Automotive Interior Material Market

Automotive Interior Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700360 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Interior Material Market Size

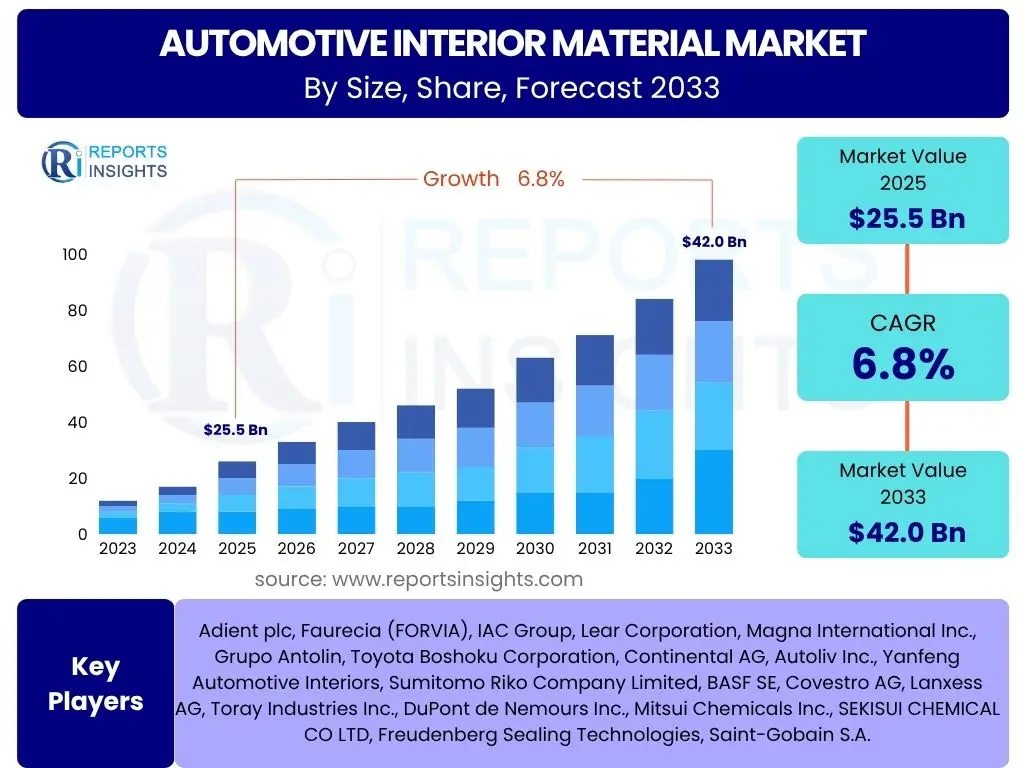

Automotive Interior Material Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 25.5 billion in 2025 and is projected to grow to USD 42.0 billion by 2033 the end of the forecast period.

Key Automotive Interior Material Market Trends & Insights

The automotive interior material market is undergoing a significant transformation driven by evolving consumer demands, technological advancements, and a heightened focus on sustainability. Key trends include a shift towards lightweighting materials to improve fuel efficiency and extend EV range, alongside a growing demand for premium, comfortable, and aesthetically pleasing interior finishes. The integration of smart surfaces and haptics, enabled by advanced materials, is enhancing user experience and interaction within the vehicle cabin. Furthermore, the market is seeing a strong emphasis on eco-friendly and recycled materials, aligning with global sustainability initiatives and consumer preferences for greener products. Customization and personalization options are also emerging as crucial differentiating factors, allowing vehicle owners to tailor their interiors.

- Increased adoption of lightweight materials for fuel efficiency and EV range extension.

- Rising demand for sustainable and recycled interior materials.

- Integration of smart surfaces, haptics, and ambient lighting for enhanced user experience.

- Growing preference for premium, luxurious, and customizable interior aesthetics.

- Technological advancements in material science leading to improved durability and functionality.

- Shift towards simplified, minimalist interior designs with integrated functionalities.

AI Impact Analysis on Automotive Interior Material

Artificial intelligence is increasingly influencing the automotive interior material market, from design and manufacturing processes to the functionality and user interaction within the vehicle cabin. AI-driven generative design tools can rapidly explore new material compositions and structural layouts, optimizing for weight, strength, and acoustic properties simultaneously. In manufacturing, AI can enhance quality control through automated inspection, predict material defects, and optimize production lines for efficiency and waste reduction. For smart interiors, AI enables adaptive environments that respond to occupant preferences, such as adjusting lighting, climate, and infotainment based on learned behaviors and real-time sensor data, thus driving demand for materials compatible with integrated sensors and displays. Predictive analytics, powered by AI, can also monitor material wear and suggest maintenance, extending the lifespan of interior components.

- AI-driven generative design for material optimization and innovative interior concepts.

- Enhanced quality control and defect detection in manufacturing processes using AI.

- Integration of AI for predictive maintenance and wear analysis of interior materials.

- Development of smart interiors with AI-powered adaptive features (e.g., climate, lighting, infotainment).

- Optimization of material sourcing and supply chain logistics through AI analytics.

Key Takeaways Automotive Interior Material Market Size & Forecast

- The global automotive interior material market is poised for robust growth, driven by increasing vehicle production and evolving consumer expectations.

- Significant market expansion is projected from USD 25.5 billion in 2025 to USD 42.0 billion by 2033, demonstrating a healthy CAGR of 6.8%.

- Sustainability and lightweighting are core market drivers, influencing material innovation and adoption.

- The advent of electric vehicles and autonomous driving is creating new opportunities for material suppliers, emphasizing comfort, aesthetics, and integrated technology.

- Asia Pacific is expected to remain a dominant region due to high automotive manufacturing volumes and rising disposable incomes.

- Manufacturers are focusing on developing advanced polymers, natural fibers, and smart materials to meet diverse industry requirements.

Automotive Interior Material Market Drivers Analysis

The growth of the automotive interior material market is propelled by a confluence of factors, including the increasing global demand for automobiles, especially in emerging economies, and the relentless pursuit of enhanced vehicle aesthetics, comfort, and safety. Furthermore, stringent environmental regulations are driving manufacturers to adopt lightweight and sustainable materials, while the rapid evolution of electric vehicles (EVs) and autonomous driving technologies necessitates innovative interior solutions that support new cabin designs and functionalities. Consumers are also exhibiting a growing preference for premium and technologically advanced interiors, prompting material suppliers to invest in research and development to offer high-quality, durable, and feature-rich products.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Automotive Production & Sales | +1.5% | Asia Pacific, North America, Europe | Short to Mid-Term |

| Rising Demand for Premium & Comfortable Vehicle Interiors | +1.2% | Europe, North America, China | Mid to Long-Term |

| Stringent Regulations for Fuel Efficiency & Emission Reduction (Lightweighting) | +1.0% | Europe, North America, Japan | Mid-Term |

| Growth in Electric Vehicle (EV) Adoption & New Interior Concepts | +1.3% | China, Europe, North America | Mid to Long-Term |

| Technological Advancements in Material Science & Smart Interiors | +0.8% | Global | Long-Term |

Automotive Interior Material Market Restraints Analysis

Despite significant growth prospects, the automotive interior material market faces several restraints that could impede its expansion. Volatility in the prices of raw materials, such as crude oil derivatives for plastics and natural fibers, directly impacts manufacturing costs and profitability for material suppliers. Furthermore, increasingly stringent environmental regulations regarding vehicle emissions and the use of hazardous substances in materials pose challenges for compliance and necessitate expensive research and development for alternative, eco-friendly solutions. Intense competition among material suppliers often leads to price pressures, compelling companies to lower margins. Additionally, the automotive industry's cyclical nature and susceptibility to economic downturns can lead to reduced vehicle production, directly affecting demand for interior materials. The complex and often fragmented supply chain for diverse interior components also presents logistical and quality control challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.7% | Global | Short to Mid-Term |

| Stringent Environmental & Emission Regulations | -0.5% | Europe, North America, Japan | Mid-Term |

| High Research & Development Costs for New Materials | -0.4% | Global | Long-Term |

| Supply Chain Disruptions & Geopolitical Tensions | -0.6% | Global | Short-Term |

Automotive Interior Material Market Opportunities Analysis

The automotive interior material market is rich with opportunities driven by emerging technologies, shifting consumer preferences, and a global pivot towards sustainability. The increasing focus on circular economy principles presents significant avenues for the development and adoption of recycled, bio-based, and sustainably sourced materials, appealing to environmentally conscious consumers and meeting future regulatory mandates. Furthermore, the rapid expansion of electric and autonomous vehicles is transforming interior spaces into "living rooms on wheels," demanding new functionalities like smart surfaces, integrated displays, and customizable ambient lighting, which in turn fuels innovation in material science. The growing demand for vehicle personalization and unique interior designs also opens doors for aftermarket customization options and specialized material offerings. Moreover, advancements in manufacturing processes, such as 3D printing, could enable more complex designs and on-demand production, creating niche market opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Sustainable & Recycled Materials | +1.4% | Europe, North America, Asia Pacific | Mid to Long-Term |

| Growth in Smart & Connected Interior Technologies | +1.1% | Global | Mid to Long-Term |

| Expansion of Electric & Autonomous Vehicle Market | +1.3% | China, Europe, North America | Mid to Long-Term |

| Increasing Demand for Vehicle Personalization & Customization | +0.9% | North America, Europe, Developed Asia | Mid-Term |

Automotive Interior Material Market Challenges Impact Analysis

The automotive interior material market faces several significant challenges that require strategic navigation from industry participants. Meeting constantly evolving consumer preferences for aesthetics, durability, and new functionalities while simultaneously managing cost pressures from original equipment manufacturers (OEMs) remains a substantial hurdle. Integrating new and complex technologies, such as haptic feedback systems and large interactive displays, into traditional material manufacturing processes demands significant investment and expertise. Furthermore, ensuring intellectual property protection for innovative material compositions and design methodologies is crucial in a competitive landscape. The global nature of the automotive supply chain also presents challenges related to logistics, quality consistency across different regions, and adaptability to regional regulatory variances. Moreover, the long development cycles for new vehicle platforms necessitate material suppliers to anticipate future trends well in advance, posing forecasting complexities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Meeting Evolving Consumer Preferences & Aesthetic Demands | -0.6% | Global | Short to Mid-Term |

| Intense Cost Pressures from OEMs | -0.8% | Global | Short to Mid-Term |

| Integration of Advanced Technologies (e.g., Smart Surfaces, Haptics) | -0.5% | Global | Mid-Term |

| Managing Complex & Global Supply Chains | -0.7% | Global | Short to Mid-Term |

| Adherence to Strict Safety & Performance Standards | -0.4% | Global | Long-Term |

Automotive Interior Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global automotive interior material market, offering a detailed understanding of its current state, historical performance, and future growth trajectories. The scope encompasses market sizing, growth forecasts, key trends, the impact of artificial intelligence, and a thorough examination of market drivers, restraints, opportunities, and challenges. It also includes extensive segmentation analysis by material type, vehicle type, application, and region, along with competitive landscaping and profiles of leading industry players, providing strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 42.0 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Adient plc, Faurecia (FORVIA), IAC Group, Lear Corporation, Magna International Inc., Grupo Antolin, Toyota Boshoku Corporation, Continental AG, Autoliv Inc., Yanfeng Automotive Interiors, Sumitomo Riko Company Limited, BASF SE, Covestro AG, Lanxess AG, Toray Industries Inc., DuPont de Nemours Inc., Mitsui Chemicals Inc., SEKISUI CHEMICAL CO LTD, Freudenberg Sealing Technologies, Saint-Gobain S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive interior material market is meticulously segmented to provide a granular view of its diverse components and drivers. This segmentation allows for precise market sizing, trend identification, and strategic planning for various industry stakeholders. Understanding how different material types, vehicle categories, and applications contribute to the overall market enables businesses to identify lucrative niches and tailor their product offerings to specific demands. The market is primarily broken down by the type of material used, the specific component within the vehicle interior, the type of vehicle it is installed in, and the sales channel through which it reaches the end-user, offering a multi-dimensional perspective of the market landscape.

- By Material Type: This segment includes the various raw materials utilized in automotive interiors.

- Plastics: The largest segment, encompassing Polypropylene (PP), Polyurethane (PU), Polyvinyl Chloride (PVC), Acrylonitrile Butadiene Styrene (ABS), Polycarbonate (PC), and Polyamide (PA), chosen for their versatility, low cost, and formability in components like dashboards, door panels, and consoles.

- Composites: Materials like Natural Fiber Composites (NFCs), Carbon Fiber Composites, and Glass Fiber Composites are increasingly used for lightweighting, structural integrity, and sustainable attributes in load-bearing or aesthetic parts.

- Fabrics: This includes Polyester, Nylon, natural fibers, and blends used for seating upholstery, headliners, and floor carpets, focusing on comfort, durability, and aesthetics. Leather and Vinyl also fall under this category, offering premium and durable surfaces.

- Metals: Used for structural support, trim, and functional components, including aluminum and steel alloys for frames and decorative elements.

- Glass: Primarily for interior mirrors and certain display covers, chosen for clarity and scratch resistance.

- Ceramics: Niche applications for specific luxury trims or functional components requiring high heat resistance or unique aesthetics.

- By Component Type: This segmentation focuses on the specific parts of the vehicle interior where these materials are applied.

- Dashboard & Cockpit: Materials for instrument panels, center consoles, infotainment surrounds, emphasizing aesthetics, tactile feel, and integration of electronics.

- Seating: Covers materials used for seat upholstery, foams, and internal structures, prioritizing comfort, ergonomics, durability, and safety features.

- Door Panels: Materials for inner door linings, armrests, and storage pockets, focusing on impact resistance, sound insulation, and tactile quality.

- Headliners: Materials for the interior roof lining, chosen for acoustic properties, thermal insulation, and aesthetic finish.

- Floor Carpets & Mats: Materials for flooring, focusing on durability, stain resistance, and sound dampening.

- Other Trim Components: Includes materials for pillars, luggage compartments, steering wheels, gear shifters, and various decorative trims.

- By Vehicle Type: This category differentiates demand based on the type of vehicle.

- Passenger Vehicles: Including Sedans, Sport Utility Vehicles (SUVs), and Hatchbacks, which represent the largest volume for interior material consumption, with varying demands based on segment (economy, luxury).

- Commercial Vehicles: Encompasses Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs), where durability, functionality, and ease of cleaning are often prioritized over luxury.

- Electric Vehicles (EVs): Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), and Hybrid Electric Vehicles (HEV) are driving demand for lightweight materials and new interior configurations that optimize cabin space and integrate advanced technologies.

- By Sales Channel: This segment identifies how the materials reach the market.

- Original Equipment Manufacturer (OEM): The primary channel where materials are supplied directly to automotive manufacturers for new vehicle production.

- Aftermarket: Involves the supply of materials for vehicle repair, maintenance, customization, and upgrades after the initial sale, including custom upholstery, floor mats, and interior trim kits.

Regional Highlights

The global automotive interior material market exhibits significant regional variations in demand, production, and technological adoption, influenced by local automotive manufacturing hubs, economic conditions, and consumer preferences. Understanding these regional dynamics is crucial for market participants to formulate effective localization strategies and identify high-growth opportunities. Each major region contributes uniquely to the market's overall trajectory, reflecting differing priorities in terms of material innovation, sustainability efforts, and vehicle segment growth.

- Asia Pacific: This region stands as the largest and fastest-growing market for automotive interior materials, primarily driven by robust automotive production, particularly in China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and the expanding middle class in countries like China and India are fueling demand for both passenger and commercial vehicles, consequently boosting the need for interior materials. The region is also becoming a hub for EV manufacturing, necessitating advancements in lightweight and smart interior components. Cost-effectiveness and production scale are key drivers here, alongside a rising interest in premium and technologically integrated interiors.

- Europe: A mature yet highly innovative market, Europe is characterized by stringent environmental regulations and a strong emphasis on premiumization, safety, and sustainable materials. Countries like Germany, France, and the UK are at the forefront of adopting advanced lightweight composites, natural fibers, and recycled plastics to meet emission targets and cater to discerning consumers seeking luxurious and eco-friendly vehicle interiors. The rapid transition to electric vehicles and the focus on autonomous driving technologies also drive demand for sophisticated and comfortable cabin designs, integrated with intelligent surfaces.

- North America: This region represents a significant market, influenced by high consumer demand for large SUVs and pickup trucks, alongside a growing shift towards EVs. Key countries like the United States and Canada are witnessing increased adoption of advanced materials that offer durability, comfort, and aesthetics. There is a strong focus on personalized interiors and the integration of advanced infotainment systems, which requires materials compatible with new display technologies, haptics, and smart sensors. Innovation in material science for improved safety features and enhanced user experience is a major trend.

- Latin America: An emerging market with steady growth, primarily led by countries such as Brazil and Mexico. The demand for automotive interior materials in this region is influenced by increasing vehicle sales, particularly in the mid-range and economy segments. While cost-effectiveness remains a key consideration, there is a gradual shift towards better quality and more aesthetically pleasing interiors. The region's automotive industry is also gradually integrating sustainable practices and materials, though at a slower pace compared to developed regions.

- Middle East and Africa (MEA): This region is experiencing growth driven by infrastructure development, rising income levels, and increased automotive imports and local assembly operations in certain countries. Demand for interior materials is rising in line with vehicle sales, with a preference for durable and climate-resistant materials due to the harsh environmental conditions in some parts of the region. The luxury vehicle segment also plays a significant role, contributing to the demand for premium interior materials.

Top Key Players:

The market research report covers the analysis of key stake holders of the Automotive Interior Material Market. Some of the leading players profiled in the report include -- Adient plc

- Faurecia (FORVIA)

- IAC Group

- Lear Corporation

- Magna International Inc.

- Grupo Antolin

- Toyota Boshoku Corporation

- Continental AG

- Autoliv Inc.

- Yanfeng Automotive Interiors

- Sumitomo Riko Company Limited

- BASF SE

- Covestro AG

- Lanxess AG

- Toray Industries Inc.

- DuPont de Nemours Inc.

- Mitsui Chemicals Inc.

- SEKISUI CHEMICAL CO LTD

- Freudenberg Sealing Technologies

- Saint-Gobain S.A.

Frequently Asked Questions:

What is the current market size and projected growth of the Automotive Interior Material Market?

The global Automotive Interior Material Market was estimated at USD 25.5 billion in 2025 and is projected to grow to USD 42.0 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This growth is driven by increasing vehicle production, evolving consumer preferences, and advancements in material technology.What are the primary drivers influencing the Automotive Interior Material Market?

Key drivers include the global increase in automotive production and sales, rising demand for premium and comfortable vehicle interiors, stringent regulations promoting lightweighting for fuel efficiency, and the significant growth in electric vehicle (EV) adoption leading to new interior design requirements. Technological advancements in material science also play a crucial role.How is sustainability impacting the Automotive Interior Material Market?

Sustainability is a major trend, driving a significant shift towards the development and adoption of recycled, bio-based, and sustainably sourced materials. Manufacturers are increasingly focusing on reducing the environmental footprint of interior components, meeting regulatory mandates, and responding to consumer demand for eco-friendly products.What role does AI play in the Automotive Interior Material sector?

AI is impacting the automotive interior material sector by enabling advanced generative design for optimal material properties, enhancing quality control and defect detection in manufacturing, and facilitating the development of smart interiors that adapt to occupant preferences. AI also aids in predictive maintenance and supply chain optimization for materials.Which regions are key contributors to the Automotive Interior Material Market?

Asia Pacific is the largest and fastest-growing market, propelled by high automotive production volumes and economic growth. Europe is a significant market driven by stringent regulations and a focus on premium and sustainable materials. North America also contributes substantially due to strong consumer demand for large vehicles and technological integration.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted