Aircraft Seating Market

Aircraft Seating Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709354 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Aircraft Seating Market Size

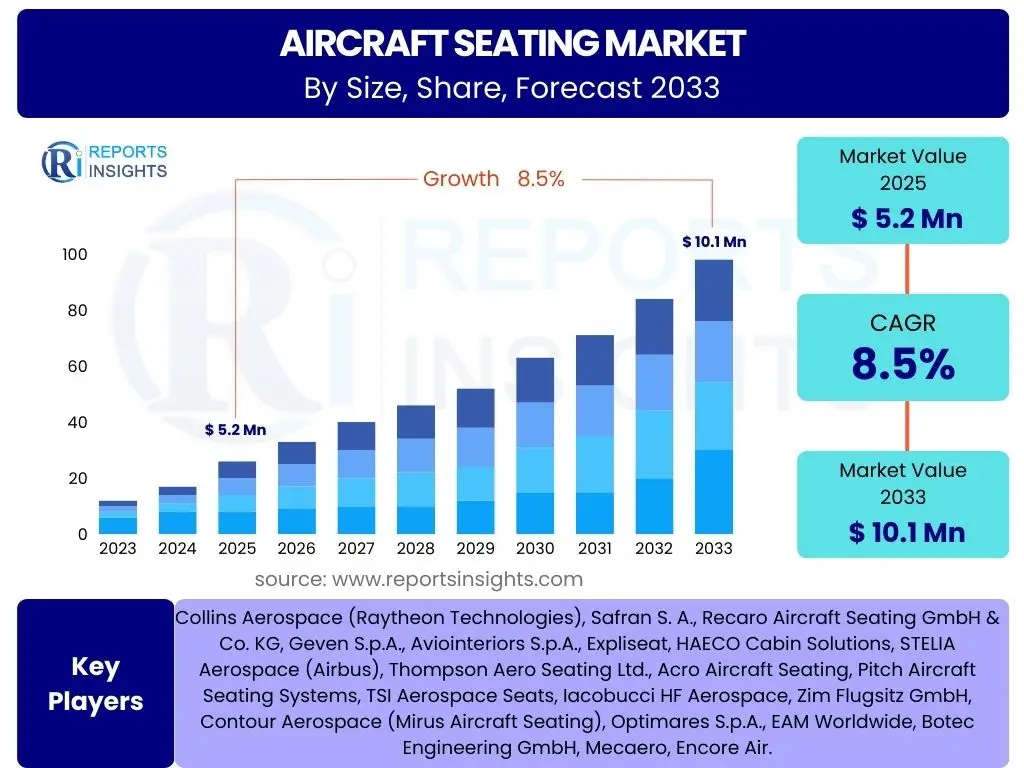

According to Reports Insights Consulting Pvt Ltd, The Aircraft Seating Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 5.2 Billion in 2025 and is projected to reach USD 10.1 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the consistent expansion of the global commercial aircraft fleet, an increasing demand for enhanced passenger comfort and premium cabin configurations, and ongoing innovations in material science and design methodologies aimed at reducing weight and improving durability.

The market's trajectory is also influenced by the post-pandemic recovery in air travel, which has stimulated new aircraft orders and retrofit programs. Airlines are increasingly focusing on optimizing cabin space, providing differentiated passenger experiences, and adopting sustainable materials, all of which contribute to the evolving landscape of aircraft seating. The shift towards lightweight seat designs is a critical factor, not only for fuel efficiency but also for meeting stricter environmental regulations and operational cost reduction targets. As air traffic volumes continue to recover and surpass pre-pandemic levels, the investment in advanced seating solutions will remain a priority for carriers globally.

Key Aircraft Seating Market Trends & Insights

The aircraft seating market is currently experiencing significant transformative trends driven by evolving passenger expectations, technological advancements, and stringent regulatory demands. Passengers are increasingly prioritizing comfort, connectivity, and personalized experiences, which has led to a surge in demand for premium economy, business, and first-class seating options offering enhanced features like lie-flat beds, advanced inflight entertainment systems, and integrated charging ports. This premiumization trend is a key driver for innovation in seat design, material selection, and overall cabin configuration.

Furthermore, sustainability and lightweighting remain paramount concerns for airlines seeking to reduce operational costs and environmental impact. Manufacturers are heavily investing in research and development to incorporate advanced composite materials, lighter metals, and eco-friendly fabrics that do not compromise on safety or durability. The modularity and customization of seating solutions are also gaining traction, allowing airlines greater flexibility in reconfiguring cabins to meet varying route demands or passenger load factors, thereby optimizing revenue per available seat mile. Ergonomic design and smart seating solutions, incorporating sensors for maintenance or passenger comfort monitoring, represent another frontier of innovation, promising enhanced operational efficiency and passenger satisfaction.

- Focus on lightweight materials (composites, advanced alloys) for fuel efficiency.

- Increasing demand for premium and customizable seating options (Business, First, Premium Economy).

- Integration of advanced in-flight entertainment and connectivity (IFEC) systems.

- Emphasis on enhanced passenger comfort, ergonomics, and personal space.

- Development of modular and reconfigurable seating solutions for operational flexibility.

- Adoption of sustainable materials and manufacturing processes.

- Implementation of smart seating technologies for predictive maintenance and personalized experiences.

AI Impact Analysis on Aircraft Seating

Artificial Intelligence (AI) is poised to significantly transform the aircraft seating industry by enhancing design, manufacturing, and operational aspects. Users frequently inquire about how AI can optimize seat design for ergonomics and weight reduction. AI-driven generative design tools can rapidly explore millions of design permutations, identifying optimal geometries and material distributions that traditional methods would miss, leading to lighter, stronger, and more comfortable seats. This capability accelerates the R&D cycle and facilitates the integration of complex features while adhering to stringent safety standards.

In manufacturing, AI can revolutionize production lines through predictive maintenance for machinery, quality control, and robotic assembly, thereby improving efficiency, reducing waste, and ensuring consistent product quality. Beyond production, AI's role extends to the operational phase of aircraft seating. Predictive analytics can forecast maintenance needs for seats, flagging potential issues before they cause service disruptions and optimizing maintenance schedules. Furthermore, AI could personalize passenger experiences by dynamically adjusting seat settings based on passenger preferences, flight conditions, or even biofeedback, paving the way for truly intelligent cabin environments that enhance comfort, safety, and operational effectiveness for airlines.

- AI-driven generative design for optimal seat structures, reducing weight and enhancing ergonomics.

- Predictive maintenance of seating components, improving reliability and reducing downtime.

- Automated quality control and inspection in seat manufacturing processes.

- Personalized in-flight experiences through AI-adjusted seat settings and features.

- Supply chain optimization for seat components using AI-powered analytics.

- Improved material selection and testing processes via machine learning algorithms.

Key Takeaways Aircraft Seating Market Size & Forecast

The aircraft seating market is on a robust growth trajectory, driven by a confluence of factors including increasing global air passenger traffic, aggressive fleet expansion plans by airlines, and a concerted focus on enhancing the in-flight passenger experience. A significant takeaway is the strong financial outlook, with the market projected to nearly double in value by 2033, underscoring sustained investment in both new aircraft and cabin retrofits. This growth is not merely volumetric but also reflects a strategic shift towards higher-value, more technologically advanced seating solutions.

Another crucial insight is the dual imperative of innovation: weight reduction for fuel efficiency and enhanced comfort/premiumization for passenger satisfaction and airline differentiation. Manufacturers must navigate the complex balance between these often-conflicting demands, leveraging new materials and smart technologies to deliver solutions that are both lightweight and feature-rich. The market also highlights the increasing importance of regional nuances, with high growth expected in Asia Pacific due to expanding middle-class populations and new airline entrants, while mature markets like North America and Europe will focus on fleet modernization and cabin upgrades. Successful market players will be those who can adapt quickly to these evolving regional needs and technological advancements.

- Robust growth projected with market value doubling by 2033, fueled by fleet expansion and passenger demand.

- Dual focus on lightweighting for operational efficiency and premiumization for passenger experience.

- Emerging markets, particularly Asia Pacific, are key growth drivers due to increasing air travel and new aircraft deliveries.

- Technological integration, including AI and advanced materials, will be critical for product differentiation and competitive advantage.

- Sustainability and eco-friendly manufacturing practices are becoming non-negotiable for market relevance.

Aircraft Seating Market Drivers Analysis

The global aircraft seating market is propelled by several potent drivers that reflect the dynamic nature of the aerospace and travel industries. A primary driver is the significant increase in global air passenger traffic, which necessitates continuous expansion and modernization of commercial aircraft fleets. As more people travel by air, airlines require more aircraft, and consequently, more advanced seating solutions to accommodate passengers effectively and comfortably. This demand extends across all cabin classes, from economy to premium segments, driving innovation in design and functionality.

Another critical driver is the ongoing emphasis by airlines on enhancing the passenger experience to gain competitive advantage and foster brand loyalty. This translates into a strong demand for more comfortable, aesthetically pleasing, and feature-rich seating, especially in premium economy, business, and first-class cabins. Additionally, the growing trend of airline fleet modernization and replacement cycles contributes significantly, as older aircraft are retired and new, more fuel-efficient models are introduced, often equipped with the latest seating technologies. Advancements in material science, offering lighter yet durable components, also enable manufacturers to meet evolving airline requirements for reduced operational costs and increased payload capacity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Air Passenger Traffic | +2.1% | Global, particularly APAC | Long-term (2025-2033) |

| Airline Fleet Expansion & Modernization | +1.8% | Global | Medium to Long-term |

| Growing Demand for Premium Cabin Segments | +1.5% | North America, Europe, APAC | Medium to Long-term |

| Advancements in Lightweight Materials | +1.3% | Global | Medium-term |

| Focus on Enhanced Passenger Experience | +1.1% | Global | Long-term |

Aircraft Seating Market Restraints Analysis

Despite robust growth drivers, the aircraft seating market faces several significant restraints that could temper its expansion. One of the primary challenges is the stringent regulatory and certification requirements imposed by aviation authorities worldwide. Ensuring compliance with rigorous safety standards, flammability tests, and crashworthiness regulations adds substantial time and cost to the design, manufacturing, and approval processes for new seating products. These complex certification procedures can delay market entry for innovative solutions and increase overall development expenditures for manufacturers.

Another notable restraint is the high initial investment cost associated with advanced aircraft seating, particularly for premium cabin configurations. Airlines, while keen to offer superior passenger experiences, often operate on tight margins, making the capital outlay for new or upgraded seats a considerable financial burden. This can lead to longer adoption cycles or a preference for more cost-effective, albeit less innovative, solutions. Furthermore, the volatility in raw material prices, particularly for metals and composites, can impact manufacturing costs and ultimately affect the pricing strategy of seating suppliers. Supply chain disruptions, as evidenced by recent global events, also pose a significant challenge, potentially delaying production and delivery schedules.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory & Certification Processes | -1.2% | Global | Continuous |

| High Initial Investment Costs for Airlines | -1.0% | Global | Long-term |

| Supply Chain Volatility & Material Price Fluctuations | -0.8% | Global | Short to Medium-term |

| Long Development & Qualification Cycles | -0.7% | Global | Continuous |

| Increased Focus on Aircraft Retrofit Challenges | -0.5% | North America, Europe | Medium-term |

Aircraft Seating Market Opportunities Analysis

Despite existing restraints, the aircraft seating market presents numerous lucrative opportunities for growth and innovation. The burgeoning demand for premium economy seating is a significant opportunity, as it offers airlines a middle ground between economy and business class, providing enhanced comfort and features at a more accessible price point. This segment allows airlines to increase revenue yield per seat while catering to a broader demographic of travelers seeking a better experience without the full expense of a business class ticket. Manufacturers capable of delivering innovative, cost-effective premium economy solutions are well-positioned for expansion.

Furthermore, the rapid expansion of the low-cost carrier (LCC) segment, particularly in emerging markets, creates an opportunity for highly durable, lightweight, and easily maintainable economy seating solutions. LCCs prioritize operational efficiency and rapid turnarounds, demanding seats that are robust, easy to clean, and minimize maintenance time and costs. Another key opportunity lies in the aftermarket and retrofit sector, as airlines frequently upgrade existing fleets rather than solely acquiring new aircraft. Providing modular and customizable seating solutions that can be easily integrated into older aircraft types opens up a substantial revenue stream. Finally, the growing emphasis on sustainable aviation and eco-friendly materials offers a significant competitive advantage for companies investing in green seating solutions, aligning with global environmental goals and consumer preferences for responsible travel.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for Premium Economy Class Seating | +1.6% | Global | Medium to Long-term |

| Growth of Low-Cost Carriers (LCCs) in Emerging Markets | +1.4% | APAC, Latin America, Africa | Long-term |

| Aftermarket & Retrofit Programs for Existing Fleets | +1.2% | North America, Europe | Medium-term |

| Development of Sustainable & Eco-Friendly Seat Materials | +1.0% | Global | Long-term |

| Customization & Personalization of Seating Solutions | +0.9% | Global | Medium-term |

Aircraft Seating Market Challenges Impact Analysis

The aircraft seating market faces several significant challenges that require strategic navigation from manufacturers and airlines alike. One prominent challenge is the increasing complexity of integrating advanced technologies into seats, such as sophisticated in-flight entertainment (IFE) systems, power outlets, and connectivity solutions. This integration must be seamless, reliable, and compliant with evolving cybersecurity and electrical safety standards, adding layers of design and testing complexity. Moreover, the weight implications of these integrated technologies can counteract efforts to create lightweight seats, forcing a delicate balance between features and fuel efficiency.

Another critical challenge stems from intense competition within the market, leading to pricing pressures and the need for continuous innovation to maintain market share. Manufacturers must invest heavily in R&D while simultaneously managing cost-effective production to remain competitive. Furthermore, geopolitical instability and trade tensions can disrupt global supply chains for critical components, leading to delays and increased costs. Adapting to the evolving regulatory landscape, especially concerning accessibility standards for passengers with disabilities, also presents design and manufacturing challenges, requiring flexible and inclusive seating solutions that meet diverse needs without compromising space or safety. The durability and maintenance of complex seating systems in high-traffic commercial environments also pose operational challenges for airlines, requiring robust designs and efficient aftermarket support.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Integration Complexity (IFE, Connectivity) | -1.1% | Global | Continuous |

| Intense Market Competition & Pricing Pressures | -0.9% | Global | Long-term |

| Geopolitical Instability & Supply Chain Disruptions | -0.8% | Global | Short to Medium-term |

| Balancing Weight Reduction with Enhanced Features | -0.7% | Global | Continuous |

| Evolving Regulatory & Accessibility Standards | -0.6% | North America, Europe | Medium to Long-term |

Aircraft Seating Market - Updated Report Scope

This comprehensive market insights report offers an in-depth analysis of the global aircraft seating market, providing a detailed assessment of its current status, historical performance, and future growth projections. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry. It delves into segmentation analysis across various parameters such as aircraft type, class, material, and sales channel, alongside a comprehensive regional outlook. The report also highlights the competitive landscape by profiling key industry players and their strategic initiatives, offering a holistic view for stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 10.1 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Collins Aerospace (Raytheon Technologies), Safran S. A., Recaro Aircraft Seating GmbH & Co. KG, Geven S.p.A., Aviointeriors S.p.A., Expliseat, HAECO Cabin Solutions, STELIA Aerospace (Airbus), Thompson Aero Seating Ltd., Acro Aircraft Seating, Pitch Aircraft Seating Systems, TSI Aerospace Seats, Iacobucci HF Aerospace, Zim Flugsitz GmbH, Contour Aerospace (Mirus Aircraft Seating), Optimares S.p.A., EAM Worldwide, Botec Engineering GmbH, Mecaero, Encore Air. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The aircraft seating market is segmented to provide a granular understanding of its diverse components and evolving demands across various operational and passenger experience parameters. This segmentation highlights the distinct requirements and growth drivers within each category, enabling manufacturers and airlines to tailor strategies effectively. Analyzing the market through these segments helps in identifying niche opportunities and understanding the specific technological and design innovations prevalent in different aircraft types, cabin classes, and material preferences.

The segmentation allows for a detailed assessment of how factors such as aircraft size, passenger demographics, airline business models, and operational philosophies influence seating choices. For instance, the demand for sophisticated, lightweight composite seats is higher in wide-body and business jet segments, while narrow-body and regional aircraft often prioritize robust, easily maintainable, and space-efficient economy class seats. Understanding these distinctions is crucial for product development, market positioning, and forecasting future trends across the global aircraft seating landscape, ensuring that product offerings align precisely with market needs and regulatory requirements.

- By Aircraft Type:

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional Aircraft

- Business Jets

- By Class:

- Economy Class

- Premium Economy Class

- Business Class

- First Class

- By Material:

- Aluminum Alloys

- Composite Materials

- Other Metals (e.g., Titanium)

- Fabrics (e.g., Wool, Polyester)

- Leather & Synthetic Leather

- Foam & Cushioning Materials

- By Sales Channel:

- Original Equipment Manufacturer (OEM)

- Aftermarket (Maintenance, Repair, and Overhaul (MRO), Retrofit)

- By End User:

- Airlines (Commercial, Cargo)

- Private Owners

- Aircraft Lessors

Regional Highlights

The global aircraft seating market exhibits significant regional variations, each driven by distinct economic, demographic, and aviation industry factors. North America remains a mature yet vital market, characterized by extensive fleet modernization programs, a strong emphasis on domestic travel, and a growing demand for premium cabin experiences. Airlines in this region are investing in retrofitting existing aircraft with lighter, more comfortable, and technologically advanced seats to enhance passenger satisfaction and operational efficiency. The presence of major aircraft manufacturers and a well-established MRO sector further supports market growth and innovation.

Europe mirrors many of North America's trends, with an added focus on sustainability and compliance with strict environmental regulations. The region sees strong demand from both full-service carriers seeking to differentiate through premium offerings and a robust low-cost carrier segment prioritizing durable, lightweight, and cost-effective economy seating. Fleet renewal initiatives and the development of next-generation aircraft also contribute significantly to the market. Innovation in smart seating and modular designs is particularly strong in European manufacturing hubs, catering to diverse airline requirements and passenger expectations.

Asia Pacific (APAC) is projected to be the fastest-growing region, driven by burgeoning air passenger traffic, rapid urbanization, and a burgeoning middle class across countries like China, India, and Southeast Asian nations. This growth fuels massive aircraft orders and fleet expansion by both established and new airlines, creating immense demand for all types of aircraft seating. The region's focus is on capacity expansion, initially prioritizing economy class, but with a rapidly increasing interest in premium and business class offerings as disposable incomes rise. Latin America and the Middle East & Africa (MEA) also present considerable opportunities, fueled by increasing tourism, improved regional connectivity, and strategic investments in aviation infrastructure, leading to consistent demand for new and upgraded seating solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Seating Market.- Collins Aerospace (Raytheon Technologies)

- Safran S. A.

- Recaro Aircraft Seating GmbH & Co. KG

- Geven S.p.A.

- Aviointeriors S.p.A.

- Expliseat

- HAECO Cabin Solutions

- STELIA Aerospace (Airbus)

- Thompson Aero Seating Ltd.

- Acro Aircraft Seating

- Pitch Aircraft Seating Systems

- TSI Aerospace Seats

- Iacobucci HF Aerospace

- Zim Flugsitz GmbH

- Contour Aerospace (Mirus Aircraft Seating)

- Optimares S.p.A.

- EAM Worldwide

- Botec Engineering GmbH

- Mecaero

- Encore Air

Frequently Asked Questions

What is the projected growth rate for the Aircraft Seating Market?

The Aircraft Seating Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, reaching an estimated USD 10.1 Billion by 2033.

What are the primary drivers of growth in the Aircraft Seating Market?

Key drivers include increasing global air passenger traffic, extensive airline fleet expansion and modernization programs, the rising demand for premium cabin segments, and continuous advancements in lightweight materials for improved fuel efficiency.

How is AI impacting the Aircraft Seating industry?

AI is transforming the industry through generative design for optimal seat structures, predictive maintenance of components, automated quality control in manufacturing, and the potential for personalized in-flight passenger experiences.

Which region is expected to dominate the Aircraft Seating Market?

Asia Pacific (APAC) is projected to be the fastest-growing region, driven by significant increases in air passenger traffic, fleet expansion, and economic growth in countries like China and India.

What are the key trends related to sustainability in aircraft seating?

Key sustainability trends include the adoption of eco-friendly and recycled materials, designing for enhanced durability and repairability to extend product life, and optimizing manufacturing processes to reduce waste and energy consumption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted