Automotive Brake Disc Market

Automotive Brake Disc Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701703 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Brake Disc Market Size

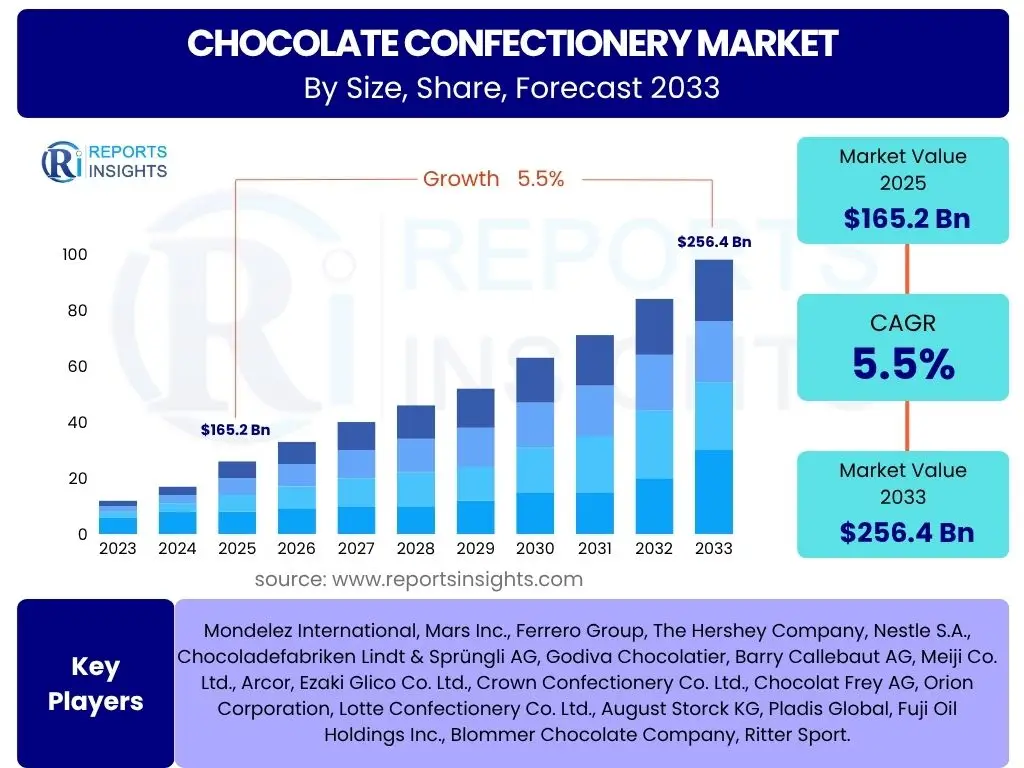

According to Reports Insights Consulting Pvt Ltd, The Automotive Brake Disc Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 24.5 Billion by the end of the forecast period in 2033.

Key Automotive Brake Disc Market Trends & Insights

The automotive brake disc market is experiencing a dynamic transformation driven by technological advancements and evolving consumer demands. Key user inquiries frequently center on the shift towards lightweight materials, the impact of electric vehicles on braking systems, and the integration of smart technologies. Manufacturers are increasingly focusing on developing brake discs that offer enhanced performance, durability, and reduced environmental impact, responding to stringent safety regulations and the growing demand for sustainable automotive solutions.

A significant trend involves the adoption of composite and carbon-ceramic materials, moving beyond traditional cast iron, particularly in premium and high-performance vehicles. This shift is driven by the need for weight reduction to improve fuel efficiency and, in the case of electric vehicles, to compensate for battery weight and enhance range. Furthermore, the market is witnessing a surge in demand for brake discs capable of handling the increased torque and unique braking characteristics of electric and hybrid vehicles, alongside developments in corrosion resistance and noise reduction.

Innovations also include the integration of sensors for real-time monitoring of brake wear and temperature, paving the way for predictive maintenance capabilities. The emphasis on global supply chain resilience and localized production is also gaining traction, mitigating risks associated with geopolitical events and trade fluctuations. These multifaceted trends collectively shape the trajectory of the automotive brake disc market, pointing towards a future of more efficient, sustainable, and intelligent braking solutions.

- Shift towards lightweight and advanced materials (e.g., carbon-ceramic, composites).

- Growing demand for brake discs optimized for Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs).

- Emphasis on enhanced durability, reduced noise, vibration, and harshness (NVH).

- Integration of smart features and sensors for condition monitoring and predictive maintenance.

- Increased focus on sustainable manufacturing processes and recyclable materials.

- Development of corrosion-resistant coatings for extended lifespan.

AI Impact Analysis on Automotive Brake Disc

Common user questions regarding AI's influence on the automotive brake disc sector highlight expectations for enhanced design processes, optimized manufacturing, and the emergence of more intelligent braking systems. Users are keenly interested in how Artificial Intelligence can streamline the product development lifecycle, from conceptualization to validation, and improve the efficiency and quality of production. The anticipation is that AI will unlock new possibilities for material innovation and performance optimization that traditional methods might overlook.

In the realm of manufacturing, AI algorithms are being deployed to monitor production lines for defects, optimize machine parameters for improved yield, and predict equipment failures, thereby minimizing downtime and waste. This translates into more cost-effective production of brake discs with consistent quality. Beyond the factory floor, AI's role extends to supply chain management, enabling better forecasting of demand and more efficient inventory management, crucial for a global industry with complex logistics.

Looking ahead, AI is integral to the development of advanced driver-assistance systems (ADAS) and autonomous vehicles, directly influencing braking system requirements. Predictive braking, adaptive brake control, and intelligent fault diagnosis are areas where AI-driven insights can significantly enhance vehicle safety and performance. This holistic integration across design, manufacturing, and operational stages positions AI as a transformative force, enabling the creation of safer, more efficient, and durable automotive brake discs.

- Optimized manufacturing processes through AI-powered predictive maintenance and quality control.

- Enhanced material design and simulation, leading to lighter and more durable brake discs.

- Development of smart braking systems with adaptive control and fault detection capabilities.

- Improved supply chain efficiency and demand forecasting using AI analytics.

- Personalized maintenance schedules based on real-time brake disc wear data.

Key Takeaways Automotive Brake Disc Market Size & Forecast

Analysis of user queries regarding key takeaways from the automotive brake disc market size and forecast consistently points to an interest in understanding the primary growth drivers, the enduring impact of new vehicle technologies, and the long-term sustainability of demand. Stakeholders are keen to discern how evolving regulations, shifting consumer preferences towards electric vehicles, and advancements in material science are collectively shaping the market's expansion and future trajectory. The overarching theme is one of cautious optimism, tempered by an awareness of the challenges presented by technological disruption and economic volatility.

The market's projected growth is underpinned by the consistent expansion of the global automotive industry, particularly in emerging economies, coupled with an increasing emphasis on vehicle safety and performance. While electric vehicles introduce a nuanced dynamic by potentially reducing brake wear due to regenerative braking, they also necessitate specialized brake components capable of handling different weight distributions and braking demands. This creates both a challenge and a significant opportunity for innovation within the sector.

Ultimately, the key insights emphasize that the automotive brake disc market is resilient and poised for substantial growth, driven by an intricate interplay of technological innovation, regulatory mandates, and global economic development. Success for market participants will hinge on their ability to adapt to changing vehicle paradigms, invest in advanced materials and manufacturing processes, and effectively navigate the complexities of a global supply chain to deliver high-performance, cost-effective, and sustainable braking solutions.

- Significant market growth anticipated, driven by global vehicle production and safety standards.

- Technological advancements in materials (e.g., composites, ceramics) are crucial for future growth.

- Electric vehicle adoption presents both opportunities for specialized discs and challenges for traditional brake wear.

- Aftermarket segment expected to remain robust due to vehicle parc expansion.

- Regional disparities in growth rates, with Asia Pacific leading the expansion.

Automotive Brake Disc Market Drivers Analysis

The automotive brake disc market's expansion is fundamentally propelled by several critical factors, including the consistent increase in global vehicle production, particularly in emerging economies. As more vehicles are manufactured and sold, the demand for both original equipment (OEM) brake discs and aftermarket replacements naturally escalates. This upward trend in vehicle parc directly correlates with a rising need for new and replacement braking components, forming a robust foundation for market growth.

Furthermore, stringent global automotive safety regulations are compelling manufacturers to integrate advanced and more reliable braking systems into their vehicles. Governments and regulatory bodies worldwide are consistently updating safety mandates to reduce road fatalities and accidents, necessitating continuous innovation in brake disc technology to meet higher performance and durability standards. This regulatory push not only drives the demand for high-quality brake discs but also encourages the adoption of technologically superior materials and designs, such as improved ventilation, lighter compositions, and enhanced friction characteristics.

The growing consumer preference for high-performance and luxury vehicles also acts as a significant market driver. These vehicle segments typically demand superior braking capabilities, often incorporating advanced brake disc materials like carbon-ceramic or composite discs, which offer enhanced stopping power, reduced fade, and greater longevity. The aftermarket, too, benefits from this trend as vehicle owners seek upgrades or high-quality replacements to maintain or improve their vehicle's braking performance. Together, these drivers create a strong positive momentum for the automotive brake disc market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production & Sales | +1.5% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Stringent Automotive Safety Regulations | +1.2% | Europe, North America, China | Medium-term (2025-2029) |

| Growing Demand for High-Performance Vehicles | +0.8% | North America, Europe, China | Medium-term (2025-2030) |

| Expansion of the Automotive Aftermarket | +1.0% | Global | Long-term (2025-2033) |

| Technological Advancements in Braking Systems | +0.9% | Global | Long-term (2025-2033) |

Automotive Brake Disc Market Restraints Analysis

Despite robust growth drivers, the automotive brake disc market faces several notable restraints that could temper its expansion. One significant challenge is the volatility and high cost of raw materials, particularly iron, steel, and advanced materials like carbon fiber or ceramics. Fluctuations in commodity prices directly impact manufacturing costs, leading to increased production expenses for brake disc manufacturers. This can, in turn, affect profit margins or necessitate higher selling prices, potentially slowing adoption in cost-sensitive segments of the market.

Another emerging restraint, particularly with the accelerating adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs), is the reduced wear on brake components due to regenerative braking systems. EVs often rely on their electric motors to slow the vehicle, converting kinetic energy back into electrical energy, thereby significantly reducing the frequency and intensity of mechanical braking. This extended lifespan of brake discs in EVs translates to a lower replacement demand in the aftermarket over time, posing a long-term challenge to market volume.

Furthermore, intense market competition, characterized by numerous established players and new entrants, often leads to price pressure. Manufacturers are constantly striving to offer competitive pricing while maintaining product quality and investing in research and development. This can squeeze profit margins, particularly for smaller players, and may lead to a focus on cost-cutting measures that could impact innovation or material quality. Economic slowdowns and geopolitical uncertainties also contribute to market restraint by affecting overall vehicle sales and consumer spending on automotive parts.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Raw Material Costs & Price Volatility | -0.7% | Global | Medium-term (2025-2029) |

| Reduced Brake Wear in Electric Vehicles (EVs) | -0.9% | Europe, North America, China | Long-term (2028-2033) |

| Intense Market Competition & Price Pressure | -0.6% | Global | Long-term (2025-2033) |

| Complex Manufacturing Processes | -0.4% | Global | Medium-term (2025-2030) |

| Economic Downturns Affecting Vehicle Sales | -0.5% | Global | Short-term (2025-2027) |

Automotive Brake Disc Market Opportunities Analysis

The automotive brake disc market presents significant opportunities for innovation and growth, primarily driven by the ongoing evolution of vehicle technology and shifting industry paradigms. A key area of opportunity lies in the development and broader adoption of innovative lightweight and high-performance materials. As vehicle manufacturers continue to prioritize weight reduction for improved fuel efficiency and reduced emissions, there is a strong demand for advanced materials such as carbon-ceramic composites, metal matrix composites, and advanced cast iron alloys. These materials not only reduce vehicle weight but also offer superior braking performance, heat dissipation, and extended lifespan, opening new avenues for product differentiation and premium market penetration.

The burgeoning electric vehicle (EV) segment represents another substantial opportunity. While regenerative braking might reduce mechanical wear, EVs often have higher curb weights due to battery packs, necessitating robust and highly efficient braking systems to manage kinetic energy effectively and provide reliable stopping power, especially in emergency situations. This creates a specific demand for brake discs optimized for EV characteristics, including enhanced corrosion resistance (due to less frequent use) and lower noise levels, presenting a niche for specialized product development and market leadership.

Furthermore, emerging markets, characterized by increasing disposable incomes and expanding middle-class populations, offer untapped potential for growth. As vehicle ownership rises in these regions, both OEM and aftermarket demand for brake discs will surge. The integration of smart braking technologies, such as those with integrated sensors for real-time monitoring and predictive maintenance, also offers a lucrative opportunity. These systems enhance safety, convenience, and efficiency, aligning with the broader trend of vehicle intelligence and connectivity. Lastly, a growing focus on sustainable and recyclable brake disc solutions, aligning with global environmental concerns, provides an opportunity for companies to innovate in eco-friendly materials and manufacturing processes, attracting environmentally conscious consumers and meeting future regulatory requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Innovative Lightweight & High-Performance Materials | +1.1% | Global | Long-term (2026-2033) |

| Growth in Electric Vehicle (EV) Segment & Specialized Braking Needs | +1.3% | Europe, North America, China | Long-term (2027-2033) |

| Emerging Markets with Rising Disposable Incomes | +0.9% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Integration of Smart Braking Technologies & Sensors | +0.7% | Global | Medium-term (2025-2030) |

| Focus on Sustainable & Recyclable Brake Disc Solutions | +0.6% | Europe, North America | Medium-term (2025-2029) |

Automotive Brake Disc Market Challenges Impact Analysis

The automotive brake disc market faces several formidable challenges that require strategic responses from industry participants. A primary challenge is the delicate balance between achieving superior performance and maintaining cost-effectiveness. Consumers and OEMs alike demand brake discs that offer excellent stopping power, durability, and low noise, but these advanced features often come with higher material and manufacturing costs. Companies must innovate to reduce production expenses without compromising quality, a task that becomes increasingly complex with the advent of specialized materials and intricate designs.

Another significant challenge involves managing complex global supply chains. The production of brake discs relies on a diverse network of raw material suppliers, component manufacturers, and logistics providers spread across various continents. Disruptions, such as geopolitical tensions, natural disasters, or pandemics, can severely impact the availability of critical materials and components, leading to production delays and increased costs. Ensuring supply chain resilience and diversification is paramount for maintaining consistent output and meeting market demand.

Furthermore, adapting to evolving vehicle architectures, particularly the rapid shift towards electric vehicles, poses a unique set of challenges. EVs have different weight distributions, higher torque, and the integration of regenerative braking, which alters the traditional stress and wear patterns on brake discs. Manufacturers must invest in research and development to design and produce brake discs specifically tailored to these new vehicle types, which may require new materials, coatings, or design methodologies. Lastly, environmental regulations concerning brake dust emissions are becoming increasingly stringent globally. Brake dust contains particulate matter harmful to human health and the environment, compelling manufacturers to develop new friction materials and braking systems that minimize these emissions, adding another layer of complexity to product development and compliance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Performance with Cost-Effectiveness | -0.8% | Global | Long-term (2025-2033) |

| Managing Complex Global Supply Chains | -0.7% | Global | Medium-term (2025-2028) |

| Adapting to Evolving Vehicle Architectures (e.g., EV-specific needs) | -0.9% | Europe, North America, China | Long-term (2027-2033) |

| Stringent Environmental Regulations (e.g., brake dust emissions) | -0.6% | Europe, North America | Medium-term (2025-2030) |

| Counterfeit Products in the Aftermarket | -0.5% | Emerging Markets | Long-term (2025-2033) |

Automotive Brake Disc Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Brake Disc Market, covering historical performance, current market dynamics, and future projections. It delves into the underlying factors driving market growth, identifies significant restraints, uncovers emerging opportunities, and addresses critical challenges. The scope includes detailed segmentation analysis by various parameters, extensive regional insights, and profiles of key industry players, offering a holistic view for strategic decision-making and investment planning in the evolving automotive braking landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 24.5 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Braking Systems Inc., Advanced Automotive Components Corp., Precision Brake Technologies Ltd., High-Performance Braking Solutions LLC, NextGen Auto Parts Group, Innovate Braking Systems, Superior Automotive Components, Dynamic Brake Solutions, Premier Automotive Parts, Elite Brake Systems Co., Future Mobility Brake Technologies, Universal Automotive Supplies, OptiBrake Innovations, Continental Brake Manufacturing, Asia Pacific Brake Co., European Braking Excellence, North American Brake Dynamics, Latin American Auto Components, Middle East & Africa Brake Solutions, Integrated Automotive Braking |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive brake disc market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This detailed segmentation allows for a comprehensive analysis of various product types, vehicle applications, and sales channels, revealing specific growth pockets and evolving consumer preferences. Understanding these segments is crucial for manufacturers to tailor their product offerings, for suppliers to optimize their raw material strategies, and for investors to identify promising areas for capital deployment.

The market is primarily categorized by disc type, material composition, vehicle application, and sales channel. Each segment possesses unique characteristics and growth trajectories influenced by factors such as cost-effectiveness, performance requirements, and regional regulatory frameworks. For instance, the demand for high-performance composite and carbon-ceramic brake discs is predominantly driven by premium and sports vehicle segments, while cast iron discs continue to dominate the mass-market and commercial vehicle segments due to their balance of cost and performance.

Further analysis within these segments considers the manufacturing processes involved, which range from traditional casting to more advanced forging and specialized techniques for complex materials. This level of detail helps to identify technological advancements and their impact on specific market niches. By dissecting the market into these core components, stakeholders can gain actionable insights into market penetration, competitive landscapes, and future innovation pathways.

- By Type: This segment distinguishes between different structural forms of brake discs, including traditional Cast Iron Brake Discs, which are widely used due to their durability and cost-effectiveness; Composite Brake Discs, offering a balance of performance and weight savings; and Carbon Ceramic Brake Discs, used in high-performance and luxury vehicles for their superior heat resistance and lighter weight. Other emerging types, such as aluminum-matrix composites, also form part of this segment.

- By Vehicle Type: Categorization based on the type of vehicle, primarily split into Passenger Vehicles (PV) and Commercial Vehicles (CV). Passenger vehicles include sedans, SUVs, and hatchbacks, while Commercial Vehicles are further sub-segmented into Light Commercial Vehicles (LCV) and Heavy Commercial Vehicles (HCV), each with distinct braking requirements based on load capacity and usage patterns.

- By Sales Channel: This segment differentiates between the Original Equipment Manufacturer (OEM) market, where brake discs are supplied directly to vehicle manufacturers for new vehicle assembly, and the Aftermarket, which caters to replacement parts for vehicles already in operation. The aftermarket is influenced by factors like vehicle parc, average vehicle age, and consumer preferences for genuine or third-party parts.

- By Material: Focuses on the primary materials used in brake disc manufacturing, including Grey Cast Iron (most common), High Carbon Cast Iron (enhanced thermal stability), Steel, Carbon-Carbon (lightweight, high-performance), and Ceramic Matrix Composites (CMCs) (superior heat and wear resistance).

- By Manufacturing Process: Analyzes the production methods employed, such as Casting (conventional and cost-effective), Forging (higher strength and durability), Stamping, and other advanced processes used for specialized materials and designs.

- By End-Use Vehicle: A more granular breakdown of vehicle types, including Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Buses, and Trucks, each presenting unique demands for brake disc size, material, and performance specifications.

Regional Highlights

The global automotive brake disc market exhibits distinct regional dynamics, influenced by factors such as vehicle production volumes, regulatory environments, technological adoption rates, and economic development. Each region contributes uniquely to the market's overall growth and innovation landscape, presenting varied opportunities and challenges for industry players. Understanding these regional nuances is crucial for developing effective market entry strategies and optimizing supply chain logistics.

- North America: Characterized by a strong demand for high-performance and luxury vehicles, alongside a growing adoption of electric vehicles. The region's stringent safety regulations drive continuous innovation in braking technology. The aftermarket segment is robust, fueled by a large vehicle parc and consumer preference for quality replacement parts.

- Europe: A pioneer in automotive safety and environmental regulations, Europe is a key market for advanced brake disc technologies, including lightweight and low-emission solutions. The shift towards electric and hybrid vehicles is rapid, creating specific demands for corrosion-resistant and quiet brake discs. Strong OEM presence and a mature aftermarket contribute significantly.

- Asia Pacific (APAC): The largest and fastest-growing market, primarily driven by high vehicle production and sales in countries like China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and expanding middle-class populations are boosting both OEM and aftermarket demand. The region is also a hub for manufacturing and material innovation, though cost-effectiveness remains a key consideration.

- Latin America: Experiences steady growth in vehicle production and sales, leading to increased demand for brake discs. Economic stability and expanding automotive manufacturing bases in countries like Brazil and Mexico drive market expansion, with a focus on cost-effective and durable solutions for diverse vehicle types.

- Middle East and Africa (MEA): Emerging markets with potential for growth, particularly in the aftermarket segment as vehicle parc expands. Investment in infrastructure and increasing economic diversification are supporting automotive sector growth, though specific demand drivers vary by country, with a growing interest in heavy-duty commercial vehicle brakes in some sub-regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Brake Disc Market.- Global Braking Systems Inc.

- Advanced Automotive Components Corp.

- Precision Brake Technologies Ltd.

- High-Performance Braking Solutions LLC

- NextGen Auto Parts Group

- Innovate Braking Systems

- Superior Automotive Components

- Dynamic Brake Solutions

- Premier Automotive Parts

- Elite Brake Systems Co.

- Future Mobility Brake Technologies

- Universal Automotive Supplies

- OptiBrake Innovations

- Continental Brake Manufacturing

- Asia Pacific Brake Co.

- European Braking Excellence

- North American Brake Dynamics

- Latin American Auto Components

- Middle East & Africa Brake Solutions

- Integrated Automotive Braking

Frequently Asked Questions

Analyze common user questions about the Automotive Brake Disc market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary materials used in automotive brake discs?

The primary materials include grey cast iron, high carbon cast iron, steel, and advanced materials such as carbon-ceramic composites and metal matrix composites. The choice depends on performance requirements, cost, and vehicle type.

How do electric vehicles (EVs) impact the demand for brake discs?

EVs reduce the mechanical wear on brake discs due to regenerative braking systems, potentially lowering aftermarket replacement rates. However, their higher weight necessitates robust and corrosion-resistant brake discs designed for specific EV braking characteristics.

What are the latest innovations in automotive brake disc technology?

Latest innovations include lightweight material development (e.g., carbon-ceramic, composites), advanced coatings for corrosion and wear resistance, integration of sensors for predictive maintenance, and designs optimized for quieter operation and reduced brake dust emissions.

What is the projected growth rate for the Automotive Brake Disc Market?

The Automotive Brake Disc Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing vehicle production, stringent safety regulations, and technological advancements.

What is the difference between OEM and aftermarket brake discs?

OEM (Original Equipment Manufacturer) brake discs are supplied directly to vehicle manufacturers for installation in new vehicles. Aftermarket brake discs are replacements sold for vehicles already in use, provided by various manufacturers, including OEM suppliers and independent companies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted