Automotive Infotainment Testing Platform Market

Automotive Infotainment Testing Platform Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708284 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

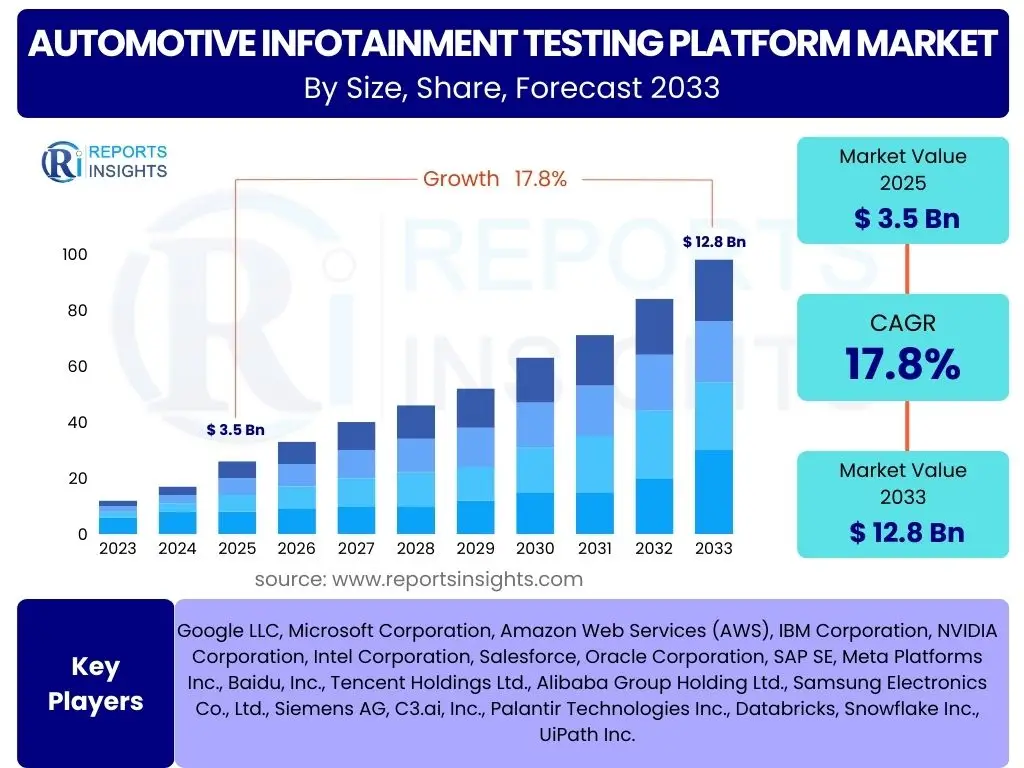

Automotive Infotainment Testing Platform Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Infotainment Testing Platform Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.8% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 12.8 Billion by the end of the forecast period in 2033.

Key Automotive Infotainment Testing Platform Market Trends & Insights

User inquiries frequently highlight the rapid evolution of in-vehicle experience and the increasing complexity of automotive infotainment systems as central to market trends. There is a strong focus on how seamless user experience, advanced connectivity options, and integration with other vehicle domains (like ADAS) are shaping the demand for sophisticated testing platforms. Users are keen to understand the shift towards software-defined vehicles and its implications for testing, including the need for continuous validation and over-the-air (OTA) update compatibility. The convergence of consumer electronics features and automotive reliability standards also presents a unique challenge, driving innovation in testing methodologies.

Furthermore, discussions often revolve around the adoption of cloud-based testing infrastructure and the growing necessity for robust cybersecurity testing within infotainment systems. The desire for personalized and contextual services, along with multimodal interaction capabilities (voice, touch, gesture), means testing platforms must adapt to a broader spectrum of user scenarios and input methods. The industry is also seeing a push towards more standardized testing frameworks, though fragmentation remains a significant point of interest for market participants.

- Shift towards software-defined vehicles and continuous integration/delivery (CI/CD) pipelines.

- Integration of advanced driver-assistance systems (ADAS) and autonomous driving features with infotainment.

- Increasing demand for hyper-personalized in-car experiences and user interfaces.

- Proliferation of cloud-based testing environments and virtual validation tools.

- Enhanced focus on cybersecurity testing for connected infotainment systems.

- Development of multi-modal human-machine interfaces (HMI) requiring comprehensive usability testing.

- Adoption of over-the-air (OTA) update capabilities necessitates extensive regression testing.

- Growing complexity of in-vehicle networking and communication protocols (e.g., Ethernet, CAN FD).

- Emphasis on performance and real-time responsiveness for rich multimedia content.

- Demand for robust tools to test advanced connectivity features (5G, V2X).

AI Impact Analysis on Automotive Infotainment Testing Platform

Common user questions regarding AI's impact on automotive infotainment testing platforms reveal a strong interest in automation, efficiency, and predictive capabilities. Users are exploring how AI can streamline the test process, reduce human intervention, and identify potential issues earlier in the development cycle. There is a particular focus on AI-driven test case generation, anomaly detection, and the ability to simulate complex real-world driving scenarios to ensure robust system performance and safety. Expectations are high for AI to address the escalating complexity of software-defined vehicles, especially in managing the vast number of permutations in infotainment features and user interactions.

Moreover, the discussion often extends to AI's role in enhancing the quality and reliability of infotainment systems by learning from past test data and predicting future failures. Users are also concerned with how AI can optimize resource allocation in testing, accelerate validation cycles for OTA updates, and contribute to better decision-making through data-driven insights. While the potential benefits are clear, questions also arise about the trustworthiness of AI-generated tests, the need for human oversight, and the ethical implications of autonomous testing. The integration of machine learning for personalized user experiences within infotainment itself also necessitates AI-powered testing to validate adaptive algorithms.

- AI-powered automated test case generation, reducing manual effort and improving coverage.

- Machine learning for predictive analytics in defect detection and failure prediction.

- Enhanced test orchestration and resource optimization through AI algorithms.

- AI-driven anomaly detection in log files and performance data for faster issue identification.

- Cognitive testing for HMI, leveraging AI to simulate human user behavior and preferences.

- Use of reinforcement learning for autonomous validation of complex, adaptive infotainment features.

- AI in virtual testing and simulation environments to create realistic and diverse test scenarios.

- Optimization of regression testing cycles through intelligent test selection and prioritization.

- Support for testing AI-driven features within infotainment itself, such as voice assistants and personalized content recommendations.

- Streamlining of data analysis from extensive test runs, providing actionable insights.

Key Takeaways Automotive Infotainment Testing Platform Market Size & Forecast

User queries indicate a strong recognition of the automotive infotainment testing platform market's substantial growth trajectory, driven by an insatiable demand for connected, intuitive, and feature-rich in-car experiences. The forecasted market expansion to USD 12.8 Billion by 2033 underscores the critical role testing plays in managing the inherent complexity and ensuring the reliability of these advanced systems. Stakeholders are particularly interested in how technological advancements, especially in software and connectivity, are not only fueling this growth but also fundamentally transforming testing methodologies. The market is not just expanding in size but also in its technological sophistication, with a clear move towards more integrated, automated, and intelligent testing solutions.

Moreover, a recurring theme in user questions is the understanding that this market's growth is intrinsically linked to broader automotive industry trends, such as the rise of electric vehicles, autonomous driving, and software-defined architectures. The need for robust validation is paramount to ensure safety, security, and a seamless user experience in a rapidly evolving vehicle landscape. The market forecast highlights a sustained investment in testing infrastructure as OEMs and Tier 1 suppliers strive to deliver cutting-edge infotainment solutions while mitigating risks associated with complex software integration and stringent regulatory requirements.

- Significant market expansion expected, driven by increasing infotainment complexity and connectivity.

- High CAGR of 17.8% reflects rapid technological adoption and investment in robust validation.

- Shift towards software-defined vehicles is a primary catalyst for testing platform innovation.

- Critical importance of ensuring system reliability, safety, and cybersecurity in connected cars.

- Growing demand for advanced, automated, and intelligent testing solutions, including AI integration.

- Validation of seamless user experience and multi-modal human-machine interfaces is a key focus.

- Market growth is global, with strong contributions from major automotive manufacturing regions.

- Continuous testing and validation for over-the-air (OTA) updates are becoming standard practice.

- Investment in cloud-based and virtual testing environments is accelerating.

- Meeting consumer expectations for smartphone-like experiences in vehicles necessitates rigorous testing.

Automotive Infotainment Testing Platform Market Drivers Analysis

The automotive infotainment testing platform market is primarily driven by the escalating demand for sophisticated in-car entertainment, navigation, and connectivity features. As consumers increasingly expect smartphone-like experiences within their vehicles, manufacturers are compelled to integrate advanced infotainment systems that are not only feature-rich but also highly reliable and secure. This push for innovation translates directly into a greater need for comprehensive testing platforms capable of validating complex software, hardware, and network integrations.

Furthermore, the rapid evolution towards software-defined vehicles (SDVs) and the integration of advanced driver-assistance systems (ADAS) with infotainment functionalities significantly contribute to market expansion. The intertwining of these critical systems necessitates testing solutions that can verify seamless interaction, real-time performance, and robust security protocols across various vehicle domains. The continuous demand for over-the-air (OTA) updates also acts as a strong driver, requiring sophisticated testing to ensure new features and bug fixes are deployed flawlessly without compromising existing functionalities. The global regulatory landscape, with its increasing focus on automotive safety and cybersecurity, further mandates rigorous testing, thereby boosting the adoption of advanced testing platforms.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of Infotainment Systems | +4.5% | Global, particularly North America, Europe, APAC | Short-term to Long-term |

| Rising Demand for Connected Cars & Enhanced User Experience | +3.8% | Global, especially tech-forward markets | Short-term to Mid-term |

| Adoption of Software-Defined Vehicle Architectures | +3.2% | Europe, North America, Japan, China | Mid-term to Long-term |

| Integration with ADAS & Autonomous Driving Systems | +2.7% | North America, Europe, China | Mid-term to Long-term |

| Stringent Regulatory Compliance and Cybersecurity Standards | +2.0% | Europe (UNECE R155/156), North America, APAC | Short-term to Long-term |

Automotive Infotainment Testing Platform Market Restraints Analysis

Despite robust growth drivers, the automotive infotainment testing platform market faces several significant restraints that could impede its full potential. One primary challenge is the high upfront investment required for developing and implementing sophisticated testing infrastructure. This includes not only the cost of advanced hardware-in-the-loop (HIL) and software-in-the-loop (SIL) systems but also the expense of specialized software licenses, skilled personnel, and continuous maintenance. For smaller players or emerging OEMs, these costs can be prohibitive, creating a barrier to entry and limiting widespread adoption of the most advanced testing solutions.

Another major restraint is the rapid pace of technological obsolescence in the infotainment sector. With new features, connectivity standards, and user interfaces emerging constantly, testing platforms need continuous upgrades and adaptability, which can be resource-intensive. The lack of standardized testing protocols across the fragmented automotive supply chain also presents a hurdle, leading to compatibility issues and redundant testing efforts. Furthermore, the increasing complexity of cybersecurity threats to connected infotainment systems, coupled with the difficulty of comprehensive vulnerability testing, poses a significant restraint, as it demands ever more sophisticated and resource-intensive security validation processes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Implementation Costs | -2.5% | Global, particularly emerging markets | Short-term to Mid-term |

| Rapid Technological Obsolescence | -2.0% | Global, especially developed markets | Short-term to Long-term |

| Lack of Standardized Testing Protocols | -1.8% | Global, across supply chain | Short-term to Mid-term |

| Complex Integration Challenges and Software Bugs | -1.5% | Global, industry-wide | Short-term to Long-term |

| Shortage of Skilled Workforce in Specialized Testing | -1.2% | North America, Europe, Japan | Mid-term to Long-term |

Automotive Infotainment Testing Platform Market Opportunities Analysis

Significant opportunities exist within the automotive infotainment testing platform market, primarily driven by the ongoing digital transformation of the automotive industry. The burgeoning adoption of cloud-based testing solutions and virtual validation environments presents a major avenue for growth. These technologies offer scalability, flexibility, and cost-effectiveness, enabling more efficient testing cycles and collaborative development across geographically dispersed teams. As vehicle architectures become increasingly software-centric, the demand for sophisticated virtual testing tools that can simulate complex real-world scenarios will only grow, accelerating time-to-market for new infotainment features.

Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into testing platforms offers a substantial opportunity to enhance automation, predictive analytics, and test coverage. AI can optimize test case generation, identify subtle anomalies, and even learn from previous test outcomes to prioritize critical areas, thereby significantly improving the efficiency and effectiveness of the testing process. The proliferation of over-the-air (OTA) updates for software-defined vehicles also opens up opportunities for continuous validation and regression testing services, ensuring the integrity and performance of infotainment systems throughout their lifecycle. Moreover, the increasing focus on advanced connectivity (e.g., 5G, V2X) and the development of new mobility services create a need for specialized testing platforms that can validate these emerging technologies, offering new revenue streams for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Cloud-Based Testing & Virtual Validation | +3.0% | Global, especially for collaborative development | Short-term to Mid-term |

| Integration of AI/ML for Automated & Predictive Testing | +2.8% | Global, across R&D centers | Mid-term to Long-term |

| Growing Demand for Continuous Integration/Deployment (CI/CD) Tools | +2.5% | Europe, North America, Japan | Short-term to Mid-term |

| Specialized Testing for 5G, V2X, & New Mobility Services | +2.2% | China, North America, Europe | Mid-term to Long-term |

| Expansion into Post-Production OTA Update Validation Services | +1.9% | Global, OEMs and Tier 1s | Mid-term to Long-term |

Automotive Infotainment Testing Platform Market Challenges Impact Analysis

The automotive infotainment testing platform market confronts several formidable challenges that require innovative solutions and strategic adjustments. One prominent challenge is managing the escalating complexity of software-defined vehicles, where infotainment systems are deeply integrated with safety-critical functions and rely on vast amounts of code. This interconnectedness makes fault isolation and comprehensive regression testing exceptionally difficult, demanding more sophisticated and adaptable testing platforms that can handle intricate dependencies and real-time interactions across multiple domains.

Another significant challenge stems from the need to ensure real-time performance and responsiveness of infotainment systems, especially as they incorporate demanding multimedia, advanced graphics, and low-latency connectivity features. Testing for these performance benchmarks under various operating conditions, including network fluctuations and high data loads, requires highly specialized tools and methodologies. Furthermore, the ever-present threat of cybersecurity vulnerabilities and the complexity of testing for robust security across the entire software stack remains a critical challenge. The automotive industry also faces a talent gap in specialized testing, particularly for expertise in AI, cybersecurity, and cloud-native testing, which can hinder the adoption and effective utilization of advanced testing platforms.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Software-Defined Vehicle Complexity | -2.8% | Global, especially established automotive regions | Short-term to Long-term |

| Ensuring Real-time Performance and Responsiveness | -2.3% | Global, with high consumer expectations | Short-term to Mid-term |

| Addressing Cybersecurity Vulnerabilities | -2.0% | Global, across all connected vehicles | Short-term to Long-term |

| Integration with Diverse Hardware and Software Ecosystems | -1.7% | Global, across OEMs and suppliers | Short-term to Mid-term |

| Talent Shortage in Specialized Testing Domains | -1.5% | North America, Europe, Asia Pacific | Mid-term to Long-term |

Automotive Infotainment Testing Platform Market - Updated Report Scope

This report provides a comprehensive analysis of the Automotive Infotainment Testing Platform market, offering detailed insights into market size, growth trends, key drivers, restraints, opportunities, and challenges from 2019 to 2033. It encompasses a thorough examination of segmentation by component, vehicle type, end-user, testing type, and deployment method, alongside a robust regional analysis. The report also profiles leading market players, assesses the impact of AI, and outlines crucial market takeaways, serving as a strategic resource for stakeholders to navigate market dynamics and identify growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 12.8 Billion |

| Growth Rate | 17.8% |

| Number of Pages | 247 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | KPIT, Harman International, Elektrobit, ETAS GmbH, dSPACE GmbH, Vector Informatik GmbH, National Instruments (NI), Tata Elxsi, Wipro Limited, Capgemini Engineering, Cognizant, Infosys, Continental AG, Aptiv PLC, Bosch GmbH, LG Electronics, Panasonic Corporation, Visteon Corporation, Siemens Digital Industries Software, Ansys Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Infotainment Testing Platform market is meticulously segmented to provide a granular view of its diverse landscape and to identify specific growth areas and market dynamics. This segmentation helps in understanding the various facets influencing market demand, technological adoption, and competitive strategies. The market is primarily bifurcated by component, reflecting the essential hardware and software elements required for comprehensive testing. Further divisions based on vehicle type and end-user highlight the specific needs of different automotive sectors and stakeholders. Moreover, the segmentation by testing type outlines the critical areas of validation, while deployment type distinguishes between traditional and modern infrastructure approaches.

Each segment offers unique insights into where investment and innovation are concentrated. For instance, the component-based segmentation distinguishes between hardware-centric solutions like HIL and software-driven tools such as test automation software. The end-user segmentation elucidates the distinct requirements of OEMs, Tier 1 suppliers, and independent software vendors, each facing different challenges in their product development cycles. This multi-dimensional segmentation ensures a holistic understanding of the market, allowing for targeted strategies and more accurate market forecasting across the automotive infotainment testing ecosystem.

- By Component: Hardware-in-the-Loop (HIL), Software-in-the-Loop (SIL), Test Automation Software, Test Rigs & Fixtures

- By Vehicle Type: Passenger Vehicles, Commercial Vehicles

- By End-User: Original Equipment Manufacturers (OEMs), Tier 1 Suppliers, Independent Software Vendors (ISVs), Test Service Providers

- By Testing Type: Functional Testing, Performance Testing, Usability Testing, Connectivity Testing, Security Testing, Regression Testing

- By Deployment Type: On-premise, Cloud-based

Regional Highlights

- North America: A dominant market due to early adoption of advanced automotive technologies, strong presence of major OEMs and tech companies, and significant R&D investment in connected and autonomous vehicles.

- Europe: Characterized by stringent regulatory standards for safety and cybersecurity, driving demand for robust testing platforms. Germany and the UK are key contributors with established automotive industries and a focus on innovation.

- Asia Pacific (APAC): The fastest-growing region, fueled by the rapid expansion of automotive manufacturing in China, India, Japan, and South Korea, coupled with increasing consumer demand for advanced infotainment features and electric vehicles.

- Latin America: An emerging market with growing automotive production and increasing demand for mid-range and premium vehicles, gradually adopting advanced testing solutions.

- Middle East and Africa (MEA): Showing nascent growth driven by investments in smart city initiatives and an increasing luxury car market, leading to a slow but steady adoption of modern infotainment testing platforms.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Infotainment Testing Platform Market.- KPIT

- Harman International

- Elektrobit

- ETAS GmbH

- dSPACE GmbH

- Vector Informatik GmbH

- National Instruments (NI)

- Tata Elxsi

- Wipro Limited

- Capgemini Engineering

- Cognizant

- Infosys

- Continental AG

- Aptiv PLC

- Bosch GmbH

- LG Electronics

- Panasonic Corporation

- Visteon Corporation

- Siemens Digital Industries Software

- Ansys Inc.

Frequently Asked Questions

What is the projected market size of the Automotive Infotainment Testing Platform by 2033?

The Automotive Infotainment Testing Platform Market is projected to reach USD 12.8 Billion by the end of 2033, growing at a CAGR of 17.8% from 2025.

What are the primary drivers for the growth of this market?

Key drivers include the increasing complexity of infotainment systems, rising demand for connected cars and enhanced user experience, the adoption of software-defined vehicle architectures, and stringent regulatory requirements for safety and cybersecurity.

How is AI impacting automotive infotainment testing?

AI is significantly impacting testing by enabling automated test case generation, predictive analytics for defect detection, intelligent test orchestration, and enhancing virtual validation through realistic scenario simulation, thereby increasing efficiency and coverage.

What are the main challenges faced by the market?

The market faces challenges such as managing the extreme complexity of software-defined vehicles, ensuring real-time performance and responsiveness, addressing sophisticated cybersecurity vulnerabilities, and overcoming the talent shortage in specialized testing domains.

Which regions are expected to contribute most to market growth?

North America and Europe are expected to maintain strong growth due to technological maturity and regulatory frameworks. The Asia Pacific region, particularly China, Japan, and South Korea, is anticipated to be the fastest-growing market owing to high automotive production and rapid adoption of advanced technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted