Automotive Catalyst Market

Automotive Catalyst Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709526 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

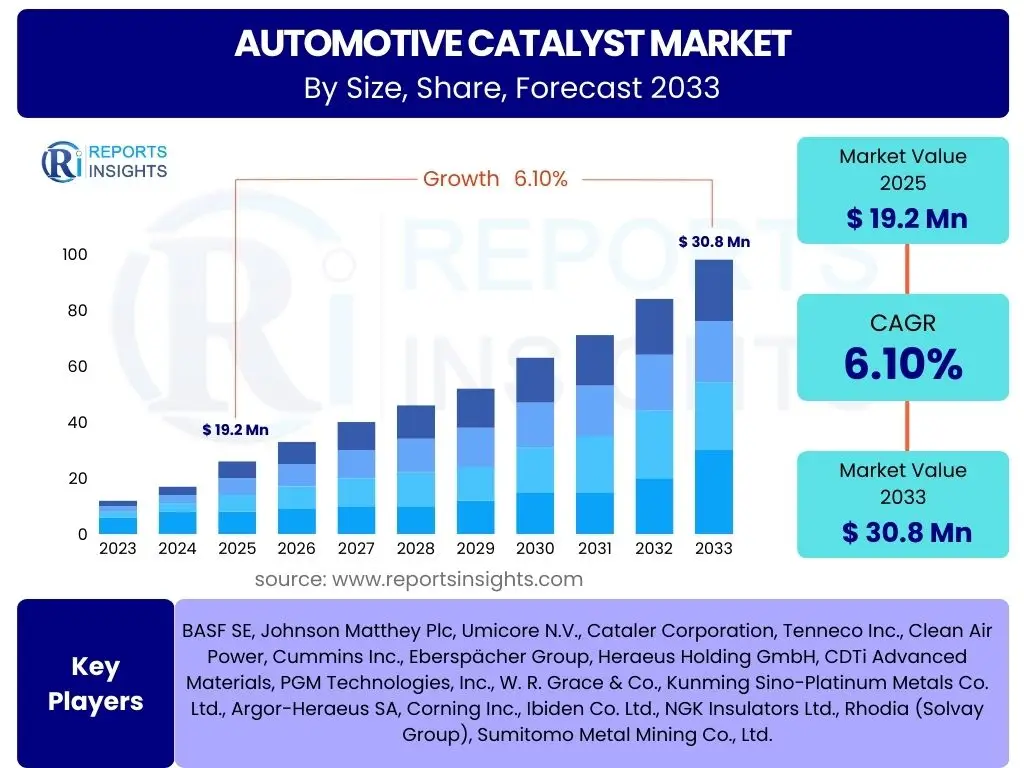

Automotive Catalyst Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Catalyst Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.1% between 2025 and 2033. The market is estimated at USD 19.2 Billion in 2025 and is projected to reach USD 30.8 Billion by the end of the forecast period in 2033.

Key Automotive Catalyst Market Trends & Insights

User inquiries frequently highlight the dynamic landscape shaped by evolving environmental regulations and technological advancements. A primary concern revolves around how stricter global emission standards, particularly in emerging economies, are driving innovation in catalyst formulations and their broader adoption. Additionally, there is significant interest in the impact of vehicle electrification on traditional catalyst demand and the emergence of new catalyst applications for hybrid and alternative fuel vehicles. Material science breakthroughs, including the development of lower-cost alternatives to precious metals and enhanced recycling capabilities, also represent a crucial area of user focus, indicating a market striving for sustainability and cost-effectiveness.

- Stricter global emission regulations are mandating advanced catalytic converter technologies, especially Euro 7 and similar standards worldwide.

- Growing adoption of hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs) drives demand for specialized catalysts.

- Development of innovative catalyst materials, including lean-burn catalysts and gasoline particulate filters (GPFs), to meet evolving powertrain requirements.

- Increased focus on catalyst recycling and recovery of precious metals due to supply chain volatility and sustainability initiatives.

- Integration of advanced sensing and control technologies with catalytic systems for improved performance and real-time emission monitoring.

AI Impact Analysis on Automotive Catalyst

Common user questions regarding AI's impact on automotive catalysts center on its potential to revolutionize research and development, optimize manufacturing processes, and enhance the operational efficiency of catalytic systems. Users are keen to understand how artificial intelligence can accelerate the discovery of novel catalyst materials, especially those that minimize reliance on expensive precious metals, thereby reducing costs and improving sustainability. Furthermore, there is considerable interest in AI's role in predictive maintenance for catalytic converters, optimizing their performance over time, and ensuring compliance with stringent emission standards by enabling real-time adjustments and diagnostics. The analytical capabilities of AI are also seen as crucial for processing complex data from vehicle emissions, leading to more effective catalyst designs and performance monitoring strategies.

- AI algorithms accelerate the discovery and design of novel catalyst materials, optimizing compositions for enhanced efficiency and durability.

- Machine learning models improve manufacturing processes through predictive analytics, reducing defects and optimizing resource utilization in catalyst production.

- AI-driven sensors and control units enable real-time optimization of catalytic converter performance, adapting to varying driving conditions and fuel types.

- Predictive maintenance for catalytic systems is enhanced by AI, forecasting potential failures and enabling timely interventions to maintain emission compliance.

- Data analytics powered by AI provides deeper insights into catalyst aging mechanisms and degradation patterns, informing future design improvements.

Key Takeaways Automotive Catalyst Market Size & Forecast

Analysis of user questions regarding market size and forecast reveals a strong emphasis on understanding the primary growth engines and the long-term sustainability of the automotive catalyst sector. Users are particularly interested in the balancing act between the rising global vehicle production, especially in developing regions, and the transformative shift towards electrification in established markets. Key concerns include identifying the most promising growth segments within the catalyst market, such as specific product types or vehicle applications, and anticipating potential disruptions from emerging technologies or regulatory shifts. The overarching theme points to a market that, while facing evolutionary changes, is still underpinned by the fundamental need for emission control across a diverse range of internal combustion engine and hybrid vehicles for the foreseeable future, driving sustained demand for innovative catalyst solutions.

- The market is poised for robust growth, driven by stringent global emission regulations and increasing vehicle parc, particularly in Asia Pacific.

- Technological innovation in catalyst materials and designs will be crucial for meeting future emission standards and sustaining market expansion.

- While electrification presents a long-term shift, catalysts for hybrid and advanced internal combustion engines will maintain significant demand during the forecast period.

- Precious metal price volatility and supply chain resilience remain critical factors influencing market dynamics and strategic planning for manufacturers.

- Investment in catalyst recycling and the development of alternative, cost-effective materials are essential for ensuring the industry's sustainable growth.

Automotive Catalyst Market Drivers Analysis

The automotive catalyst market is primarily driven by the global imperative to mitigate vehicular emissions and improve air quality. Stringent government regulations, such as Euro 6/7, EPA standards, and China VI, compel automakers to integrate advanced catalytic converter technologies into their vehicles. This regulatory pressure, combined with the continuous growth in global vehicle production, particularly in emerging economies, forms a strong foundation for market expansion. Furthermore, ongoing technological advancements in catalyst formulations, including the development of more efficient and durable materials, contribute significantly to market growth by enabling compliance with increasingly strict environmental targets while maintaining vehicle performance.

The increasing consumer awareness regarding environmental protection and the resultant demand for greener transportation solutions also indirectly fuels the market. This societal shift, coupled with the rapid evolution of powertrain technologies towards hybrid and cleaner internal combustion engines, necessitates continuous innovation and adoption of advanced catalysts. The industry is also seeing a push towards catalysts capable of handling diverse fuel qualities and varying operating conditions, further solidifying the demand for sophisticated emission control systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Global Emission Regulations | +2.5% | Europe, Asia Pacific (China, India), North America | Short- to Mid-Term |

| Increasing Vehicle Production & Sales | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Mid- to Long-Term |

| Technological Advancements in Catalyst Materials | +1.5% | Global | Continuous |

| Growth in Hybrid & Fuel Cell Electric Vehicles | +1.2% | Europe, North America, Japan, China | Mid- to Long-Term |

Automotive Catalyst Market Restraints Analysis

Despite significant growth drivers, the automotive catalyst market faces several notable restraints that could temper its expansion. One of the primary concerns is the high and often volatile cost of precious metals such as platinum, palladium, and rhodium, which are critical components in most catalytic converters. Fluctuations in these raw material prices can significantly impact manufacturing costs and product pricing, potentially affecting market accessibility and profitability for manufacturers. This volatility also creates uncertainty for long-term strategic planning and investment.

Furthermore, the accelerating global shift towards battery electric vehicles (BEVs), which do not require traditional catalytic converters, poses a long-term existential threat to the market. While hybrid vehicles still incorporate catalysts, the complete transition to electric mobility in certain regions could eventually reduce the overall demand for these components. Additionally, the complexity and capital intensity of manufacturing advanced catalysts, coupled with the need for continuous research and development to meet ever-evolving standards, present barriers to market entry for new players and can strain the resources of existing manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High and Volatile Cost of Precious Metals | -1.5% | Global | Short- to Mid-Term |

| Increasing Adoption of Battery Electric Vehicles (BEVs) | -1.2% | Europe, North America, China | Mid- to Long-Term |

| Complex Manufacturing Processes & R&D Costs | -0.8% | Global | Continuous |

| Emergence of Alternative Emission Reduction Technologies | -0.7% | Global | Long-Term |

Automotive Catalyst Market Opportunities Analysis

Significant opportunities exist within the automotive catalyst market, particularly driven by the need for sustainable solutions and expansion into underserved segments. The development and commercialization of alternative, non-precious metal catalysts represent a major opportunity to mitigate the impact of volatile raw material costs and enhance the economic viability of emission control systems. This includes research into base metal catalysts and novel material combinations that offer comparable performance at a reduced cost. Such innovations can unlock new market segments and improve the competitiveness of catalyst manufacturers.

Additionally, the burgeoning focus on circular economy principles presents a substantial opportunity in the form of enhanced catalyst recycling and precious metal recovery technologies. Improved efficiency in recovering valuable materials from end-of-life catalytic converters can create a more sustainable supply chain, reduce environmental impact, and provide a stable source of raw materials. Furthermore, the expansion of vehicle markets in developing economies, coupled with their anticipated adoption of stricter emission standards, offers a fertile ground for market penetration and growth for advanced catalyst solutions. The niche market for catalysts designed for hydrogen fuel cell vehicles and other emerging alternative fuels also represents a forward-looking growth avenue.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Alternative Catalyst Materials | +1.7% | Global | Mid- to Long-Term |

| Enhanced Recycling and Recovery of Precious Metals | +1.4% | Global | Short- to Mid-Term |

| Expansion in Developing Economies with Stricter Norms | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Mid- to Long-Term |

| Catalysts for Hydrogen Fuel Cell & Alternative Fuel Vehicles | +1.0% | North America, Europe, Japan, South Korea | Long-Term |

Automotive Catalyst Market Challenges Impact Analysis

The automotive catalyst market faces several significant challenges that necessitate strategic innovation and robust supply chain management. One critical challenge is the inherent scarcity and geographical concentration of precious metal resources, which can lead to supply chain vulnerabilities and geopolitical risks. Ensuring a stable and ethical supply of these essential raw materials is paramount for sustained production and innovation within the industry. This challenge is further compounded by the environmental and social impacts associated with precious metal mining, which increasingly draws scrutiny from regulators and consumers.

Another major challenge involves the effective disposal and end-of-life management of used catalytic converters. While recycling offers a solution, developing economically viable and environmentally sound processes for processing the vast volume of spent catalysts remains a complex task. Furthermore, the rapid pace of technological change in the automotive sector, particularly the ongoing shift towards diverse powertrain architectures including various hybrid forms and hydrogen fuel cells, demands continuous and costly research and development efforts to adapt catalyst technologies. Competition from alternative emission reduction methods and the need to achieve increasingly stringent emission targets without compromising vehicle performance or affordability also present ongoing hurdles for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scarcity & Volatility of Precious Metal Supply | -1.6% | Global | Short- to Mid-Term |

| Complexities in Catalyst Recycling & Disposal | -1.0% | Global | Mid-Term |

| Adapting to Diverse Powertrain Technologies (e.g., Hybrids) | -0.9% | Global | Continuous |

| Balancing Emission Reduction with Performance & Cost | -0.8% | Global | Continuous |

Automotive Catalyst Market - Updated Report Scope

This report provides an in-depth analysis of the global automotive catalyst market, offering a comprehensive overview of its current state, historical performance, and future growth trajectory. It meticulously segments the market by material, product type, application, and vehicle type, providing detailed insights into each category's dynamics and contribution to overall market expansion. The scope encompasses a thorough examination of key market drivers, restraints, opportunities, and challenges, along with an impact analysis to gauge their influence on market growth. Furthermore, the report presents a regional outlook, identifying key growth regions and countries, and profiles leading market players, offering strategic intelligence for stakeholders. The objective is to equip businesses with a holistic understanding of market trends, competitive landscape, and future prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.2 Billion |

| Market Forecast in 2033 | USD 30.8 Billion |

| Growth Rate | 6.1% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Johnson Matthey Plc, Umicore N.V., Cataler Corporation, Tenneco Inc., Clean Air Power, Cummins Inc., Eberspächer Group, Heraeus Holding GmbH, CDTi Advanced Materials, PGM Technologies, Inc., W. R. Grace & Co., Kunming Sino-Platinum Metals Co. Ltd., Argor-Heraeus SA, Corning Inc., Ibiden Co. Ltd., NGK Insulators Ltd., Rhodia (Solvay Group), Sumitomo Metal Mining Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive catalyst market is broadly segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market drivers and trends across various technological applications and material compositions. Each segment reflects distinct market characteristics, influenced by regulatory frameworks, technological innovations, and specific vehicle requirements. Understanding these segments is crucial for identifying key growth areas and developing targeted strategies within the competitive landscape.

- By Material: This segment analyzes the demand for different precious and base metals utilized in catalysts, including Platinum, Palladium, Rhodium, Cerium, and other emerging materials. Precious metals remain dominant due to their superior catalytic activity, but research into cost-effective alternatives is gaining traction.

- By Product Type: This segment includes Three-Way Catalytic Converters (TWC) for gasoline engines, Diesel Oxidation Catalysts (DOC), Selective Catalytic Reduction (SCR) systems, Lean NOx Traps (LNT), Gasoline Particulate Filters (GPF), and Diesel Particulate Filters (DPF). Each type addresses specific emission challenges for different engine technologies.

- By Application: The market is segmented by the type of vehicle application, encompassing Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Off-Road Vehicles. Passenger cars represent the largest volume, but commercial vehicles require robust and efficient systems due to high usage and stringent regulations.

- By Vehicle Type: This segmentation differentiates between Gasoline Vehicles, Diesel Vehicles, Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicles (PHEV), and Fuel Cell Electric Vehicles (FCEV). The growth of HEVs and PHEVs presents new opportunities for specialized catalyst designs, while FCEVs utilize catalysts in a different capacity for power generation.

Regional Highlights

- Asia Pacific: This region is projected to be the largest and fastest-growing market for automotive catalysts, driven by increasing vehicle production and sales, particularly in China and India, coupled with the escalating implementation of stringent emission regulations akin to Euro 6/7 standards. The rising disposable incomes and expanding middle class contribute to higher demand for personal and commercial vehicles, consequently boosting the need for advanced emission control systems. Government initiatives focused on improving air quality and promoting greener transportation also play a crucial role in market expansion across this region.

- Europe: Europe represents a mature but highly innovative market, primarily characterized by some of the world's most stringent emission standards. The region's focus on reducing NOx and particulate matter from both gasoline and diesel vehicles, alongside the rapid growth of hybrid vehicle sales, fuels the demand for advanced and highly efficient catalytic converters, including SCR systems and GPFs. Investments in R&D for next-generation catalyst technologies and recycling initiatives are also prominent here.

- North America: The North American market is significantly influenced by Environmental Protection Agency (EPA) regulations and California Air Resources Board (CARB) standards. Demand for automotive catalysts is steady, supported by consistent vehicle sales and the ongoing need to upgrade emission control systems to meet evolving standards. The increasing popularity of light trucks and SUVs also impacts catalyst design and consumption, with a growing emphasis on durable and high-performance solutions.

- Latin America, Middle East, and Africa (LAMEA): These regions are anticipated to experience substantial growth in the mid- to long-term as their respective governments increasingly adopt and enforce stricter emission standards. While currently lagging behind developed markets in terms of regulatory stringency, the burgeoning automotive manufacturing bases and rising vehicle parc in key countries like Brazil, Mexico, South Africa, and the UAE will drive significant demand for automotive catalysts. Infrastructure development and economic growth further support market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Catalyst Market.- BASF SE

- Johnson Matthey Plc

- Umicore N.V.

- Cataler Corporation

- Tenneco Inc.

- Clean Air Power

- Cummins Inc.

- Eberspächer Group

- Heraeus Holding GmbH

- CDTi Advanced Materials

- PGM Technologies, Inc.

- W. R. Grace & Co.

- Kunming Sino-Platinum Metals Co. Ltd.

- Argor-Heraeus SA

- Corning Inc.

- Ibiden Co. Ltd.

- NGK Insulators Ltd.

- Rhodia (Solvay Group)

- Sumitomo Metal Mining Co., Ltd.

Frequently Asked Questions

What are automotive catalysts primarily made of?

Automotive catalysts are primarily made from a ceramic or metallic honeycomb structure coated with a washcoat containing precious metals like platinum, palladium, and rhodium, along with rare earth elements such as cerium. These materials facilitate chemical reactions to convert harmful exhaust gases into less toxic substances.

How do automotive catalysts reduce vehicle emissions?

Automotive catalysts reduce emissions through chemical reactions. Three-way catalysts, for instance, simultaneously oxidize carbon monoxide (CO) and unburnt hydrocarbons (HC) into carbon dioxide and water, while reducing nitrogen oxides (NOx) into nitrogen and oxygen, converting them into less harmful components before they exit the exhaust system.

What is the typical lifespan of a catalytic converter?

A typical catalytic converter is designed to last the entire lifespan of a vehicle, often 100,000 miles or more, provided the engine is maintained properly. Factors such as engine misfires, oil contamination, or impact damage can significantly reduce its operational life.

Are catalytic converters still necessary with the rise of electric vehicles?

While fully battery electric vehicles (BEVs) do not require catalytic converters, they remain essential for all internal combustion engine (ICE) vehicles and hybrid electric vehicles (HEVs/PHEVs) that utilize an ICE. As hybrids are expected to be a significant part of the automotive landscape for decades, the demand for catalysts will continue, albeit with evolving specifications.

What innovations are shaping the future of automotive catalysts?

Future innovations in automotive catalysts are focused on developing more cost-effective materials (e.g., reducing precious metal content), enhancing durability, improving efficiency for diverse fuel types and operating conditions, and integrating smart technologies like AI for real-time performance optimization and predictive maintenance. Advancements in recycling technologies are also crucial.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted