Automotive MLCC Market

Automotive MLCC Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701571 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive MLCC Market Size

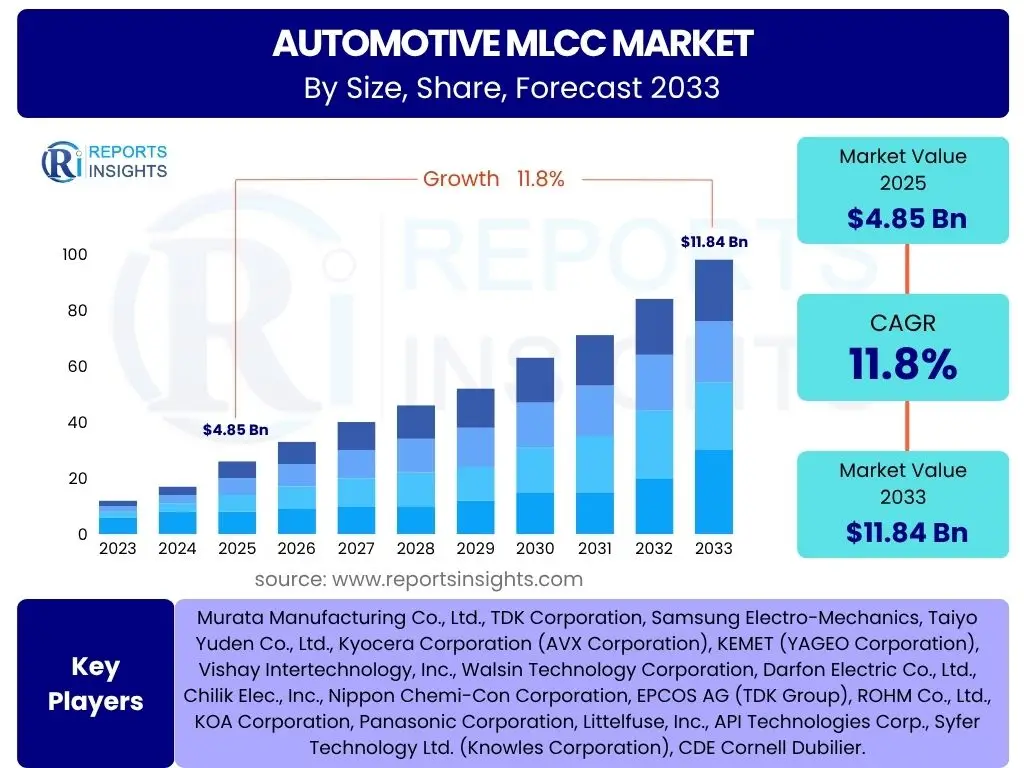

According to Reports Insights Consulting Pvt Ltd, The Automotive MLCC Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 4.85 Billion in 2025 and is projected to reach USD 11.84 Billion by the end of the forecast period in 2033.

Key Automotive MLCC Market Trends & Insights

The Automotive MLCC (Multilayer Ceramic Capacitor) market is currently undergoing significant transformation driven by the escalating demand for advanced electronic systems in modern vehicles. Key user inquiries often revolve around the impact of vehicle electrification, the proliferation of Advanced Driver-Assistance Systems (ADAS), and the continuous push for miniaturization and higher performance components. The industry is witnessing a strong shift towards high-capacitance MLCCs to support the power demands of electric vehicle (EV) powertrains and sophisticated infotainment systems.

Furthermore, the trend towards autonomous driving capabilities necessitates an increasing number of MLCCs capable of operating reliably under harsh automotive conditions, including extreme temperatures and vibrations. This drives innovation in material science and manufacturing processes to enhance durability and performance. Supply chain resilience, particularly post-pandemic, remains a critical concern, leading to strategic investments in regional manufacturing and diversification of raw material sources to ensure stable supply for automotive OEMs and Tier 1 suppliers.

Another emerging trend is the integration of passive components with active ones, striving for greater functional density and reduced overall system size. This contributes to the complexity of MLCC design and manufacturing, pushing manufacturers to invest in advanced simulation and testing capabilities. The convergence of these trends underscores a dynamic market landscape focused on high reliability, performance, and efficiency, directly responding to the evolving demands of the global automotive industry.

- Escalating demand from Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) for high-voltage and high-capacitance MLCCs.

- Proliferation of Advanced Driver-Assistance Systems (ADAS) and autonomous driving features requiring a significant increase in MLCC count per vehicle.

- Miniaturization and higher power density requirements driven by space constraints and performance demands in modern automotive electronics.

- Development of high-temperature tolerant and high-reliability MLCCs for demanding under-hood applications.

- Focus on supply chain resilience and regional manufacturing to mitigate geopolitical and logistical risks.

AI Impact Analysis on Automotive MLCC

User inquiries frequently explore how Artificial Intelligence (AI) and Machine Learning (ML) are influencing the Automotive MLCC market, particularly regarding manufacturing efficiency, quality control, and component design. AI is increasingly being leveraged in the production phase to optimize processes, predict equipment failures, and enhance throughput. Predictive maintenance, powered by AI algorithms analyzing sensor data from manufacturing lines, minimizes downtime and ensures consistent quality, which is paramount for safety-critical automotive components.

In terms of quality control, AI-driven visual inspection systems are becoming indispensable, detecting microscopic flaws at speeds and accuracies unattainable by human operators. This leads to superior product reliability and reduced waste, directly impacting the cost-effectiveness and reputation of MLCC manufacturers. Furthermore, AI is beginning to play a role in the design phase, enabling more rapid prototyping and simulation of new MLCC configurations, optimizing material use and performance characteristics for specific automotive applications.

Looking ahead, AI's influence is expected to expand into demand forecasting and supply chain optimization, allowing manufacturers to respond more agilely to market fluctuations and potential disruptions. The ability of AI to process vast datasets can provide deeper insights into market trends and customer needs, enabling MLCC producers to innovate more strategically. This pervasive integration of AI across the value chain is set to enhance productivity, improve product quality, and accelerate the development cycle within the Automotive MLCC sector.

- Enhanced manufacturing efficiency and yield optimization through AI-driven process control and predictive analytics.

- Superior quality inspection and defect detection using AI-powered computer vision systems, ensuring high reliability for automotive applications.

- Accelerated design and simulation of new MLCC architectures and materials, optimizing performance and reducing development cycles.

- Improved supply chain management and demand forecasting through advanced AI algorithms for better inventory control and responsiveness.

- Development of smart MLCCs with embedded intelligence for self-monitoring or enhanced fault detection in critical automotive systems.

Key Takeaways Automotive MLCC Market Size & Forecast

Common questions concerning key takeaways from the Automotive MLCC market size and forecast highlight the industry's rapid expansion, primarily propelled by the global electrification of vehicles and the increasing sophistication of in-car electronics. A significant takeaway is the substantial projected growth rate, indicating robust demand driven by both volume increases in vehicle production and a higher per-vehicle content of electronic components. The shift from traditional internal combustion engine (ICE) vehicles to Electric Vehicles (EVs) is a cornerstone of this growth, as EVs require a significantly higher number of MLCCs, particularly high-capacitance and high-voltage variants, for their power management, charging, and motor control systems.

Another crucial insight is the imperative for MLCC manufacturers to scale production capabilities while simultaneously focusing on technological innovation. The forecast underscores the need for continuous research and development into new materials and designs that can withstand the increasingly harsh operating conditions within modern automobiles, such as higher temperatures and vibration. Furthermore, the market's trajectory emphasizes the growing importance of regional supply chain diversification, as geopolitical stability and trade policies significantly impact component availability and pricing. This highlights a strategic pivot towards localized manufacturing and strong supplier relationships to ensure resilience.

Ultimately, the market size and forecast data reveal a dynamic landscape where adaptability and innovation are key to success. The consistent demand for smaller, more reliable, and higher-performing MLCCs across various automotive applications ensures sustained growth, but also presents challenges related to manufacturing scalability, raw material access, and technological advancements. Companies that can effectively navigate these complexities while maintaining high quality and cost-efficiency are poised to capitalize on the substantial opportunities presented by the evolving automotive sector.

- Significant growth primarily driven by the escalating adoption of electric vehicles (EVs) and hybrid vehicles (HVs).

- Increasing electronic content per vehicle, including ADAS, infotainment, and connectivity features, boosts MLCC demand.

- The market is shifting towards high-capacitance and high-voltage MLCCs to support advanced power management systems in EVs.

- Technological advancements in miniaturization and enhanced reliability are critical for future market competitiveness.

- Supply chain robustness and diversification are crucial factors influencing market stability and growth trajectory.

Automotive MLCC Market Drivers Analysis

The Automotive MLCC market is propelled by a confluence of powerful drivers stemming from the ongoing transformation of the global automotive industry. Foremost among these is the accelerating transition towards electric vehicles (EVs) and hybrid electric vehicles (HEVs). These vehicles rely heavily on advanced power electronics, including inverters, converters, and battery management systems, all of which require a large number of high-capacitance and high-voltage MLCCs for filtering, energy storage, and noise suppression. This electrification trend significantly increases the MLCC content per vehicle compared to traditional internal combustion engine (ICE) vehicles.

Another major driver is the widespread adoption and continuous evolution of Advanced Driver-Assistance Systems (ADAS). Features such as adaptive cruise control, lane-keeping assist, automatic emergency braking, and parking assist systems demand vast amounts of data processing and real-time decision-making, necessitating robust and numerous electronic control units (ECUs). Each ECU, along with its array of sensors and communication modules, utilizes hundreds of MLCCs to ensure stable power delivery, signal integrity, and electromagnetic compatibility (EMC), thereby fueling the demand for these components.

Furthermore, the increasing integration of infotainment, connectivity, and telematics systems in modern vehicles contributes substantially to MLCC market growth. Consumers expect seamless connectivity, high-definition displays, and sophisticated in-car entertainment, all of which require complex electronic circuits. The drive for vehicle lightweighting and space optimization also pushes for smaller, more efficient electronic components, making miniaturized MLCCs a preferred choice. These combined factors create a sustained and escalating demand, underpinning the positive growth trajectory of the Automotive MLCC market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Adoption of Electric Vehicles (EVs) and HEVs | +4.5% | Asia Pacific (China, Japan, South Korea), Europe (Germany, Norway), North America (USA) | 2025-2033 |

| Proliferation of Advanced Driver-Assistance Systems (ADAS) | +3.2% | North America, Europe, Asia Pacific (Japan, South Korea, China) | 2025-2033 |

| Increasing Electronic Content Per Vehicle (Infotainment, Telematics) | +2.8% | Global | 2025-2033 |

| Miniaturization and Space Optimization in Vehicle Design | +1.3% | Global | 2025-2033 |

| Development of Autonomous Driving Technologies | +1.0% | North America, Europe, Asia Pacific (China) | 2028-2033 |

Automotive MLCC Market Restraints Analysis

Despite the strong growth drivers, the Automotive MLCC market faces several significant restraints that could impede its expansion. One primary concern is the volatility of raw material prices, particularly for critical metals like palladium, nickel, and copper, as well as ceramic materials like barium titanate. Fluctuations in these commodity prices directly impact manufacturing costs, which can then be passed on to automotive OEMs, potentially slowing down the adoption of new electronic systems if costs become prohibitive. This price instability makes long-term planning and stable pricing strategies challenging for MLCC manufacturers.

Another substantial restraint is the susceptibility to supply chain disruptions. The global MLCC market has historically experienced periods of tight supply, exacerbated by factors such as natural disasters, geopolitical tensions, and global pandemics. The COVID-19 pandemic, for instance, highlighted the fragility of global supply chains, leading to widespread component shortages that significantly impacted automotive production worldwide. A highly concentrated manufacturing base in specific regions further amplifies this risk, making the market vulnerable to localized disruptions that have ripple effects globally.

Furthermore, the automotive industry's stringent quality and reliability standards pose a continuous challenge. MLCCs used in automotive applications must withstand extreme temperatures, vibrations, and harsh environmental conditions over extended periods, often ten years or more. Meeting these rigorous requirements necessitates highly precise manufacturing processes and extensive testing, leading to higher production costs and longer qualification cycles. The constant pressure for cost reduction from automotive OEMs, coupled with these demanding quality specifications, creates a difficult balancing act for MLCC suppliers, potentially limiting profit margins and discouraging investment in certain segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (e.g., Palladium, Nickel) | -1.5% | Global | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Tensions | -1.2% | Global (esp. Asia Pacific, Europe) | 2025-2030 |

| Strict Automotive Quality and Reliability Standards | -0.8% | Global | 2025-2033 |

| Intense Competition and Pricing Pressures | -0.7% | Global | 2025-2033 |

| Technological Obsolescence and Rapid Innovation Cycle | -0.5% | Global | 2028-2033 |

Automotive MLCC Market Opportunities Analysis

The Automotive MLCC market is ripe with opportunities, primarily driven by the ongoing electrification and digitalization of vehicles. The increasing adoption of electric and hybrid vehicles presents a significant opportunity for manufacturers of high-capacitance and high-voltage MLCCs. As battery technology advances and charging infrastructure expands, the demand for power electronics in EVs will continue to surge, requiring a greater number of specialized MLCCs capable of handling high currents and voltages efficiently. This segment offers premium pricing opportunities due to the stringent performance and reliability requirements.

Another substantial opportunity lies in the continuous advancement of Advanced Driver-Assistance Systems (ADAS) and the progression towards higher levels of autonomous driving. Each new ADAS feature, from Lidar and Radar systems to high-resolution cameras and advanced computing platforms, necessitates a dense array of high-performance MLCCs to ensure signal integrity and power stability. The development of next-generation sensor fusion and AI processing units for autonomous vehicles will further escalate the demand for sophisticated and reliable MLCCs, creating a long-term growth avenue for manufacturers capable of meeting these evolving technological needs.

Furthermore, emerging markets, particularly in Asia Pacific and Latin America, present untapped potential as vehicle ownership increases and consumers demand more technologically advanced cars. As these regions experience economic growth and urbanization, the adoption of modern automotive technologies, including EVs and ADAS, is expected to accelerate. This provides an opportunity for MLCC manufacturers to expand their geographical footprint and establish strong supply partnerships in these burgeoning markets. Additionally, strategic collaborations and mergers & acquisitions can enable companies to consolidate market share, gain access to new technologies, and enhance their production capabilities, positioning themselves for sustained growth in this dynamic sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Capacitance/Voltage MLCCs in EVs | +3.5% | Global, particularly Asia Pacific, Europe, North America | 2025-2033 |

| Development of Advanced ADAS and Autonomous Driving Levels | +2.8% | North America, Europe, Asia Pacific (China, Japan) | 2026-2033 |

| Expansion in Emerging Automotive Markets (e.g., India, Southeast Asia) | +1.8% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Miniaturization and High-Density Packaging Solutions | +1.0% | Global | 2025-2030 |

| Strategic Partnerships and Collaborations for R&D | +0.8% | Global | 2025-2033 |

Automotive MLCC Market Challenges Impact Analysis

The Automotive MLCC market, while experiencing robust growth, faces several intricate challenges that demand strategic navigation. One prominent challenge is the intense competition among a relatively small number of large global players. This competitive landscape often leads to price wars and downward pressure on margins, compelling manufacturers to continually optimize production costs and innovate. Maintaining a competitive edge requires significant investment in research and development, as well as in advanced manufacturing technologies to improve efficiency and yield, which can be particularly demanding for smaller or emerging players.

Another significant hurdle is the rapid pace of technological change within the automotive industry. As vehicles become increasingly software-defined and integrated with new functionalities like 5G connectivity and advanced computing, the requirements for MLCCs are constantly evolving. This necessitates continuous innovation in terms of capacitance, voltage rating, size, and reliability. Manufacturers must not only keep pace with these changes but also anticipate future demands, which requires substantial R&D expenditure and agility in product development cycles to avoid technological obsolescence.

Furthermore, ensuring a stable and ethical supply of critical raw materials remains a persistent challenge. The reliance on specific minerals and compounds, often sourced from geopolitically sensitive regions, exposes the supply chain to risks of disruption and price volatility. Ethical sourcing and environmental regulations are also becoming increasingly scrutinized, adding complexity to the procurement process. Companies must invest in robust supply chain management systems and explore diversification strategies to mitigate these risks, ensuring uninterrupted production and adherence to global sustainability standards. Navigating these challenges effectively will be crucial for sustained success in the highly dynamic Automotive MLCC market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure | -1.1% | Global | 2025-2033 |

| Rapid Technological Advancements in Automotive Electronics | -0.9% | Global | 2025-2033 |

| Ensuring Consistent and Ethical Raw Material Supply | -0.7% | Global | 2025-2033 |

| High Capital Expenditure for Manufacturing Capacity Expansion | -0.6% | Global | 2025-2030 |

| Counterfeit Products and Intellectual Property Infringement | -0.4% | Global, particularly emerging markets | 2025-2033 |

Automotive MLCC Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Automotive MLCC market, encompassing historical data, current market dynamics, and future projections. It delivers crucial insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry landscape. The report also includes a detailed segmentation analysis, regional insights, and profiles of key market players, offering a holistic view for strategic decision-making in the rapidly evolving automotive electronics sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.85 Billion |

| Market Forecast in 2033 | USD 11.84 Billion |

| Growth Rate | 11.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Murata Manufacturing Co., Ltd., TDK Corporation, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd., Kyocera Corporation (AVX Corporation), KEMET (YAGEO Corporation), Vishay Intertechnology, Inc., Walsin Technology Corporation, Darfon Electric Co., Ltd., Chilik Elec., Inc., Nippon Chemi-Con Corporation, EPCOS AG (TDK Group), ROHM Co., Ltd., KOA Corporation, Panasonic Corporation, Littelfuse, Inc., API Technologies Corp., Syfer Technology Ltd. (Knowles Corporation), CDE Cornell Dubilier. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive MLCC market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation is crucial for stakeholders to identify niche opportunities, tailor product development, and refine market strategies. The primary segmentation categories include type, capacitance, application, and vehicle type, each offering unique insights into the demand patterns and technological requirements across the automotive industry.

By dissecting the market through these segments, it becomes evident that the demand for High Capacitance MLCCs and Automotive Grade MLCCs is particularly robust, driven by the escalating power demands of electric vehicles and sophisticated ADAS systems. Similarly, applications such as Powertrain and Safety Systems are significant consumers of MLCCs, given their critical role in vehicle performance and occupant safety. The vehicle type segmentation clearly illustrates the disproportionately higher MLCC content in Electric Vehicles compared to traditional internal combustion engine cars, signaling a major shift in component demand.

This multi-faceted segmentation analysis not only highlights the dominant market areas but also reveals emerging segments with high growth potential, such as those catering to advanced infotainment and connectivity solutions. Understanding these segment dynamics is paramount for manufacturers to allocate resources effectively, optimize their product portfolios, and strategically position themselves to capitalize on the evolving needs of the global automotive sector.

- By Type

- General Purpose MLCCs

- Mid Voltage MLCCs

- High Voltage MLCCs

- High Capacitance MLCCs

- Automotive Grade MLCCs

- By Capacitance

- Under 100 nF

- 100 nF to 1 µF

- 1 µF to 10 µF

- Above 10 µF

- By Application

- Powertrain Systems

- Safety Systems

- Infotainment & Telematics Systems

- Body & Comfort Electronics

- Chassis Electronics

- By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles (BEV, PHEV, HEV)

Regional Highlights

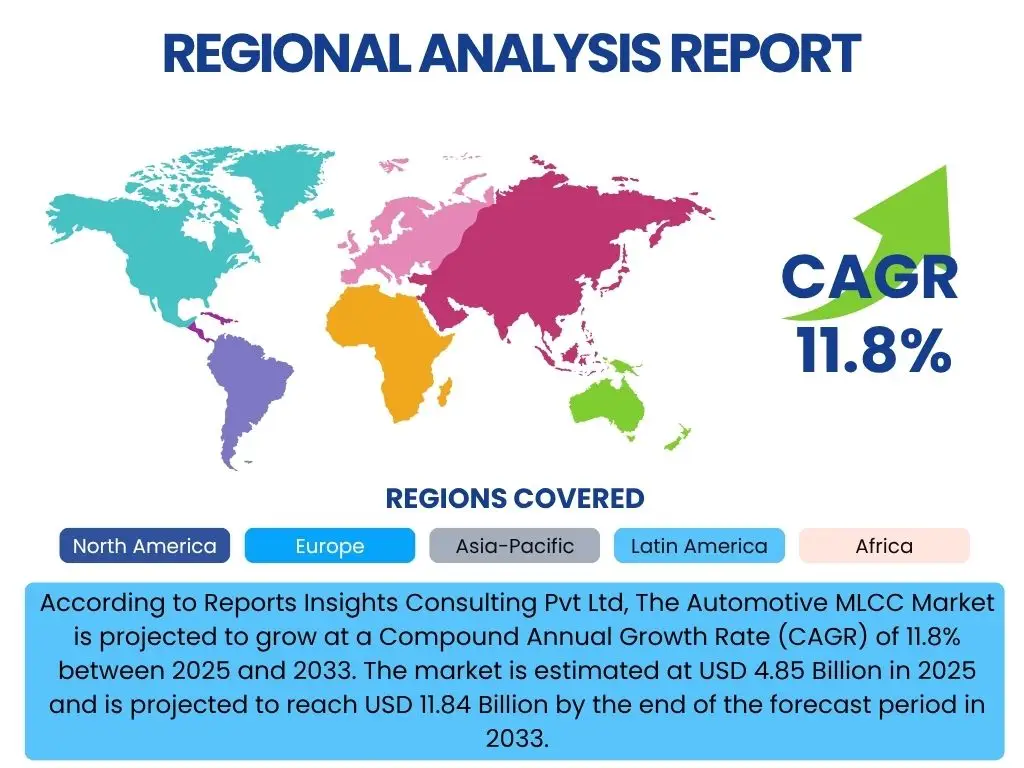

- Asia Pacific (APAC): Dominates the Automotive MLCC market, primarily driven by the region's robust automotive manufacturing base, leading position in EV production (especially China), and significant presence of major MLCC manufacturers. Countries like China, Japan, and South Korea are key contributors to both demand and supply, benefiting from government initiatives supporting EV adoption and technological advancements in automotive electronics. The rapid expansion of ADAS and infotainment systems in new vehicles across the region further fuels demand.

- Europe: Represents a substantial market for Automotive MLCCs, characterized by stringent emission regulations driving EV adoption and strong R&D in autonomous driving technologies. Countries such as Germany, France, and the UK are at the forefront of automotive innovation, creating high demand for high-reliability and high-performance MLCCs for advanced vehicle systems. The region's focus on premium and luxury vehicle segments also contributes to higher electronic content per vehicle.

- North America: Exhibits strong growth, propelled by increasing consumer demand for advanced in-car technologies, significant investments in EV infrastructure, and the presence of leading automotive OEMs and technology companies. The United States, in particular, is a key market for ADAS integration and electric vehicle manufacturing, driving the need for a wide range of MLCCs. Canada and Mexico also contribute through their respective automotive production capabilities.

- Latin America: An emerging market with growing potential, influenced by increasing vehicle production and a gradual shift towards more technologically equipped cars. While the adoption of EVs and ADAS is slower compared to developed regions, the market is expected to witness steady growth as economic conditions improve and automotive trends permeate the region. Brazil and Mexico are key automotive manufacturing hubs within Latin America.

- Middle East and Africa (MEA): A developing market for Automotive MLCCs, primarily driven by investments in new automotive manufacturing facilities and a rising demand for modern vehicles. While smaller in market share, the region presents long-term growth opportunities as governments focus on economic diversification and infrastructure development, which includes the automotive sector. The adoption of EVs and advanced electronics is still nascent but poised for future expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive MLCC Market.- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Samsung Electro-Mechanics

- Taiyo Yuden Co., Ltd.

- Kyocera Corporation (AVX Corporation)

- KEMET (YAGEO Corporation)

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Darfon Electric Co., Ltd.

- Chilik Elec., Inc.

- Nippon Chemi-Con Corporation

- EPCOS AG (TDK Group)

- ROHM Co., Ltd.

- KOA Corporation

- Panasonic Corporation

- Littelfuse, Inc.

- API Technologies Corp.

- Syfer Technology Ltd. (Knowles Corporation)

- CDE Cornell Dubilier

- DMEGC Components Co., Ltd.

Frequently Asked Questions

What is the current estimated market size of the Automotive MLCC market?

The Automotive MLCC market is estimated at USD 4.85 Billion in 2025, reflecting robust demand driven by automotive electronics growth.

What is the projected growth rate for the Automotive MLCC market by 2033?

The Automotive MLCC market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8%, reaching USD 11.84 Billion by 2033, primarily due to vehicle electrification and advanced systems.

Which key factors are driving the growth of the Automotive MLCC market?

Key drivers include the rapid adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs), the proliferation of Advanced Driver-Assistance Systems (ADAS), and the increasing electronic content per vehicle in infotainment and connectivity.

What impact does AI have on the Automotive MLCC industry?

AI significantly impacts MLCC manufacturing through enhanced efficiency, superior quality control via automated inspection, accelerated design and simulation, and improved supply chain optimization, leading to higher quality and faster production.

What are the primary challenges facing Automotive MLCC manufacturers?

Primary challenges include intense market competition, volatility in raw material prices, the need to meet stringent automotive quality standards, and managing rapid technological advancements in vehicle electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted