomous parking features also presents a challenge, requiring effective education and demonstration of system reliability and safety.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of standardized interfaces and communication protocols | -1.2% | Global | Mid-term (2027-2032) |

| Ensuring cybersecurity and data privacy in connected parking systems | -1.5% | Global, particularly Europe and North America | Mid to Long-term (2028-2033) |

| High reliability requirements and extensive validation testing | -0.9% | Global | Short to Mid-term (2025-2030) |

| Managing complex software development and integration efforts | -1.0% | Global | Mid-term (2027-2032) |

| Overcoming consumer skepticism and ensuring public acceptance of autonomous features | -0.7% | Global | Long-term (2030-2033) |

Automotive Semiconductor for Parking Assist Market - Updated Report Scope

This comprehensive market insights report provides an in-depth analysis of the Automotive Semiconductor for Parking Assist Market, covering its current landscape, future projections, and the underlying dynamics shaping its evolution. The scope encompasses a detailed examination of market size and growth forecasts, driven by a thorough assessment of key trends, drivers, restraints, opportunities, and challenges. It further delves into the impact of Artificial Intelligence (AI) on the market, offering a forward-looking perspective on technological advancements. The report presents a segmented analysis across various components, vehicle types, applications, and parking types, alongside a comprehensive regional breakdown to highlight specific market dynamics and growth pockets. Additionally, it features profiles of leading industry stakeholders, offering insights into the competitive landscape and strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 8.4 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NXP Semiconductors, Infineon Technologies AG, Renesas Electronics Corporation, STMicroelectronics N.V., Texas Instruments Incorporated, Analog Devices Inc., Qualcomm Technologies Inc., Intel Corporation, ON Semiconductor Corporation, Microchip Technology Inc., Rohm Semiconductor, Cypress Semiconductor (now Infineon), Magna International Inc., Valeo S.A., ZF Friedrichshafen AG, Continental AG, Robert Bosch GmbH, NVIDIA Corporation, Mobileye (an Intel Company), Mitsubishi Electric Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Semiconductor for Parking Assist Market is segmented to provide a granular view of its various facets, enabling a detailed understanding of market dynamics across different product categories, vehicle types, and technological applications. This segmentation is crucial for identifying specific growth areas, understanding competitive landscapes within niches, and tailoring product development strategies. The market is primarily analyzed based on the types of semiconductor components utilized, the categories of vehicles integrating these systems, the specific applications of parking assistance, and the diverse parking maneuvers these systems facilitate.

Each segment contributes uniquely to the overall market trajectory, with certain components or applications experiencing higher growth due to technological advancements or increased adoption rates. For instance, high-performance MCUs and advanced sensors are pivotal for enabling sophisticated parking features in premium vehicles, while cost-effective solutions might target mass-market passenger cars. Understanding these segment-specific trends is essential for both established players and new entrants to effectively position their offerings and capitalize on emerging opportunities across the diverse automotive ecosystem.

- By Component: Includes Microcontroller Units (MCUs), Memory Integrated Circuits (ICs), various Sensors (Ultrasonic, Radar, Camera, LiDAR), Power Management ICs (PMICs), Analog ICs, Interface ICs, and other specialized ICs.

- By Vehicle Type: Differentiated into Passenger Cars and Commercial Vehicles, reflecting varying integration levels and requirements.

- By Application: Covers Parking Assist System (PAS), Automatic Parking Assist (APA), Remote Parking Assist (RPA), and other emerging parking solutions.

- By Parking Type: Categorized by the specific maneuver assisted, such as Parallel Parking, Perpendicular Parking, and Diagonal Parking.

Regional Highlights

- North America: Characterized by early adoption of ADAS technologies and stringent safety regulations, driving demand for advanced parking assist semiconductors. High consumer disposable income also supports the integration of premium features.

- Europe: A leading region due to strict automotive safety standards and a strong focus on autonomous driving development. High R&D investments and the presence of major automotive OEMs contribute significantly to market growth.

- Asia Pacific (APAC): Expected to exhibit the highest growth due to burgeoning automotive production, increasing vehicle sales, and a rapidly expanding middle class demanding enhanced safety and convenience features in countries like China, India, Japan, and South Korea. Government initiatives promoting smart cities and advanced vehicle technologies also play a crucial role.

- Latin America: Demonstrating steady growth as vehicle penetration increases and consumers show greater interest in modern safety features, albeit with a focus on more cost-effective solutions compared to developed markets.

- Middle East and Africa (MEA): An emerging market with growing automotive sales and increasing investments in smart infrastructure. Adoption of parking assist systems is gradual but promising, driven by urbanization and rising safety awareness.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Semiconductor for Parking Assist Market.- NXP Semiconductors

- Infineon Technologies AG

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Qualcomm Technologies Inc.

- Intel Corporation

- ON Semiconductor Corporation

- Microchip Technology Inc.

- Rohm Semiconductor

- Cypress Semiconductor (now Infineon)

- Magna International Inc.

- Valeo S.A.

- ZF Friedrichshafen AG

- Continental AG

- Robert Bosch GmbH

- NVIDIA Corporation

- Mobileye (an Intel Company)

- Mitsubishi Electric Corporation

Frequently Asked Questions

What is the projected growth rate of the Automotive Semiconductor for Parking Assist Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033, reaching USD 8.4 Billion by 2033.

What are the primary drivers for this market's expansion?

Key drivers include the increasing adoption of Advanced Driver-Assistance Systems (ADAS), stringent global safety regulations, and growing consumer demand for advanced convenience and safety features in vehicles.

How is AI influencing the Automotive Semiconductor for Parking Assist market?

AI is significantly impacting the market by enabling enhanced object detection, predictive parking, intelligent sensor fusion, and the development of dedicated AI accelerators within semiconductor units for more autonomous and intelligent parking solutions.

Which regions are expected to show significant growth?

The Asia Pacific (APAC) region is expected to exhibit the highest growth due to increased automotive production, rising vehicle sales, and governmental initiatives promoting advanced vehicle technologies.

What are the key challenges facing the market?

Major challenges include the lack of standardized interfaces, ensuring robust cybersecurity and data privacy in connected systems, the high cost of advanced components, and the complexity of integrating diverse technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted