Automotive Electric Motor for Electric Vehicle Market

Automotive Electric Motor for Electric Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708484 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Electric Motor for Electric Vehicle Market Size

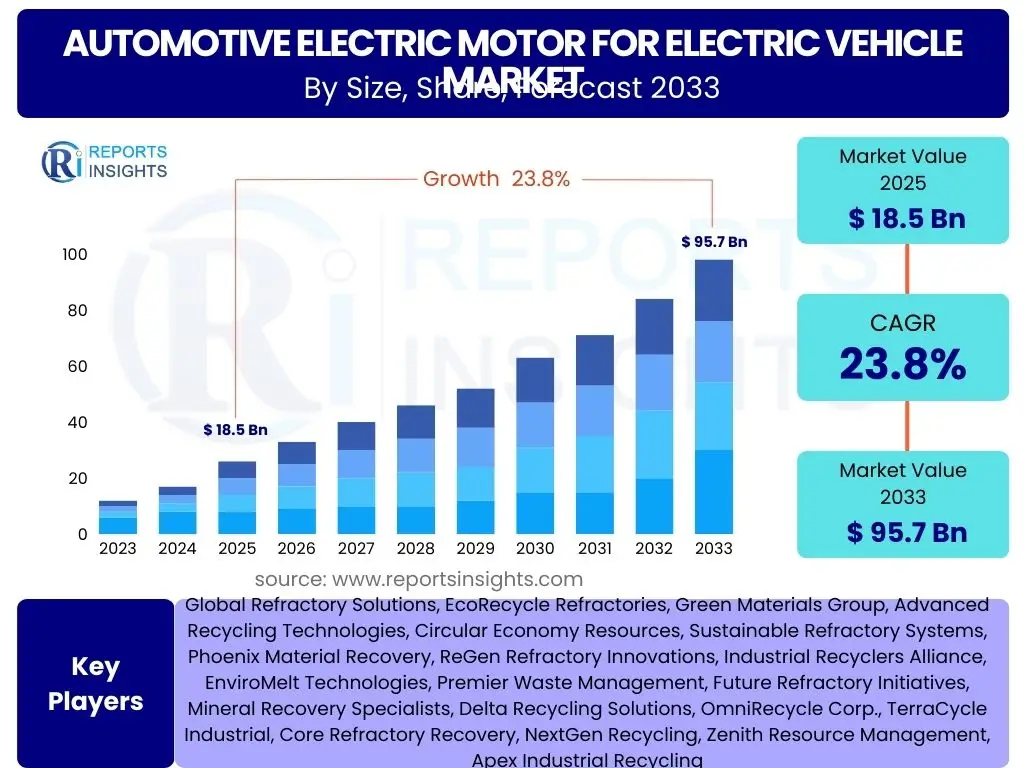

According to Reports Insights Consulting Pvt Ltd, The Automotive Electric Motor for Electric Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 95.7 Billion by the end of the forecast period in 2033.

Key Automotive Electric Motor for Electric Vehicle Market Trends & Insights

The Automotive Electric Motor for Electric Vehicle market is experiencing rapid evolution driven by technological advancements, evolving consumer preferences, and stringent environmental regulations. Key trends indicate a shift towards higher efficiency, greater power density, and more compact motor designs, directly impacting vehicle performance and range. Furthermore, the integration of advanced materials and manufacturing techniques is enhancing the durability and reducing the overall cost of these critical components, making EVs more accessible to a broader consumer base.

Market insights suggest a growing demand for permanent magnet synchronous motors (PMSMs) due to their superior efficiency and power output, alongside increasing research into alternative motor types like axial flux motors for improved compactness and torque. The trend towards vertical integration within the automotive supply chain, where OEMs develop in-house motor capabilities, is also reshaping market dynamics. Additionally, the focus on sustainable production practices and the lifecycle management of materials used in electric motors are gaining prominence, reflecting broader industry commitments to environmental stewardship.

- Growing adoption of Permanent Magnet Synchronous Motors (PMSM) for higher efficiency.

- Emergence of Axial Flux Motors for compact design and superior torque density.

- Increased focus on integrated motor, inverter, and gearbox (e-axle) solutions.

- Advancements in power electronics, particularly Silicon Carbide (SiC) inverters, enhancing motor performance.

- Development of rare-earth-free motors to reduce dependency on critical minerals and address supply chain vulnerabilities.

- Emphasis on lightweight materials and advanced manufacturing techniques (e.g., additive manufacturing) for motor components.

- Expansion of charging infrastructure and government incentives accelerating EV adoption, directly driving motor demand.

AI Impact Analysis on Automotive Electric Motor for Electric Vehicle

Artificial intelligence is profoundly influencing the design, manufacturing, and operational aspects of automotive electric motors, addressing common user inquiries regarding performance optimization, cost reduction, and reliability. Users are keen to understand how AI can lead to more efficient, durable, and affordable motors. AI-driven generative design tools are enabling engineers to explore vast design spaces, optimizing motor topologies for maximum efficiency, power density, and thermal management far beyond what traditional methods can achieve. This capability helps in identifying innovative material combinations and structural layouts that were previously unfeasible.

Furthermore, AI plays a crucial role in predictive maintenance and quality control during manufacturing. Machine learning algorithms analyze sensor data from motors in real-time to predict potential failures, allowing for proactive maintenance and preventing costly downtime. In the manufacturing process, AI-powered vision systems detect microscopic defects and optimize assembly line parameters, ensuring higher quality and consistency. For the end-user, AI integration can lead to smarter energy management within the vehicle, optimizing motor operation based on driving conditions, battery state, and external factors, thereby extending range and battery life, which are key consumer concerns.

- AI-driven generative design for optimizing motor geometry, material selection, and thermal management.

- Predictive maintenance analytics using machine learning to forecast motor component failures.

- Enhanced manufacturing process control and quality assurance through AI-powered vision systems and robotics.

- Optimization of motor control units and energy management systems for improved efficiency and range.

- Development of smart diagnostics for real-time performance monitoring and fault detection.

- AI-assisted material discovery for novel magnetic and structural components.

Key Takeaways Automotive Electric Motor for Electric Vehicle Market Size & Forecast

The Automotive Electric Motor for Electric Vehicle market is poised for substantial and sustained growth, driven by an accelerating global transition to electric mobility. The forecast indicates a robust expansion, making it a pivotal sector for automotive suppliers, technology developers, and investors. The primary takeaway is the undeniable shift towards electrification, which mandates continuous innovation in motor technology to meet increasing demands for performance, efficiency, and cost-effectiveness. This growth is not merely incremental but represents a fundamental reshaping of the automotive powertrain landscape.

Strategic stakeholders must recognize the critical importance of investing in research and development, particularly in areas like advanced material science, power electronics, and AI-driven design methodologies, to remain competitive. Furthermore, market participants should anticipate evolving regulatory environments and consumer expectations, which will continue to push the boundaries of electric motor capabilities. The market's significant projected value by 2033 underscores the immense opportunities available for companies that can effectively innovate, scale production, and navigate the complexities of the global EV supply chain.

- Significant market expansion expected, reaching nearly USD 96 billion by 2033, driven by global EV adoption.

- Technological innovation in motor design and materials is crucial for competitive advantage and market leadership.

- Strong governmental support and environmental regulations globally act as key accelerators for market growth.

- Supply chain resilience, particularly for rare-earth metals and semiconductors, remains a critical strategic consideration.

- Integration of advanced software and AI into motor control and manufacturing processes is becoming a standard.

- Emerging markets present substantial growth opportunities as EV infrastructure and adoption expand.

Automotive Electric Motor for Electric Vehicle Market Drivers Analysis

The Automotive Electric Motor for Electric Vehicle market is fundamentally propelled by a confluence of environmental imperatives, governmental policies, and technological advancements. The global push to reduce carbon emissions and combat climate change has led to increasingly stringent fuel efficiency and emission standards for vehicles, making electric propulsion a highly attractive solution. Governments worldwide are actively supporting the transition to EVs through various incentives, subsidies, and infrastructure investments, creating a fertile ground for market expansion. This regulatory and policy framework serves as a foundational driver, compelling both manufacturers and consumers towards electric vehicles and, consequently, their core electric motors.

Concurrently, the continuous decline in battery costs and improvements in energy density have significantly enhanced the affordability and practicality of electric vehicles, directly impacting the demand for electric motors. As battery technology advances, the range anxiety associated with EVs diminishes, making them more appealing to a broader consumer base. Furthermore, advancements in motor technology itself, such as higher power density, improved efficiency, and reduced noise, vibration, and harshness (NVH) levels, contribute to a superior driving experience, further accelerating consumer adoption. These interconnected factors collectively act as powerful drivers, ensuring robust and sustained growth in the automotive electric motor market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations & Government Incentives | +7.5% | Europe, China, North America | Short to Mid-term (2025-2030) |

| Declining Battery Costs & Improved Energy Density | +6.2% | Global | Mid to Long-term (2025-2033) |

| Increasing Consumer Awareness & Demand for EVs | +5.8% | Global, particularly developed economies | Short to Mid-term (2025-2030) |

| Technological Advancements in Motor Design & Materials | +4.9% | Global | Long-term (2028-2033) |

| Expansion of EV Charging Infrastructure | +4.1% | China, Europe, North America, India | Mid-term (2026-2031) |

| Growth in Commercial Electric Vehicle Segment | +3.5% | Europe, North America, Asia Pacific | Mid to Long-term (2027-2033) |

| Strategic Investments & Partnerships by OEMs | +3.0% | Global | Short to Mid-term (2025-2030) |

Automotive Electric Motor for Electric Vehicle Market Restraints Analysis

Despite the robust growth trajectory, the Automotive Electric Motor for Electric Vehicle market faces several significant restraints that could temper its expansion. One primary concern is the relatively high initial purchase cost of electric vehicles compared to their internal combustion engine counterparts, which can deter price-sensitive consumers. This cost is intrinsically linked to the components, including the electric motor and the battery pack, making it a critical barrier to widespread adoption in certain demographics and regions. Furthermore, the limited availability and slow deployment of comprehensive charging infrastructure, particularly in rural areas and emerging economies, contribute to range anxiety among potential EV buyers, posing a substantial challenge to market penetration.

Another notable restraint involves the geopolitical and supply chain risks associated with critical raw materials, such as rare-earth elements (e.g., Neodymium, Dysprosium) used in permanent magnet motors. Volatility in the prices and availability of these materials can lead to increased manufacturing costs and production delays, impacting the overall market stability and growth. Additionally, the nascent stage of recycling infrastructure for electric vehicle components, including motors and batteries, presents environmental and economic challenges related to end-of-life management. These combined factors necessitate strategic responses from industry players and policymakers to mitigate their negative impact on the market's long-term potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Electric Vehicles | -5.8% | Emerging Markets, Price-Sensitive Regions | Short to Mid-term (2025-2029) |

| Limited Charging Infrastructure Availability | -4.5% | Global, particularly rural areas | Short to Mid-term (2025-2030) |

| Supply Chain Volatility of Critical Raw Materials (e.g., Rare Earths) | -4.0% | Global | Mid-term (2026-2031) |

| Range Anxiety Among Consumers | -3.2% | Global | Short to Mid-term (2025-2028) |

| Grid Strain and Power Supply Challenges in Some Regions | -2.8% | Specific Developing Countries, Heavily Populated Urban Centers | Mid to Long-term (2028-2033) |

| Lack of Standardization in Charging Technologies | -2.0% | North America, Europe | Short-term (2025-2027) |

Automotive Electric Motor for Electric Vehicle Market Opportunities Analysis

The Automotive Electric Motor for Electric Vehicle market is rich with transformative opportunities driven by continuous technological evolution and expanding market horizons. One significant opportunity lies in the ongoing research and development of advanced motor technologies, such as axial flux motors and rare-earth-free designs. These innovations promise to deliver higher power density, increased efficiency, and reduced reliance on geopolitically sensitive materials, thereby addressing critical market restraints and opening new avenues for product differentiation and cost reduction. The ability to develop and commercialize these next-generation motors will be a key differentiator for market players seeking long-term growth.

Furthermore, the rapid growth of electric vehicles in emerging economies presents substantial market expansion opportunities. Countries in Asia Pacific, Latin America, and Africa are increasingly adopting electrification strategies, spurred by urbanization, rising environmental concerns, and improving economic conditions. This demographic shift, coupled with the nascent stage of EV market development in these regions, offers a fertile ground for manufacturers to establish early market leadership. Additionally, the burgeoning demand for electric commercial vehicles, including buses, trucks, and vans, represents a significant untapped segment that requires robust and specialized electric motor solutions, creating a new frontier for innovation and market penetration beyond passenger cars.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Motor Architectures (e.g., Axial Flux, Segmented Stator) | +6.5% | Global | Mid to Long-term (2027-2033) |

| Expansion into Emerging EV Markets (e.g., India, Southeast Asia, Brazil) | +5.9% | Asia Pacific, Latin America, Africa | Mid to Long-term (2026-2033) |

| Growth of Electric Commercial Vehicle Segment (Buses, Trucks, Vans) | +5.2% | North America, Europe, China | Short to Mid-term (2025-2030) |

| Focus on Rare-Earth-Free or Reduced-Rare-Earth Motors | +4.8% | Global | Long-term (2028-2033) |

| Integration with Smart Grid and Vehicle-to-Grid (V2G) Technologies | +4.0% | Europe, North America, Japan | Long-term (2029-2033) |

| Development of Modular and Scalable Motor Platforms | +3.5% | Global | Mid-term (2026-2031) |

| Enhancement of Recycling and Circular Economy Initiatives for Motor Components | +3.0% | Europe, North America | Long-term (2029-2033) |

Automotive Electric Motor for Electric Vehicle Market Challenges Impact Analysis

The Automotive Electric Motor for Electric Vehicle market, despite its high growth potential, is confronted by several significant challenges that necessitate strategic navigation and robust solutions. Intense competition among established automotive suppliers and new entrants in the EV component sector is a formidable challenge, leading to price pressures and demanding continuous innovation. Companies must differentiate their offerings through superior performance, cost-efficiency, and reliability to gain and maintain market share. Furthermore, the rapid pace of technological advancements, while an opportunity, also poses a challenge in terms of keeping pace with evolving motor designs, power electronics, and manufacturing processes. Investments in R&D are substantial, and the risk of technological obsolescence is ever-present.

Another critical challenge involves securing a stable and ethical supply chain for key materials, particularly rare-earth elements and high-grade copper, amidst increasing global demand and geopolitical tensions. Disruptions in the supply chain can lead to production delays, increased costs, and ultimately impact vehicle availability. Additionally, the development of skilled labor capable of designing, manufacturing, and maintaining advanced electric motors and their associated systems is a growing concern. The specialized knowledge required in fields like electrical engineering, power electronics, and material science often outstrips the current supply of talent, creating a workforce gap that could hinder innovation and scaling efforts. Addressing these multifaceted challenges is paramount for the sustained and successful growth of the automotive electric motor market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure from Market Entrants | -4.2% | Global | Short to Mid-term (2025-2029) |

| Managing Supply Chain Risks for Critical Raw Materials | -3.8% | Global | Mid-term (2026-2031) |

| Rapid Technological Obsolescence and Need for Continuous Innovation | -3.5% | Global | Long-term (2028-2033) |

| Shortage of Skilled Labor and Engineering Talent | -3.0% | North America, Europe, Japan | Mid-term (2027-2032) |

| Ensuring Motor Durability and Reliability in Diverse Operating Conditions | -2.5% | Global | Short to Mid-term (2025-2029) |

| High Research and Development Costs | -2.0% | Global | Short to Mid-term (2025-2028) |

| Standardization and Interoperability Issues | -1.5% | Global | Short-term (2025-2027) |

Automotive Electric Motor for Electric Vehicle Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Automotive Electric Motor for Electric Vehicle market, providing a detailed analysis of market size, trends, drivers, restraints, opportunities, and challenges. The report offers an in-depth segmentation analysis by motor type, vehicle type, power output, application, and geographic region, delivering actionable insights for stakeholders across the value chain. It integrates an examination of the impact of artificial intelligence on motor design, manufacturing, and performance, alongside a thorough competitive landscape analysis of key market players, aiming to equip decision-makers with a holistic understanding of the market's current state and future trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 95.7 Billion |

| Growth Rate | 23.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, Siemens AG, ZF Friedrichshafen AG, Magna International Inc., Nidec Corporation, BorgWarner Inc., Denso Corporation, Mitsubishi Electric Corporation, Hitachi Astemo, Valeo S.A., Schaeffler AG, Remy International (BorgWarner), Toshiba Corporation, Johnson Electric Holdings Ltd., Mahle GmbH, Brose Fahrzeugteile GmbH & Co. KG, LG Electronics Inc., Hyundai Mobis, Beijing E-drive Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Electric Motor for Electric Vehicle market is segmented to provide a granular view of its diverse components and drivers. This detailed breakdown enables stakeholders to identify specific growth areas, understand competitive landscapes within niches, and tailor strategies effectively. Segmentation by motor type differentiates between widely adopted technologies like Permanent Magnet Synchronous Motors (PMSM) and emerging alternatives, highlighting the technological evolution in the industry. Vehicle type segmentation, including BEV, PHEV, HEV, and FCEV, reflects the varying requirements for electric motors across different levels of vehicle electrification, from partial to full electric powertrains.

Further segmentation by power output categorizes motors based on their capacity, crucial for understanding their application in vehicles ranging from compact urban cars to high-performance and heavy-duty commercial vehicles. Application-based segmentation distinguishes between passenger cars, commercial vehicles, and two-wheelers, each presenting unique market dynamics and demand characteristics. Finally, geographic segmentation provides regional insights into adoption rates, regulatory impacts, and market maturity, essential for global market participants to refine their expansion strategies and localized product offerings. This multi-dimensional segmentation offers a comprehensive framework for analyzing the market's current structure and future potential.

- By Motor Type: Permanent Magnet Synchronous Motor (PMSM), Induction Motor (IM), Switched Reluctance Motor (SRM), Brushless DC (BLDC) Motor, Others (Axial Flux, Synchronous Reluctance)

- By Vehicle Type: Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV), Fuel Cell Electric Vehicle (FCEV)

- By Power Output: Less than 100 kW, 100 kW to 200 kW, More than 200 kW

- By Application: Passenger Cars, Commercial Vehicles (Buses, Trucks, Vans), Two-Wheelers

Regional Highlights

- Asia Pacific: Dominates the market due to robust EV production and adoption in China, strong government support for electrification, and increasing demand from countries like India, Japan, and South Korea. The region is a manufacturing hub for electric motors and benefits from a large consumer base and proactive environmental policies.

- Europe: Exhibits significant growth, driven by stringent emission regulations, substantial government incentives for EV purchases, and extensive investments in charging infrastructure. Germany, Norway, France, and the UK are leading the transition, with a strong focus on premium and performance-oriented EVs, often featuring advanced motor technologies.

- North America: Demonstrates strong potential, fueled by increasing consumer interest in EVs, investments from major automotive manufacturers in electric vehicle production facilities, and supportive policies from federal and state governments. The United States and Canada are key markets, characterized by a growing demand for electric trucks and SUVs.

- Latin America: An emerging market with growing interest in electric mobility, particularly in countries like Brazil and Mexico. The region is seeing initial adoption driven by public transport electrification projects and increasing environmental consciousness, offering long-term growth opportunities as infrastructure develops.

- Middle East & Africa (MEA): Currently a nascent market but with significant long-term potential. Investments in sustainable energy and diversification away from fossil fuels are driving initial EV adoption, particularly in wealthier Gulf Cooperation Council (GCC) countries. Infrastructure development and favorable policies will be critical for accelerating growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Electric Motor for Electric Vehicle Market.- Robert Bosch GmbH

- Continental AG

- Siemens AG

- ZF Friedrichshafen AG

- Magna International Inc.

- Nidec Corporation

- BorgWarner Inc.

- Denso Corporation

- Mitsubishi Electric Corporation

- Hitachi Astemo

- Valeo S.A.

- Schaeffler AG

- Toshiba Corporation

- Johnson Electric Holdings Ltd.

- Mahle GmbH

- Brose Fahrzeugteile GmbH & Co. KG

- LG Electronics Inc.

- Hyundai Mobis

- Beijing E-drive Co. Ltd.

- Shandong United Power Electric Co., Ltd.

Frequently Asked Questions

What are the primary types of electric motors used in electric vehicles?

The primary types of electric motors used in EVs include Permanent Magnet Synchronous Motors (PMSM), which are highly efficient and offer excellent power density, and Induction Motors (IM), known for their robustness and cost-effectiveness. Other emerging types include Switched Reluctance Motors (SRM) and Axial Flux Motors, which are gaining traction for their specific performance characteristics and potential for rare-earth-free designs.

How does AI impact the development and performance of automotive electric motors?

AI significantly impacts EV motors by optimizing design through generative algorithms, enabling the creation of more efficient and power-dense motor topologies. It also enhances manufacturing processes through predictive quality control and automation. In operation, AI improves motor control for better energy management, extending vehicle range and enabling predictive maintenance to prevent failures, thereby increasing overall reliability and lifespan.

What are the key factors driving the growth of the automotive electric motor market?

Key growth drivers include stringent global emission regulations and supportive government incentives for EV adoption, continuous advancements in battery technology leading to lower costs and increased range, and a growing consumer demand for sustainable transportation solutions. Technological innovations in motor design, such as increased power density and efficiency, also significantly contribute to market expansion.

What are the main challenges faced by manufacturers in the electric motor for EV market?

Manufacturers face challenges such as intense competition leading to price pressures, volatility in the supply chain for critical raw materials like rare-earth elements, and the rapid pace of technological obsolescence requiring constant research and development investments. Additionally, the shortage of skilled labor specializing in EV powertrain engineering and the high initial R&D costs present considerable hurdles.

What future trends are expected to shape the automotive electric motor market?

Future trends include a greater emphasis on integrated e-axle solutions combining the motor, inverter, and gearbox into a single unit for compactness and efficiency. There will be increased adoption of Silicon Carbide (SiC) inverters for improved power electronics. Furthermore, the market will see more development in rare-earth-free motors to mitigate supply chain risks and a growing focus on sustainable manufacturing practices and recycling of motor components.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted