Automotive Disc Brake Market

Automotive Disc Brake Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709941 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

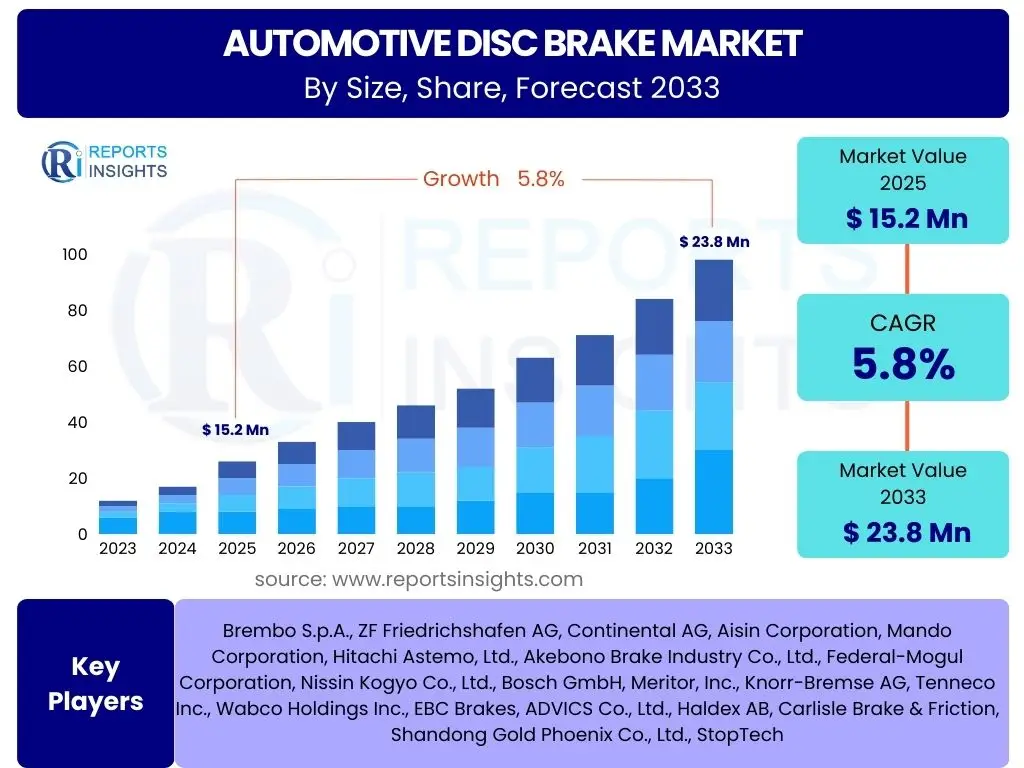

Automotive Disc Brake Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Disc Brake Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 23.8 Billion by the end of the forecast period in 2033.

Key Automotive Disc Brake Market Trends & Insights

The automotive disc brake market is currently experiencing transformative trends driven by the pursuit of enhanced vehicle performance, safety, and sustainability. Key developments include the increasing adoption of lightweight materials, such as aluminum alloys and composites, aimed at reducing vehicle weight and improving fuel efficiency. This shift is crucial for meeting stringent emission regulations and extending the range of electric vehicles.

Furthermore, the integration of advanced sensor technologies and electronic control units is leading to the proliferation of smart braking systems. These systems offer features like predictive maintenance, enhanced emergency stopping capabilities through sophisticated ABS and EBD, and seamless integration with advanced driver-assistance systems (ADAS).

The rapid expansion of the electric vehicle (EV) segment is also profoundly influencing design and material considerations for disc brakes. EVs place unique demands on braking systems due to their regenerative braking capabilities, which reduce the reliance on friction brakes, and often higher vehicle weight due to batteries. This necessitates the development of specialized disc brakes optimized for EV-specific challenges, including corrosion resistance due to less frequent use, noise reduction, and efficient thermal management.

- Shift towards lightweight and high-performance materials for improved fuel efficiency and EV range.

- Integration of smart braking systems with advanced sensors and electronic controls for enhanced safety features and ADAS compatibility.

- Development of specialized disc brakes tailored for electric vehicles (EVs), addressing regenerative braking, corrosion, and noise.

- Growing adoption of ceramic and carbon-ceramic disc brakes in premium and performance vehicle segments.

- Increasing demand for noise, vibration, and harshness (NVH) optimized braking systems to enhance driver comfort.

AI Impact Analysis on Automotive Disc Brake

Artificial Intelligence (AI) is poised to significantly impact various facets of the automotive disc brake industry, from design and manufacturing to predictive maintenance and supply chain management. Users frequently inquire about how AI will enhance product development efficiency, improve brake performance, and contribute to overall vehicle safety. AI-driven simulation tools can rapidly optimize brake component designs, test various material compositions, and predict performance under extreme conditions, drastically reducing development cycles and costs.

In manufacturing, AI and machine learning algorithms can monitor production lines in real-time, identifying defects, predicting equipment failures, and optimizing processes for efficiency and quality control. This leads to higher precision in component fabrication and a reduction in waste, addressing user concerns about product reliability and cost-effectiveness. The potential for autonomous quality inspection systems, leveraging computer vision and AI, is particularly significant in ensuring stringent safety standards.

Moreover, AI plays a crucial role in the lifecycle management of disc brakes through advanced predictive maintenance. By analyzing data from vehicle sensors, AI algorithms can accurately forecast when brake pads or discs will need replacement, optimizing service schedules and preventing unexpected failures. This not only enhances vehicle safety and reliability for end-users but also creates new service models and revenue streams for manufacturers and service providers. Users also anticipate AI contributing to more responsive and adaptive braking systems in autonomous vehicles.

- AI-driven design optimization and simulation for enhanced brake performance and material selection.

- Real-time AI-powered quality control and defect detection in manufacturing processes.

- Predictive maintenance analytics using AI to forecast brake wear and optimize service intervals.

- Integration of AI in ADAS for more intelligent and responsive braking in critical situations.

- Supply chain optimization through AI, improving material sourcing and logistics for brake components.

Key Takeaways Automotive Disc Brake Market Size & Forecast

The automotive disc brake market is on a robust growth trajectory, primarily driven by increasing vehicle production globally, stringent safety regulations, and continuous technological advancements. The projected CAGR of 5.8% indicates a stable and expanding market, reflecting the indispensable role of disc brakes in modern vehicles. This growth is also significantly influenced by the rising demand for premium vehicles, which often incorporate advanced braking systems for enhanced safety and performance.

A significant portion of the market expansion will be attributed to the burgeoning automotive sectors in emerging economies, alongside the ongoing replacement and upgrade cycles in mature markets. The forecast of reaching USD 23.8 Billion by 2033 underscores the sustained demand for reliable and high-performance braking solutions across all vehicle types, from passenger cars to heavy commercial vehicles. Furthermore, the market's resilience is supported by the aftermarket segment, which consistently drives demand for replacement components.

The market's future is intrinsically linked to innovation, particularly in materials science and smart technologies. The transition towards electric vehicles, while potentially altering friction brake usage patterns, simultaneously opens new avenues for specialized disc brake solutions that cater to unique EV requirements. Therefore, manufacturers focusing on these areas are well-positioned for long-term success, adapting to evolving industry standards and consumer expectations.

- Steady market expansion fueled by rising global vehicle production and stringent safety mandates.

- Significant growth potential from emerging economies and continuous aftermarket demand.

- Technological innovation, particularly in lightweight materials and smart systems, is critical for future market leadership.

- Electric Vehicle (EV) proliferation presents both challenges and new opportunities for specialized disc brake development.

- Overall market value is set to increase by approximately 56% over the forecast period, emphasizing sustained investment in the sector.

Automotive Disc Brake Market Drivers Analysis

The automotive disc brake market is significantly propelled by several concurrent factors. Foremost among these is the global increase in vehicle production, especially in developing economies, which directly translates into higher demand for original equipment (OE) brake systems. This is further bolstered by the continuous evolution and enforcement of stricter automotive safety regulations worldwide, compelling manufacturers to equip vehicles with more advanced and reliable braking technologies to meet compliance standards and consumer safety expectations.

Technological advancements in braking systems, such as the development of lighter, more durable, and higher-performance materials like ceramic composites, also act as a strong market driver. These innovations cater to the growing consumer demand for vehicles with superior stopping power, reduced noise, and extended component lifespan. The rising disposable incomes and changing consumer preferences towards premium and performance-oriented vehicles, which often feature advanced disc brake systems, further contribute to market growth.

Moreover, the expansion of the aftermarket segment, driven by the routine replacement of worn-out brake components, ensures a consistent revenue stream for disc brake manufacturers. Urbanization and the consequent increase in vehicle density lead to more frequent braking cycles and accelerated wear, thereby necessitating regular maintenance and part replacement. The rapid growth of the electric vehicle market, while unique, also creates demand for specialized disc brake solutions optimized for EV architecture and regenerative braking interplay.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production | +1.5% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Stringent Automotive Safety Regulations | +1.2% | Europe, North America, Japan, China | Medium to Long-term |

| Technological Advancements in Materials & Design | +1.0% | Global | Long-term |

| Rising Demand for Premium & Performance Vehicles | +0.8% | North America, Europe, China | Medium-term |

| Growth in Aftermarket Sales | +0.7% | Global | Long-term |

Automotive Disc Brake Market Restraints Analysis

Despite robust growth, the automotive disc brake market faces several significant restraints that could impede its trajectory. A primary concern is the relatively high manufacturing cost associated with advanced disc brake systems, particularly those utilizing premium materials like ceramic composites or incorporating complex electronic components. This elevated cost can restrict adoption in budget-sensitive vehicle segments and emerging markets, limiting overall market penetration.

Another crucial restraint is the intense competition from alternative braking technologies and systems, especially the increasing prevalence of regenerative braking in electric and hybrid vehicles. While friction brakes are still essential, regenerative braking reduces their frequency of use, potentially impacting replacement cycles and demand for traditional disc brake components. Environmental regulations concerning brake dust emissions, which contain particulate matter, also pose a growing challenge, pushing manufacturers towards developing cleaner, potentially more expensive, solutions.

Furthermore, volatility in raw material prices, such as steel, iron, and specialized alloys, can significantly impact production costs and profit margins for disc brake manufacturers. Supply chain disruptions, exacerbated by geopolitical tensions or global events, can lead to material shortages and increased lead times, further constraining market growth. The complexity of integrating advanced braking systems with evolving vehicle architectures and software platforms also presents engineering and cost challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Systems | -0.9% | Global, particularly emerging markets | Long-term |

| Competition from Regenerative Braking in EVs | -0.8% | North America, Europe, China | Medium to Long-term |

| Stringent Environmental Regulations (Brake Dust) | -0.7% | Europe, North America | Medium-term |

| Volatility in Raw Material Prices | -0.6% | Global | Short to Medium-term |

| Supply Chain Disruptions | -0.5% | Global | Short to Medium-term |

Automotive Disc Brake Market Opportunities Analysis

The automotive disc brake market is ripe with opportunities driven by several evolving industry dynamics. One of the most significant opportunities lies in the rapid growth of the electric vehicle (EV) segment. While regenerative braking reduces friction brake usage, EVs still require robust disc brakes for emergency stops and low-speed braking, creating demand for specialized, corrosion-resistant, and NVH-optimized solutions that can withstand longer periods of inactivity. This niche but growing requirement offers significant scope for innovation and market penetration.

Another key opportunity emerges from the continuous development of advanced materials, such as lighter alloys, advanced composites, and ceramic matrix materials. These materials offer superior performance, reduced weight, and extended lifespan, catering to the increasing demand for high-performance and fuel-efficient vehicles. Manufacturers investing in research and development of these next-generation materials can gain a competitive edge and tap into the premium and performance vehicle segments. The expansion of connected car technologies also presents an opportunity for integrating smart brake systems with vehicle-to-everything (V2X) communication for enhanced predictive safety features.

Furthermore, the robust and consistently growing aftermarket segment presents a stable and profitable avenue for disc brake manufacturers. With millions of vehicles on the road requiring regular brake maintenance and replacement, the aftermarket ensures a sustained demand irrespective of new vehicle sales fluctuations. Additionally, emerging markets in Asia Pacific, Latin America, and Africa, characterized by rising disposable incomes and increasing vehicle ownership, offer untapped potential for both OEM and aftermarket sales as their automotive industries mature and expand.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of EV-Specific Braking Solutions | +1.3% | Global, particularly developed regions | Long-term |

| Advancements in Lightweight & High-Performance Materials | +1.1% | Global | Medium to Long-term |

| Growing Aftermarket Demand in Emerging Economies | +0.9% | Asia Pacific, Latin America, Africa | Long-term |

| Integration with Connected Car & ADAS Technologies | +0.8% | North America, Europe, Japan | Medium-term |

| Focus on Noise, Vibration, and Harshness (NVH) Reduction | +0.7% | Global | Medium-term |

Automotive Disc Brake Market Challenges Impact Analysis

The automotive disc brake market faces a series of complex challenges that demand strategic responses from manufacturers. One significant challenge is the ongoing pressure from regulatory bodies worldwide to reduce emissions, which now extends to non-exhaust emissions like brake dust. Developing brake materials and systems that minimize particulate matter while maintaining performance and cost-effectiveness is a substantial engineering and material science hurdle. This drives the need for costly research and development into new, environmentally friendly friction materials.

Technological obsolescence also poses a threat, particularly with the rapid evolution of vehicle architectures, including the increasing sophistication of electric vehicle powertrains and autonomous driving systems. Disc brake manufacturers must continuously innovate to ensure their products remain compatible and optimized for these new platforms, which often means adapting to new interfaces and performance requirements. The shift towards brake-by-wire systems, for example, demands significant investment in electronic integration and software development.

Furthermore, intense global competition among a large number of established and emerging players places downward pressure on pricing and profit margins. Maintaining market share requires constant innovation, efficient production, and strong supply chain management in a highly commoditized segment for standard brakes. Intellectual property protection and the rapid pace of technological imitation in certain regions add another layer of complexity. The need for global standardization, while beneficial for mass production, also presents challenges in adapting products to diverse regional regulations and consumer preferences.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulations on Brake Dust Emissions | -0.9% | Europe, North America, Japan | Long-term |

| Technological Obsolescence with EV & Autonomous Tech | -0.8% | Global | Medium to Long-term |

| Intense Price Competition | -0.7% | Global, especially Asia Pacific | Long-term |

| Complexity of Material Science & Engineering | -0.6% | Global | Long-term |

| Intellectual Property Protection & Counterfeiting | -0.5% | Global, particularly emerging markets | Ongoing |

Automotive Disc Brake Market - Updated Report Scope

This report provides a comprehensive analysis of the global automotive disc brake market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It covers the period from 2019 to 2033, with detailed forecasts up to 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 23.8 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Brembo S.p.A., ZF Friedrichshafen AG, Continental AG, Aisin Corporation, Mando Corporation, Hitachi Astemo, Ltd., Akebono Brake Industry Co., Ltd., Federal-Mogul Corporation, Nissin Kogyo Co., Ltd., Bosch GmbH, Meritor, Inc., Knorr-Bremse AG, Tenneco Inc., Wabco Holdings Inc., EBC Brakes, ADVICS Co., Ltd., Haldex AB, Carlisle Brake & Friction, Shandong Gold Phoenix Co., Ltd., StopTech |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive disc brake market is meticulously segmented to provide a granular understanding of its diverse components and evolving dynamics. This comprehensive segmentation allows for a detailed analysis of market performance across different vehicle types, brake technologies, material compositions, sales channels, and end-user applications. Each segment exhibits unique growth patterns and demand drivers, influenced by technological advancements, regulatory pressures, and consumer preferences.

Understanding these segments is crucial for manufacturers to tailor their product offerings, develop targeted marketing strategies, and optimize their supply chains. For instance, the demand for carbon ceramic disc brakes is primarily driven by the luxury and high-performance vehicle segments, while cast iron remains dominant in mass-market passenger cars. Similarly, the growth of the aftermarket segment underscores the importance of component durability and widespread distribution networks for replacement parts.

- By Vehicle Type: Passenger Cars (Hatchback, Sedan, SUV/MPV), Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)

- By Brake Type: Fixed Caliper Disc Brake, Floating Caliper Disc Brake

- By Disc Type: Ventilated Disc, Solid Disc, Drilled Disc, Slotted Disc

- By Material Type: Cast Iron, Composite Materials, Carbon Ceramic, Ceramic Matrix Composites, Aluminum Alloys

- By Sales Channel: Original Equipment Manufacturer (OEM), Aftermarket

- By End User: Passenger Vehicles, Commercial Vehicles

Regional Highlights

- Asia Pacific: This region is anticipated to dominate the automotive disc brake market, primarily due to the large-scale vehicle production and sales in countries like China, India, and Japan. Rapid industrialization, increasing disposable incomes, and the expansion of the automotive manufacturing sector are key drivers. The demand for both OEM and aftermarket components is consistently high, supported by a growing middle-class population and evolving vehicle ownership trends.

- Europe: Europe represents a mature but technologically advanced market for automotive disc brakes. Stringent safety regulations and a strong emphasis on vehicle performance and environmental standards drive the adoption of premium and advanced braking systems, including ceramic and lightweight composite disc brakes. Countries such as Germany, France, and the UK are at the forefront of innovation in brake technology, further supported by the presence of major automotive OEMs.

- North America: The North American market is characterized by a high demand for SUVs, pickup trucks, and luxury vehicles, which typically require robust and high-performance braking systems. The region benefits from significant aftermarket sales driven by a large existing vehicle parc and a strong culture of vehicle maintenance and customization. Innovation in smart braking systems and ADAS integration is a key trend in this region.

- Latin America: This region is experiencing steady growth in the automotive sector, leading to increased demand for disc brakes. Economic development and rising vehicle production in countries like Brazil and Mexico are contributing factors. The market is primarily driven by the need for cost-effective yet reliable braking solutions for mass-market vehicles, with a growing focus on safety features in newer models.

- Middle East and Africa (MEA): The MEA region is emerging as a growth market, particularly due to increasing infrastructure development, urbanization, and a rise in vehicle sales. Demand for commercial vehicle disc brakes is strong owing to construction and logistics activities. The market is influenced by imports and a gradual increase in local manufacturing capabilities, with a focus on durability and performance in diverse environmental conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Disc Brake Market.- Brembo S.p.A.

- ZF Friedrichshafen AG

- Continental AG

- Aisin Corporation

- Mando Corporation

- Hitachi Astemo, Ltd.

- Akebono Brake Industry Co., Ltd.

- Federal-Mogul Corporation

- Nissin Kogyo Co., Ltd.

- Bosch GmbH

- Meritor, Inc.

- Knorr-Bremse AG

- Tenneco Inc.

- Wabco Holdings Inc.

- EBC Brakes

- ADVICS Co., Ltd.

- Haldex AB

- Carlisle Brake & Friction

- Shandong Gold Phoenix Co., Ltd.

- StopTech

Frequently Asked Questions

Analyze common user questions about the Automotive Disc Brake market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary factors driving the growth of the Automotive Disc Brake Market?

The primary factors driving market growth include increasing global vehicle production, stringent automotive safety regulations, continuous technological advancements in brake materials and design, and the rising demand for high-performance and premium vehicles. The expansion of the aftermarket segment also consistently contributes to market demand.

How do electric vehicles (EVs) impact the demand for automotive disc brakes?

EVs present a dual impact. While regenerative braking reduces the frequency of friction brake use, leading to potentially longer replacement cycles, they still require robust disc brakes for emergency stopping and low-speed braking. This creates a specific demand for EV-optimized disc brakes that are corrosion-resistant, quieter, and durable despite less frequent activation.

What are the key technological trends shaping the future of disc brakes?

Key technological trends include the adoption of lightweight and high-performance materials like carbon ceramics and aluminum alloys, integration of smart braking systems with advanced sensors for predictive maintenance, development of environmentally friendly friction materials to reduce brake dust emissions, and enhanced noise, vibration, and harshness (NVH) optimization.

What challenges do manufacturers face in the Automotive Disc Brake Market?

Manufacturers face challenges such as stringent environmental regulations concerning brake dust emissions, the high manufacturing costs of advanced systems, intense price competition, volatility in raw material prices, and the need to constantly innovate to keep pace with evolving vehicle technologies like autonomous driving and brake-by-wire systems.

Which regions offer the most significant growth opportunities for disc brake manufacturers?

Asia Pacific is projected to offer the most significant growth opportunities due to its large and expanding automotive production bases in countries like China and India. Emerging markets in Latin America and Africa also present substantial potential for both OEM and aftermarket sales, driven by increasing vehicle ownership and economic development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted