Automotive Film Market

Automotive Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708887 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

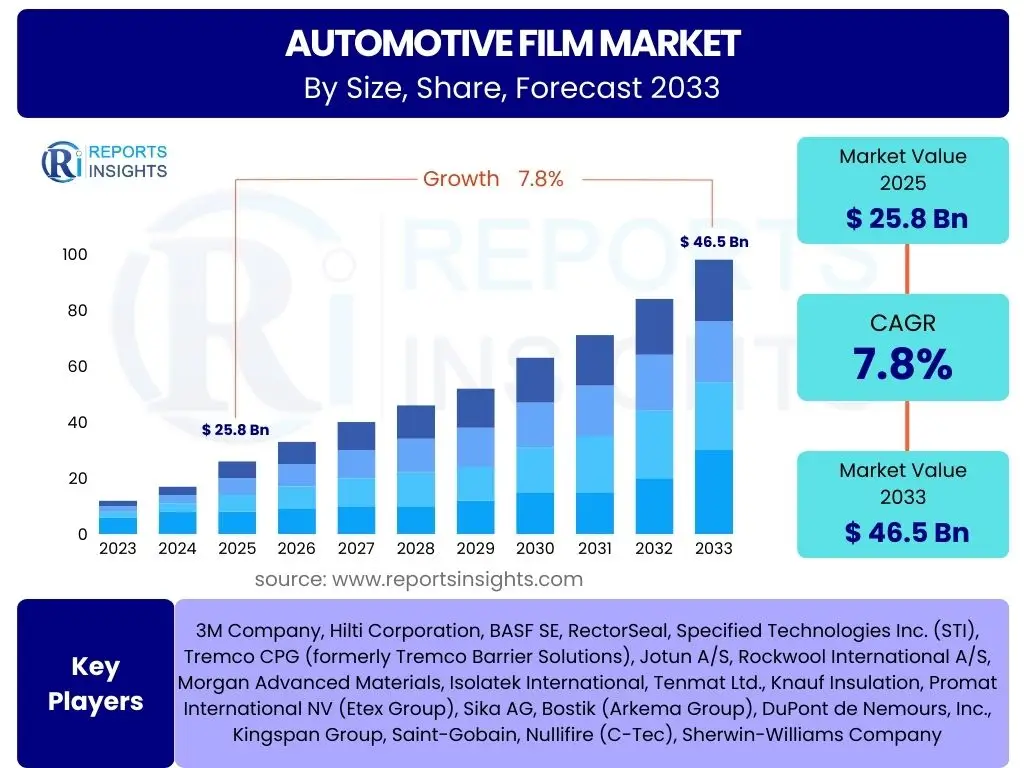

Automotive Film Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 25.8 Billion in 2025 and is projected to reach USD 46.5 Billion by the end of the forecast period in 2033.

Key Automotive Film Market Trends & Insights

The automotive film market is witnessing a transformative period, driven by evolving consumer preferences for vehicle aesthetics and protection, coupled with advancements in material science. Users frequently inquire about the latest innovations, how environmental concerns are shaping product development, and the integration of smart technologies. The market is increasingly focused on high-performance films offering multi-functional benefits, from enhanced durability and solar control to privacy and anti-graffiti properties. This shift reflects a broader industry movement towards value-added products that cater to both luxury and mass-market segments.

Furthermore, the rapid expansion of the electric vehicle (EV) sector is creating new avenues for specialized film applications, particularly in thermal management and interior cabin comfort. There is a growing demand for films that can adapt to unique EV designs and energy efficiency requirements. Concurrently, the aftermarket segment continues to thrive, fueled by personalization trends and a desire among vehicle owners to preserve their assets. These dynamics highlight a market that is not only expanding in volume but also diversifying in terms of product offerings and technological sophistication.

- Growing adoption of Paint Protection Films (PPF) for enhanced vehicle longevity and resale value.

- Rising demand for ceramic and carbon window films offering superior heat rejection and UV protection.

- Development of smart films with switchable privacy or augmented reality features.

- Increasing preference for sustainable and eco-friendly film materials.

- Customization trends driving the market for vehicle wraps and graphic films.

- Integration of advanced functional films for electric vehicles, focusing on thermal regulation and cabin comfort.

AI Impact Analysis on Automotive Film

The integration of Artificial Intelligence (AI) is beginning to profoundly influence various stages of the automotive film market, from product development to customer experience. Common user questions revolve around how AI can enhance film properties, streamline manufacturing processes, and personalize consumer choices. AI-driven analytics can optimize material formulations for desired characteristics such as durability, UV resistance, and optical clarity, leading to more efficient R&D cycles and superior product performance. Furthermore, AI algorithms can predict market trends and consumer preferences with greater accuracy, enabling manufacturers to tailor their offerings to emerging demands, thus reducing waste and increasing responsiveness.

In manufacturing, AI is revolutionizing quality control and operational efficiency. Machine vision systems powered by AI can detect microscopic flaws in film production in real-time, ensuring higher quality outputs and minimizing costly recalls. Predictive maintenance for manufacturing equipment, also enabled by AI, reduces downtime and extends the lifespan of machinery, contributing to cost savings and increased production capacity. On the consumer front, AI could potentially assist in virtual film simulations, allowing customers to visualize different film types and tints on their specific vehicle models before purchase, thereby enhancing the buying experience and reducing decision-making friction.

- Optimized material R&D: AI algorithms accelerate the discovery and formulation of new film compositions with enhanced properties.

- Predictive analytics for market trends: AI helps forecast consumer demand and design preferences, guiding product development and inventory management.

- Enhanced manufacturing quality control: AI-powered vision systems detect defects during film production, ensuring consistent quality and reducing waste.

- Streamlined supply chain management: AI optimizes logistics, inventory, and distribution, improving efficiency and reducing operational costs.

- Personalized customer experience: AI-driven tools may offer virtual simulations and recommendations for film selection based on individual vehicle and aesthetic preferences.

Key Takeaways Automotive Film Market Size & Forecast

Analysis of the automotive film market size and forecast reveals a robust growth trajectory, underscoring significant opportunities for innovation and expansion. Users frequently seek to understand the primary factors driving this growth and the core implications for stakeholders. The market's projected value exceeding USD 46.5 Billion by 2033 highlights an escalating consumer appreciation for both aesthetic enhancement and functional protection of vehicles. This growth is not merely volumetric but indicative of a deeper shift towards premium and technologically advanced film solutions.

The sustained Compound Annual Growth Rate (CAGR) of 7.8% signifies a resilient market, propelled by increasing automotive production, a burgeoning aftermarket, and continuous advancements in film technologies. A critical insight is the bifurcation of growth, with strong demand emanating from both original equipment manufacturers (OEMs) integrating films during vehicle assembly and the vibrant aftermarket segment catering to customization and protection needs. This dual growth engine, coupled with increasing environmental and safety regulations, positions the automotive film market as a dynamic and strategically important sector within the broader automotive industry.

- Significant market expansion: The market is poised for substantial growth, nearly doubling its value by 2033.

- Driven by dual demand: Both OEM integration and aftermarket customization are key growth contributors.

- Technological innovation is crucial: Advanced films offering multi-functional benefits are gaining traction.

- Emerging markets offer high potential: Rapid vehicle ownership growth in developing regions will fuel demand.

- Sustainability and performance are paramount: Films with eco-friendly attributes and superior protective qualities will lead the market.

Automotive Film Market Drivers Analysis

The automotive film market's expansion is fundamentally driven by a confluence of factors, prominently including the escalating global automotive production and sales figures, which directly correlate with the demand for both factory-installed and aftermarket film solutions. Consumers are increasingly aware of the long-term benefits of protecting their vehicle's paintwork and interiors from environmental damage, leading to a surge in demand for products like Paint Protection Films (PPF) and high-performance window tints. This protective aspect is complemented by a strong desire for vehicle personalization and aesthetic enhancement, where films offer a versatile and cost-effective solution compared to traditional painting or modifications.

Technological advancements also play a crucial role, with manufacturers continuously innovating to produce films that offer superior performance characteristics, such as self-healing properties, enhanced UV and IR rejection, and improved durability. Furthermore, evolving regulatory landscapes in various regions, particularly concerning vehicle safety and energy efficiency, indirectly boost the market for films that can contribute to these goals. For instance, solar control films help reduce cabin temperatures, decreasing the reliance on air conditioning and improving fuel efficiency, aligning with environmental regulations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Automotive Production and Sales | +1.2% | Asia Pacific, North America, Europe | Short to Mid-term |

| Growing Consumer Awareness of Vehicle Protection & Aesthetics | +1.0% | Global | Mid to Long-term |

| Technological Advancements in Film Manufacturing | +0.8% | North America, Europe, Asia Pacific | Mid to Long-term |

| Rising Demand for Energy-Efficient & UV-Protective Solutions | +0.7% | Europe, North America, Middle East | Mid-term |

Automotive Film Market Restraints Analysis

Despite robust growth drivers, the automotive film market faces several significant restraints that could impede its full potential. One primary challenge is the relatively high upfront cost associated with premium film products, particularly advanced Paint Protection Films (PPF) and high-performance window tints. This cost can be a deterrent for budget-conscious consumers, especially in price-sensitive emerging markets. Additionally, the installation of these films often requires specialized skills and equipment, leading to higher labor costs and potentially limiting the widespread availability of professional installation services, thereby creating a barrier to market entry for some consumers.

Another restraint stems from the complex and often varying regulatory landscape concerning window tinting across different regions and countries. Strict laws regarding visible light transmission (VLT) percentages can limit product applicability and confuse consumers, leading to compliance issues or reluctance to invest in certain film types. Furthermore, the presence of counterfeit products and low-quality alternatives in the market poses a threat to reputable manufacturers. These inferior products not only damage consumer trust but also undercut genuine product pricing, affecting market integrity and profit margins for quality providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Installation Cost of Premium Films | -0.9% | Global, particularly Emerging Markets | Mid-term |

| Complex & Varied Regulatory Landscape for Window Tinting | -0.6% | North America, Europe, Asia Pacific | Ongoing |

| Presence of Low-Quality & Counterfeit Products | -0.5% | Asia Pacific, Latin America, MEA | Long-term |

| Availability of Alternative Protection Solutions (e.g., Ceramic Coatings) | -0.4% | North America, Europe | Mid-term |

Automotive Film Market Opportunities Analysis

The automotive film market is ripe with opportunities for innovation and expansion, particularly driven by emerging technological trends and evolving consumer demographics. The rapid global shift towards electric vehicles (EVs) presents a significant untapped market, as EVs have unique requirements for thermal management and battery cooling, which specialized films can address. These films can enhance energy efficiency, extend battery range, and improve cabin comfort, creating a niche for high-performance thermal films tailored specifically for the EV segment. This shift mandates novel film solutions that differ from those traditionally used in internal combustion engine (ICE) vehicles.

Furthermore, the growing demand for customization and personalization among vehicle owners, particularly younger demographics, offers a substantial opportunity for aesthetic films such as vehicle wraps and interior decorative films. These products allow individuals to express their style and update their vehicle's appearance without permanent modifications. Additionally, expanding into developing economies, where vehicle ownership is rapidly increasing, represents a fertile ground for market penetration. As these markets mature, so too will the demand for vehicle protection and enhancement, creating a long-term growth trajectory for film manufacturers and installers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Market & Related Film Needs | +1.5% | Global, particularly Europe, Asia Pacific, North America | Long-term |

| Increasing Demand for Vehicle Customization & Personalization | +1.0% | North America, Europe, Asia Pacific | Mid to Long-term |

| Expansion into Developing Economies with Rising Vehicle Ownership | +0.9% | Asia Pacific, Latin America, MEA | Long-term |

| Innovation in Functional Films (e.g., Self-Healing, Smart Films) | +0.8% | North America, Europe, Japan | Mid to Long-term |

Automotive Film Market Challenges Impact Analysis

The automotive film market navigates a landscape punctuated by several inherent challenges that demand strategic responses from industry players. Intense competition from a multitude of regional and international manufacturers often leads to price wars, eroding profit margins and making it difficult for new entrants to establish a foothold. This competitive pressure also necessitates continuous investment in research and development to maintain a technological edge and differentiate products in a crowded market. The rapid pace of technological advancements, while an opportunity, also poses a challenge as companies must constantly adapt and innovate to avoid product obsolescence and meet evolving consumer expectations.

Furthermore, the market is highly susceptible to the volatility of raw material prices, particularly for polymers and adhesives, which can directly impact production costs and final product pricing. Supply chain disruptions, exacerbated by geopolitical events or natural disasters, further complicate material procurement and can lead to production delays. Another significant challenge is the shortage of skilled labor required for precise and high-quality film installation. Improper application can lead to customer dissatisfaction and damage the brand's reputation, highlighting the critical need for continuous training and certification programs within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure | -0.8% | Global | Ongoing |

| Volatility of Raw Material Prices | -0.7% | Global | Short to Mid-term |

| Shortage of Skilled Labor for Installation | -0.6% | North America, Europe, Australia | Long-term |

| Maintaining Product Quality and Authenticity | -0.5% | Global | Ongoing |

Automotive Film Market - Updated Report Scope

This report provides an in-depth analysis of the global automotive film market, encompassing comprehensive insights into market dynamics, segmentation, regional outlook, and competitive landscape. The scope includes a detailed examination of current market trends, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory. Utilizing a robust research methodology, the report offers quantitative and qualitative assessments to forecast market performance and identify strategic imperatives for stakeholders. It aims to empower businesses with actionable intelligence to navigate the complexities and capitalize on the growth avenues within this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.8 Billion |

| Market Forecast in 2033 | USD 46.5 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Company A, Company B, Company C, Company D, Company E, Company F, Company G, Company H, Company I, Company J, Company K, Company L, Company M, Company N, Company O, Company P, Company Q, Company R, Company S, Company T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive film market is meticulously segmented to provide a granular understanding of its diverse components and growth dynamics. These segments are categorized based on film type, material composition, application in various vehicle types, and end-use, allowing for precise market sizing and forecasting across distinct product categories and consumer bases. Understanding these segmentations is critical for businesses to tailor their product offerings, marketing strategies, and distribution channels to specific market niches, ensuring optimal resource allocation and competitive advantage. Each segment demonstrates unique growth drivers and market potential, influenced by technological advancements, regulatory frameworks, and evolving consumer preferences.

For instance, the segmentation by film type clearly delineates the demand for protective films like PPF versus aesthetic solutions like vehicle wraps, each catering to different consumer priorities. Similarly, the distinction between OEM and aftermarket applications highlights the two primary sales channels and their respective market sizes. Material-based segmentation, such as ceramic versus carbon films, helps differentiate products based on their performance characteristics and price points. This comprehensive segmentation framework is essential for detailed market analysis and strategic planning within the automotive film industry.

- By Film Type: Window Films (Tint, Safety & Security, Solar Control), Paint Protection Films (PPF - Clear, Matte, Colored), Vehicle Wrap Films (Cast, Calendered), Decorative & Specialty Films.

- By Material: Ceramic, Carbon, Metallized, Dyed, Hybrid, Polyurethane (TPU), Polyvinyl Chloride (PVC).

- By Application: Passenger Vehicles (Sedans, SUVs, Hatchbacks, Luxury Cars), Commercial Vehicles (LCVs, HCVs, Buses & Coaches).

- By End-use: OEM (Original Equipment Manufacturer), Aftermarket.

- By Vehicle Type: Internal Combustion Engine (ICE) Vehicles, Electric Vehicles (EVs).

Regional Highlights

- North America: This region is characterized by a strong aftermarket demand for vehicle customization and protection, particularly for high-end luxury vehicles and SUVs. Stringent safety regulations and a high consumer awareness regarding UV protection and paint preservation further bolster market growth. Technological adoption and a preference for premium film solutions also contribute to its significant market share.

- Europe: The European market is driven by increasing environmental regulations promoting energy efficiency, leading to a higher adoption of solar control films. A strong luxury automotive segment and a growing trend towards vehicle personalization, alongside robust OEM integration, are key factors. Regional variations in tinting laws can, however, present localized challenges.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, propelled by rapidly increasing vehicle production and sales, especially in countries like China, India, and Japan. Rising disposable incomes, urbanization, and a growing middle class are fueling demand for both new vehicles and aftermarket accessories, including protective and aesthetic films. The region also serves as a major manufacturing hub for automotive films.

- Latin America: The market in Latin America is witnessing steady growth, largely due to increasing vehicle ownership and a rising interest in vehicle protection against harsh climates and road conditions. Economic development and an expanding automotive industry, particularly in countries like Brazil and Mexico, are creating new opportunities for film manufacturers.

- Middle East and Africa (MEA): The MEA region exhibits significant potential, primarily driven by extreme climatic conditions that necessitate effective solar control and protective films. High demand for luxury vehicles and a growing aftermarket segment, particularly in Gulf countries, contribute to market expansion. Economic diversification efforts are also supporting industrial growth in the automotive sector.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Film Market.- 3M Company

- Eastman Chemical Company

- Saint-Gobain S.A.

- Avery Dennison Corporation

- Madico Inc.

- LLumar

- XPEL Inc.

- Hanita Coatings RCA Ltd. (a unit of Raven Industries)

- Solar Gard (a subsidiary of Saint-Gobain)

- SunTek Films (an Eastman Company)

- Johnson Window Films Inc.

- Autozkin

- KDX Window Film

- Ziebart International Corporation

- Hexis S.A.

- Global Window Films

- Nexfil

- Garware Hi-Tech Films Ltd.

- Sharptop Films

- Concordia Manufacturing Co. Ltd.

Frequently Asked Questions

What is automotive film and what are its primary uses?

Automotive film refers to thin, adhesive-backed layers applied to vehicle surfaces, primarily windows and paintwork. Its primary uses include enhancing vehicle aesthetics, protecting paint from scratches, chips, and environmental damage, and improving passenger comfort and safety through solar control, UV rejection, and shatter resistance.

What are the different types of automotive films available in the market?

The market offers several types of automotive films: window films (tint, safety and security, solar control), paint protection films (PPF) for paint safeguarding, and vehicle wrap films for aesthetic customization and branding. These categories further branch into materials like ceramic, carbon, metallized, and hybrid, each offering distinct performance benefits.

How do automotive films contribute to vehicle protection and resale value?

Automotive films, particularly Paint Protection Films (PPF), form a robust barrier against road debris, stone chips, scratches, and environmental contaminants like bird droppings and bug splatters. Window films protect interiors from harmful UV rays, preventing fading and cracking. By preserving the original finish and interior condition, films significantly reduce wear and tear, thereby maintaining the vehicle's aesthetic appeal and maximizing its potential resale value.

What is the expected lifespan of automotive films, and how is it maintained?

The lifespan of automotive films varies by type and quality, typically ranging from 3 to 10 years for window films and 5 to 10 years or more for high-quality Paint Protection Films (PPF). Proper maintenance involves regular cleaning with non-abrasive cleaners, avoiding harsh chemicals, and ensuring professional installation. Adhering to manufacturer guidelines helps maximize durability and performance.

Are there any legal restrictions or regulations regarding automotive window tinting?

Yes, legal restrictions on automotive window tinting vary significantly by country, state, or even local jurisdiction. These regulations primarily focus on Visible Light Transmission (VLT) percentages, dictating how much light must pass through the tinted windows. It is crucial for vehicle owners to research and comply with local laws to avoid fines or vehicle inspection failures, as non-compliance can lead to legal penalties.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted