Automotive Fuel Tank Part Market

Automotive Fuel Tank Part Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708594 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

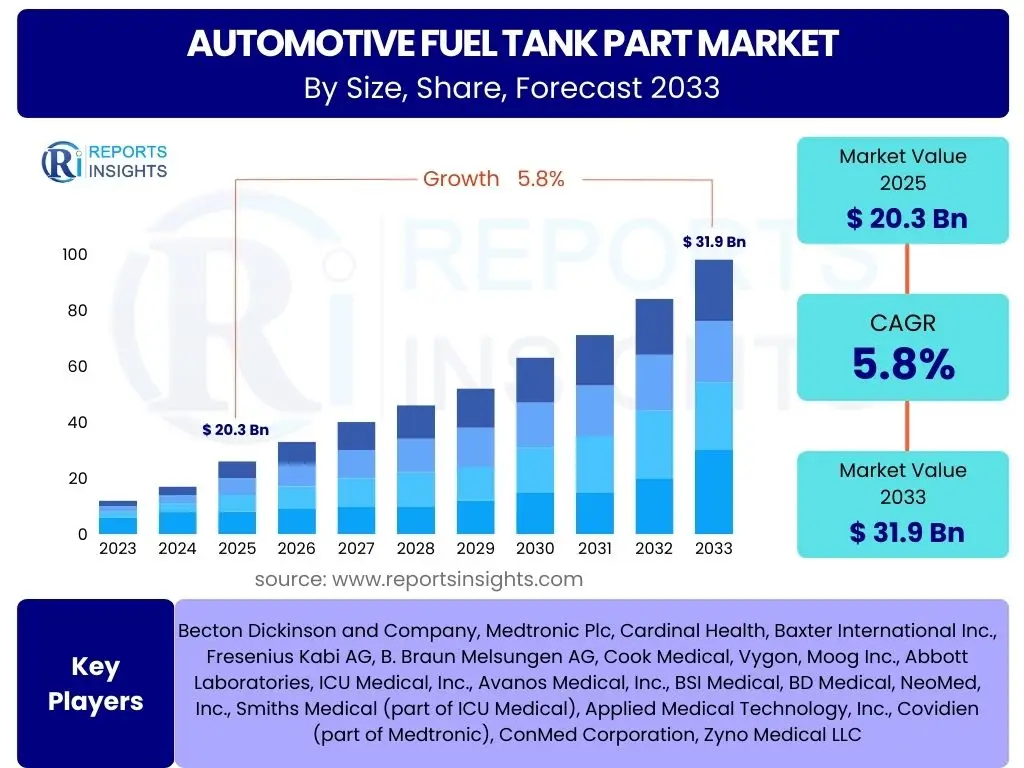

Automotive Fuel Tank Part Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Fuel Tank Part Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 20.3 billion in 2025 and is projected to reach USD 31.9 billion by the end of the forecast period in 2033.

Key Automotive Fuel Tank Part Market Trends & Insights

User inquiries frequently focus on the evolving landscape of materials, design, and regulatory influences impacting the automotive fuel tank part sector. A significant trend involves the increasing adoption of lightweight materials, primarily high-density polyethylene (HDPE) plastics, over traditional steel to enhance fuel efficiency and reduce vehicle emissions. This shift is driven by stringent global environmental regulations and consumer demand for more efficient vehicles. Additionally, advancements in fuel system integration and the development of specialized tanks for hybrid electric vehicles (HEVs) are shaping market dynamics, alongside innovations in manufacturing processes such as blow molding and welding technologies for plastic tanks.

Another crucial insight pertains to the ongoing innovation in fuel tank part design to accommodate advanced fuel types and propulsion systems, even as the automotive industry transitions towards electrification. While electric vehicles reduce demand for traditional fuel tanks, the extensive lifespan of internal combustion engine (ICE) and hybrid vehicles ensures a sustained need for replacement parts and continued development in existing and emerging markets. Furthermore, the market is seeing a focus on enhanced safety features and evaporative emission control systems, necessitating new designs for filler necks, fuel lines, and sensors that comply with stricter environmental standards.

- Lightweighting initiatives through increased adoption of high-density polyethylene (HDPE) plastic tanks.

- Integration of advanced fuel system components and modules for enhanced efficiency and safety.

- Development of specialized fuel tank solutions for hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs).

- Stringent global emission regulations driving innovation in evaporative emission control systems and tank permeability.

- Focus on modular designs and standardization of components to streamline manufacturing and supply chains.

- Growing demand for robust and durable fuel tank parts in emerging automotive markets.

AI Impact Analysis on Automotive Fuel Tank Part

Common user questions regarding AI's impact on the automotive fuel tank part sector revolve around efficiency gains, design optimization, and quality control. Artificial intelligence is increasingly being leveraged in the design phase through generative design, allowing engineers to explore numerous optimal fuel tank shapes and structures that are lighter and more robust, significantly reducing material usage and improving crashworthiness. Predictive analytics powered by AI algorithms can also optimize manufacturing processes, foreseeing potential equipment failures, streamlining production lines, and enhancing overall operational efficiency for complex component fabrication.

Furthermore, AI-driven solutions are transforming quality inspection and supply chain management within the automotive fuel tank part industry. Computer vision and machine learning algorithms enable automated, high-precision inspection of parts for defects, ensuring superior product quality and reducing recall risks. In the supply chain, AI helps in forecasting demand more accurately, optimizing inventory levels, and identifying potential disruptions, leading to a more resilient and cost-effective production and distribution network. The integration of AI thus promises to deliver significant advantages in cost reduction, speed to market, and product innovation.

- Generative design for lightweight and structurally optimized fuel tank geometries, reducing material consumption.

- AI-driven predictive maintenance for manufacturing equipment, minimizing downtime and optimizing production schedules.

- Automated quality inspection using computer vision to detect defects in parts with high accuracy and speed.

- Supply chain optimization through AI-powered demand forecasting and inventory management, enhancing resilience.

- Material science innovation accelerated by AI, identifying new composites and plastics for enhanced performance and sustainability.

- Robotics and automation integration in manufacturing, guided by AI, for precision assembly and welding of complex tank structures.

Key Takeaways Automotive Fuel Tank Part Market Size & Forecast

User queries about key takeaways often seek a succinct understanding of the market's trajectory and the factors underpinning its growth. The primary insight is that despite the accelerating transition to electric vehicles, the automotive fuel tank part market is set for moderate growth driven by the sustained production of hybrid and conventional internal combustion engine vehicles, particularly in developing economies. The emphasis on fuel efficiency, reduced emissions, and enhanced safety standards will continue to spur innovation in material science and manufacturing processes, ensuring a robust demand for advanced fuel tank components throughout the forecast period.

Another critical takeaway highlights the strategic importance of adapting to evolving regulatory frameworks and technological shifts. Manufacturers focusing on flexible, modular designs and developing solutions for alternative fuels or hybrid architectures are best positioned for long-term success. The aftermarket segment will also play a significant role, providing a stable revenue stream as the global vehicle parc of ICE and hybrid vehicles continues to age. Investments in sustainable materials and advanced manufacturing technologies will be crucial for maintaining competitiveness and addressing environmental concerns.

- Steady growth projected, primarily fueled by sustained demand for hybrid and ICE vehicles globally.

- Technological advancements in lightweight plastics and integrated fuel systems are key market enablers.

- Stringent emission regulations are driving innovation in evaporative emission control and fuel tank material permeability.

- Aftermarket segment provides consistent demand for replacement and repair parts.

- Emerging markets, particularly in Asia Pacific and Latin America, will contribute significantly to market expansion.

- Focus on sustainability and recyclability in material choices is becoming increasingly vital for manufacturers.

Automotive Fuel Tank Part Market Drivers Analysis

The automotive fuel tank part market is primarily propelled by the continuous global production of internal combustion engine (ICE) and hybrid electric vehicles (HEVs), which still dominate a significant portion of the automotive landscape. Increasing demand for fuel-efficient vehicles, coupled with stringent emission norms worldwide, necessitates the development and adoption of advanced fuel tank systems that minimize evaporative emissions and optimize fuel delivery. This drives innovation in materials and design, favoring lightweight, durable, and highly integrated components.

Furthermore, the robust aftermarket demand for replacement parts contributes significantly to market growth, ensuring a sustained need for various fuel tank components across the globe. Government initiatives and mandates promoting fuel economy and reduced environmental impact also encourage automotive manufacturers to invest in newer, more efficient fuel tank technologies. The expansion of the automotive sector in emerging economies, characterized by rising disposable incomes and increased vehicle sales, further stimulates the demand for both original equipment and aftermarket fuel tank parts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sustained Production of ICE & Hybrid Vehicles | +2.1% | Global, particularly Asia Pacific, Latin America, MEA | 2025-2033 |

| Increasing Demand for Lightweight & Fuel-Efficient Vehicles | +1.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Stringent Global Emission Regulations (e.g., Euro 7, CAFE standards) | +1.5% | Europe, North America, China | 2025-2030 |

| Robust Aftermarket Demand for Replacement Parts | +0.9% | Global, especially developed markets | 2025-2033 |

| Advancements in Fuel System Integration and Safety Features | +0.7% | Global | 2025-2033 |

Automotive Fuel Tank Part Market Restraints Analysis

A primary restraint on the automotive fuel tank part market is the accelerating global shift towards electric vehicles (EVs), which do not require traditional fuel tanks. This long-term trend poses a significant challenge, as the demand for ICE vehicle components is expected to gradually decline over the coming decades, impacting new vehicle installations. Furthermore, volatility in raw material prices, particularly for plastics (HDPE) and steel, can lead to increased manufacturing costs and put pressure on profit margins for part suppliers, making long-term planning difficult.

The complexity of manufacturing advanced fuel tank systems, particularly those for hybrid vehicles that require intricate designs and multi-layer structures for enhanced safety and emission control, presents another restraint. These complexities often translate to higher production costs and necessitate significant investments in specialized machinery and skilled labor. Additionally, the intensive research and development required to meet ever-tightening emission standards and integrate new technologies can be a substantial burden for smaller manufacturers, limiting market entry and innovation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Shift Towards Electric Vehicles (EVs) | -2.5% | Global, especially Europe, North America, China | 2025-2033 |

| Volatile Raw Material Prices (Plastics, Steel) | -1.2% | Global | 2025-2030 |

| High R&D Costs for New Materials and Advanced Systems | -0.8% | Global | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Instabilities | -0.6% | Global | 2025-2028 |

Automotive Fuel Tank Part Market Opportunities Analysis

Significant opportunities in the automotive fuel tank part market arise from the growing demand for hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs), which still require specialized fuel tanks that can integrate with electric powertrains. These vehicles often necessitate unique tank designs, including saddle tanks or designs that accommodate battery packs, creating new avenues for specialized component manufacturers. Furthermore, the development of sustainable and recycled materials for fuel tank construction presents a burgeoning opportunity to meet environmental targets and appeal to eco-conscious consumers, potentially leading to a competitive advantage.

Another key opportunity lies in the expansion of aftermarket services and parts, particularly in regions with a large and aging fleet of ICE and hybrid vehicles, ensuring a consistent revenue stream for replacement and repair components. Innovations in advanced manufacturing technologies, such as additive manufacturing for prototyping or complex small-batch parts, can also open new doors for efficiency and customization. Moreover, exploring compatibility with alternative fuels like E85 (ethanol blends) or synthetic fuels, which might gain traction in the future, offers potential growth areas for fuel tank part development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Hybrid Electric Vehicles (HEVs/PHEVs) | +1.5% | Global, particularly Europe, North America, Japan | 2025-2033 |

| Development of Sustainable and Recycled Materials | +1.0% | Europe, North America | 2026-2033 |

| Expansion of Aftermarket Services and Parts | +0.8% | Global | 2025-2033 |

| Innovation in Advanced Manufacturing Technologies (e.g., Additive Manufacturing) | +0.6% | Global | 2027-2033 |

Automotive Fuel Tank Part Market Challenges Impact Analysis

The most significant challenge facing the automotive fuel tank part market is the ongoing and accelerated transition of the global automotive industry towards electric vehicles. This fundamental shift necessitates a gradual but inevitable decline in the demand for traditional fuel storage components in new vehicle production over the long term. Manufacturers must strategically adapt their business models and product portfolios to mitigate this existential threat, possibly by diversifying into related fields or focusing heavily on the aftermarket for ICE and hybrid vehicles.

Another critical challenge involves navigating a complex and continuously evolving landscape of global regulatory compliance, particularly concerning evaporative emissions and safety standards. Meeting these stringent requirements often demands substantial investments in research, development, and advanced manufacturing techniques, increasing operational costs and market entry barriers. Intense price competition among existing manufacturers, coupled with pressure from major automotive OEMs to reduce component costs, further compresses profit margins, making it difficult for companies to sustain innovation and growth without significant scale or unique technological advantages.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerating Global Transition to Electric Vehicles | -3.0% | Global | 2025-2033 |

| Complex and Evolving Regulatory Compliance | -1.0% | Europe, North America, China | 2025-2030 |

| Intense Price Competition and Cost Pressures from OEMs | -0.7% | Global | 2025-2033 |

| Global Supply Chain Volatility and Material Scarcity | -0.5% | Global | 2025-2028 |

Automotive Fuel Tank Part Market - Updated Report Scope

This report provides a comprehensive analysis of the global automotive fuel tank part market, encompassing detailed market sizing, trends, drivers, restraints, opportunities, and challenges. It offers in-depth insights into market segmentation by material, vehicle type, and component, alongside a thorough regional analysis. The scope includes an examination of the competitive landscape, profiling key industry players and their strategic initiatives, to deliver actionable intelligence for stakeholders navigating this evolving automotive segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.3 Billion |

| Market Forecast in 2033 | USD 31.9 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TI Fluid Systems, Kautex Textron (A Textron Company), Yachiyo Industry Co., Ltd., Magna International Inc., Compagnie Plastic Omnium SE, YAPP Automotive Parts Co., Ltd., Spectra Premium Industries Inc., Futaba Industrial Co., Ltd., LyondellBasell Industries N.V., BASF SE, SMP Automotive Systems, Unipres Corporation, Posco, Nippon Steel Corporation, Toyota Boshoku Corporation, Continental AG, Robert Bosch GmbH, Denso Corporation, Aisin Corporation, Visteon Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive fuel tank part market is meticulously segmented to provide a granular understanding of its diverse components and applications. Segmentation by material is critical, differentiating between traditional steel tanks and the increasingly dominant high-density polyethylene (HDPE) plastic tanks, along with niche applications of aluminum and composite materials. This distinction highlights material innovation driven by lightweighting and cost-efficiency goals. Further segmentation by vehicle type, encompassing passenger cars and various commercial vehicles, allows for an assessment of demand patterns across different automotive categories, recognizing distinct requirements for fuel tank capacity and durability.

Additional segmentation factors, such as fuel tank capacity (below 45 liters, 45-75 liters, and above 75 liters), offer insights into trends related to vehicle size and usage. Crucially, the market is also segmented by specific components, including the tank shell, filler neck, fuel pump module, sending units, fuel lines, straps, gaskets, and sensors, reflecting the intricate ecosystem of parts that constitute a complete fuel system. Finally, the distinction between OEM (Original Equipment Manufacturer) and aftermarket sales channels provides a clear view of market dynamics in new vehicle assembly versus replacement and repair markets, which have different demand drivers and competitive landscapes.

- By Material:

- Steel: Traditional material, still used for heavy-duty vehicles and specific applications, known for strength.

- Plastic (HDPE): Dominant material due to lightweight properties, corrosion resistance, and design flexibility, especially for passenger cars.

- Aluminum: Used in some premium or specialized vehicles for lightweighting and corrosion resistance.

- Composites: Emerging for ultra-lightweight and complex shapes, albeit with higher costs.

- By Vehicle Type:

- Passenger Cars: Highest volume segment, largely transitioning to plastic tanks for efficiency.

- Commercial Vehicles (LCV, HCV): Requires larger, more robust tanks, often steel or heavy-duty plastic, with a focus on durability.

- By Capacity:

- Below 45 Liters: Typically for compact cars and smaller passenger vehicles.

- 45-75 Liters: Common for mid-size sedans and SUVs.

- Above 75 Liters: Primarily for larger SUVs, trucks, and commercial vehicles.

- By Component:

- Fuel Tank Shell: The primary storage unit.

- Filler Neck: Component connecting the fuel tank to the outside for refueling.

- Fuel Pump Module: Integrated unit often including pump, filter, and level sensor.

- Sending Units: Measures fuel level and sends data to the gauge.

- Fuel Lines: Conduits for transporting fuel.

- Straps: Secure the fuel tank to the vehicle chassis.

- Gaskets & Seals: Prevent leaks and ensure system integrity.

- Sensors: Monitor various parameters like pressure and temperature.

- Others: Includes valves, baffles, and other small fittings.

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Sales to vehicle manufacturers for new vehicle assembly.

- Aftermarket: Sales of replacement parts for repair and maintenance of existing vehicles.

Regional Highlights

- Asia Pacific: This region dominates the automotive fuel tank part market, primarily due to the large-scale production and sales of passenger cars and commercial vehicles in countries like China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and the continuous expansion of the automotive manufacturing base contribute to significant OEM and aftermarket demand. The region is also a hub for innovation in cost-effective manufacturing processes and lightweight materials.

- Europe: Characterized by stringent emission regulations and a strong focus on advanced vehicle technologies, Europe is a key market for innovative fuel tank part solutions, particularly for hybrid vehicles and those utilizing advanced evaporative emission control systems. Germany, France, and the UK are major contributors, driving demand for high-performance and environmentally compliant components. The aftermarket is also robust due to a large existing vehicle fleet.

- North America: The market in North America is driven by substantial demand for SUVs, light trucks, and commercial vehicles, often requiring larger capacity and durable fuel tank parts. The region is also an early adopter of advanced fuel efficiency standards and hybrid technologies, pushing manufacturers towards innovative materials and integrated fuel systems. The US and Canada represent significant aftermarket potential.

- Latin America: This region is experiencing steady growth in the automotive sector, leading to increased demand for both new vehicles and aftermarket parts. Brazil and Mexico are key markets with growing production capabilities, focusing on cost-effective and reliable fuel tank solutions for a diverse range of vehicles. Economic stability and growing consumer base contribute to market expansion.

- Middle East and Africa (MEA): The MEA region is a growing market, particularly in countries with developing automotive industries and high demand for affordable vehicles. Investment in infrastructure and increasing vehicle ownership contribute to demand for fuel tank parts, with a strong emphasis on durability and performance in varying environmental conditions. The aftermarket segment is also gaining traction.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Fuel Tank Part Market.- TI Fluid Systems

- Kautex Textron (A Textron Company)

- Yachiyo Industry Co., Ltd.

- Magna International Inc.

- Compagnie Plastic Omnium SE

- YAPP Automotive Parts Co., Ltd.

- Spectra Premium Industries Inc.

- Futaba Industrial Co., Ltd.

- LyondellBasell Industries N.V.

- BASF SE

- SMP Automotive Systems

- Unipres Corporation

- Posco

- Nippon Steel Corporation

- Toyota Boshoku Corporation

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Aisin Corporation

- Visteon Corporation

Frequently Asked Questions

What is the projected growth rate for the Automotive Fuel Tank Part Market?

The Automotive Fuel Tank Part Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 31.9 billion by 2033.

How is the rise of electric vehicles impacting the fuel tank part market?

While the long-term shift to EVs poses a restraint, the market is sustained by continued production of hybrid and conventional ICE vehicles, alongside robust aftermarket demand. Manufacturers are adapting by innovating for hybrid solutions and focusing on lighter, more efficient components.

What are the key materials used in automotive fuel tank parts?

The primary materials are high-density polyethylene (HDPE) plastic for its lightweight and design flexibility, and steel for durability, especially in commercial vehicles. Aluminum and composites are also used in specialized applications.

Which region holds the largest share in the Automotive Fuel Tank Part Market?

Asia Pacific currently dominates the automotive fuel tank part market due to high vehicle production volumes, expanding automotive manufacturing bases, and growing demand in countries like China, India, and Japan.

What role do emission regulations play in the market?

Stringent global emission regulations are a significant driver, compelling manufacturers to develop advanced fuel tank systems that reduce evaporative emissions, enhance fuel efficiency, and ensure compliance with environmental standards, thereby fostering innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted